Autor: KarenZ, Foresight News

Título original: Strategy se enfrenta a MSCI: La defensa definitiva de DAT

La batalla que determinará el desarrollo de la industria de las empresas de tesorería de activos digitales (DAT) continúa en desarrollo.

En octubre, la empresa global de compilación de índices MSCI lanzó una propuesta para excluir de sus índices globales de mercados invertibles a las empresas cuyas tenencias de activos digitales representen el 50% o más de sus activos totales. Esta medida amenaza directamente la posición en el mercado de empresas de tesorería de activos digitales como Strategy, e incluso podría reescribir los flujos de capital de toda la industria.

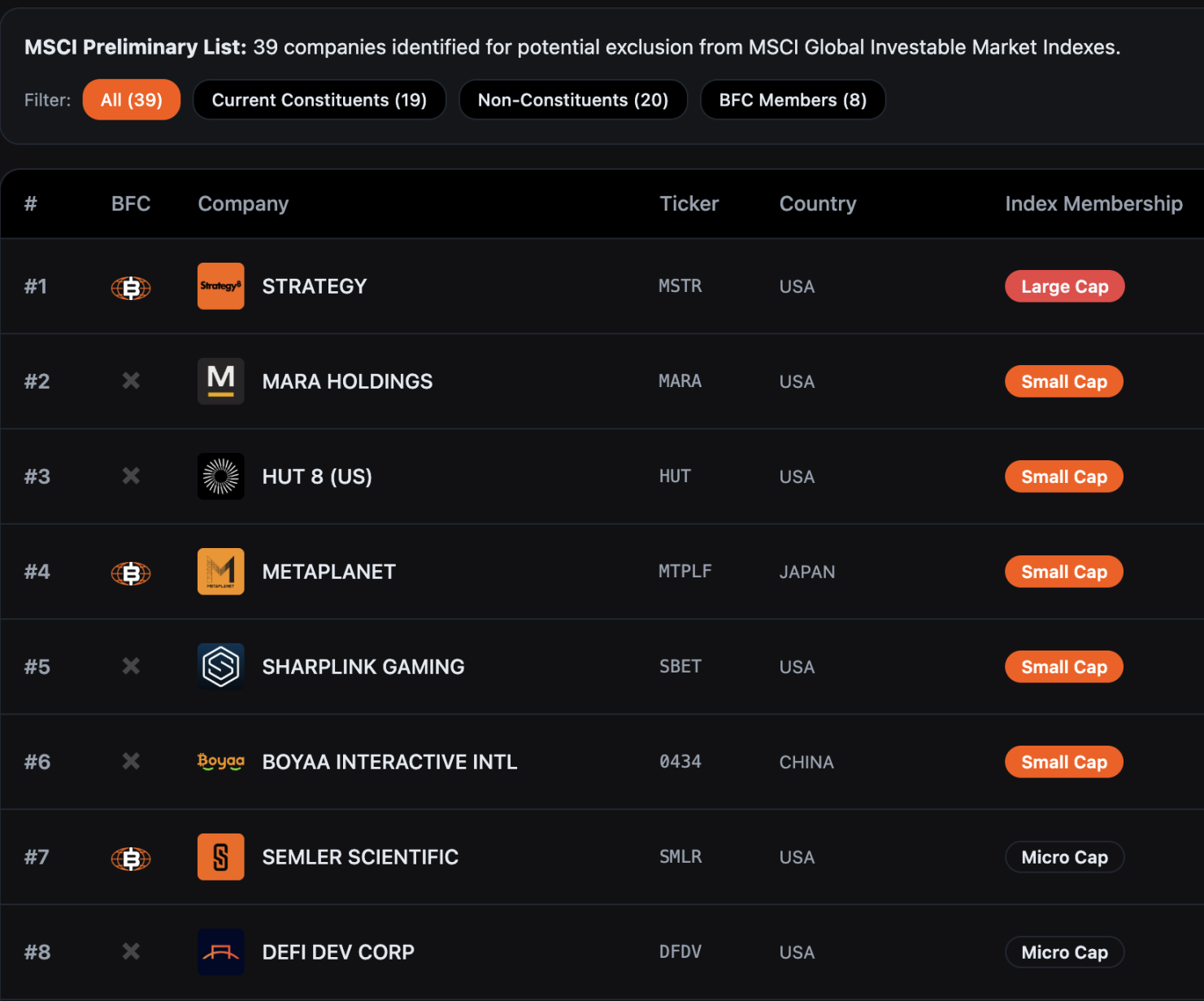

Según datos compilados por Bitcoin for Corporations, 39 empresas podrían ser excluidas del índice MSCI Global Investable Market. Analistas de JPMorgan advirtieron previamente que solo la exclusión de Strategy podría provocar una salida de casi $2.8 mil millones en capital pasivo. Si otros proveedores de índices replicaran esta regla, las salidas podrían alcanzar los $8.8 mil millones.

Actualmente, el período de consulta de MSCI sobre esta propuesta se extenderá hasta el 31 de diciembre de 2025, y se espera que la conclusión final se anuncie antes del 15 de enero de 2026. Cualquier ajuste se implementaría formalmente en la revisión de índices de febrero de 2026.

Frente a esta situación urgente, Strategy envió el 10 de diciembre una enérgica carta pública de 12 páginas al Comité de Índices de Acciones de MSCI, firmada conjuntamente por el Presidente Ejecutivo y Fundador, Michael Saylor, y el Presidente y CEO, Phong Le, expresando claramente su firme oposición a la propuesta. La carta declara: "Esta propuesta es gravemente engañosa y tendrá consecuencias destructivas de gran alcance para los intereses de los inversores globales y el desarrollo de la industria de activos digitales. Solicitamos enfáticamente que MSCI retire por completo este plan".

Los cuatro argumentos centrales de la defensa de Strategy

