Original | Odaily Planet Daily (@OdailyChina)

Author | Asher (@Asher_ 0210)

"The big crash" has happened again.

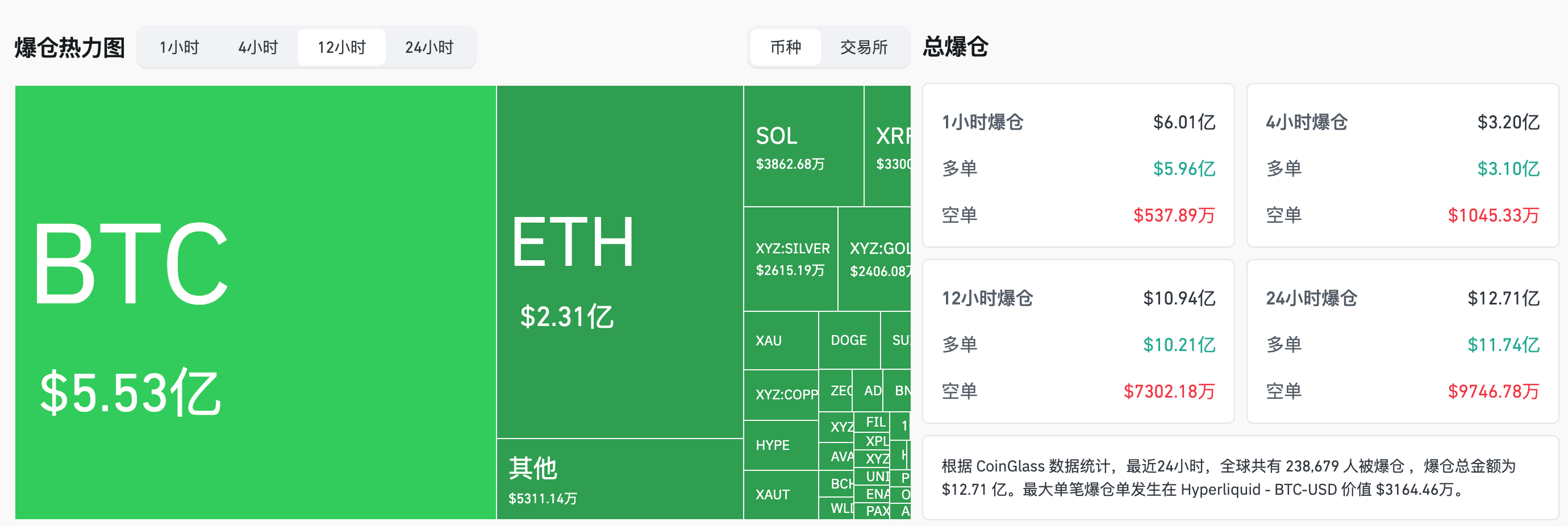

OKX market data shows that from last night to this morning Beijing time, BTC quickly fell from around $88,000, once dropping below $81,200, with a 24-hour decline of over 7%; ETH fell from $2,940 to a low of $2,690, with a 24-hour decline of nearly 10%; SOL dropped from $123 to around $112, with a 24-hour decline of over 8%. Coinglass data shows that in the past 12 hours, the market saw liquidations of $1.094 billion, with long positions accounting for as much as $1.021 billion; the number of liquidated traders in 24 hours was nearly 240,000.

This decline was not triggered by a single negative factor, but rather the result of multiple factors converging at the same time.

Middle East tensions suddenly escalate, geopolitical risks reemerge in the market

The sudden escalation of geopolitical risk was one of the earliest important background factors factored into the market decline last night.

Latest news indicates that the U.S. aircraft carrier USS Abraham Lincoln and its strike group have entered a state of "total blackout" with communications中断. This move is usually seen as a standard operating procedure before major military actions, leading the market to speculate that actions related to Iran are entering a highly sensitive phase.

At the same time, statements from Iran have also明显 turned to a备战 posture. Iran's First Vice President Aref, speaking on the regional situation, stated that Iran has maintained a state of readiness since the current administration took office, will not initiate war, but if conflict is provoked, it will defend itself with a firm stance, emphasizing that "the outcome of the war will not be decided by the enemy." He pointed out that it is currently necessary to prepare for a state of war.

Although the situation has not yet evolved into substantial conflict, this state of "high opacity, unverifiability, and unpredictability" itself is enough to influence market behavior. Against a backdrop of already tight liquidity and receding risk appetite, geopolitical uncertainty was quickly priced in, prompting funds to倾向于 reduce directional exposure rather than continue betting on high-volatility assets.

