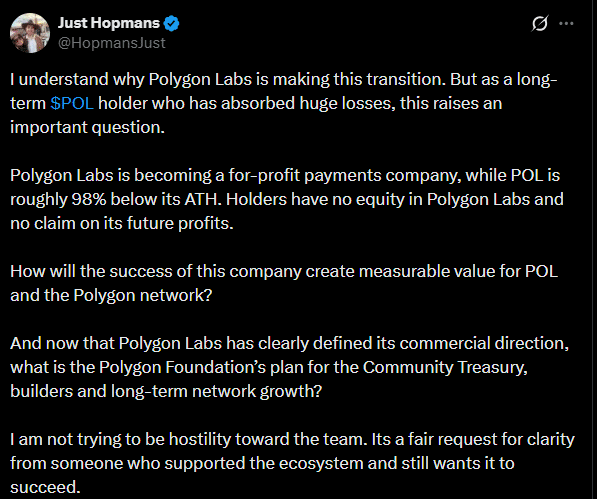

The community of Polygon holders is now pressing for clarity on whether the recent Polygon Labs profitability push will trickle down to them. One of the token holders, Just Hopmans, said,

Polygon Labs is becoming a for-profit payments company, while POL is roughly 98% below its ATH. Holders have no equity in Polygon Labs and no claim on its future profits.

He further posed,

How will the success of this company create measurable value for POL and the Polygon network?

How will POL holders benefit?

POL, the native governance token in the Polygon ecosystem, was rebranded from MATIC in late 2024. During its debut, it surged to $1 before a massive crash to $0.06, or about a 93% drop in 2026.

Despite the losses, POL holders have surged 78% to over 245K in the past month. For Hopmans, clarity on how these holders will benefit from future Polygon payment profits would be worthwhile.

He also sought details on how the community treasury, under the Polygon Foundation, will be handled after the transition. Hopmans claimed that Polygon Foundation, which oversees governance, moved over 50M POL in H1 2026 without clear communication to the community.

For Polygon Labs CEO Marc Boiron, the transition into a blockchain payment firm would ensure its profitability in 2027.

As of writing, the project has yet to respond to Hopmans’ call for transparency and accountability to the community. That said, Polygon’s move was not surprising given its resilience in the competitive payments segment.

Will Polygon increase its stablecoin market share?

