Written by: Thejaswini M A

Compiled by: Saoirse, Foresight News

The simplest way to control other people's money is to wait until they let their guard down and stop paying attention. A significant portion of financial institution profits is built purely on people's procrastination and inertia.

Years ago, two economists, Richard Thaler and Shlomo Benartzi, concluded that trying to convince others through argument is a futile endeavor. Instead of exhausting oneself in debate, it's better to design rules that leverage the inertia of inaction to change choices. Clearly, most people are too lazy to actively opt out.

If one had to manually fill out forms to join a retirement savings plan, fewer than half would participate. But once enrollment is set as the default, requiring a manual action to opt out, participation rates instantly soar above 90%. The same principle applies to auto-renewing subscriptions: over half of paying users don't even use the service they're subscribed to. Last week, I subscribed to watch the FIFA World Cup, fully aware I'd completely forget about the service after the tournament.

A key premise of this mechanism: the fund holder and the person designing the product allocation must be two different people. The employer selects the fund menu for the 401(k) plan, and employees are passively enrolled into this allocation framework.

On June 18th, Franklin Templeton filed an application to launch two ETFs, embedding this 'default allocation' logic into Bitcoin investment.

Looking at the broader capital landscape, the protective moat these products can create is actually minuscule.

The decision to buy Bitcoin itself is a major barrier to industry adoption. Even though Trump's appearance at a Bitcoin conference briefly alleviated public concerns, this barrier remains objectively present.

Financial advisors need to actively allocate Bitcoin, explain the decision to clients and compliance departments, and bear all the risk of loss if the price plummets. Due to career risk considerations, the vast majority of advisors deliberately avoid recommending Bitcoin to their clients.

Financial advisors build standardized portfolio models, autonomously selecting underlying funds, and clients passively hold the allocated assets. When clients review their holdings statements, they only see generic labels like 'US Large-Cap Stocks, 40%' and don't delve into what assets are actually held underneath. If an advisor uses this dividend reinvestment version of the fund, the client unknowingly holds Bitcoin.

This product is not designed to trick ordinary retail investors—institutions know retail investors actively review their holdings. This underlying structure is actually tailored for financial advisors.

This is Wall Street's core playbook. The target-date fund industry, which grew to $4 trillion, expanded on this same logic: the default allocation itself is the product; as long as users choose inaction, they automatically hold the asset. Investors who manually enter tickers to select stocks themselves are not covered by this logic, and Franklin doesn't rely on such retail investors. The funds are truly targeting capital managed downstream by other professionals.

The Dividend Reinvestment Plan (DRIP) is the most effortless 'set-and-forget' tool in investing: when a stock pays a dividend, the money doesn't go into your account but is automatically used to buy more of the same stock. You continuously add to positions you already hold, with almost no effort required to manage it—that's what DRIP means.

Franklin has reversed this mechanism: its two funds—the Franklin US Equity Bitcoin Dividend Reinvestment Index ETF and the Franklin US Equity Innovation Sector Bitcoin Dividend Reinvestment Index ETF—will not use dividends to buy more stocks but will directly purchase Bitcoin.

