一则“让跨链桥回家”(bring the bridge home)的温情标语,在8月11日的凌晨,引爆了加密社区一场关于忠诚、价值与权力的激烈辩论 。主角是跨链互操作性协议LayerZero及其生态中最耀眼的明星项目——跨链桥Stargate。LayerZero基金会正式向Stargate DAO提交了一份收购提案,计划以约1.1亿美元的总价,将其一手孵化并推向成功的“孩子”完全收归囊中。

这并非一次寻常的商业并购,更像是一场复杂的家族内部事务。提案的核心是将所有流通的Stargate原生代币STG,按照1 STG兑换0.08634 ZRO的固定比例,全部转换为LayerZero的原生代币ZRO,并在此后解散Stargate DAO,将其所有治理权和未来收入统一整合进LayerZero生态 。市场的初步反应是热烈的,消息一出,ZRO与STG代币价格双双飙升超过20%,似乎预示着一次双赢的整合 。然而,在这短暂的狂欢之下,Stargate治理论坛内却早已硝烟弥漫,一场来自社区的强烈抵制正在酝酿。

这起收购案远不止是一笔资产的转移,它已然演变成一场对去中心化治理本质的公投,一个关于代币经济模型演进的鲜活案例,更是在愈演愈烈的高风险互操作性战争中,一次关键的战略布局。这背后交织的,是效率与公平的博弈,是创始团队的战略雄心与社区成员切身利益的直接碰撞。

造物主与造物:解构LayerZero与Stargate的共生与分裂

在加密世界中,协议与应用的关系时常如同星系与行星,彼此吸引却又保持着独立的轨道。但LayerZero与Stargate的渊源却是个例外,它更像是一场精心安排的“父与子”的叙事。Stargate并非旁落的生态项目,而是LayerZero Labs在2022年3月,由其核心创始团队亲手打造并推向世界的“长子”。

彼时,LayerZero的全链互操作愿景宏大但仍显抽象,市场需要一个具体、可触的范例来理解其价值。Stargate的诞生,便承载了这样一个清晰的使命:它必须成为LayerZero底层技术最闪耀的橱窗,用真实的用户、真实的资产和真实的交易量,向世界证明,LayerZero所承诺的无缝跨链通信,并非仅仅停留在白皮书里的一个概念。

市场的回应堪称一场风暴。Stargate上线仅十天,其总锁仓价值(TVL)便如火箭般蹿升至惊人的34亿美元,这在当时几乎改写了DeFi应用增长速度的神话。每一个在Stargate上完成跨链的用户,每一次资产的无缝流转,都在为LayerZero的底层网络投下信任票。因此,这不仅是Stargate的高光时刻,更是LayerZero完成的第一次、也是最重要的一次公开“价值验资”——一次无可争议且动人心魄的成功。这段共生关系,也为今天这场“家庭内部”的收购风波,埋下了最深的伏笔。

在最初的战略设计中,将协议(LayerZero)与应用(Stargate)分离,并各自发行代币(ZRO与STG),是一种巧妙的叙事策略。它成功地将LayerZero塑造成一个超越普通跨链桥的“第0层”基础协议——一个如同互联网TCP/IP协议般的存在,未来可以承载无数个类似Stargate的应用 。这种分层架构,使得ZRO代币看起来比其他任何跨链桥代币都“更高级”,为其赢得了更高的估值想象空间。

然而,时过境迁,曾经的优势如今却成了创始人眼中的累赘。LayerZero首席执行官Bryan Pellegrino在解释收购动机时直言不讳:“我们想要行动得更快,交付得更快。” 。他认为,两个独立实体的并行运作带来了不必要的沟通成本和决策摩擦,“每天我们都在纠结微小的选择……谁来负责写代码?这一切都是负担,都太慢了。” 。因此,将Stargate重新整合,旨在消除内部摩擦,创建一个开发者可以无缝采用的“单一堆栈”,并以更集中的资源和“统一的方向”来帮助Stargate实现其宏伟的路线图 。