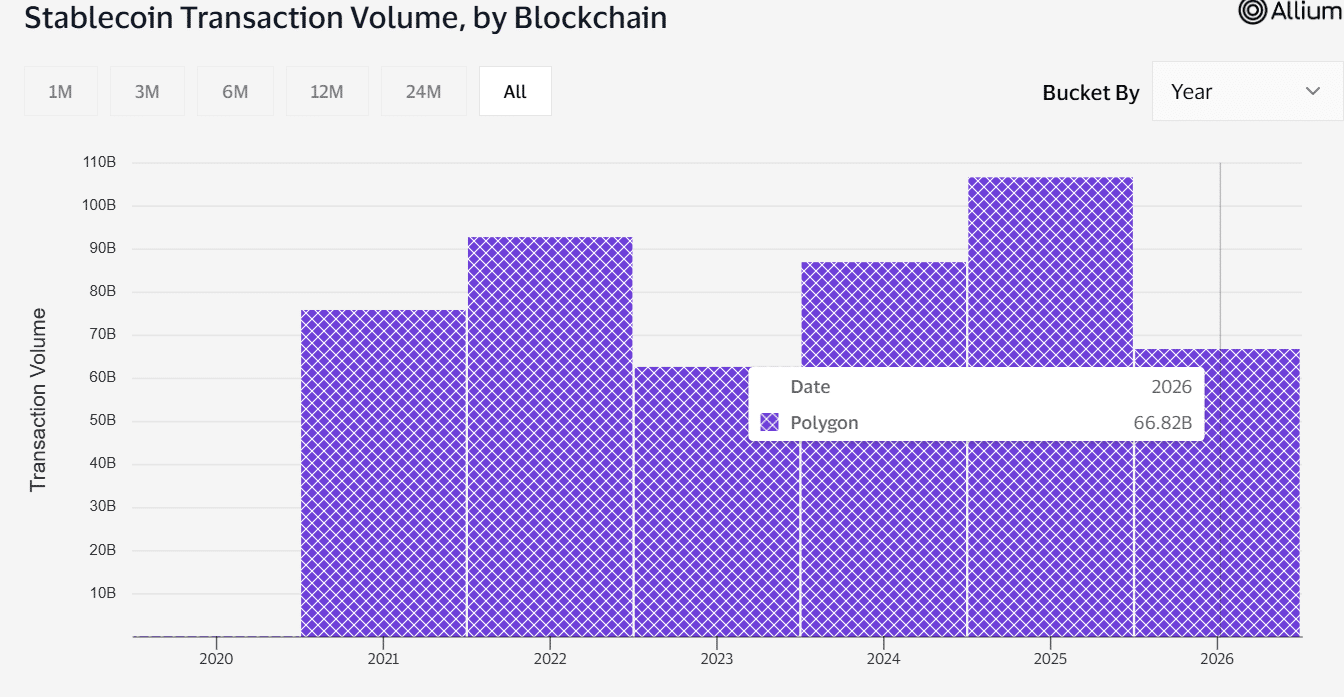

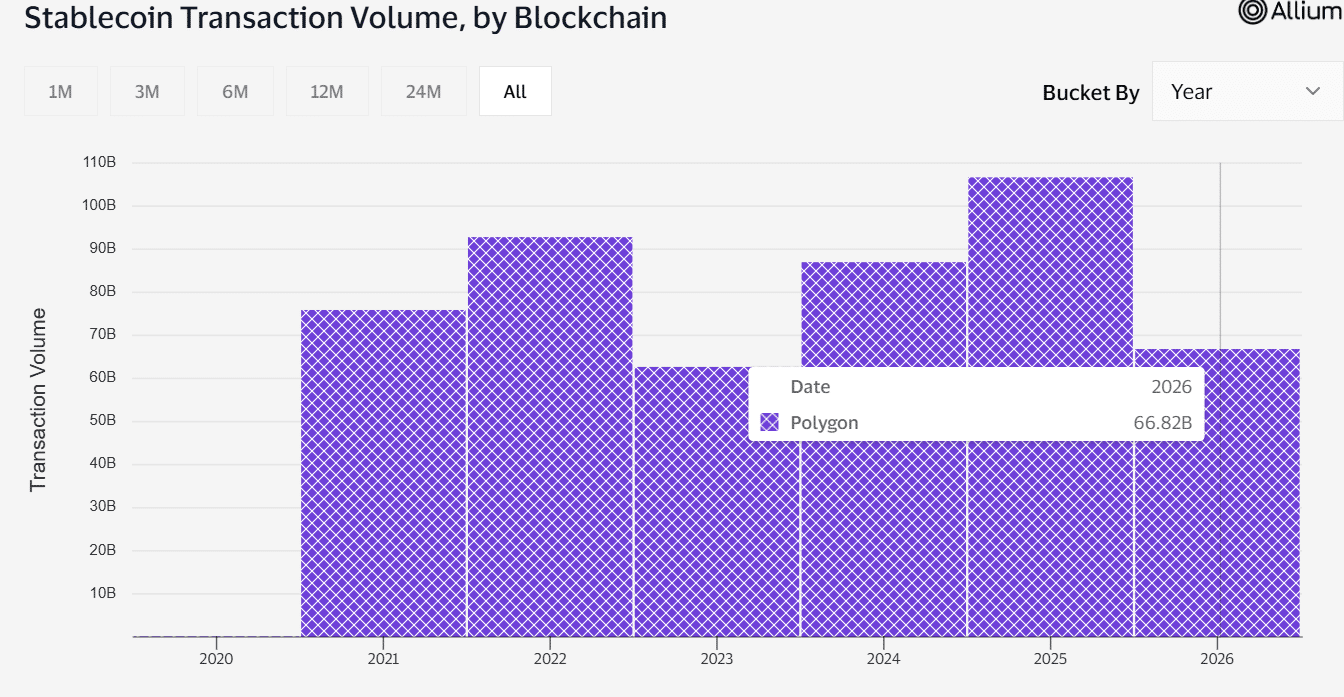

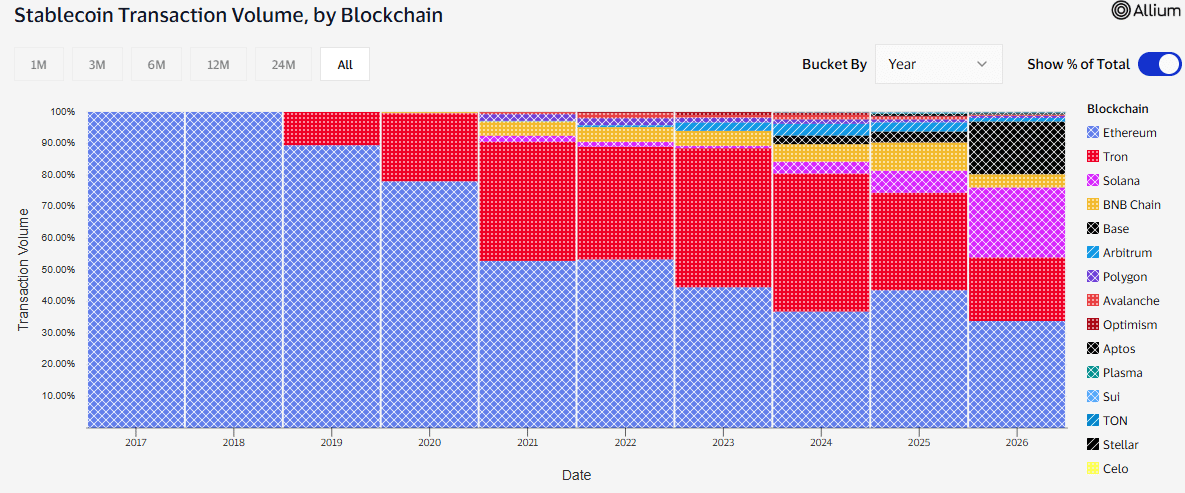

The Ethereum L2 hit a record $106B in annual stablecoin transfer volume in 2025. So far in 2026, the volume is clocking $70B. This has been a growing trend since 2023, making it a key settlement layer for stablecoins, just like Ethereum, Tron, and Arbitrum.

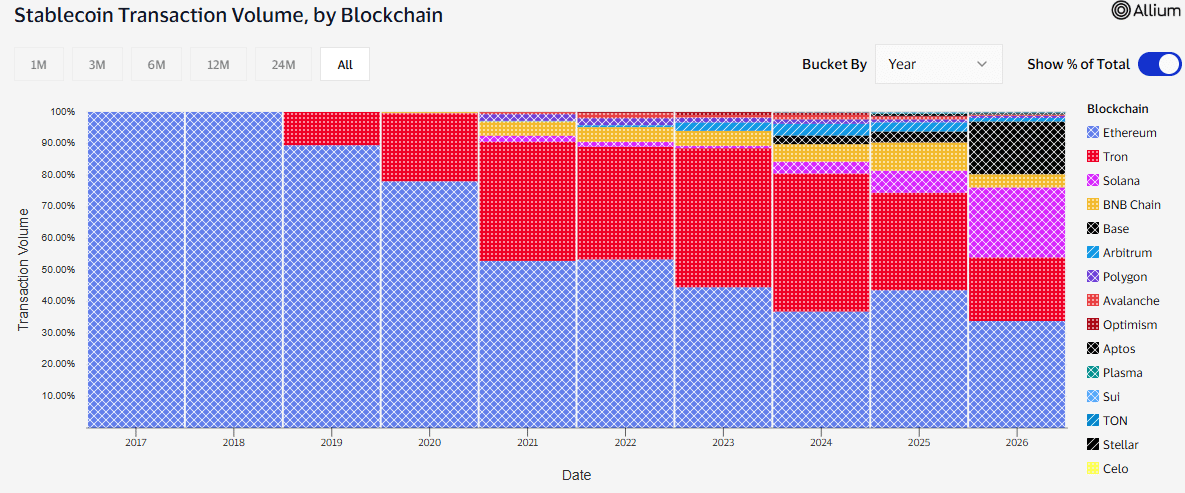

But in terms of market share, Polygon’s rising stablecoin volumes didn’t translate to increasing dominance.

In fact, since 2023, its market share of the stablecoin settlement market has dropped from 1.54% to 0.72% in 2026. In other words, it has lost about half of its market share in an increasingly competitive segment.

Over the same period, Solana [SOL] and Base have increased their market share from zero to 22% and 16%, respectively.

It remains to be seen how the aggressive shifts to payments will bolster Polygon’s standings in the stablecoin settlement sector.

Final Summary

- Community sought to know whether POL tokenholders will benefit from Polygon’s future profitability in payments

- Polygon’s stablecoin volumes have increased from $62B to a record $106B, but market share dropped by half