原文作者:Vitalik Buterin

编译:Luke,火星财经

以太坊的目标自始至终未曾改变:构建一个全球性的、抗审查且无需许可的区块链。这个为去中心化应用打造的自由开放平台,其根基与GNU/Linux、Mozilla、Tor、维基百科等伟大自由开源软件项目共享相同的原则(当代可称为"再生主义"与"密码朋克伦理")。

过去十年间,以太坊进化出另一个让我极为珍视的特质:除了密码学与经济机制的创新,它还是一项社会技术的创新。以太坊生态系统本身就是一个正在运行的、活生生的示范,展示了一种全新、更开放且去中心化的协作建设方式。政治哲学家Ahmed Gatnash如此描述他在Devcon的体验:

"...这是对另一种可能世界的惊鸿一瞥——一个几乎不存在守门人、不依附于遗留系统的世界。在这里,社会标准地位体系被彻底倒置:最受尊崇的是那些将所有时间投入专注解决特定技术难题的极客,而非在传统机构等级制度中玩弄权术向上攀爬的人。这里几乎所有的权力都是软实力。我发现这种生态既美丽又充满启发性——它让你感觉在这样的世界里一切皆有可能,而这样的世界实际上触手可及。"

技术工程与社会工程本质上是相互交织的。如果在时间T拥有一个去中心化的技术系统,但由中心化的社会进程维护它,就无法保证在时间T+1该系统仍保持去中心化。同理,社会进程也通过技术以多种方式维持生命力:技术吸引用户,由技术实现的生态系统为开发者提供留存激励,它使社区保持务实并专注于建设而非空谈。

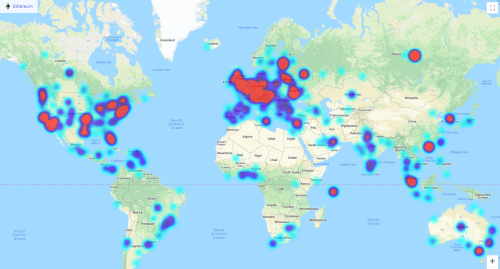

Where you can use Ethereum to pay for things around the world, Oct 2024. Source.

经过十年由技术与社会双重属性驱动的不懈努力,以太坊已具备另一关键品质:以太坊正在大规模地为人们提供实用价值。数百万人持有ETH或稳定币作为储蓄形式,更多人用这些资产进行支付:我本人就是其中之一。它拥有有效的隐私工具,我用来支付保护互联网数据的VPN费用。它拥有ENS——DNS的强健去中心化替代方案,更广义上是公共密钥基础设施。它拥有可用且易用的Twitter替代品。它提供DeFi工具,为数百万人提供比传统金融更高收益的低风险资产。

五年前,我不愿谈论后者的应用场景,主要原因在于:基础设施与代码尚未成熟,我们刚从2016-17年大规模智能合约攻击的创伤中恢复不久。如果每年有5%的概率遭遇-100%年化收益率(本金全损),那么7% APY相比5% APY的优势将毫无意义。此外,当时交易手续费过高,难以支撑规模化应用。如今,这些工具已展现出时间考验下的韧性,审计工具质量显著提升,我们对它们的安全性日益充满信心。我们已了解哪些做法应当避免。L2扩容正在发挥作用。交易手续费已持续近一年保持低位。

我们必须继续强化以太坊的技术社会属性与实用价值。若仅有前者而无后者,我们将退化为日益无效的"减速主义"(decel)社区,只能在风中徒劳呐喊主流势力的不道德,却无力提供更好的替代方案。若仅有后者而无前者,我们就会重蹈华尔街"贪婪即美德"的覆辙——而这正是许多人投身于此所要逃离的。

上述二元性带来诸多启示。本文中,我将聚焦对以太坊用户在中短期内至关重要的具体议题:以太坊的扩容战略。

L2的崛起

当前,我们选择的扩容路径是Layer 2协议(L2s)。2025年的L2已远非2019年的早期实验品:它们已达成关键去中心化里程碑,守护着数十亿美元价值,目前正将以太坊交易处理能力提升17倍,手续费亦同比下降相近幅度。

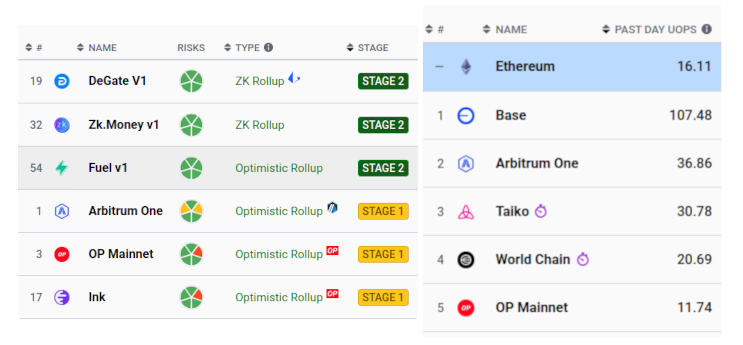

Left: stage 1 and stage 2 rollups. On Jan 22, Ink has joined as the sixth stage 1+ rollup (and third full-EVM stage 1+ rollup). Right, top rollups by TPS, with Base leading at roughly 40% of Ethereum's capacity.

