作者:加洋

2026 年 2 月,bot.ai 在域名交易平台 Sedo 以 120 万美元成交,是 .ai 后缀至今公开记录里第一笔七位数交易。买家身份没披露,卖家据说是一位叫 Philipp Michel 的域名投资人。这个域名此前页面上只有一行字:想买 bot.ai 吗?

.ai 是加勒比海上一座 1.5 万人小岛的国家代码后缀。这座小岛叫安圭拉,英国海外领地,经济主要靠高端旅游,每年秋天还要应付飓风季。2025 年,它从注册和续费 .ai 域名里收了 9,300 万美元,占政府预算的 47%。

图丨安圭拉的位置(来源:Britannica)

今年 1 月,全球平均每天有 2,008 个新的 .ai 域名被注册,每 43 秒一个。

从不到 1% 到 47%

1995 年,互联网编号分配机构按照国际标准化组织的国家代码列表,给每个国家和地区指派两位字母的后缀。安圭拉分到了 .ai,邻岛安提瓜分到了 .ag。当时没人想过这两个字母后来会值多少钱。安圭拉前总理 Ellis Webster 后来反复说,“这是纯粹的运气”。

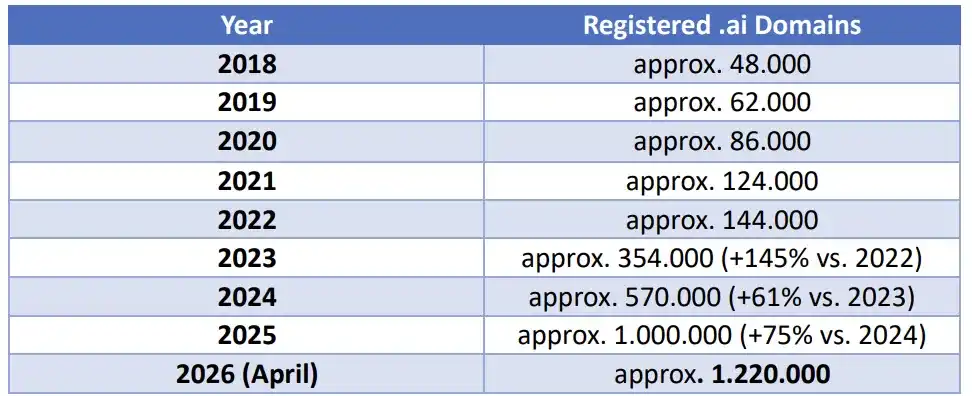

2018 年,安圭拉 .ai 注册收入是 290 万美元,占国家预算 4%。2022 年是 770 万美元,6%。这个数字在 2022 年 11 月之前一直平缓。直到那一个月,OpenAI 推出了 ChatGPT。

2023 年,.ai 收入跳到 3,200 万美元,占预算 21%。2024 年 3,900 万美元,23%。2025 年 9,300 万美元,47%。三年之内,它从一项边角税源跃升为与旅游业并列的财政支柱,后者贡献了 GDP 的 37%。

“AI 真正爆发之前,.ai 收入占国家收入的比例不到 1%。2023 年涨到 25% 到 27%,到 2025 年是 47% 左右。”安圭拉基础设施与通讯部部长 Jose Vanterpool 在年度财政说明里这样总结。

2025 年的跃升还有一层叠加因素。.ai 域名最低注册期是两年,2023 年那一波 ChatGPT 之后涌入的注册者,集中在 2025 年迎来第一次续费。Domaintechnik 创始人 Fabian Ledl 解释,.ai 续费率约 90%,意味着 2023 年的注册暴涨在 2025 年第二次进入了财政账本。按照原本的节奏,安圭拉政府 2024 年底预测 2025 年 .ai 收入应该为 1.32 亿东加勒比元(约 4,884 万美元)、2026 年 1.386 亿、2027 年 1.4553 亿,但 2025 年实际收入达到 2.5 亿东加勒比元,几乎是政府自己预测的两倍。

图丨.ai 域名的注册量(来源:Domaintechnik)

后市场的成交价格也在同步抬升。bot.ai 之前的纪录是 wisdom.ai,2025 年 10 月以 75 万美元成交。再往前是 you.ai,70 万美元,买家是美国软件公司 HubSpot 联合创始人 Dharmesh Shah。他对媒体说自己当时有“一个让人创建数字分身去帮自己做事的产品想法”。

再下来是 cloud.ai 60 万、blockchain.ai 40.5 万、law.ai 35 万。Escrow.com 的 CEO Matt Barrie 还透露过更夸张的一桩:某个 .ai 域名以 30 万美元转手,几个月后又以 150 万美元卖掉,具体名字至今未披露。

不过对照起来,.ai 的价值其实并不算特别高。2026 年 2 月公开的 AI.com 成交价是 7,000 万美元,.ai 后缀至今最高的公开成交价只有它的不到 2%。Dharmesh Shah 自己也说,长期看 .com 的价值会比 .ai 维持得更好、更久。他买 .ai 主要是因为合适的 .com 拿不到时,这是一个还能传达 AI 含义的次优选择。