Los activos digitales son una tecnología fundamental revolucionaria que remodela el sistema financiero

Strategy considera que la propuesta de MSCI subestima el valor estratégico de Bitcoin y otros activos digitales. Desde que Satoshi Nakamoto lanzó Bitcoin hace 16 años, este activo digital ha crecido gradualmente hasta convertirse en un componente clave de la economía global, con una capitalización de mercado actual de aproximadamente $1.85 billones.

Para Strategy, los activos digitales no son meramente instrumentos financieros, sino una innovación tecnológica fundamental capaz de remodelar el sistema financiero global: las empresas que invierten en infraestructura relacionada con Bitcoin están construyendo un nuevo ecosistema financiero, al igual que lo hicieron las empresas líderes que se centraron profundamente en una sola tecnología emergente en el pasado.

Al igual que Standard Oil en el siglo XIX profundizó en la extracción de petróleo y AT&T en el siglo XX construyó masivamente redes telefónicas, estas empresas, mediante inversiones前瞻ivas en infraestructura central, sentaron una base sólida para las posteriores transformaciones económicas, convirtiéndose finalmente en referentes de la industria. Strategy argumenta que las empresas que se enfocan en activos digitales hoy están repitiendo esta trayectoria de "fundadores tecnológicos" y no deberían ser simplemente descalificadas por reglas indexadas tradicionales.

Las DAT son empresas operativas, no fondos de inversión pasivos

Este es el argumento central de la defensa de Strategy: las empresas de tesorería de activos digitales (DAT) son empresas operativas con un modelo comercial completo, no fondos de inversión que simplemente mantienen Bitcoin de forma pasiva. Aunque Strategy posee actualmente más de 600,000 bitcoins, su valor central no depende de la volatilidad del precio de Bitcoin, sino que se genera a través del diseño y lanzamiento de herramientas únicas de "crédito digital" que crean retornos sostenibles para los accionistas.

