原文作者:Frank,PANews

2016 年 ICO 募集了 82 万枚 ETH 的项目 Golem Network 最近频繁出售 ETH 备受关注,截至 7 月 8 日,近期累计出售了 3.6 万枚 ETH,价值约 1.145 亿美元。结合此前创造行业内最大的 ICO 案例的 EOS 创始公司至今仍持有 14 万枚比特币,价值约 80 亿美元。

投资者忽然发现,当年自己争先恐后投资的那些项目,团队有些都已销声匿迹, 持币不动的项目反而赚的盆满钵满。PANews 就 2016 ~ 2017 年 ICO 最火的 10 个项目的资产状况做了一个盘点,发现所有的项目投资回报均不及持币 BTC 和以太坊。

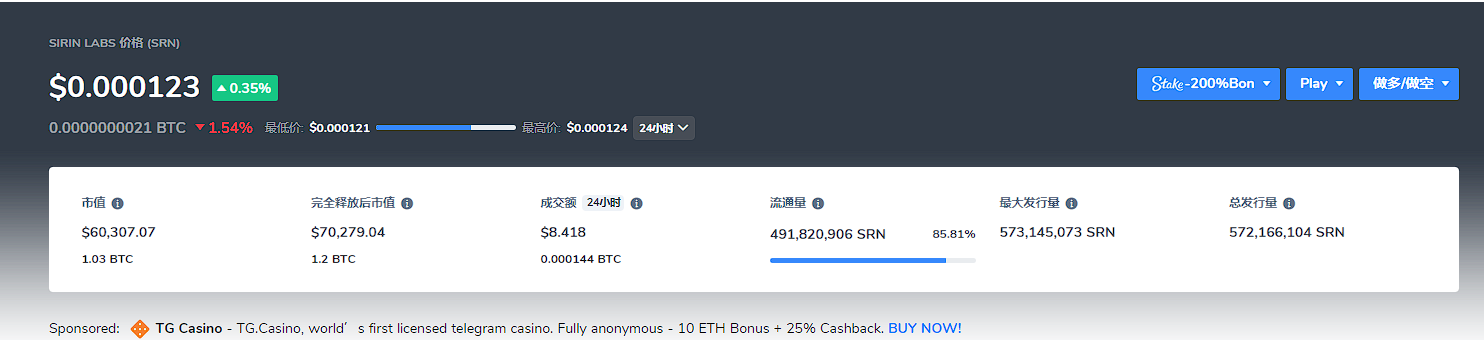

Sirin Labs:融资 1.57 亿,代币市值仅 7 万美元

融资额与发展现状反差最大的莫过于 Sirin Labs,该项目于 2017 年通过 ICO 的形式融资约 1.58 亿美元。成为当年 ICO 最大金额的明星项目之一,其所发现的代币为 SRN,目前的市值仅剩 7 万美元, 24 小时成交额仅为 8 美元。

Sirin Labs 是最早瞄准Web3手机产品的公司,早在 2017 年就以区块链智能手机 Finney 为噱头在 ICO 市场狂揽 1.58 亿美元融资, 2018 年足球运动员梅西还为这款加密手机进行了代言。好景不长, 2019 年 Sirin Labs 被曝出因手机销售不佳,裁员 25% 还有拖欠工厂工钱的消息。2021 年,Sirin Labs 的投资人被起诉利用 ICO 欺诈,挪用超过 2.5 亿美元。

如今,Sirin Labs 的社交媒体账号已经超过 3 年未更新了,评论区里仅留下“骗子”的骂声。

EOS:史上最高的 ICO 创造最富有的 Block.one

EOS 创造了一个 ICO 的募资高峰,这个记录至今仍未能被打破。2017 年,凭借 BM 的明星光环和李笑来的背书。EOS 以以太坊杀手、第三代公链之名获得超过 40 亿美元的融资,成为迄今为止加密领域 ICO 金额最高的项目。

而 EOS 背后的公司 Block.one 随后将募集的 ETH 均换成了 BTC,持有量一度超过 16.4 万枚,超过比特币持有大户微策略公司。据最新数据,Block.one 公司仍持有超过 14 万枚比特币,总价值超过 80 亿美元。

2022 年,EOS 基金会曾多次尝试通过法律手段让 Block.one 归还 41 亿美元,并将 EOS 转型为 DAO 组织。今年 4 月份,EOS 基金会尝试推出新的代币经济学,但市场似乎已经彻底抛弃了这个曾经的公链新星,价格自 4 月份又下跌了近 40% 。如今,EOS 代币的市值仅为 7.8 亿美元,不及 Block.one 持有的比特币价值十分之一。

Tezos: 代币市值不如基金会资产多

公链 Tezos 在 2017 年通过 ICO 获得了 2.32 亿美元的投资,虽然网传 Tezos 基金会持有 1.75 万枚比特币,但 PANews 据 Tezos 基金会 2024 年 3 月的报告显示,该组织目前仍持有价值 2.95 亿美元的 BTC,以当时的 BTC 价格计算,数量约为 5000 枚左右。不过,Tezos 当时在 ICO 时共募集了 65, 681 枚比特币、 36.1 万枚以太坊。这些代币如今的价值约合 48 亿美元,而 Tezos 代币 TXZ 目前的总市值约为 7.4 亿美元,也仅为筹款金额的 3 倍,甚至不如 Tezos 基金会的 7.6 亿资产。

