原文作者:深潮 TechFlow

现在的加密市场,逐渐陷入倦怠。

比特币和以太坊价格在来回波动中挣扎,热点被加密美股和稳定币霸占,以前加密行业那股极客与草根交织的社区精神——玩梗、实验、集体狂欢——似乎已被行情和骗局碾平。

而最近两天,那种久违的社区整活又回来了,还带着一种淡淡的加密文艺复兴味道。

6 月 19 日,Solana 联合创始人 Anatoly Yakovenko(Toly)在社媒上的闲聊讨论,催生了一个叫做 Gorbagana 的 Meme 币 ;

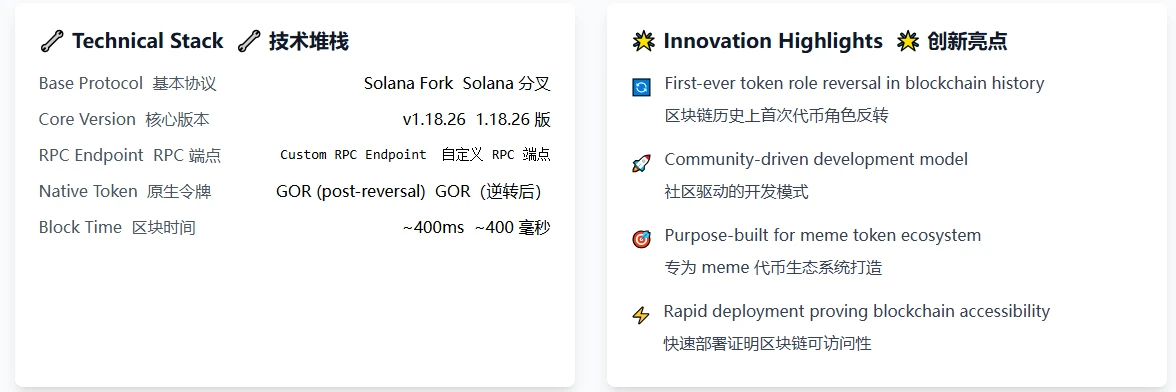

有趣之处在于,仅仅 48 小时后,和该币同名的L1链 Gorbagana Chain 就上线了测试网,并且在技术上对 Solana 进行了分叉。

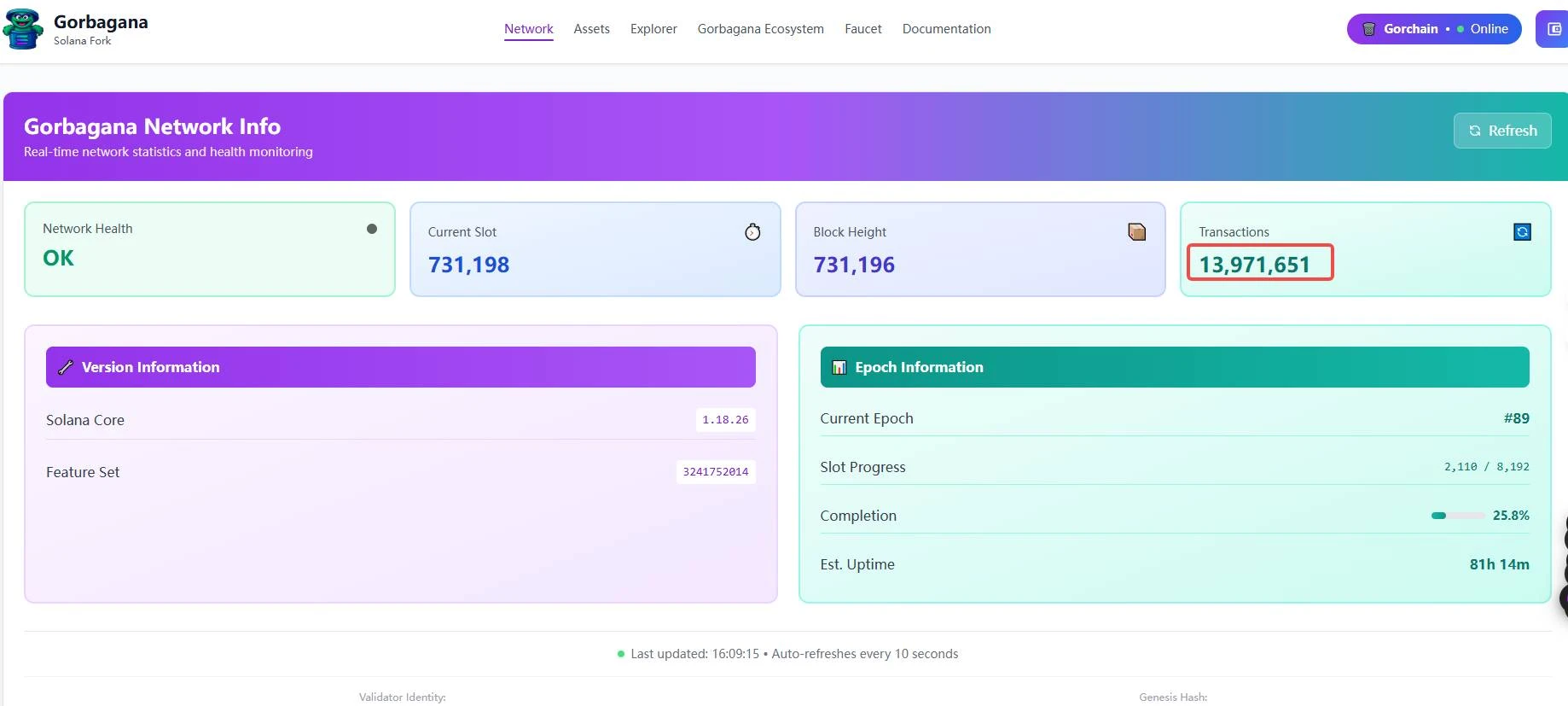

截止目前, Gorbagana 运行稳定,并已经处理了近 1400 万笔交易;代币 $GOR 市值在 4 天内已经来到了 3000 万美金(峰值 6000 万美金)。

一个 Meme 本身当然不足为奇,但有趣且讽刺的地方是,从社区发个 Meme 到做一条链只要 2 天;而之前所谓的天王级 L1 项目们,从宣发到上线测试网慢的可能要 1-2 年。

没有线路图、白皮书和营销,这不是那种典型的、精心策划的 ICO,而是一个由 Telegram 群组里的 Degen 和开发者们驱动的即兴行为。

