На прошлой неделе крипторынок в основном находился в состоянии консолидации, а быки стремились вернуть контроль. Разбираемся, какие валюты покупали киты в этих условиях

Киты активно скупают некоторые альткоины на волатильном рынке. Возможно, так они готовятся к возможному отскоку. На этой неделе их внимание привлекли Cardano (ADA), ApeCoin (APE) и Toncoin (TON).

Киты и Cardano (ADA)

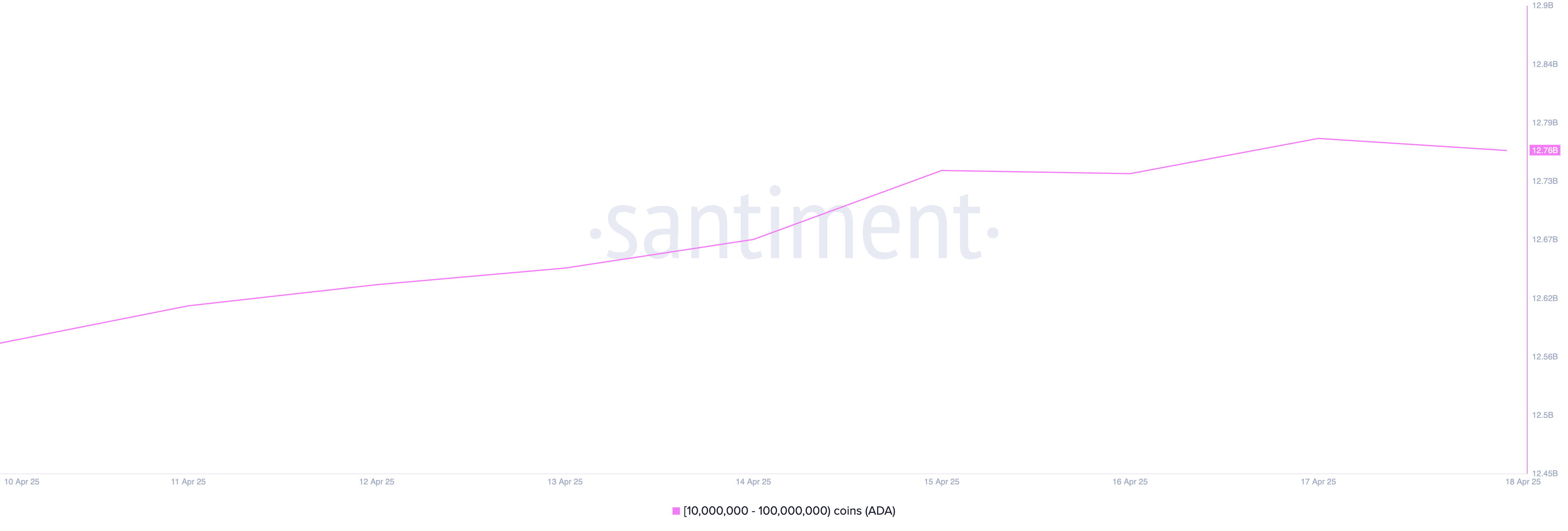

На этой неделе ADA, монета блокчейна первого уровня (L1), привлекла внимание крупных инвесторов. Данные Santiment показывают увеличение числа монет, приобретенных адресами, которые держат от 10 млн до 100 млн ADA.

По данным ончейн-платформы, за последние семь дней эта группа инвесторов приобрела 190 млн ADA (около $2,40 млрд по текущим ценам).

Всплеск покупок произошел, хотя ADA колеблется в диапазоне $0,59 — $0,63. Когда киты увеличивают свои запасы в период консолидации цены, это свидетельствует о доверии к долгосрочной ценности актива.

Такое поведение предполагает возможный бычий импульс, так как крупные держатели ожидают прорыва. Если спрос усилится, ADA может преодолеть сопротивление на уровне $0,63 и подняться до $0,70.

Однако если начнется фиксация прибыли, ADA может снизиться до $0,55.

ApeCoin (APE)

