Solana [SOL] has given back its gains made earlier in the week as Bitcoin slipped below $63K on Friday, the 17th of July.

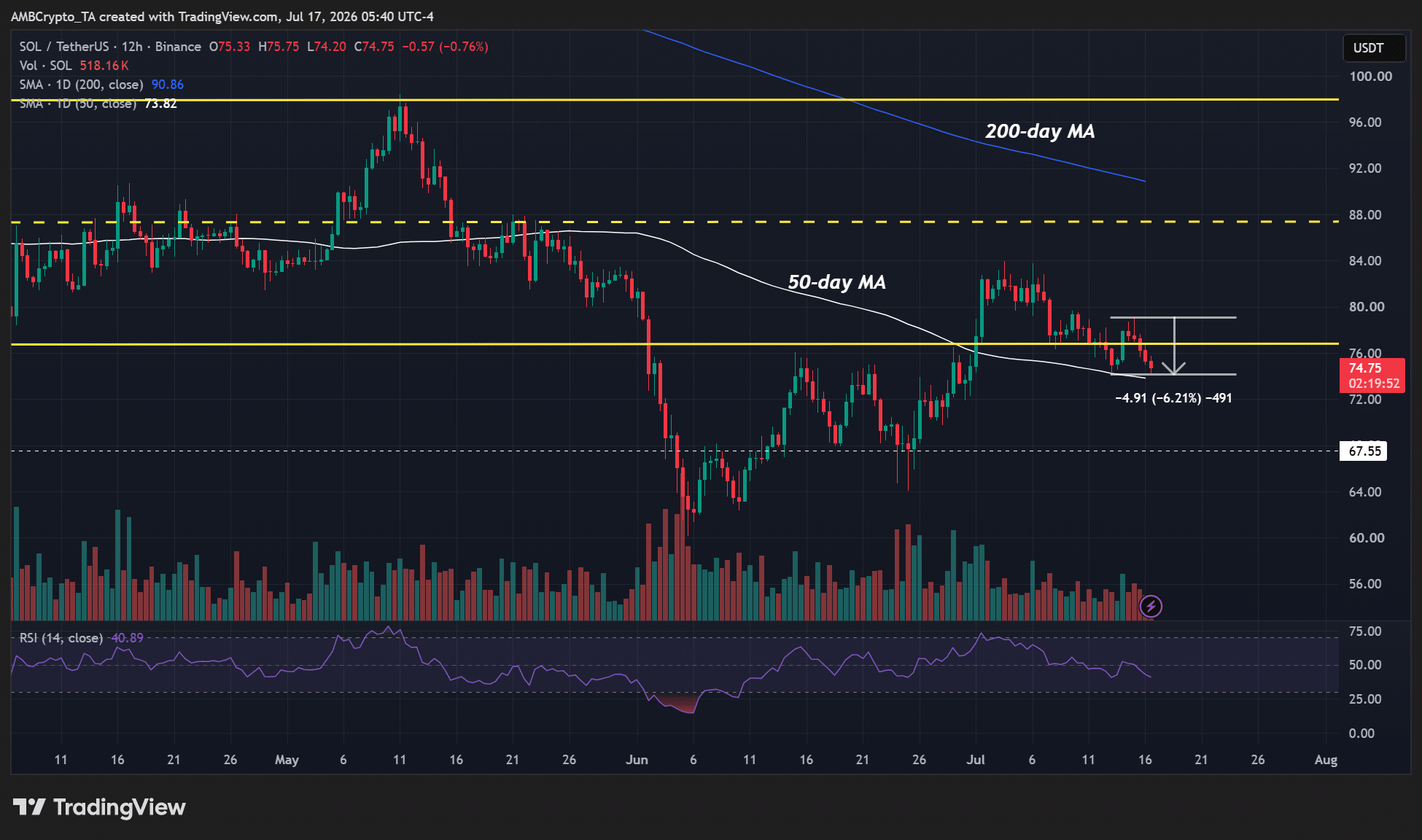

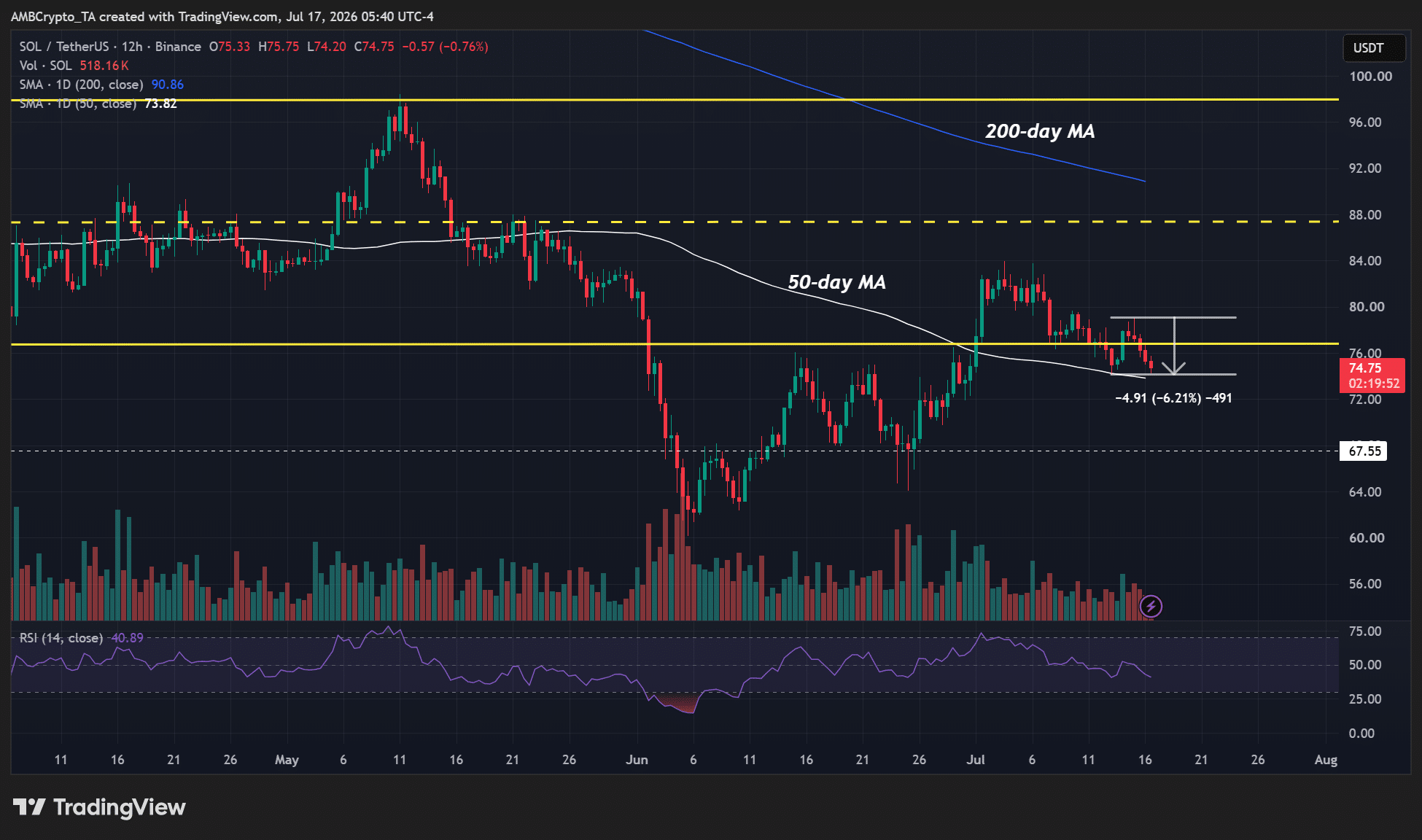

As of writing, SOL was valued at $74.8, down 6% from this week’s high of $79. But the pullback retested a crucial short-term support at the 50-day Moving Average (MA, white).

This dynamic support has stopped the dumps in July. If the trend repeats, relief demand could be possible at the 50-day MA or the $74 level.

If so, the next upside targets would be $80, $84, or the mid-range level at $88. That would be 8%-18% in upside potential.

But the price reversal projection would be invalidated if bears decisively push Solana [SOL] below the 50-day MA. In such a scenario, another dip below $70 couldn’t be overruled.

Will Morgan Stanley’s move boost Solana crypto?

This raises the most crucial question: what are the potential catalysts that could shape SOL’s price direction in the next few days?

First, on Thursday, Morgan Stanley activated spot trading for Solana [SOL], Bitcoin and Ethereum through its E*TRADE platform. Commenting on the same, Chad Turner, Head of Morgan Stanley Wealth Management Platforms, said,

With the rollout of crypto trading on E*TRADE, we’re advancing our digital assets strategy and bringing new capabilities to clients in an integrated way.

Worth pointing out that more banks and brokerage firms are now supporting spot crypto trading, including Charles Schwab and Fidelity. However, only Morgan Stanley has expanded support for SOL, as the other top-tier banks only support BTC and ETH for now.

It remains to be seen whether this will boost demand for SOL.

