Author: Thejaswini M A

Compiled and Edited: BitpushNews

Bitpush Note:

On May 22, 2026, the China Securities Regulatory Commission (CSRC) dropped a bombshell: it plans to impose severe penalties on the illegal cross-border business activities of institutions such as Tiger Brokers, Futu Securities, and Longbridge Securities. Not only are they facing huge fines, but all illegal gains of related entities both inside and outside China will be confiscated according to law. Furthermore, during a two-year centralized rectification period, all related domestic business will be completely banned, with existing mainland clients only allowed to sell unidirectionally. Upon the news, related US-listed broker stocks plummeted over 40% in pre-market trading.

When compliant cross-border channels are being blocked one by one, where will the capital that still craves global asset allocation, participation in pre-IPO pricing for companies like SpaceX, and the ability to trade any asset anytime, anywhere, flow to?

The answer seems to be faintly emerging: flowing into RWA, flowing into Hyperliquid.

This is not a prophecy. This is happening right now.

On the very same day the news of the fines broke, HYPE hit a new high.

Coincidence? Perhaps. But capital doesn't believe in coincidences. It only believes in exits.

The following is the main text:

CME Group (Chicago Mercantile Exchange) is the world's largest derivatives exchange. It's where professional traders buy and sell futures on crude oil, gold, interest rates, stock indices, and Bitcoin. It handles trillions of dollars in daily trading volume and has existed since 1898.

Intercontinental Exchange (ICE) owns the New York Stock Exchange and operates multiple derivatives exchanges globally. It's another industry giant.

They are among the most powerful financial market infrastructure companies on Earth. When they point at something and call it "extremely dangerous," regulators find it hard not to listen.

Currently, CME and ICE are pressuring the U.S. Commodity Futures Trading Commission (CFTC) and Capitol Hill to crack down hard on Hyperliquid, warning that this "KYC-free" platform is a breeding ground for market manipulation and sanctions evasion.

- There is indeed zero KYC. While Hyperliquid uses filters on its main site front-end to block addresses sanctioned by the U.S. Office of Foreign Assets Control (OFAC), its underlying protocol is completely permissionless. If someone bypasses the website and interacts directly with the smart contracts, there is no identity check waiting for them.

- Additionally, there are no position limits on Hyperliquid. At CME, no single trader can hold a position larger than a specific size in any contract, to guard against manipulation and systemic risk. Hyperliquid has no such restrictions.

- CME closely monitors manipulative trading behaviors like spoofing, wash trading, and coordinated attacks. Hyperliquid has no surveillance system watching for these.

These are indeed objective facts.

Influenced by this news, the HYPE token dropped 9% on May 15. Subsequently, two market makers withdrew $100 million in liquidity on May 18 in response.

coingecko.com

But, note which specific product they are targeting. It's not the cryptocurrency perpetual contracts that Hyperliquid has been running for years, which regulators never batted an eye at. Their focus is entirely on the crude oil contracts. These are the contracts that generated $720 million in trading volume over weekends when CME's own crude market is closed.

Regarding this regulatory growing pain, CME and ICE's concerns are not entirely without merit, but we also know in our hearts they are anything but neutral observers. Their business models are entirely reliant on a legally protected "trading hours monopoly." They don't mind competing on technology, but when someone competes with them on time, they go absolutely crazy.

By bringing real volume into the crude oil market over weekends, Hyperliquid has essentially broken the space-time continuum of TradFi. And the incumbents are asking the government to force everyone else to also close their eyes while they sleep. If it were me, I'd prefer to apply for a permit to operate on weekends; but clearly, that's just my thinking.

Hyperliquid's office in Singapore has only 11 people. In the 30 days ending May 21, 2026, the protocol generated $51 million in revenue. In March, it processed a staggering $2.6 trillion in nominal derivatives trading volume.

tokenterminal.com

Hyperliquid routes 97% of trading fees through an on-chain fund to buy back HYPE tokens. Generating $51 million in monthly revenue with just 11 people finds no real comparison, whether inside or outside the cryptocurrency industry, in terms of per capita economic efficiency. As of late May, HYPE is up 101% year-to-date.

All of this isn't necessarily because Hyperliquid built a technically superior derivative, strictly speaking. It's simply because it remains open when CME is closed, and therein lies immense value. Recently, some new developments have pushed this logic to an even deeper level.

On May 1, Trade.xyz, a platform built on Hyperliquid, launched a Pre-IPO perpetual futures contract for AI chipmaker Cerebras. The contract ran for two weeks before the IPO. Early in that window, traders had smoothed out a roughly 50% premium relative to the $185 IPO price, implying an opening price around $277. Then market information updated. One hour before Cerebras opened on NASDAQ, the perpetual contract on Trade.xyz was pricing the stock at $340, within less than 3% of the actual opening price. In the end, Cerebras opened at $350 on May 14, a stunning 89% surge from its $185 IPO price. Traditional pre-IPO market platforms like Forge and EquityZen had prediction errors of 35%, while Hyperliquid's error was just 3%.

When genuine uncertainty still existed, $277 was the price the market implied. As information kept flowing in and being priced in, the wisdom of the crowd smoothed out that gap. This is how price discovery is supposed to work.