En concreto, las herramientas de "crédito digital" emitidas por Strategy incluyen varios tipos, como acciones preferentes con tasa de dividendo fija, tasa flotante, diferentes niveles de prioridad y cláusulas de protección crediticia. La empresa recauda fondos vendiendo estas herramientas y luego los utiliza para adquirir más Bitcoin. Mientras el retorno de la inversión a largo plazo en Bitcoin supere el costo de financiamiento en dólares de Strategy, se pueden generar ganancias estables para accionistas y clientes. Strategy enfatiza que este modelo de "operación activa + apreciación de activos" es fundamentalmente diferente de la lógica de gestión pasiva de los fondos de inversión tradicionales o ETFs, y por lo tanto debería ser considerado una empresa operativa normal.

Además, Strategy cuestiona en la carta: ¿Por qué los gigantes petroleros, los fideicomisos de inversión en bienes raíces (REITs), las empresas madereras, etc., pueden mantener concentraciones altas de una sola clase de activo sin ser clasificados como fondos de inversión y excluidos de los índices? Establecer restricciones especiales solo para las empresas de activos digitales claramente no cumple con el principio de equidad sectorial.

El umbral del 50% de activos digitales es arbitrario, discriminatorio e impráctico

Strategy señala que la propuesta de MSCI utiliza un estándar discriminatorio. Muchas grandes empresas de industrias tradicionales también mantienen altas concentraciones de una sola clase de activo en sus carteras, incluyendo compañías de petróleo y gas, REITs, empresas madereras y de infraestructura eléctrica. Sin embargo, MSCI solo ha establecido un estándar de exclusión especial para las empresas de activos digitales, lo que constituye un trato claramente injusto.

Desde la perspectiva de la viabilidad de implementación, la propuesta también presenta serios problemas. Debido a la alta volatilidad de los precios de los activos digitales, una misma empresa podría entrar y salir repetidamente del índice MSCI en cuestión de días debido a cambios en el valor de sus activos, creando caos en el mercado. Además, las diferencias entre los principios contables (el tratamiento de los activos digitales difiere entre los US GAAP y los estándares internacionales IFRS) resultarán en un tratamiento diferenciado para empresas con el mismo modelo de negocio dependiendo de su lugar de registro.

Infringe el principio de neutralidad del índice, inyectando sesgo político

Strategy argumenta que la propuesta de MSCI es, en esencia, un juicio de valor sobre una clase de activo, lo que infringe el principio básico de que los proveedores de índices deben mantenerse neutrales. MSCI afirma ante el mercado y los reguladores que sus índices brindan una cobertura "exhaustiva", destinada a reflejar la "evolución del mercado bursátil subyacente", y no debería "juzgar la bondad o conveniencia de ningún mercado, empresa, estrategia o inversión".

Al excluir selectivamente a las empresas de activos digitales, MSCI está efectivamente haciendo un juicio político en nombre del mercado, que es precisamente lo que los proveedores de índices deberían evitar.

Entra en conflicto con la estrategia estadounidense sobre activos digitales

Strategy enfatiza especialmente que esta propuesta entra en conflicto con los objetivos estratégicos de la administración Trump de avanzar en el liderazgo en activos digitales. La administración Trump firmó una orden ejecutiva en su primera semana para promover el crecimiento de las tecnologías financieras digitales y estableció una reserva estratégica de Bitcoin, con el objetivo de posicionar a Estados Unidos como líder global en el ámbito de los activos digitales.

Sin embargo, si la propuesta de MSCI se implementa, impediría directamente que fondos a largo plazo como las pensiones estadounidenses y los planes 401(k) inviertan en empresas de activos digitales, provocando una salida de decenas de miles de millones de dólares de capital de la industria. Esto no solo obstaculizaría el desarrollo de empresas innovadoras estadounidenses de activos digitales, sino que también podría debilitar la competitividad de Estados Unidos en este campo estratégico, yendo en contra de la dirección política establecida por el gobierno.

Strategy citó estimaciones de analistas que indican que solo Strategy podría enfrentar una liquidación pasiva de acciones de hasta $2.8 mil millones debido a la propuesta de MSCI. Esto no solo perjudica a Strategy itself, sino que también tendría un efecto escalofriante en todo el ecosistema de activos digitales, por ejemplo, podría forzar a las empresas mineras de Bitcoin a vender activos prematuramente para ajustar su estructura de activos, distorsionando así las relaciones normales de oferta y demanda del mercado de activos digitales.