FOMC "Hawkish Hold", liquidity expectations repriced

decline in crypto行情 still cannot绕开 the Federal Reserve.

At the January FOMC meeting, the Fed kept the benchmark interest rate unchanged in the range of 3.50% to 3.75%, and emphasized in its statement that the unemployment rate has stabilized while inflation remains at a relatively high level. The stance itself did not significantly exceed market expectations, but it emotionally completed an "expectation收官"—the market's previously held vague幻想 of short-term rate cuts, or even a policy pivot, were formally compressed or even cleared.

For risk assets, such moments often do not appear in the form of "new negatives," but rather as a realization that "positive factors can no longer be further透支." Since 2025, Bitcoin has seen pullbacks多次 after FOMC meetings, which is a repeated演绎 of this mechanism: it's not that policy suddenly turned hawkish, but that the market had to admit that liquidity would not arrive as early as expected.

When positions have already built up and leverage is high, this kind of "靴子落地" confirmation is itself enough to trigger risk release—it is not the first push that knocks down the dominoes, but rather what causes all the already precarious structures to simultaneously lose support.

It's not just the crypto圈 falling; stocks, precious metals also "turn" simultaneously

More alarmingly, this decline is not a "solo performance" by the crypto market.

In U.S. stocks, the decline in major indices became an important signal of weakening risk appetite. The Nasdaq 100 index fell about 1.6%, the S&P 500 index dropped about 0.75%, and the Dow Jones Industrial Average also declined about 0.2%. The three major indices were generally under pressure, with the technology sector performing particularly weakly, dragging down overall market risk appetite.

At the same time, precious metals, which are traditionally seen as "safe-haven assets," also experienced剧烈波动. After a recent strong rally, gold prices saw a sharp short-term pullback last night, with significant profit-taking appearing in the market; silver also retreated rapidly from its highs, with a notable decline. This indicates that funds are not simply switching from risk assets to safe-haven assets, but are rather reducing risk exposure overall in a high-volatility environment.

When stocks fall, crypto assets are under pressure, and precious metals also pull back simultaneously, the signal sent by the market is quite clear. Funds are simultaneously reducing exposure across multiple asset classes, with overall risk appetite contracting rapidly.

In such an environment, Bitcoin naturally cannot remain unscathed. It is neither truly regarded by the market as a safe-haven asset, nor, due to its own high volatility, does it often become one of the first to be sold when sentiment turns risk-averse.

Sustained ETF outflows significantly reduce the crypto market's capacity to absorb selling

Changes in the capital flow provided the final piece of the puzzle for this decline.

Looking at Bitcoin spot ETF data, funds are continuously withdrawing. Data shows that in the past week alone, BTC spot ETFs saw sustained net outflows, with multiple days recording outflows of over $100 million per day, with cumulative net outflows already exceeding $1 billion.

More importantly, the withdrawal of ETF funds is not a one-time宣泄, but rather a continuous, multi-day, trend-driven reduction of positions. This means that institutional funds are not choosing to "buy the dip and support the bottom" during the pullback, but are instead more inclined to reduce overall risk exposure and wait for clearer macro and market signals.

In such a capital environment, the market does not have a "buffer." When prices fall, ETFs do not provide sustained buying power; the market relies more on existing funds to消化 selling pressure on their own. Once key price levels are broken, selling behavior quickly dominates, while buying interest明显 lags, forcing prices to rapidly探 lower to find a new balance.

Not a black swan, but a concentrated release of "forced de-risking"

The essence of BTC's current decline is not triggered by a single突发 negative alone, but is the result of the market repricing risk assets overall under the叠加 of multiple risk factors. Geopolitical uncertainty intensified, macro liquidity expectations were修正, and against the backdrop of持续 net outflows from ETFs, the crypto market lacked stable structural support, ultimately triggering the market's主动 "braking" behavior.

When long-term funds and passive buying are absent, the market often completes the first stage of risk clearing by having prices break through key trend levels, forcing trend-following strategies and leveraged funds to exit被动. In this process, Bitcoin broke below the highly watched 100-week moving average (around $85,000), a level that has acted as a "safety net"多次 during adjustments since last year and is also the default defense line for many trend models and leveraged positions.

From the result, the market has now completed the first round of rapid deleveraging and emotional clearing, but true stabilization still relies on two conditions: first, whether key technical levels can be recaptured and held firmly, and second, whether risk capital is willing to return to the market to participate in pricing. Before that, high volatility and low confidence may still be the阶段性主旋律.