Then on May 17, a Sunday morning, Trade.xyz launched a SpaceX perpetual futures contract. It opened at a reference price of $150, soared to $216 within hours, and eventually stabilized around $203, implying the crowd valued the company at $2.4 trillion.

Yet at that time, SpaceX had not publicly filed an S-1 registration statement, no Wall Street analyst had given a price target, and an official roadshow was nowhere in sight.

Traders had no idea that SpaceX had actually confidentially submitted a draft filing to the SEC as early as April 1, with a target valuation set between $1.75 trillion and $2 trillion.

Traders settled the contract at $203, implying a $2.4 trillion valuation. Before bankers held their first meeting, without access to the filing documents, the crowd landed smartly at the top end of the company's own target range. Just days later, on May 20, a Wednesday, SpaceX formally filed its actual 277-page S-1 prospectus with the public.

Currently, three products are trying to provide investors with exposure to SpaceX. Each legally bets on a different solution.

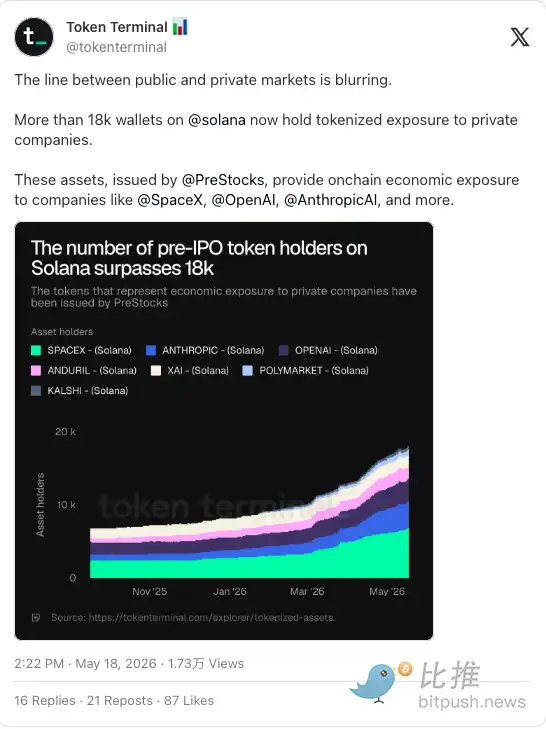

PreStocks tried to be clever. They set up special purpose vehicle (SPV) funds to buy real SpaceX shares, then split and mapped those fund shares into blockchain tokens so retail investors could get a slice. It looked like a clean backdoor into private tech companies.

However, shortly before Hyperliquid launched its SPCX contract, Anthropic and OpenAI publicly distanced themselves from third-party SPV products claiming to track their valuations. Platforms in Hong Kong and the UAE had been selling tokenized exposure to these two companies without board approval. Both companies issued warnings that the equity transfers behind these products were invalid. PreStocks' token promptly plunged 50%. When you try to operate by anchoring to real shares, the company you hold shares in always reserves the right to intervene.

Ondo Global Markets tokenizes shares through a U.S.-registered broker-dealer, with each token backed by underlying securities. Its compliance is very clean; even the Depository Trust & Clearing Corporation (DTCC) is building settlement infrastructure around it.

But Ondo's greatest strength is also its biggest vulnerability. It has a specific physical address. If the SEC decides to shut it down, they know exactly whose door to knock on. If Elon Musk objects, SpaceX's lawyers know exactly which custodian to sue. By choosing to play the game by the rules, Ondo has made itself a perfect target for pinpoint strikes.

Then look at Hyperliquid's SPCX contract — this thing is built entirely on air.

No shares, no registered broker-dealer, no claim on any physical asset. It's a synthetic perpetual contract, a ghost through and through. A pure bet on a price feed, settled entirely in USDC on a decentralized network.

Even if SpaceX wanted to stop people from trading derivatives based on its valuation, it couldn't. There's no corporate entity to serve legal papers to, no central issuer to pressure.

This is really clever. Hyperliquid basically figured out: if you have no face, no one can punch you in the face. By anchoring the product to nothing physical, they've become impossible to target.

I'm not sure this is purely a good thing.

A zero-KYC venue rerouting trillions of dollars around the global banking system — the national security nightmare this poses is hard to argue against. The fact that Hyperliquid co-founder Jeff Yan flew to Washington on May 17 to meet policymakers is proof enough of how real this pressure is.

Speaking of Jeff Yan. He is a real person, shows his face, and went to Harvard. If SpaceX wanted to sue him for trademark infringement or IP violation because his platform lists a contract called "SPCX," they could absolutely serve him the lawsuit.

But suing Jeff wouldn't make the contract disappear.

With PreStocks, if the company deletes the underlying shares, the product ceases to exist. With Ondo, if a judge freezes the bank or custodian, the product stalls. But Hyperliquid's SPCX is an autonomously deployed piece of code. Even if Jeff Yan gets sued into oblivion, those smart contracts are live, the code is immutable, and the global order book would keep running on-chain.

This is the "flawless theory" of decentralization. Reality is more fragile. Hyperliquid only runs on 20 validators, not 900,000. These validators can be identified. And the JELLY incident has already shown: they will intervene if they want to. Validators are not immutable.

Again, time is the only product they can't replicate.