作者:克洛德,深潮 TechFlow

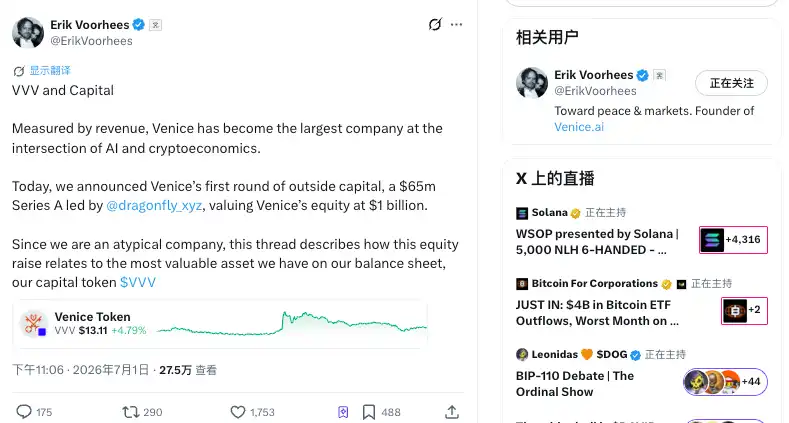

深潮导读:隐私 AI 平台 Venice 完成首轮外部融资 6500 万美元,估值 10 亿美元跻身独角兽,Dragonfly 领投、Coinbase Ventures 跟投。对 VVV 持有者,真正的看点不是这笔钱,而是这轮的股权+代币混合结构:创始人 Erik Voorhees 强调团队一枚币没卖、还要继续回购销毁并降低发行量;但投资人手里握着 8 年内可买 500 万枚 VVV 的认股权证,一年后开始行权,每天约 6000 枚新币入场。消息公布后 VVV 应声上涨,市场将其解读为利好。

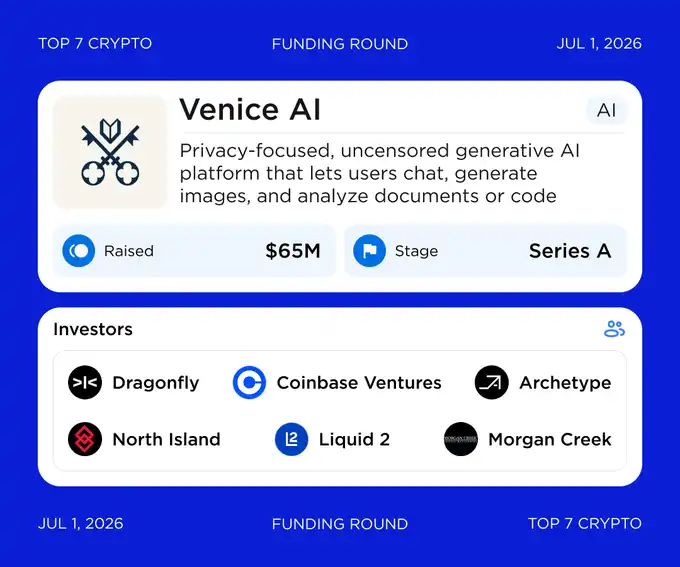

Erik Voorhees 的 Venice 拿到了成立以来第一笔外部资金。

据 The Block 报道,这家由 ShapeShift 创始人 Voorhees 打造的隐私 AI 平台,完成 6500 万美元 A 轮融资,估值 10 亿美元。加密风投 Dragonfly 领投,Coinbase Ventures、North Island Ventures、F-Prime、Archetype、Liquid2 Ventures、Morgan Creek 等跟投。这是 Venice 两年前上线以来首次引入外部资本,此前既未做 VC 私募,也没靠国库里的 VVV 代币变现。

股权+代币双层结构,投资人拿走近 9% 股权外加两批 VVV

Voorhees 在 X 长帖里披露了这轮的完整对价。6500 万美元换来三样东西,Venice 公司 8.98% 的股权、150 万枚 VVV 代币的归属权,以及未来 8 年内按约定价格再买 500 万枚 VVV 的认股权证(warrants)。