La demanda final de Strategy

Strategy plantea dos demandas principales en su carta pública:

Primero, que MSCI retire completamente la propuesta de exclusión, permitiendo que el mercado pruebe el valor de las empresas de tesorería de activos digitales (DAT) mediante la libre competencia, para que los índices reflejen de manera neutral y fiel las tendencias de desarrollo de la próxima generación de tecnología financiera.

Segundo, si MSCI insiste en "tratar de manera especial" a las empresas de activos digitales, debe ampliar el alcance de la consulta sectorial, extender el tiempo de consulta y proporcionar una justificación lógica más completa para explicar la racionalidad de la regla.

Strategy no está luchando sola

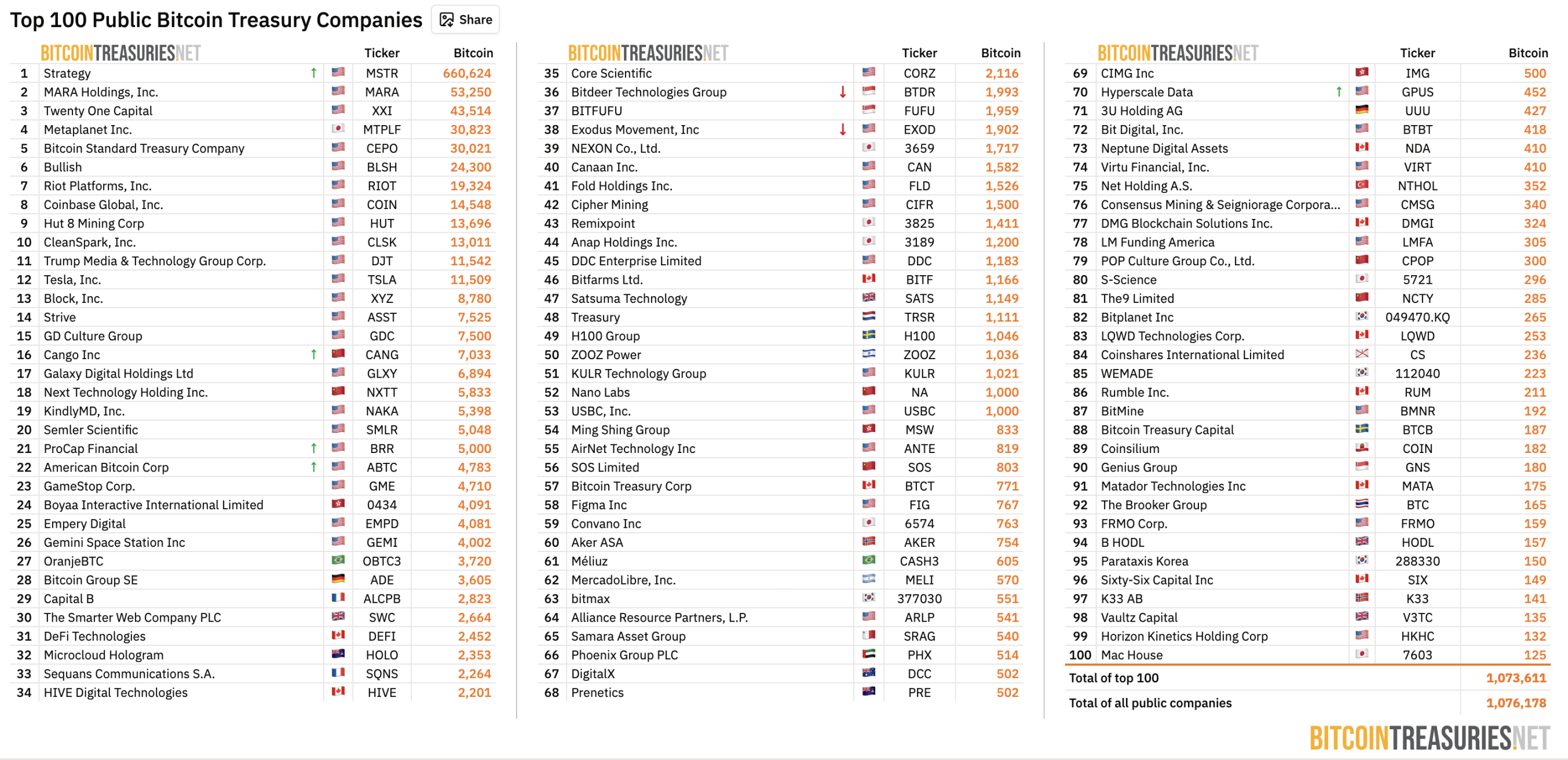

Strategy no está luchando sola. Según datos de BitcoinTreasuries.NET, al 11 de diciembre, 208 empresas que cotizan en bolsa a nivel mundial poseen más de 1.07 millones de bitcoins, superando el 5% del suministro total de Bitcoin, con un valor actual de aproximadamente $100 mil millones.

Fuente: BitcoinTreasuries.NET

Estas empresas de tesorería de activos digitales se han convertido en un puente crucial para la adopción institucional de criptomonedas, proporcionando exposición indirecta y合规 a instituciones financieras tradicionales como fondos de pensiones y fondos de dotación.

Anteriormente, Strive, una empresa que cotiza en bolsa y posee Bitcoin, sugirió que MSCI debería devolver la "opción" sobre las empresas de activos digitales al mercado. Una solución simple y directa sería crear versiones de los índices existentes "excluyendo empresas de tesorería de activos digitales", por ejemplo, el índice MSCI USA ex Digital Asset Treasuries y el índice MSCI ACWI ex Digital Asset Treasuries. Mediante un mecanismo de filtrado transparente, los inversores podrían elegir su benchmark de seguimiento de forma autónoma, preservando así la integridad del índice y satisfaciendo las necesidades de diferentes inversores.