这种从共生到寻求统一的转变,在传统科技界并不罕见,类似于母公司分拆出一个成功的子公司后又寻求重新整合。但加密世界的独特之处在于,这个“子公司”拥有一个由代币持有者组成的、拥有实际投票权的去中心化自治组织(DAO) 。这意味着,这场“家庭团聚”无法由“家长”LayerZero单方面决定,而必须与一个庞大、活跃且当前充满敌意的社区进行艰难的“政治协商”。这使得一场本应是商业决策的事件,演变成了一场对去中心化公司治理模式的极限测试。

经济模型的裂痕:一场两种价值主张的对决

这场收购争议的核心,实际上是两种截然不同的代币经济模型的直接冲突。

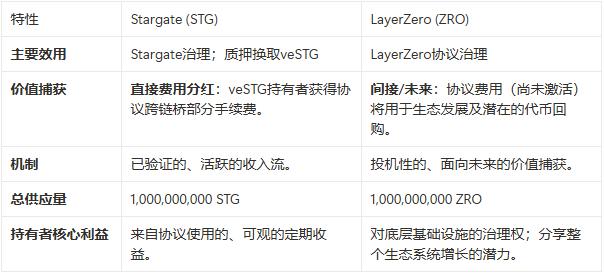

Stargate (STG):久经考验的收入引擎

STG代币的核心吸引力在于其直接且可量化的价值捕获机制。持有者可以通过质押STG获得veSTG,从而分享协议产生的跨链桥手续费收入 。这是一个已经得到市场验证、持续运作的真实收益模型。Stargate作为一个协议,其基本面十分健康。链上数据显示,它已处理了超过700亿美元的历史交易量 ,根据DeFiLlama的数据,其年化手续费收入约88.6万美元,国库资金高达4797万美元,累计桥接交易量超过440亿美元 。这些数据描绘出一个被广泛使用且具备强大创收能力的应用,与任何关于其“陷入困境”的说法都背道而驰。

LayerZero (ZRO):着眼未来的协议价值

相比之下,ZRO的价值主张更为宏大和抽象。其主要效用是对LayerZero整个协议的治理权。尽管代币经济学中包含了协议费用开关的设计,但该功能至今尚未激活 。ZRO的价值更多地建立在对LayerZero生态系统未来全面成功的预期之上,是一种投机性的未来价值 。值得注意的是,ZRO代币于2024年6月刚刚通过一场声势浩大的空投活动上线 ,这意味着其大部分持有者是新用户,而STG社区中则不乏经历了数轮牛熊周期的长期支持者。

这场收购,本质上是要求Stargate社区用“手中鸟”(已实现的稳定收益)去交换“林中鸟”(未兑现的未来潜力)。这种价值主张的根本性不对称,是社区激烈反对的经济学根源。当一个价值流是活跃且被证实的,而另一个仍停留在“路线图”层面时,任何关于“公平”兑换比例的讨论都显得苍白无力,自然会引发普遍的质疑。同时,这一举动也反映了行业内关于代币模型思潮的变迁。尽管双代币模型在特定时期能提供专门化的效用,但近年来,单一模型因其能更好地凝聚价值、减少经济摩擦和简化社区认知,正逐渐成为行业共识 。LayerZero的收购,可以被视为其追赶这一行业趋势的激进尝试。

忠诚的代价:一场社区反叛的解剖

LayerZero的提案在Stargate的治理论坛上引发了山呼海啸般的反对声浪。社区成员的愤怒主要集中在三个层面,每一个都直指提案的核心缺陷。

首先是报价的“侮辱性”。许多社区成员直斥该提案“毫无吸引力”且“存在根本性缺陷” 。他们指出,STG代币的历史高点曾达到4.14美元 ,而当前市场正处于复苏初期,以约0.17美元的历史低位价格进行收购,是对Stargate协议巨大收入规模和发展潜力的“严重低估”。

其次是对长期主义者的背叛。Stargate采用了ve (vote-escrowed) 治理模型,该模型旨在通过赋予长期锁仓用户更高的治理权重和收益,来奖励他们对协议的长期承诺 。然而,收购提案并未对这些veSTG持有者提供任何额外补偿。他们为了协议的未来而选择牺牲流动性,如今却发现这份忠诚不仅没有换来溢价,反而使自己陷入了被低价收购的困境。这种做法无疑是对ve模型精神的公然践踏。

