Original Author: Xu Chao

Original Source: Wall Street News

One quarter's profit of 24.7 billion yuan, a half-year profit approaching 57 billion yuan — this chip company, once a perennial loss-maker mockingly called a "cash incinerator" by the market, is staging the most astonishing profit turnaround in China's tech history.

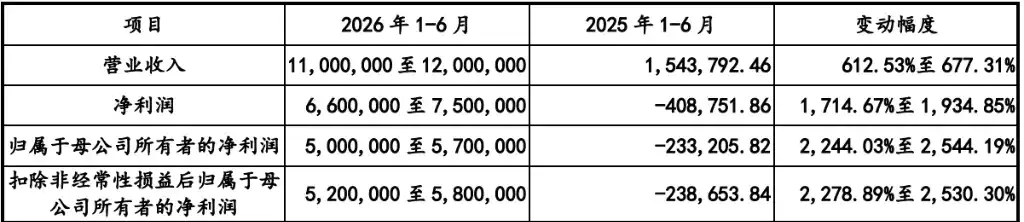

On May 17th, ChangXin Technology updated its IPO prospectus on the STAR Market. A set of numbers shocked the entire capital market: In the first quarter of 2026, the company's revenue reached 50.8 billion yuan, skyrocketing 719% year-over-year; net profit attributable to the parent company after non-recurring gains/losses was 26.34 billion yuan, soaring 1993.41% year-over-year; the company expects revenue for the first half of this year to be between 110 and 120 billion yuan, a year-over-year increase of 612.53% to 677.31%; net profit attributable to the parent company is projected to be between 50 and 57 billion yuan, up 2244% to 2544% year-over-year.

Just how extraordinary is this report card? A horizontal comparison makes it clear.

Among non-financial A-share companies, only three—PetroChina, China Mobile, and CNOOC—had annual net profits exceeding 100 billion yuan in 2025; Kweichow Moutai was 80+ billion yuan; CATL was 70+ billion yuan; the sixth-ranked CHN Energy Group was just 52.9 billion yuan. ChangXin Technology, with its net profit attributable to the parent company for just half a year, has already reached a level comparable to CHN Energy Group, placing it among the top six non-financial A-share companies.

Even more astonishing is that if this data is extrapolated linearly, ChangXin Technology's net profit for 2026 is expected to potentially exceed 100 billion yuan. Thus, this chip company's annual profitability is catching up to the profit scale of those former oil giants.

However, just over a year ago, this company was a veritable "cash incinerator."

The Abyss of Past Losses: Burning Through 36.6 Billion in Three Years

Looking at ChangXin Technology's historical public financial data: a loss of 16.34 billion yuan in 2023, a loss of 7.145 billion yuan in 2024, and cumulative losses reaching 36.65 billion yuan as of December 31, 2025. Over nearly a decade, ChangXin Technology poured almost every cent it raised into the bottomless pit of chip manufacturing.

Now, how did this "cash incinerator" transform into a "money printing machine" earning nearly 400 million yuan per day in less than half a year?

The answer lies in two key phrases: AI and the chip shortage.

The Epic Super Cycle: AI is "Devouring" Memory

The world is experiencing an epic-level memory chip cycle.

The root of this super boom cycle is the "violent consumption" of memory by AI large models.

Every model inference is essentially a massive data grab between GPUs and memory. The demand for DRAM from a single AI server is 8 to 10 times that of a traditional server. As global cloud providers and AI computing infrastructure construction continues to accelerate, DRAM demand is experiencing structural explosion.

Simultaneously, the three major camps—Samsung, SK Hynix, and Micron—are shifting a significant portion of their advanced capacity to higher-margin HBM (High Bandwidth Memory), severely constricting production line resources for general-purpose chips like DDR4 and DDR5.

This extreme supply-demand mismatch has driven DRAM prices to historic highs.

TrendForce data shows that DRAM contract prices surged 93% to 98% quarter-over-quarter in Q1 2026; Q2 is still expected to maintain gains of 58% to 63%. Data from the National Development and Reform Commission's Price Monitoring Center shows that as of January 2026, mainstream DRAM product prices had hit their highest levels since 2016. All 2026 production capacity from Samsung, SK Hynix, and Micron has reportedly been sold out.

Industry institutions predict this memory upcycle could last until 2030, with a supply gap exceeding 20%.

Optimal Volume & Price: ChangXin Technology Hit the Node

In this epic memory super cycle, ChangXin Technology not only caught the tailwind but also maximized the realization of industry dividends through its years of strategic positioning.

Founded in 2016, ChangXin Technology is currently the only true IDM enterprise in mainland China achieving large-scale DRAM production—meaning it covers the entire industrial chain: design, manufacturing, and packaging/testing. The company has three 12-inch wafer fabs in Beijing and Hefei, with capacity utilization climbing to 94.63% in 2025.