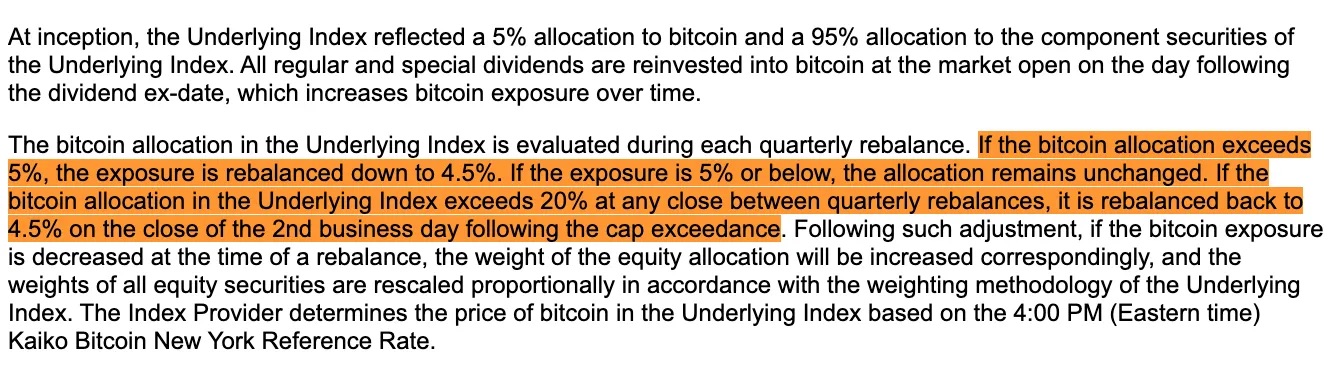

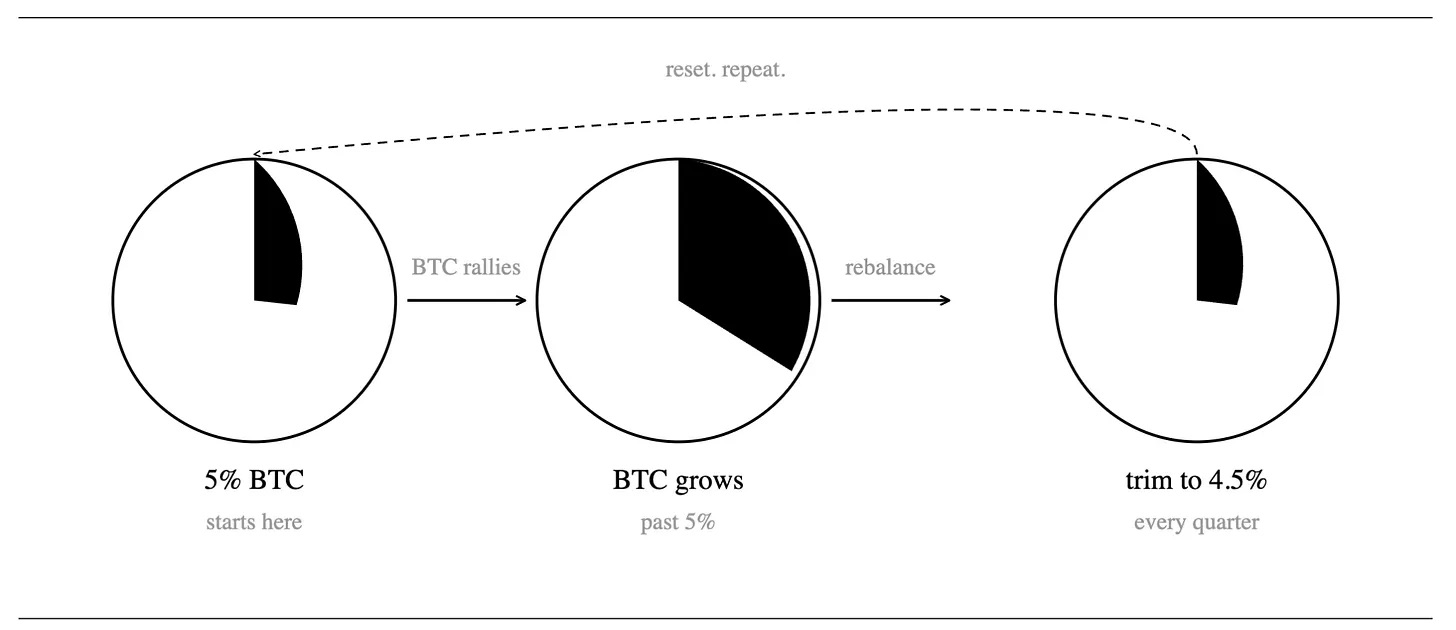

For the Bitcoin allocation, the funds plan to hold spot Bitcoin ETFs, Bitcoin futures, and options. The products have built-in quarterly rebalancing with asymmetric rules: if Bitcoin rises significantly and its weight breaches the 5% target line, it will be reduced to 4.5% during the next quarter's rebalancing. A hard cap is also set, limiting Bitcoin holdings to a maximum of 20% of the fund's total assets.

The initial allocation is 95% stocks and 5% Bitcoin. All dividends distributed quarterly will be used to increase the Bitcoin position. If the Bitcoin price rises and its allocation expands, during the quarterly rebalancing, some Bitcoin will be sold to bring the allocation back down to 4.5%. The proceeds from this reduction will flow back into stock assets.

Even if Bitcoin prices surge wildly between two rebalancing periods, its share in the fund will never break through the 20% red line.