最后,也是最关键的一点,是优质经济模型的丧失。社区成员明确指出,“STG的收入分成机制在ZRO上并不适用” 。他们失去的不仅仅是一个代币,更是一种优越的、直接的经济权利。提案中提到的用Stargate未来收入回购ZRO的方案,被普遍认为是一种间接、低效的价值传递方式,远不如他们目前享有的直接费用分红来得实在。

这场反叛并非单纯的拒绝,而是一场积极的谈判。社区在表达不满的同时,也提出了明确的修改条款,构成了一份事实上的反向要约。这些要求包括:大幅提高兑换比例,部分成员甚至喊出了1:1兑换ZRO的诉求;为veSTG持有者提供基于锁仓时长的额外溢价补偿;以及在新体系下,为原STG持有者保留某种形式的持续性收入分成机制 。这场激烈的反弹揭示了ve代币模型在面对收购时的一个潜在结构性缺陷:它创造了一个高度忠诚但缺乏流动性的利益相关者群体,而这个群体恰恰最容易受到基于短期市场流动价格的低价要约的伤害。

生态回响:前车之鉴与战略要务

LayerZero的这场“家族内斗”并非孤例,也并非仅仅源于内部的效率考量。放眼整个加密生态,我们可以从其他项目的整合案例以及日益白热化的竞争格局中,找到更深层次的动因。

他山之石:ASI联盟的合并范例

就在不久前,三大AI概念协议Fetch.ai (FET)、SingularityNET (AGIX)和Ocean Protocol (OCEAN)宣布合并其代币,共同组建“人工智能超级联盟”(ASI) 。这次合并为我们提供了一个极具价值的参照系。ASI联盟的合并,其核心驱动力是创建一个强大的、去中心化的AI基础设施,以对抗谷歌、OpenAI等科技巨头的垄断地位,这是一个宏大且一致的外部战略目标 。其过程也体现了高度的协作精神,通过多轮社区投票,并最终成立了一个由三方领袖共同组成的治理委员会 。相比之下,LayerZero的收购案,更多被包装成一个“让孩子回家”的内部整理事务,其叙事格局和协作姿态,显然未能赢得社区的共鸣。

未言明的驱动力:互操作性战场

更重要的是,这次收购的背后,是互操作性赛道日益残酷的竞争现实。LayerZero虽然在消息传递量上处于领先地位 ,但它面临着来自Wormhole、Axelar,尤其是Chainlink跨链互操作协议(CCIP)的巨大压力 。Chainlink的CCIP不仅仅是一项技术,更是一个强大的分销网络。通过与SWIFT、DTCC、澳新银行乃至万事达卡等金融巨头的深度合作,Chainlink正在构建一个机构级的跨链价值传输标准 。其统一的LINK代币捕获了生态系统内所有服务的价值,向市场呈现了一个清晰、强大的价值主张 。

从这个角度看,LayerZero的整合举动就不仅仅是内部优化,而是一项迫在眉睫的战略要务。一个价值被ZRO和STG分割的、叙事复杂的生态系统,在面对像Chainlink这样统一而强大的对手时,无疑是一种竞争劣势。将价值统一到ZRO之下,能让LayerZero以一个同样简洁有力的经济故事去吸引开发者、用户和投资者。因此,这场看似为了提升内部效率的收购,其更深层的、未被言明的驱动力,或许是为了应对Chainlink CCIP及其统一的LINK代币经济所带来的外部生存威胁。这是一场以效率为名的防御性战略收缩。

结论:一场关于去中心化治理灵魂的公投

目前,LayerZero与Stargate社区陷入了僵局。一方是出于战略需要、信奉统一生态的创始团队;另一方是感觉被低估和背叛、手握最终决定权的社区。这场对峙的结果,将取决于需要获得70%支持率的Snapshot投票 。

这起事件已经成为DAO治理能力的一次关键压力测试。一个创始团队和它的社区,能否在类似企业并购的高风险谈判中找到共赢的路径?还是说,中心化的战略导向与去中心化的所有权之间的内在张力,终将导致无法弥合的分裂?无论最终结果是提案失败、团队被迫修改方案,还是在争议中强行通过,这场“让跨链桥回家”的传奇,都将作为加密史上关于链上组织未来、权力平衡以及在去中心化世界中忠诚与进步代价的深刻案例,被长久地讨论与铭记。