整个 .ai 生态都是建立在“次优”这个位置上的。.com 仍然是互联网命名的默认共识,.ai 是 AI 公司在 .com 拿不到时的备选。这层关系让 .ai 的溢价能力跟 AI 周期绑得更紧。

图瓦卢交过的那笔学费

太平洋上的图瓦卢 1998 年就走过相似的路。

它拿到的是 .tv,恰好是 television 的缩写。在视频流媒体兴起之前,这两个字母就已经是营销资产。当时图瓦卢政府跟一家加拿大公司签了排他协议,对方承诺一次性支付 5,000 万美元,这笔钱从未到账。后来合同辗转到 Idealab、Verisign,2021 年再转给 GoDaddy。

Verisign 时期,图瓦卢拿到的是固定费用加销售分成:每年 220 万美元,外加销售额超过 2,000 万美元部分按 5% 提成。结构稳定,天花板很低。2010 年前后,图瓦卢财政部长 Lotoala Metia 公开抱怨 Verisign 给的钱是“花生米”。直到 2021 年换约 GoDaddy,年收入才接近 1,000 万美元。

安圭拉的合同结构跟图瓦卢相反。2024 年 10 月,它与美国域名注册商 Identity Digital 签了五年协议,明确以收入分成为主,而非买断。Identity Digital 的分成据 BBC 报道约为 10%,剩下的归安圭拉财政。2025 年 1 月,Identity Digital 正式接管 .ai 注册业务,把所有 .ai 域名的服务器从安圭拉本岛迁到自己的全球网络。这是为了防飓风。2017 年的飓风 Irma 给安圭拉造成 3.2 亿美元损失,几乎瘫痪了岛上的电力和通讯。

这种结构让安圭拉在 AI 周期里拿到了大头。Identity Digital 接管后开启的拍卖业务在第一年就为安圭拉政府额外贡献了 60 万美元以上的收入,单是日拍机制就让 .ai 周收入提升了 20%。钱怎么花的,公开了一部分。

2025 年财政说明里写明:偿还国债(截至 2025 年底约 2.92 亿美元,约占 GDP 的 19.9%,远低于加勒比地区 60% 的红线)、扩建机场和路网、可再生能源投资、五岁以下儿童和七十岁以上老人的免费医疗。机场是关键,安圭拉的旅游业一直被有限的航班数量卡住。

Cora Richardson-Hodge 在 2025 年 2 月接任总理时拿到的就是这样一份财政。她是安圭拉首位女总理,所属的安圭拉联合阵线在大选中拿下议会 11 席中的 8 席,Webster 领导的进步运动党退到反对席。Vanterpool 也是联合阵线成员,进入新内阁。

图丨 Cora Richardson-Hodge(来源:Anguilla Focus)

押在两个字母上

安圭拉前首相 Webster 卸任前在多个场合重复过同一句警告:你没法预测这能持续多久。我们的经济和项目不能完全依赖它,否则一旦风向变了,就得在很短时间里做出剧烈削减。

这话搁在 2025 年的预算盈余面前听起来扫兴,但它指向的是一个很具体的可能性。

.ai 的高溢价建立在一个前提上,就是 AI 仍然是科技公司值得贴在自己门牌上的标签。当一项技术从前沿变成基础设施,像电,像云,它会从品牌资产变成默认属性。没有公司还把自己叫做 electric company 或 cloud company,因为这些已经是默认。如果未来五到十年 AI 走完同样的路径,.ai 后缀的营销价值会逐渐贬值,新增注册放缓,续费率下降,二级市场冷却。

Identity Digital 在自己的对外通讯里也写过一句话,AI 主题域名能否维持高位,取决于 AI 行业的资本周期。他们也知道这件事的脆弱。

但反过来看,.ai 也可能走出另一条路。当 AI 公司集体性地占领 .ai 后缀,比如 claude.ai、x.ai、perplexity.ai、meta.ai,这种集体占领反而强化了后缀本身的含义。.com 也不是因为美国才值钱的,而是因为最早入场的玩家把它做成了行业默认。.ai 能不能复制 .com 的稳定性,至少要再观察两到三个 AI 周期。

另外,如果这些收入真的进入偿债、基建、教育和医疗(目前的支出结构看起来确实如此),那么即使 .ai 红利退潮,这些投资本身也会留下来。机场扩建后多飞几条航线,债务降到 GDP 的 15% 以下,这些不会跟着 AI 周期消失。但如果钱被吸收到经常性支出里,公务员加薪、福利扩大,那么红利退潮的那一年就会很难看。

截至 2026 年 4 月,.ai 注册总数大约 110 万。Domaintechnik 的预测是 2026 年底可能达到 170 万。每天 2,000 多个新域名进入注册系统,每个域名背后是一笔进入安圭拉财政的钱。

但每一笔钱都默认了同一件事:在世界某处的某个产品负责人,仍然认为在自己产品的英文域名后面贴上 .ai,能让用户多看一眼。

这种判断还能持续多久,没人真的知道。