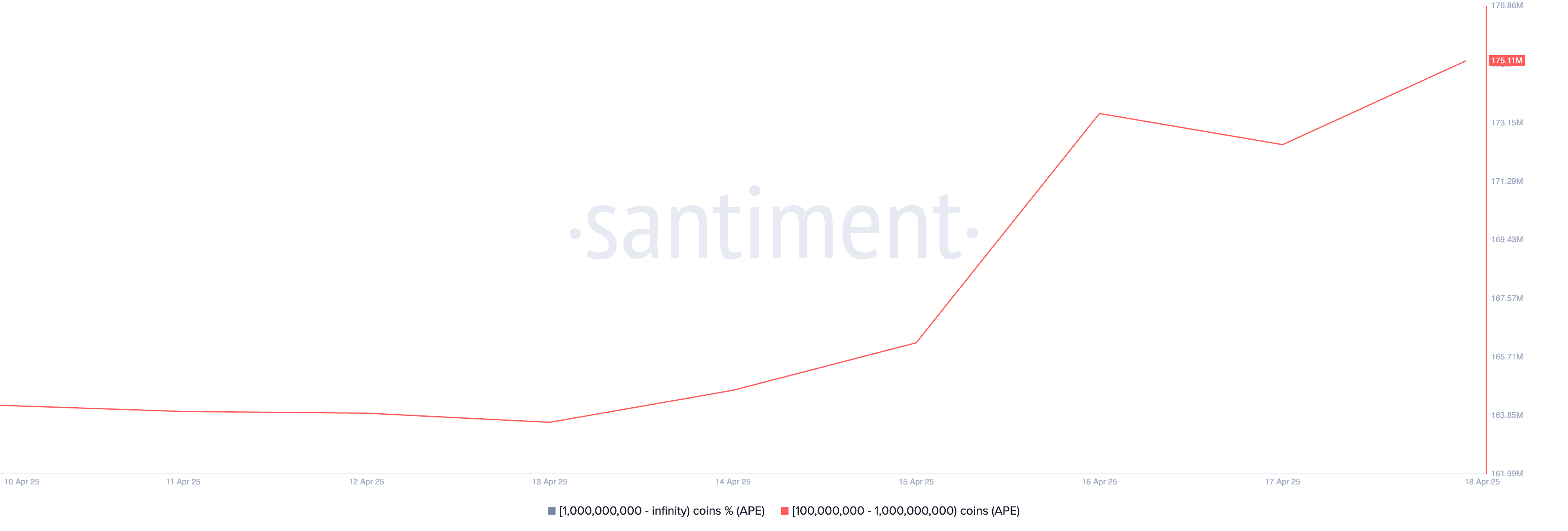

Альткоин APE, связанный с метавселенной, на этой неделе привлек внимание крупных инвесторов. Это привело к умеренному росту его цены на 4% за последние семь дней. По данным Santiment, крупные адреса, которые держат от 100 млн до 1 млрд APE, накопили 11 млн токенов за эту неделю.

Эти инвесторы сейчас держат 175 млн токенов на сумму примерно $75,25 млн по текущим рыночным ценам. Это их наибольшие запасы с декабря 2024 года.

APE может продолжить стабильный рост, если спрос со стороны крупных инвесторов увеличится. Если тренд сохранится, токен может достичь $0,59.

Однако если спрос снизится, цена может упасть до $0,34.

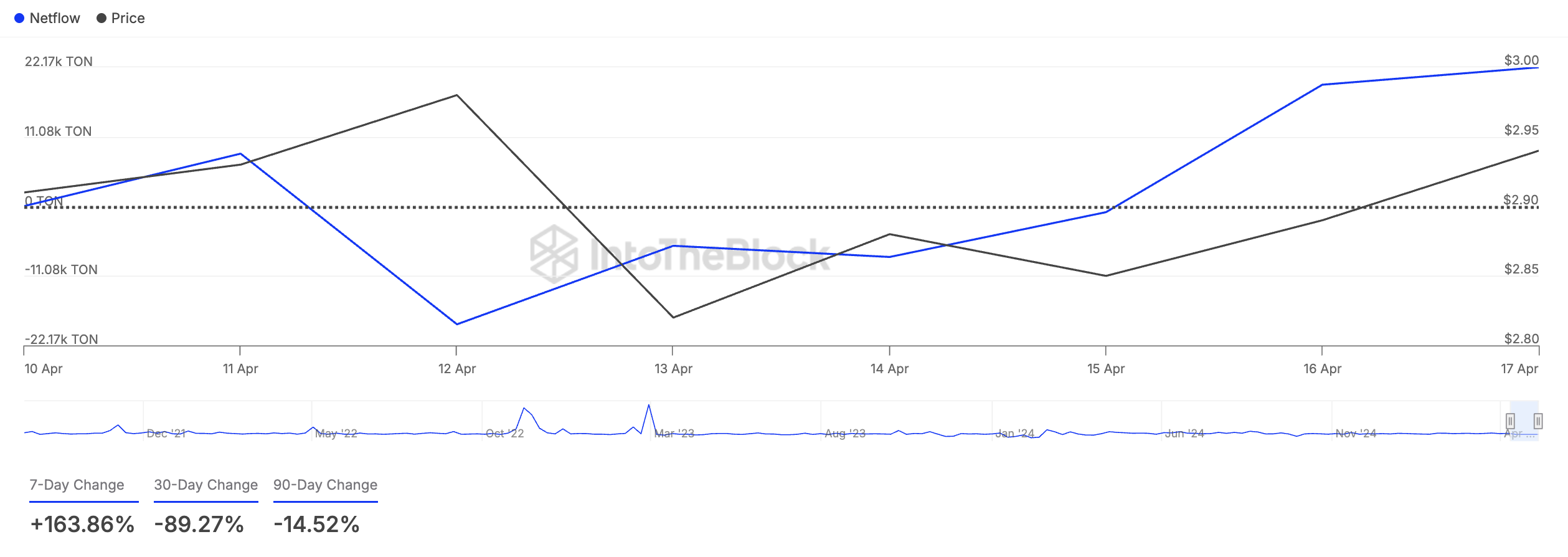

Toncoin (TON)

Токен Toncoin, связанный с «Телеграмом», на этой неделе также заинтересовал китов. Это подтверждается чистым потоком капитала в сегменте крупных держателей. Показатель вырос на 164% за последние семь дней.

Киты TON — это адреса, которые владеют более 0,1% его циркулирующего предложения. Чистый поток показывает разницу между количеством токенов, которые они продают и покупают за определенный период.

Когда показатель растет, это указывает на рост интереса со стороны крупных игроков. Это может подтолкнуть к активности и розничных трейдеров. Это, в свою очередь, может привести к росту цены в ближайшем будущем.

Если киты TON продолжат накапливать актив, его цена может устроить ралли к $3,75.

Однако если распродажи продолжатся, TON может снизиться до $2,35.