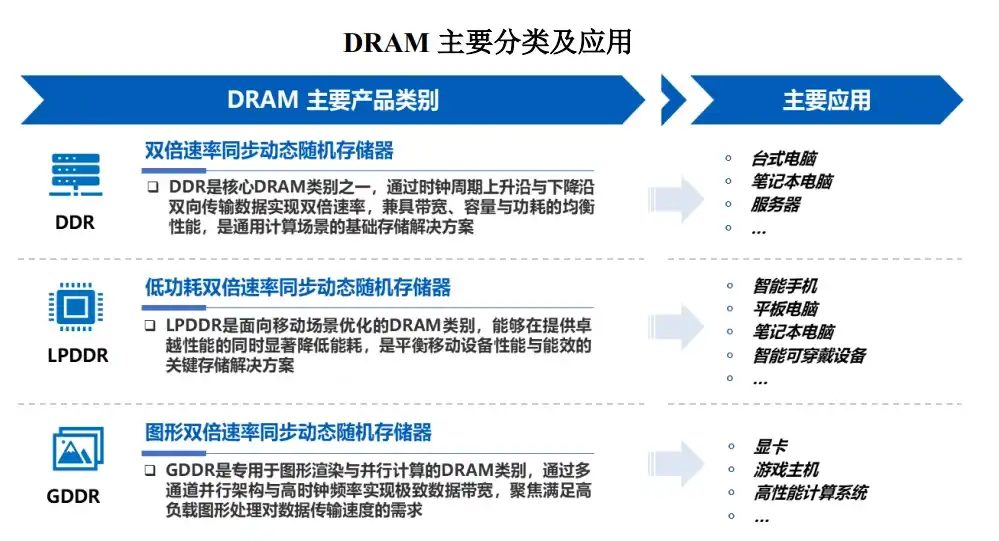

On the product front, ChangXin Technology has completed a full upgrade from DDR4 to DDR5, and from LPDDR4X to LPDDR5/5X. The continuous promotion of high-end products directly amplified the profit elasticity brought by price increases.

In market share, according to Omdia data, based on DRAM sales in Q4 2025, ChangXin Technology's global market share had increased to 7.67%, ranking fourth globally and first in China. From 3.97% in Q2 2025 to 7.67% in Q4 2025, its market share nearly doubled in just half a year.

The result is: simultaneous volume growth and price increases, leading to an explosive profit surge.

Zhu Yiming's Decade-Long Gamble: No Salary Until Profitable

ChangXin Technology's journey to this point is inseparable from one key figure: Chairman Zhu Yiming.

As the founder of Gigadevice, Zhu Yiming made a decision in 2016 that the industry couldn't comprehend — he abandoned the stable path of a chip design company and staked everything on establishing ChangXin Technology in Hefei, betting heavily on domestic DRAM.

How difficult was this path? DRAM is the most fiercely competitive chip category globally, with Samsung, SK Hynix, and Micron collectively holding over 90% of the global market share, leaving almost no room for new entrants. Even more critical, DRAM manufacturing is extremely capital-intensive, with 12-inch wafer fabs requiring investments of hundreds of millions or billions of dollars. For a long time, ChangXin was essentially using money to "fill a hole."

Zhu Yiming made a military-style pledge back then: He would not receive a single yuan in salary or bonus until ChangXin became profitable.

That promise has been significantly over-fulfilled.

Valuation Debate: One Trillion or Two Trillion?

With such explosive performance, what is ChangXin Technology really worth?

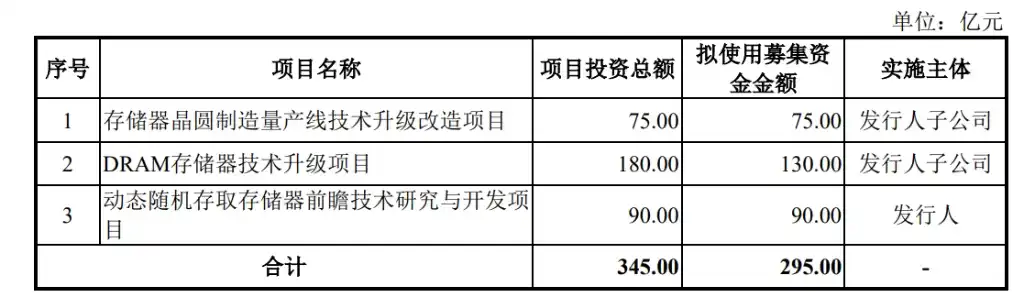

According to the current IPO plan, ChangXin Technology plans to raise 29.5 billion yuan on the STAR Market, with a post-issue share capital of no less than 10%, implying a valuation of approximately 295 billion yuan. This planned IPO fundraising of 29.5 billion yuan would also be the highest in STAR Market history (SMIC planned to raise 20.7 billion yuan in 2020, but actually raised over 53.2 billion).

Current market valuation expectations for ChangXin Technology are around 1 trillion yuan in the short term and 2 trillion yuan in the long term. Based on the projected 100 billion yuan net profit attributable to the parent company by the end of 2026, using relatively conservative valuation estimates, a market capitalization breakthrough of one trillion yuan also has ample support.

Of course, controversy also exists.

The cyclicality of DRAM is an unavoidable historical pattern — ChangXin Technology was still suffering massive losses last year, is exploding with profits this year, and once the super cycle ends and prices fall, its performance could contract significantly at any time.

However, some argue that the core logic of this cycle has shifted from "short-term peaks in consumer electronics" to "structural demand from AI," making its sustainability far exceed that of past cycles. Additionally, the scarcity premium of ChangXin Technology as the domestic DRAM "lone champion" is a factor that cannot be ignored in pricing.

A Textbook Financial Turnaround

From cumulative losses of 36.6 billion yuan to raking in 50 billion yuan in half a year, ChangXin Technology has completed a textbook financial turnaround in less than half a year.

But behind this turnaround lies capital investment, technological accumulation, and strategic persistence maintained day after day for ten years. What Zhu Yiming and the ChangXin team bet on was not just an industry cycle, but also the industrial imperative of China securing a place on the global DRAM map.

The report card of earning nearly 400 million yuan per day is a gift from the tailwind and also the reward for a decade of grinding.

When ChangXin Technology finally rings the bell on its IPO day, the answer it gives to the capital market will perhaps be more convincing than any analyst report.