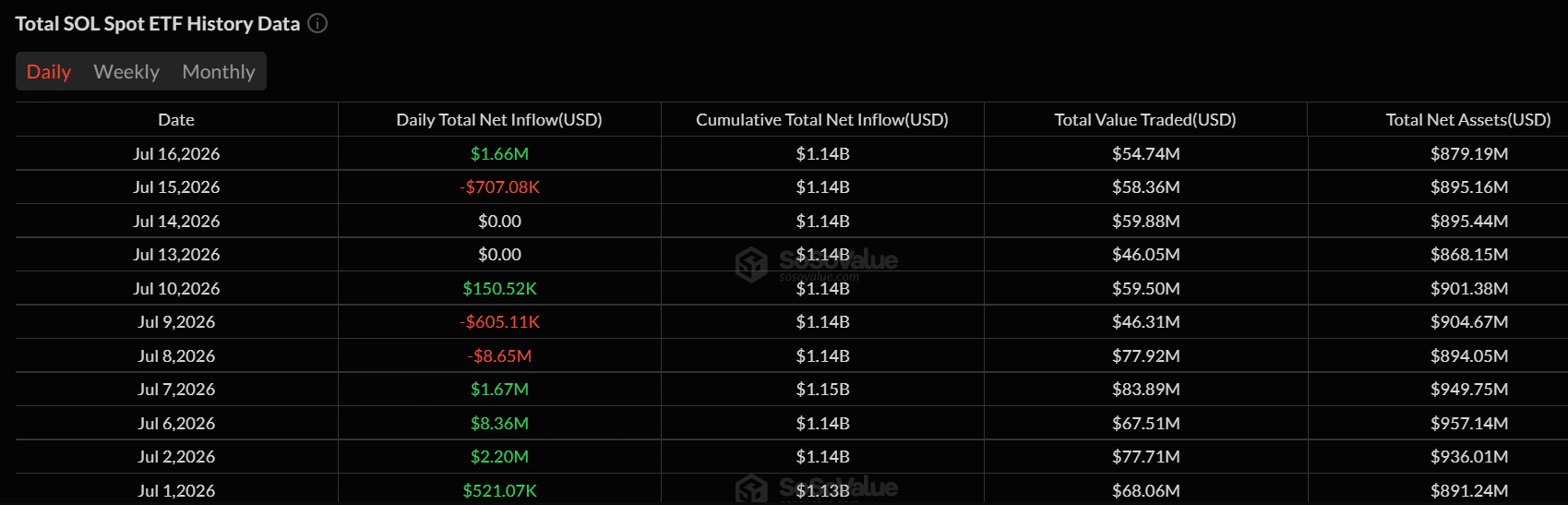

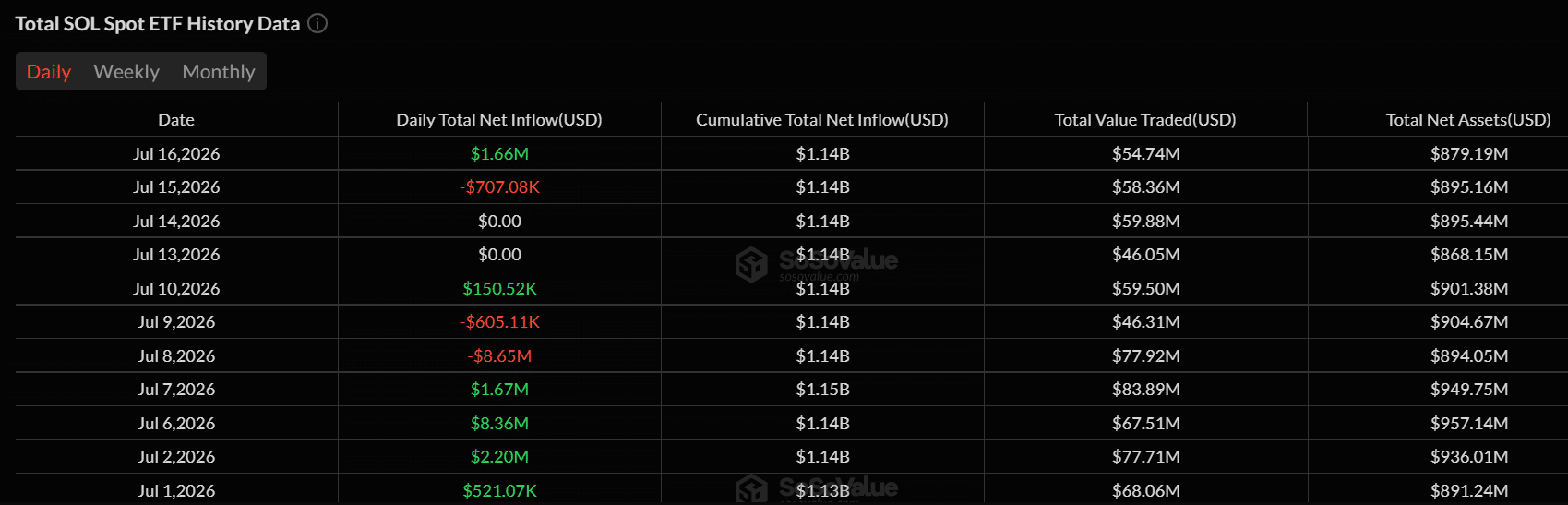

Secondly, U.S. spot ETFs saw a positive daily net inflow of $1.66M on Thursday, breaking the trend of zero or negative outflows seen throughout the week. If inflows remain sustainable, SOL price could defend $74 and attempt a recovery.

In fact, the overall spot SOL accumulation has been strong in the first half of July and in the past 30-days.

However, if macro and geopolitical jitters worsen in the next few days, the potential de-risking could drag SOL lower.

Final Summary

- Morgan Stanley rolled out support for spot SOL trading via its E*TRADE platform.

- SOL’s short-term recovery could be determined if bulls hold above $74.