Author:angelilu, Foresight News

ARB hit $0.094 intraday today, up nearly 20% in the past week, making it one of the best-performing mainstream L2 tokens over that period.

The catalyst for this rally is the launch of "Robinhood Chain"—Robinhood's RWA (Real World Asset) Layer2 built on Arbitrum technology, which officially went live on mainnet at a launch event in London on July 1.

A more subtle logic behind this is that a year-and-a-half-old rule has been brought back into the spotlight: A portion of Robinhood Chain's revenue will automatically flow back into the Arbitrum ecosystem, with a significant chunk going directly to the ArbitrumDAO treasury. This isn't a new policy, but a previously lukewarm revenue-sharing mechanism that is now being seriously priced in by the market for the first time, thanks to the entry of the heavyweight TradFi brand Robinhood.

The First Major Tenant in a Year and a Half

This rule is called the Arbitrum Expansion Program (AEP), launched jointly by the Arbitrum Foundation and Offchain Labs in January 2024. Simply put, it allows Arbitrum to open up its technology for others to build their own chains, with the condition of revenue sharing.

The sharing logic is straightforward: Any independent chain built using Arbitrum Orbit technology but not settling on Arbitrum One/Nova (e.g., settling directly to Ethereum or Base) must share 10% of its net protocol revenue with the Arbitrum ecosystem—8% to the DAO treasury and 2% to the Developer Guild. However, L3s that settle back to Arbitrum One/Nova, like Xai and Sanko, are exempt from this share and retain their status as first-tier ecosystem members.

The key point is that Robinhood Chain is not the first chain to trigger the AEP. Smaller chains settling on Base, like Degen Chain, Onyx, and Flynet, have been paying this share for a while, but their volumes were too small to draw attention. What sets Robinhood Chain apart is simply that it's the first heavyweight chain to bring scale to this shared revenue amount.