认股权证是一种在未来某个时间、以约定价格购买代币的权利。据 Voorhees 测算,投资人若把这 500 万枚认股权证全部行权,还需再向 Venice 支付约 6650 万美元,这样一来这轮实际总募资将抬升到约 1.315 亿美元。代币归属权和认股权证都设一年锁定期,之后在随后三年内线性解锁。

投资人现在到手的是股权,加一份「以后可以按约定价买币」的期权,而不是立刻可流通的代币。这种把股权、代币归属、代币认股权证捆在一起的结构,在加密融资里并不常见,多数项目要么纯股权,要么直接卖币给 VC。

创始人「先做产品和代币,再引 VC」,反着行业惯例来

Voorhees 强调,Venice 选择卖股权,而不是卖国库里的代币来融资。他称 Venice 目前仍是 VVV 最大持有者,在当前逾 8000 万枚的总供应中持有 3000 万枚以上,公司和团队至今没有卖出过一枚 VVV,尽管这枚代币今年已上涨逾 700%。

Venice 的融资节奏和行业惯例正好相反。多数项目在条款不公开的情况下先把代币预售给 VC,承诺以后再做产品、再找用户,Venice 则先上线产品和代币、跑出用户和收入,再引入外部投资人。

这套打法有业务数据托底。据公司披露,Venice 在 4 月用户达到 300 万,第一季度已实现盈利,多家媒体援引 Voorhees 的说法称其年化收入(run-rate)已超过 7000 万美元。一家 A 轮阶段的 AI 创业公司融资前就盈利,并不寻常。

认股权证是 VVV 的未来抛压,但节奏被创始人算成「不痛不痒」

对持币者来说,那 500 万枚认股权证是绕不开的问题。它们是未来的潜在增发,一旦行权就变成新的流通供应,也就是抛压。

据 Voorhees 测算,投资人若全额行权,从大约一年后开始,每天约有 6000 枚 VVV 进入市场,约相当于当前日交易量的 0.2%。这个量级相对市场深度不算大。没有行权的那部分认股权证,对应代币继续留在 Venice 资产负债表上,不进入流通。

代币策略这一端,Venice 称维持不变,继续用一部分收入回购并销毁 VVV,同时逐步降低代币发行量。销毁减少存量,认股权证增加潜在供应,两股力量方向相反。VVV 的净供应往哪个方向走,取决于回购销毁的力度能否盖过认股权证解锁和常规发行。这是持币者接下来要盯的核心变量,比这次融资本身更值得跟踪。

这里要提醒一句,「每天 6000 枚、占日交易量 0.2%」这组数字来自 Voorhees 本人测算,属于融资方自述,深潮暂无独立数据交叉验证,读者宜作参考而非定论。

钱要拿去自建算力,指向 GPU 和第一座数据中心

依据创始人所述,这轮融资的用途拿去自建算力基础设施,包括 Venice 的第一座数据中心,以降低对租赁 GPU 的依赖。

他给出的逻辑是,自建算力能在「即将到来的资源紧张」中锁定产能,并提高毛利率,从而让「更大规模的 VVV 销毁成为可能」。

言下之意,自建算力压低成本、抬高利润,利润再拿去回购销毁 VVV。除了算力,Venice 还计划用这笔钱进入新市场、收购「有协同效应」的业务、招人和扩大客户群。

产品侧,Venice 定位为 ChatGPT 的隐私、抗审查替代品,声称不在自有系统上存储用户提示词,请求经加密后通过外部代理转发,付费订阅还提供端到端加密。平台称接入了 200 多个 AI 模型,既有自托管的开源模型,也有通过 API 匿名调用的 OpenAI、Anthropic 等闭源模型。VVV 之外,Venice 还有一枚 DIEM 代币:用户质押 VVV 得到 sVVV,再锁定一部分 sVVV 铸造 DIEM,每枚 DIEM 对应平台上价值 1 美元、永不过期的 API 额度。