如果你并不了解这一事件,我们也将 Gorbagana 事件始末整理如下。

48 小时,从玩笑 Meme 到正经 L1

和以前的一些经典 Meme 类似,Gorbagana 的诞生也始于一句玩笑。

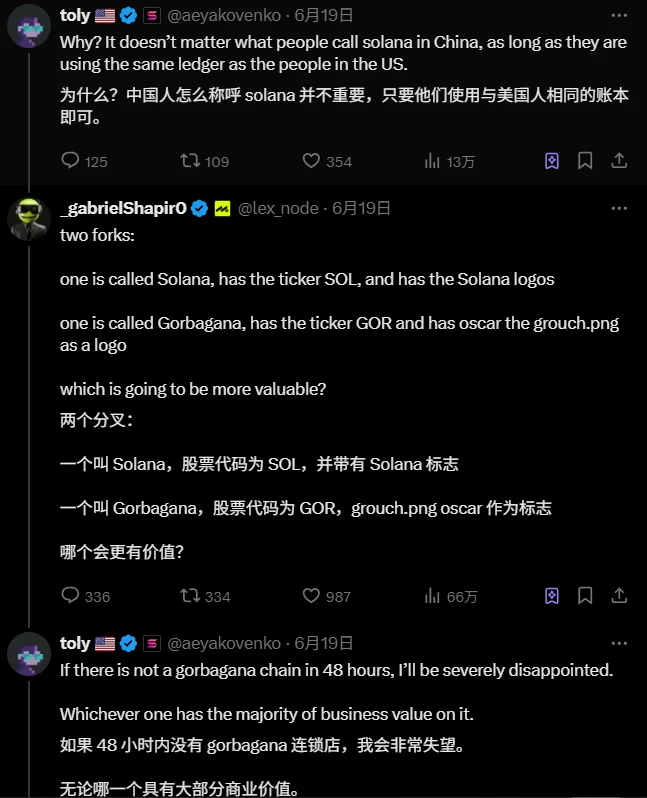

19 日,Toly 在 X 上与其他用户闲聊 Solana 的品牌辨识度等问题时,网友 @lex_node 为了驳斥 Toly 认为“品牌名其实没那么重要”的观点时,随口编造了一个概念:

如果一条链叫 Solana,另一个分叉链叫 Gorbagana,技术都差不多,但显然是 Solana 更有价值。

随后 Toly 将计就计,回帖表示“ 48 小时内如果没有一条叫 gorbagana 的链出现,那我还挺失望的”。

显然这个 gorbagana 只是一个听起来像 Solana 但更长更胡扯的名字,不过社区至此开始了整活:

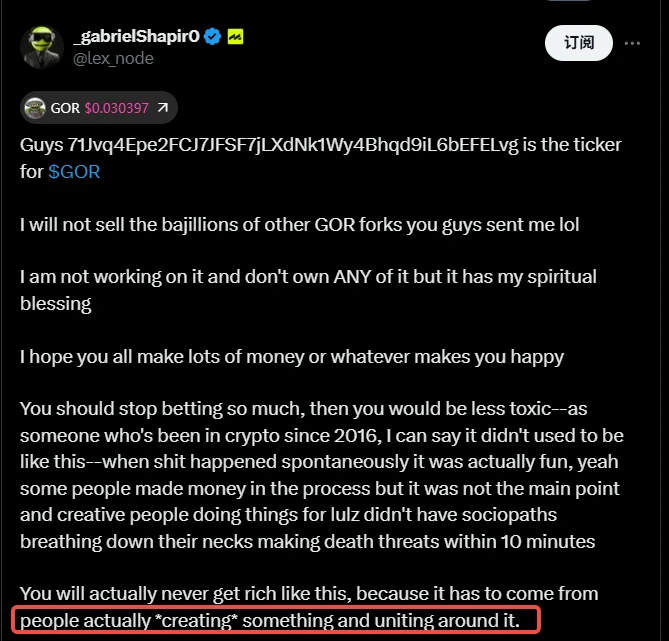

这个讨论贴 6 小时后, @lex_node 就发了一个 gorbagana 的同名代币$GOR,并告诉大家这只是个纯 meme,不要下重注。

的确发个相关 Meme 并不是什么新鲜事,事情到这里也谈不上精彩。

不过,他帖子里的这句话却发人深省:

"你实际上永远不会像这样炒 Meme 致富,因为致富必须来自人们真正*创造*某物并围绕它团结起来"。

在这句话之后,社区里的开发老哥们开始当真了。

Solana 之前在 2022 年就有一个陈年老梗叫做 SQL Chain,实际上是社区调侃 Solana 因高性能而被戏称为“SQL 数据库链”,并一直有那种 Solana 分叉出一个“垃圾版” SQL Chain 的想法。

借着这个 Gorbagana 的玩笑,分叉 Solana 的行动真的开始了。

网友 @Sarv_shaktiman 也做过开发,看到 Toly 的讨论贴和 GOR 代币后少量买了点币,并召集 Milady 项目的开发者团队,决定将这个老笑话变成现实。

只是这个从玩笑到现实的速度,过于快了:

帖子发出 6 小时,代币 GOR 上线;

帖子发出 18 小时后,这几个开发老哥就已经着手开始对 Solana 的代码架构进行逆向工程,试图分叉出一条新的 L1;

帖子发出 24 小时后,Gorbagana Chain 的测试网就上线了,并且配备了自定义 RPC 的功能,以及支持 Backpack 钱包。

48 小时后,Gorbagana 链交易量突破了 1000 万笔,虽然是测试网,但也证明了社区开发老哥们的技术实力。$GOR 的市值峰值也来到了 6000 万美金。

整个过程,有一种久违的加密娱乐气息 ---社区的 Builder,从购买 Meme,到研究区块链架构,再到运行一条 Solana 的分叉链,买了就干,知行合一。

除了分叉了整个 Solana 的代码库做了个新 L1 外,这条链还把 Meme 币 $GOR 当作了原生代币,支持 gas 费的消耗和转账使用。

没有风投、没有营销,只有社区成员们的集体即兴发挥和协作,一个 meme 在 48 小时内变成了一条 L1 的原生代币。

这事算不上多大,但足够有意思。

是那种几年前链上活跃,各种社区项目层出不穷时的有意思。

社区协作 VS 机构孵化

复制一条链,真的那么简单吗?

分叉 Solana 听起来简单,实则有很多让人头疼的事情,比如钱包兼容性。

主流 Solana 钱包如 Phantom 和 Solflare 等因“硬编码”(预设程序只认 Solana 主网和测试网)无法支持 Gorbagana 的自定义链功能,等于把新链孤立在 Solana 的生态之外。

换言之,分叉一个 Solana 可以,但钱包不一定支持。

社区开发老哥们,面临的不是简单抄作业,而是 48 小时内打破这些技术壁垒。

其中,一位叫做 @armaniferrante 的用户,通过使用 Backpack 钱包的“远程过程调用”(RPC,一种让钱包与链通信的协议)自定义功能,让 Gorbagana 在 24 小时内就接入了 Solana 生态,也使得自定义 RPC 功能得以在新链上使用。

回头来看,你可以把这件事看作一个“degen”版的黑客马拉松。没有赛事的组织和规划,全靠群组里的老哥们实时头脑风暴提供讨论和解决方法。

虽然带头的开发老哥可能是因为买了 GOR 币而不得不扩大项目的影响力,但这一整套做法充满了技术极客那种久违的能量:

靠热情填补技术空缺,用协作来对症下药,最终完成一个大项目。

虽然 Gorbagana 整活只上了个测试网,但 48 小时相比来说仍然是神速。考虑到某些机构背书、团队豪华、资金拉满的天王级基建项目动辄几年的项目落地周期,Gorbagana 的社区协作就显得更加难能可贵。

同时,我们不禁也要问,如果全速前进,一条完备的 L1 推出测试网真的要花那么久吗?

草根有自己的的灵活性,社区协作只是为了一个娱乐化的项目,没有 KPI,也没有营销和 TGE 的节奏考虑,相较而言当然更加纯粹;

而机构级 L1 的问世,本身就牵涉着不同轮次投资者的利益。何时上线、何时公布测试网、空投预期和交互模式的 管理,不再是搞定技术那么简单。

更不用说,有时天王级项目代币是否 TGE, 还得看市场行情和情绪的好坏。这些基建项目们更像是一艘大船,装载着万千利益,在风浪中难以迅速决策和掉头。

很久之前,加密有意思的地方也正是靠草根创意而非资本堆砌。

Gorbagana 或许热度不会持续很久,但它至少证明了一件事:

在现在这个沉闷的市场中,活跃的草根从未缺席,缺的或许只是激发他们热情的导火索。