Impressive Data, but the Rent Plate is Still Small

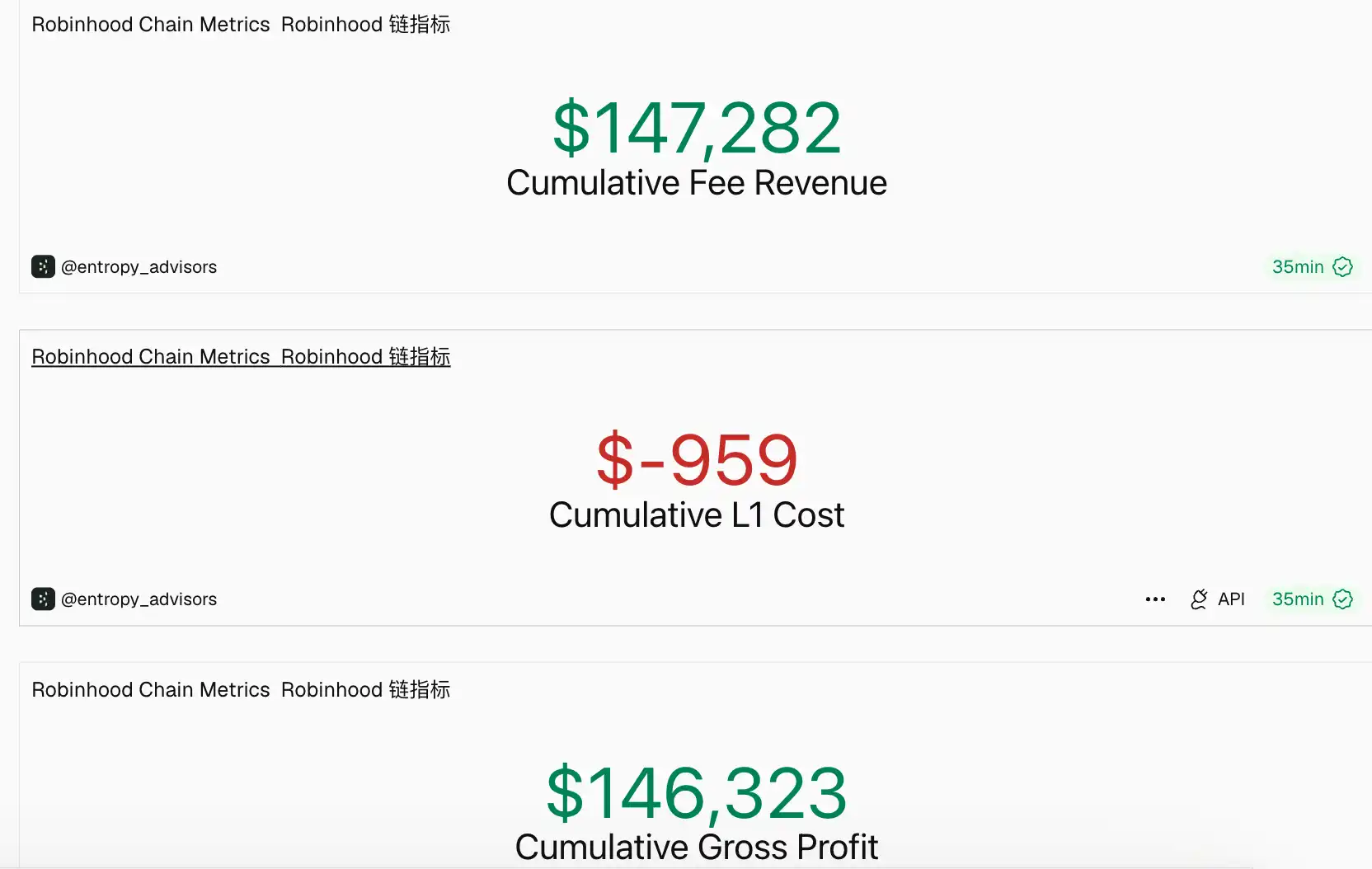

According to the latest data disclosed by Johann, Robinhood's Head of International & Crypto Business: As of July 10, just over a week after launch, Robinhood Chain has processed over 17 million transactions, has over 350,000 addresses, a TVL of approximately $250 million, and DEX trading volume exceeding $1 billion. For a newly launched chain, this report card is indeed impressive.

But the rent plate is far from this large. According to Dune data, as of the time of writing, Robinhood Chain's current protocol revenue is about $147,000. After deducting the cost of data settlement back to Ethereum L1, it's only $146,000. Even if 10% of this is shared with Arbitrum DAO, the amount is pitifully small. ARB's current rally reflects the market's premium valuation on the future scaling boundaries of the AEP protocol—a typical narrative-driven market move.

Looking at the potential upside, the ceiling for AEP is indeed not low: The Robinhood platform holds total assets of approximately $324 billion, custodies assets of about $143.6 billion, and its tokenized stocks have expanded to over 2,000 tokens covering 120 countries—most of these assets are not yet on-chain today. Once settlement gradually migrates, the $57,000 sharing base will stand at a completely different scale.

Old Landlord About to Lose Biggest Tenant, New Landlord Just Landed a Big Deal

Arbitrum's "rent collection" model isn't actually new. Optimism has been running the "landlord" business for a long time.