To bypass numerous regulatory processes, the Bitcoin held by the funds will be uniformly held by Franklin's wholly-owned subsidiary in the Cayman Islands. This subsidiary will handle the allocation using spot crypto, futures, and options.

Both funds track proprietary indices customized by VettaFi. Franklin plans to officially launch them on September 1st; the fee section in the filing is blank, and the management fee has not been announced yet.

Setting Aside Rosy Expectations, Facing Reality

While it seems to connect to the Wall Street system, creating new stable Bitcoin buyers with promising prospects, calculating the real numbers reveals that the so-called incremental buying is merely a trickle.

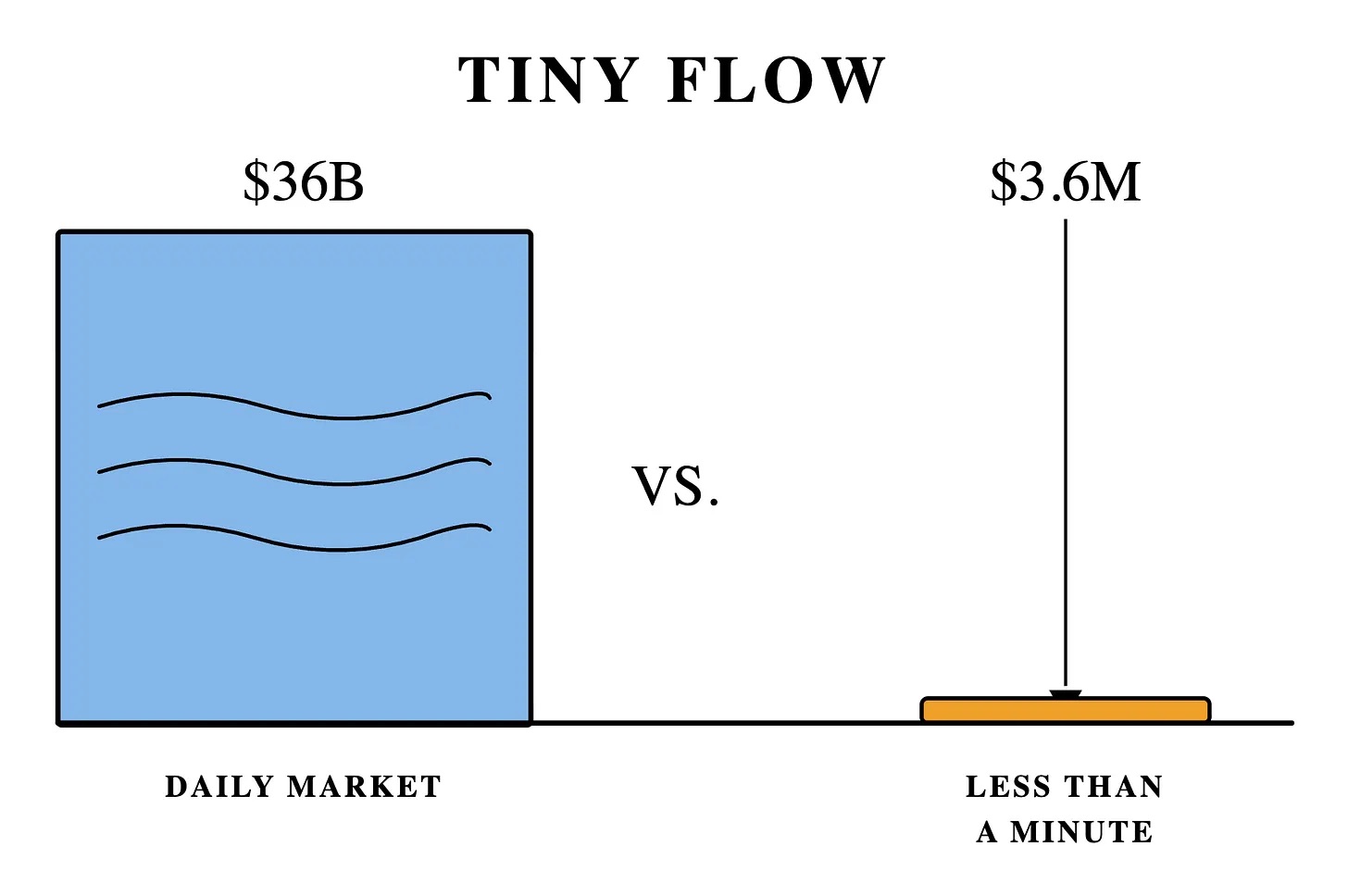

The annualized dividend yield of broad US equity indices is 1.05%, while the innovation sector index yields only 0.52%. Both funds have an initial allocation of 95% stocks and 5% Bitcoin, and only dividends generated by the stock portion are used to buy Bitcoin. Converted, the broad-based fund can only allocate about 1% of its total assets annually to buy Bitcoin, and the innovation fund only 0.5%.

