据各大媒体援引知情人士消息,pump.fun 准备以 40 亿美元估值出售 25% 的 PUMP 代币以筹集 10 亿美元。这个价格有吸引力吗?Messari 的 Sunny Shi 为 PUMP 构建了一个估值模型,结果显示其 FDV(完全流通市值)可能达 70 亿美元。如果预测正确,则 PUMP 代币买到就是赚到。但有一个重要前提。以下是他们的估值过程(Sunny Shi 视角,「我们」指 Messari):

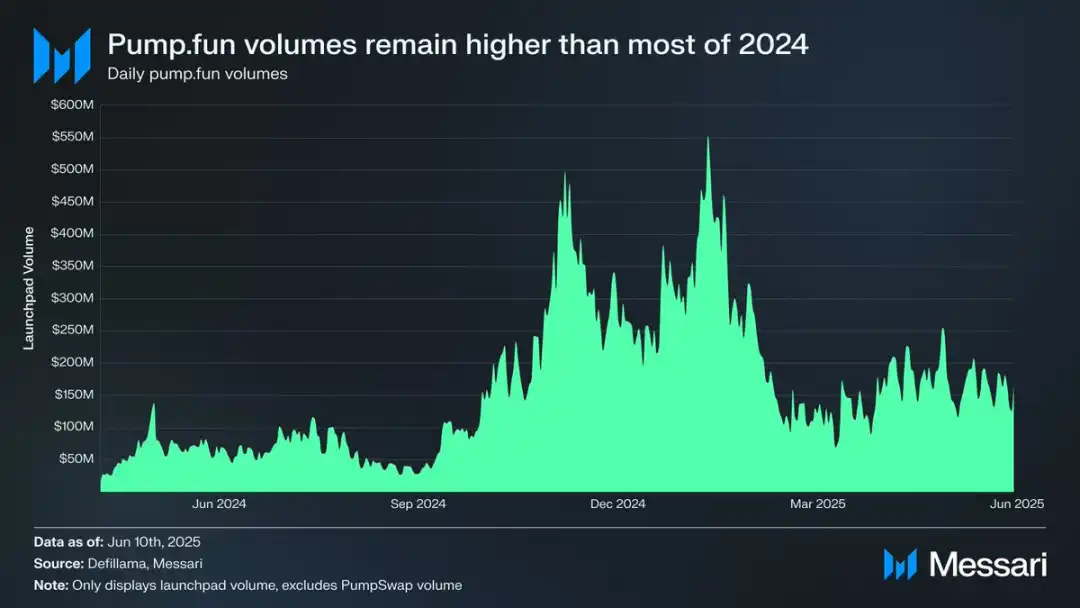

无论你怎么看待迷因币(Memecoin),这个赛道依旧在持续「印钞」。尽管 pump.fun 发币平台的交易量相比年初有所下滑,但仍远高于 2024 年大部分时间的水平。

Pump.fun 的交易量高于 24 年的多数时间,数据:Messari

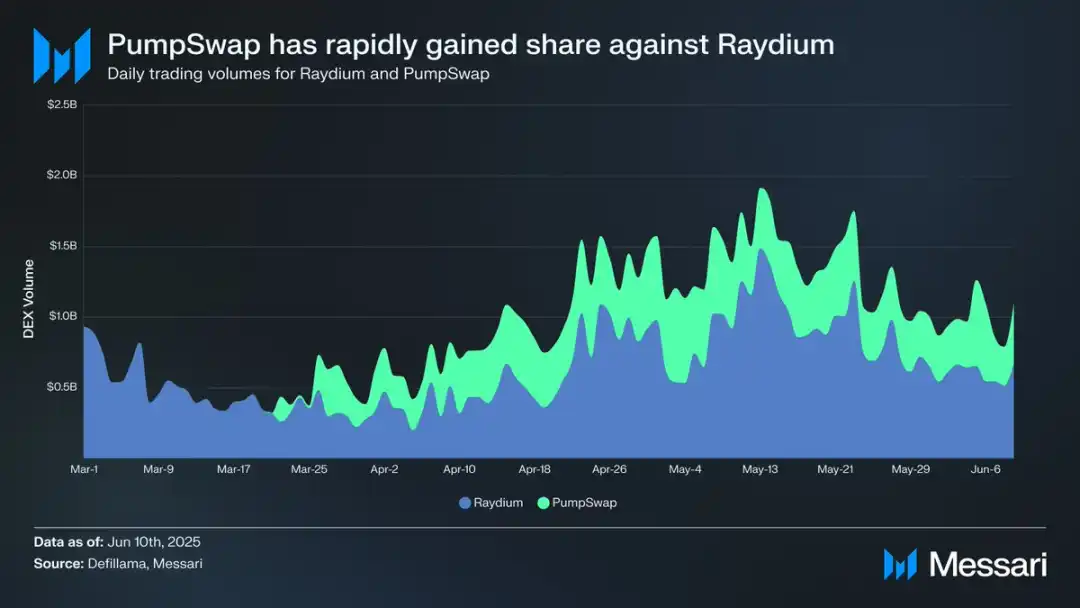

人们可能也低估了 PumpSwap 的成功。这个 DEX 在大约三个月前上线,但已经显著蚕食了 Raydium 在 Solana 上的市场份额。

PumpSwap 与 Raydium 的市场份额对比,数据:Messari

我们的估值方法采用自上而下(top-down)的模型,假设了加密市场整体交易量、Solana 占比、启动平台份额和 PumpSwap 市场份额。这些假设和模型仅对企业客户开放,但我会分享主要结论。

在我们的基本情景(base case)中,我们认为 Memecoin 会在更广泛的加密经济中占据一个细分市场,因为它们比 NFT 更适合投机用途。当然,Solana 生态随着成熟无疑会向新的资产对多元化发展,但这点也很可能成立。

我们认为,即使 pump.fun 在 Solana 生态内占据的份额略有下降,但 PumpSwap 持续增长,pump 项目仍然有望在未来两年内产生约 6.75 亿美元的收入。按 10 倍估值倍数计算,对应的 FDV 为约 70 亿美元。

然而,关键前提是:如果项目方选择一种不透明的代币 / 股权结构,将大部分收入分配给内部人士而非代币持有者,那我们认为当前市场已变得相当谨慎,不会忽视这种糟糕的价值积累方式。在我们的完整报告中,我们提供了估值表格,用于根据代币持有者能获取的收入百分比来评估 PUMP 的潜在价值。

无论市场最终如何判断,这都是一个参与史上最赚钱的加密应用的绝佳机会。现在就看项目团队是否给予代币持有者足够的参与价值(buy-in),使其成为一项值得投资的项目了。

编者注:在 Aevo 的盘前永续交易市场上,此刻 PUMP 的价格为 6 美元,对应 60 亿的 FDV(完全流通市值)。

PUMP 在 Aevo 上的盘前价格