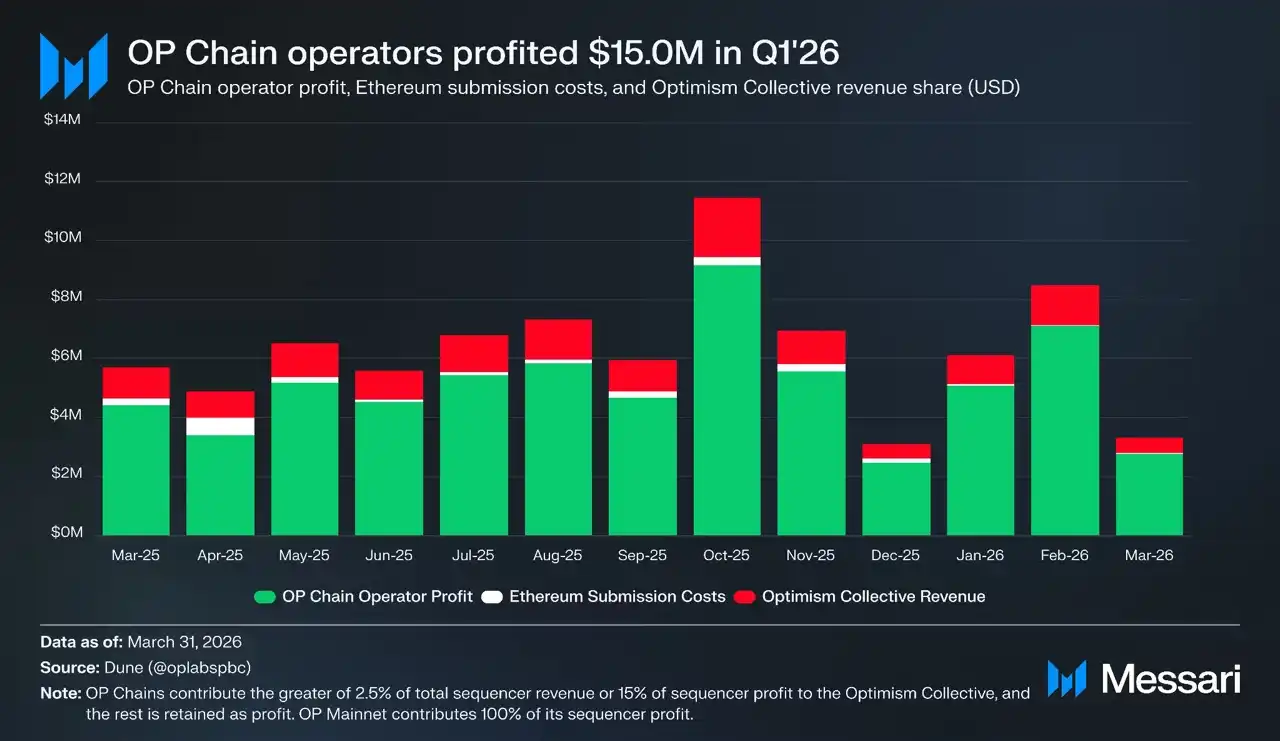

The Optimism Collective collects rent from all Superchain member chains (Base, Zora, Mode, Unichain, etc.) through OP Stack—charging 2.5% of sequencer revenue or 15% of net profit (whichever is higher), and OP Mainnet itself also contributes its net revenue to the treasury. However, its rental income has been gradually shrinking, falling further to about $2.9 million in Q1 2026 (with Base alone contributing about $1.4 million), down 21.5% quarter-on-quarter from $3.7 million in the previous quarter.

In February of this year, Base officially announced plans to leave OP Stack—Base accounted for about 96.5% of revenue flowing into the Collective on a gas fee basis. Upon the news, the OP token fell 28% within two days.

Meanwhile, Arbitrum just managed to revitalize its own landlord business from zero, thanks to Robinhood Chain. Their structures are completely parallel—both are underlying technologies charging rent from external chains, with the money going into their own DAO treasuries (ArbitrumDAO vs. Optimism Collective). The only difference is that Arbitrum's AEP, although the rules were written in 2024, never had a major tenant until this week, finally giving its "rent collection" a sense of scale for the first time.

But Can This Big Tenant Be Kept?

It's precisely this history with Base that some analysts are using to throw cold water. Some believe that, following the same script, Robinhood Chain will eventually leave Arbitrum Orbit just as Base left OP Stack and align directly with Ethereum. According to growthepie data, Robinhood Chain's daily sequencer revenue is already nearly $60,000, second only to Base's $72,000 among Ethereum L2s, approaching three times that of its parent chain, Arbitrum.

Even more delicate is the question of the beneficiary. In its first week, Robinhood Chain has become the second-largest demand source for Ethereum DA after Base, with its sequencer paying blob fees, settling in ETH, and permanently burning it. Some analysts argue that if this chain can only have one ecosystem currency, it's more likely to be ETH than ARB.