Polkadot:仍持有 30 万枚以太坊未售出

最近,公链 Polkadot 因上半年财报引发热议, 8700 万美元的推广费支出和 110 万美元的收入引发了社区的担忧。似乎, 8700 万的推广费用不及一份财报引发的话题更高。作为 2017 年的明星项目,Polkadot 在当年的融资额就已达到 1.4 亿美元,募集超过 42.9 万个以太坊。据链上数据显示,目前 ICO 的智能合约地址中仍持有 30.6 万枚以太坊,价值约 9.3 亿美元。因此,外界对 Polkadot 金库的担忧似乎是多余的。这部分的以太坊代币从最初至今仍未有售出。

Bancor:从无人不知到无人问津

去中心化交易协议 Bancor 在 2017 年通过 ICO 募集了约 39 万枚以太坊,价值超 1.5 亿美元,超过了 The DAO 的募资金额。这些代币目前的价值约为 11 亿美元,而 Bancor 的代币 BNT 的市值则仅剩约 7000 万美元,对于当时投资的用户来说,这个结果显然是难以接受的。

Golem:精打细算,资产越卖越多

Golem Network 是非常早期的一个 ICO 项目,早在 2016 年 Golem Network 就提出去中心化算力市场这一概念,到了 2024 年,Golem Network 出名的并非具有前瞻性的市场部署,而是擅长理财的持币策略。2016 年 Golem Network 曾通过 ICO 募集了 82 万枚以太坊,是除了 EOS 之外募集以太坊最多的项目。Golem 的项目进展虽然一直不温不火,但项目方并未像其他团队一样快速将 ETH 变卖,而是在多年内少量多次的出手。从最早的 ICO 价值 900 万美元,到 2019 年 6 月,虽然持币数量降至 36.9 万枚,但价值却超过 1 亿美元。再到目前持币数量降至 12.5 万枚,总价值还有 3.9 亿美元。坐上以太坊价格增长的红利,Golem 的资产可谓是越卖越多。而当时用 11 美元的 ETH 投资 Golem 的人不知作何感想。

TenX:项目方一波变现,市值仅剩 164 万美元

支付项目 TenX 在 2017 年募资了超过 8000 万美元,共 245832 个以太坊。不过项目方似乎对加密市场没有太大的信心,在 ICO 后一个月就开始陆续操作将大部分的代币通过交易所出售。目前该项目的代币 PAY 市值仅剩 164 万美元。

Filecoin:去中心化存储的明星仍有余热

Filecoin 作为去中心化存储的热门项目,也是 2017 年融资金额最高的项目之一。Filecoin 通过 ICO 募集了 2.53 亿美元。时至今日仍有不少加密投资人通过矿机挖取 FIL 代币。从结果来看,FIL 代币当前的市值约为 22 亿美元,在 2017 年的明星项目中仅次于 Polkadot。

Qtum:一盘录音带跌下神坛

Qtum 是 2017 年红极一时又饱受争议的有一个项目。从 ICO 的金额来看,Qtum 1560 万美元的金额并不算多,而 2018 年量子链的价格飙升使得该项目成为知名的区块链项目。但随着李笑来的录音曝光,Qtum 创始人的形象也被拉下神坛,从此 Qtum 一蹶不振。Qtum 筹集了 11000 枚 BTC 和 75000 枚 ETH,如今的价值超过 8.7 亿美元。远超 QTUM 代币市值的 2.4 亿美元。

Status:当年一币难求,如今万幸未投

Status 于 2017 年完成了 1.05 亿美元的 ICO 融资,共计筹款 30 万枚 ETH。自 2017 年以来,项目陆续将手中所持有的代币卖出,目前仍持有 1.7 万枚以太坊,价值约 5400 万美元。其代币 SNT 的市值约为 1.5 亿美元。Status 在 2017 年火爆的程度也是非比寻常,据官方透露,ICO 退回的 ETH 高达 34.7 万枚,比筹集的数量还多。不知这些没有成功上车的投资人现在是否庆幸自己没能用手中的 ETH 换了 SNT。

总结

除了上述列举的项目,在 2016 ~ 2017 年火热的 ICO 时代还有大量的项目,不少已经彻底停运,在市场中沉寂。回顾历史总是有意义的,从盘点的 10 个项目来看,这些项目无疑是那个时代最耀眼的明星,顶着名人光环,轻而易举的获取巨额投资。时间走过 7 年的时间,当年宣称要打造下一个比特币和以太坊的项目则又换了一批选手。这也不禁引发我们的思考,再过 7 年今天的明星项目还有多少能存在于大众视野,又有谁能兑现承诺或是靠着融资苟活。