Based on Franklin's existing Bitcoin ETF (size $359 million), the corresponding annual new Bitcoin buying power is only $3.6 million. Bitcoin's daily trading volume is about $36 billion. The fund's entire year of buying volume can be absorbed by the market in less than a minute.

The design of the innovation sector fund hides deeper flaws: it is heavily weighted in stocks like Nvidia, Apple, and Microsoft, which pay very low or no dividends. Since the fund buys Bitcoin solely using stock dividends, it lacks a steady cash flow for continuous additions. Coupled with the reverse mechanism of quarterly rebalancing, once Bitcoin's allocation exceeds 5%, it must be reduced to 4.5%. The higher Bitcoin rises, the harder the fund sells. In a bull market, the selling pressure from continuous disposals could easily offset the tiny buying increment from meager dividends. From its foundational design, this product is destined to struggle with holding an appreciating asset long-term.

On days when Bitcoin performs well, this fund will instead become a passive seller.

Why? Index funds are forced into passive trades by the market. Traders familiar with the fixed trading times and targets of an index can position ahead to profit from arbitrage. Franklin's two funds恰恰 create the opposite scenario: they are programmed, passive, continuous selling tools. The funds buy Bitcoin the day after dividends are received and sell uniformly during quarterly rebalancing. Short-term traders can accurately predict these operation nodes and harvest the fund from both the buying and selling sides.

The selling pressure from a single fund of similar size is minuscule, like a mosquito bite. But once similar products form a complete category, the cumulative selling pressure will become significant. If a large amount of similar capital floods the market, every Bitcoin price rise would face continuous selling, creating a difficult-to-break price ceiling.

Beyond this core default allocation playbook, the filing subtly incorporates three other clever designs:

- Compliance Evasion Tactics. Internal regulations at many financial institutions prohibit allocating to cryptocurrencies. However, this fund is externally labeled merely as a 'US Large-Cap Equity Product,' allowing advisors to allocate it compliantly for clients, indirectly achieving Bitcoin exposure.

- Offshore Structure Compliance Solution. Bitcoin is uniformly held by a wholly-owned subsidiary in the Cayman Islands. This is a common compliance method for public funds holding commodity-like assets. It doesn't disrupt the fund's existing tax qualifications, is legal, and is widely used in the industry.

- Tax Legacy Issue. Dividends are automatically converted to Bitcoin before they ever reach you, but this dividend income is still taxable. The funds are locked within the crypto asset, forcing you to use additional personal cash to pay taxes on dividend income that never hit your account.

For this model to truly take shape, such funds must become the default allocation for pensions or be positioned right next to the default asset pool. With the passage of the Pension Protection Act of 2006, employers received legal support to automatically enroll employees, defaulting them into corresponding funds.

Back then, only 5% of 401(k) plans offered target-date funds. Today, the coverage rate is 96%, and the industry's total size has exploded from $100 billion to $4 trillion.

In August 2025, Trump signed an executive order officially lifting restrictions, allowing 401(k) plans to allocate to cryptocurrencies. In March 2026, the US Department of Labor issued a new rule draft stating that if a plan fiduciary includes alternative assets like cryptocurrencies in the pension options menu, they can enjoy liability protection.

The public comment period for the draft ended on June 1st. For formal regulations to be enacted by the end of this year, the relevant processes must be completed before then. Compared to adding optional crypto products for investors, directly setting crypto assets as the pension default allocation faces higher implementation hurdles. Therefore, regardless of the final rule text, corporate legal departments generally judge that most employers will choose to wait and see, acting only after court precedents confirm the safe harbor liability clauses.

The core of this system is never about convincing anyone to actively buy Bitcoin. Human attention is the scarcest resource in the world. Any model that eliminates the need for thought and runs automatically on inertia will ultimately prevail.

The entire system just needs to leverage people's laziness.