Además, la organización del sector Bitcoin for Corporations ha iniciado una iniciativa conjunta, instando a MSCI a retirar esta propuesta sobre activos digitales, argumentando que la clasificación debería basarse en el modelo comercial real, el desempeño financiero y las características operativas de la empresa, y no simplemente en un límite basado en el porcentaje de activos. Según se muestra en el sitio web de la organización, actualmente 309 empresas o inversores han firmado la carta conjunta. Los firmantes, además de Strategy, incluyen altos ejecutivos de empresas conocidas en el sector como Strive, BitGo, Redwood Digital Group, 21MIL, Btc inc, DeFi Development Corp, así como numerosos desarrolladores e inversores individuales.

Resumen

Este enfrentamiento entre Strategy y MSCI es, en esencia, un debate fundamental sobre "cómo se integran las nuevas innovaciones financieras en el sistema tradicional". Las empresas de tesorería de activos digitales (DAT), como "híbridos" entre el mundo financiero tradicional y el de las criptomonedas, no son empresas puramente tecnológicas ni simples fondos de inversión, sino un nuevo modelo comercial construido sobre la base de los activos digitales.

La propuesta de MSCI intenta utilizar el estándar del "50% de participación de activos" para clasificar estas entidades complejas como "fondos de inversión" y excluirlas de los índices; mientras que Strategy insiste en que este tratamiento simplificado es un grave malentendido de su naturaleza comercial y una desviación del principio de neutralidad del índice. A medida que se acerca la fecha de decisión del 15 de enero de 2026, el resultado de esta batalla no solo determinará la "elegibilidad" para ingresar al índice de varias empresas que cotizan en bolsa y poseen Bitcoin, sino que también delineará los cruciales "límites de supervivencia" para la futura posición de la industria de activos digitales dentro del sistema financiero tradicional global.

Twitter:https://twitter.com/BitpushNewsCN

Grupo de Telegram de Bitpush:https://t.me/BitPushCommunity

Suscripción a Telegram de Bitpush: https://t.me/bitpush