这些进展正及时应对成功应用的浪潮:各类DeFi平台、社交网络、预测市场、Worldchain(现拥有1000万用户)等创新产品。曾被视作死胡同的"企业区块链"运动(因2010年代联盟链失败而衰落),正借助L2重获新生,Soneium即为典型范例。

这些成功也印证了以太坊去中心化模块化扩容路径的社会维度:无需以太坊基金会亲自招揽所有用户,已有数十个独立实体主动承担此任。这些实体也为技术做出关键贡献,没有它们,以太坊远不可能取得今日成就。由此,我们终将接近逃逸速度。

挑战:规模与异构性应对

当前L2面临两大核心挑战:

- 规模:现有blob空间勉强满足当前L2与应用需求,远不足以支撑未来需求

- 异构性挑战:早期以太坊扩容愿景设想区块链包含多个分片,每个分片作为EVM副本由部分节点处理。理论上,L2正是该路径的实现。但实践中存在关键差异:每个分片(或分片组)由不同主体创建,被基础设施视为独立链,且常遵循不同标准。如今,这导致开发者与用户面临可组合性与体验问题。

首个问题属于易理解的技术挑战,且有明确(但难实现)的技术解决方案:为以太坊提供更多blob。此外,短期内L1也可进行适度扩容,包括权益证明改进、无状态与轻验证、存储、EVM与密码学优化。

第二个问题(公众关注焦点)本质是协调问题。以太坊并非首次应对多团队复杂技术协作:我们曾完成合并(The Merge)。但此次协调更具挑战性,因涉及更多元的主体与目标,且进程启动较晚。尽管如此,我们生态曾解决过类似难题,此次亦能成功。

可能的捷径与取舍

一种扩容捷径是放弃L2,通过大幅提高gas limit(多分片或单分片)在L1完成所有操作。但此方案将过度牺牲以太坊现有社会结构的优势——该结构有效整合了不同形式的研究、开发与生态建设文化。因此,我们应坚持既定路线,继续以L2为主扩容,同时确保L2真正兑现其承诺。

这意味着:

- L1需加速blob扩容

- L1需适度扩容EVM并提高gas limit,以应对L2主导时代仍需处理的L1活动(如证明、大规模DeFi、存取款、极端大规模退出场景、密钥库钱包、资产发行)

- L2需持续提升安全性:分片应有的安全保证(包括抗审查、轻客户端可验证性、无固有信任方)须在L2实现

- L2与钱包需加速推进互操作性标准化:包括链特定地址、消息传递与桥接标准、高效跨链支付、链上配置等。使用以太坊应如同使用单一生态系统,而非34条不同区块链

- L2存取款时间需大幅缩短

- 在满足基本互操作性前提下,L2异构性有益:部分L2将是基于最小化治理的Rollups,运行与L1完全相同的EVM;其他L2将尝试不同虚拟机;还有些将充当利用以太坊为用户提供额外安全保证的服务器。我们需要覆盖该光谱各环节的L2

- 需明确ETH经济学设计:确保即便在L2主导时代,ETH仍持续捕获价值,理想情况下覆盖多种价值累积模型

扩容:Blob、Blob、Blob

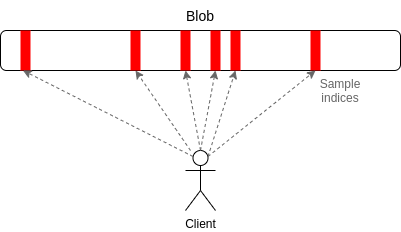

通过EIP-4844,当前每个slot包含3个blob(数据带宽384 kB/slot)。速算显示这相当于32 kB/s,每笔交易链上占用约150字节,故处理能力约210 TPS。L2beat数据与此高度吻合。

计划于3月发布的Pectra升级将blob数量翻倍至6个/slot。

当前Fusaka的核心目标是专注PeerDAS,理想情况下仅包含PeerDAS与EOF。PeerDAS可再将blob数量提升2-3倍。

此后目标将持续增加blob数量。采用2D采样技术后可达128 blobs/slot,后续可继续提升。配合数据压缩改进,最终可实现链上10万TPS。

以上均为2025年前既有路线图的重申。关键问题在于:如何加速该进程?我的答案是:

- 更明确地暂缓非blob相关功能开发

- 更清晰传递blob扩容目标,将相关P2P研发作为人才引进重点

- 允许stakers直接调整blob目标(类似gas limit机制),无需等待硬分叉即可响应技术进步

- 可探索更激进方案(在低资源stakers承担更多信任假设前提下加速blob扩容),但需谨慎

提升安全性:证明系统与原生Rollups

当前存在3个Stage 1 Rollups(Optimism、Arbitrum、Ink)与3个Stage 2 Rollups(DeGate、zk.money、Fuel)。多数活动仍发生在Stage 0 Rollups(即多签系统)。必须改变此现状。进展缓慢的主因在于:构建证明系统并获得足够信心以放弃训练轮(training wheels)、完全依赖其保障安全,极具挑战性。

实现路径有二:

- Stage 2 + 多证明者 + 形式化验证:采用多证明系统冗余,通过形式化验证(参见Verified ZK-EVM计划)确保安全性

- 原生Rollups:将EVM状态转换验证纳入协议自身(如通过预编译,参见研究[1][2][3])

当前应并行推进两者。对Stage 2 + 多证明者 + 形式化验证路径,路线图相对明确。主要实践加速点在于加强软件栈协作,减少重复工作同时提升互操作性。

原生Rollups仍处早期阶段。需深入探索如何设计最大化灵活性的原生Rollup预编译。理想目标是:不仅支持EVM精确克隆,还能兼容各类EVM变体,使采用修改版EVM的L2仍可使用原生Rollup预编译,仅需为修改部分自带证明者。该机制可应用于预编译、操作码、状态树等组件。

互操作性与标准

目标是让用户在不同L2间转移资产、使用应用的体验如同操作同一区块链的不同分片。现有路线图已明确数月:

- 链特定地址:地址应包含链标识符与账户信息。ERC-3770是早期尝试,现有更复杂方案将L2注册表移至以太坊L1

- 标准化跨链桥与消息传递:应建立标准化的跨链证明验证与消息传递机制,且这些标准仅需信任L2自身证明系统。依赖多签桥的生态不可接受。若某项信任假设在2016式分片设计中不存在,则今日亦不可接受

- 加速存取款时间:使"原生"消息传递耗时从数周缩短至分钟级(最终目标单slot)。这需要更快ZK-EVM证明者与证明聚合技术

- L2同步读取L1状态:参见L1SLOAD、REMOTESTATICCALL提案。这将极大简化跨L2互操作,并助力密钥库钱包

- 共享排序与其他长期工作:基于Rollups的部分价值源于其在此领域的高效性

只要满足上述标准,L2仍可在虚拟机、排序模型、安全与规模权衡等方面保持差异性。但必须向用户与应用开发者明确其安全等级。

为加速进展,大量工作可由跨生态实体(以太坊基金会、客户端开发团队、主流应用团队等)承担。这将减少协调成本,使标准采用更易推进,因为单个L2与钱包需完成的工作量将减少。但作为以太坊的延伸,L2与钱包仍需在功能实现与用户体验环节持续发力。

ETH经济学

我们应采取多管齐下策略,覆盖ETH作为"三相点资产"价值来源的所有主要可能性:

- 巩固ETH核心资产地位:广泛共识支持ETH作为以太坊(L1+L2)经济体系首要资产,鼓励应用采用ETH作为主要抵押品

- 推动L2费用与ETH挂钩:可通过销毁部分费用、永久质押并将收益捐赠生态公共品等机制实现

- 支持基于Rollups的MEV价值捕获:但不应强制所有Rollups采用此模式(因并非适用所有应用),也不应假定单凭此解决所有问题

- 扩容blob与探索blob定价机制:举例而言,若blob数量增至128个且30天平均费用维持当前水平(假设需求同步增长),以太坊年销毁量将达713,000 ETH。但需注意此类理想需求曲线并非必然

结论:前行之路

以太坊已作为技术栈和社会生态系统成熟发展,使我们更接近一个更加自由和开放的未来——数亿人将能够从加密资产和去中心化应用中受益。然而,仍有大量工作亟待完成,现在正是加倍努力的时刻。

如果你是L2开发者,请为以下领域贡献力量:开发工具以使blob扩容更加安全,编写代码以扩展EVM的执行能力,以及实现功能和标准以使L2更具互操作性。如果你是钱包开发者,请同样积极参与标准的贡献与实施,使用户体验更加无缝,同时确保生态系统的安全性和去中心化程度与以太坊仅作为L1时相当。如果你是ETH持有者或社区成员,请积极参与这些讨论;仍有许多领域需要积极的思考和头脑风暴。以太坊的未来取决于我们每个人的积极参与。

声明:本内容为作者独立观点,不代表 CoinVoice 立场,且不构成投资建议,请谨慎对待,如需报道或加入交流群,请联系微信:VOICE-V。