Original | Odaily Planet Daily(@OdailyChina)

Author | Azuma(@azuma_eth)

Before the US stock market opened on May 11th, stablecoin issuer Circle officially announced its Q1 2026 earnings report.

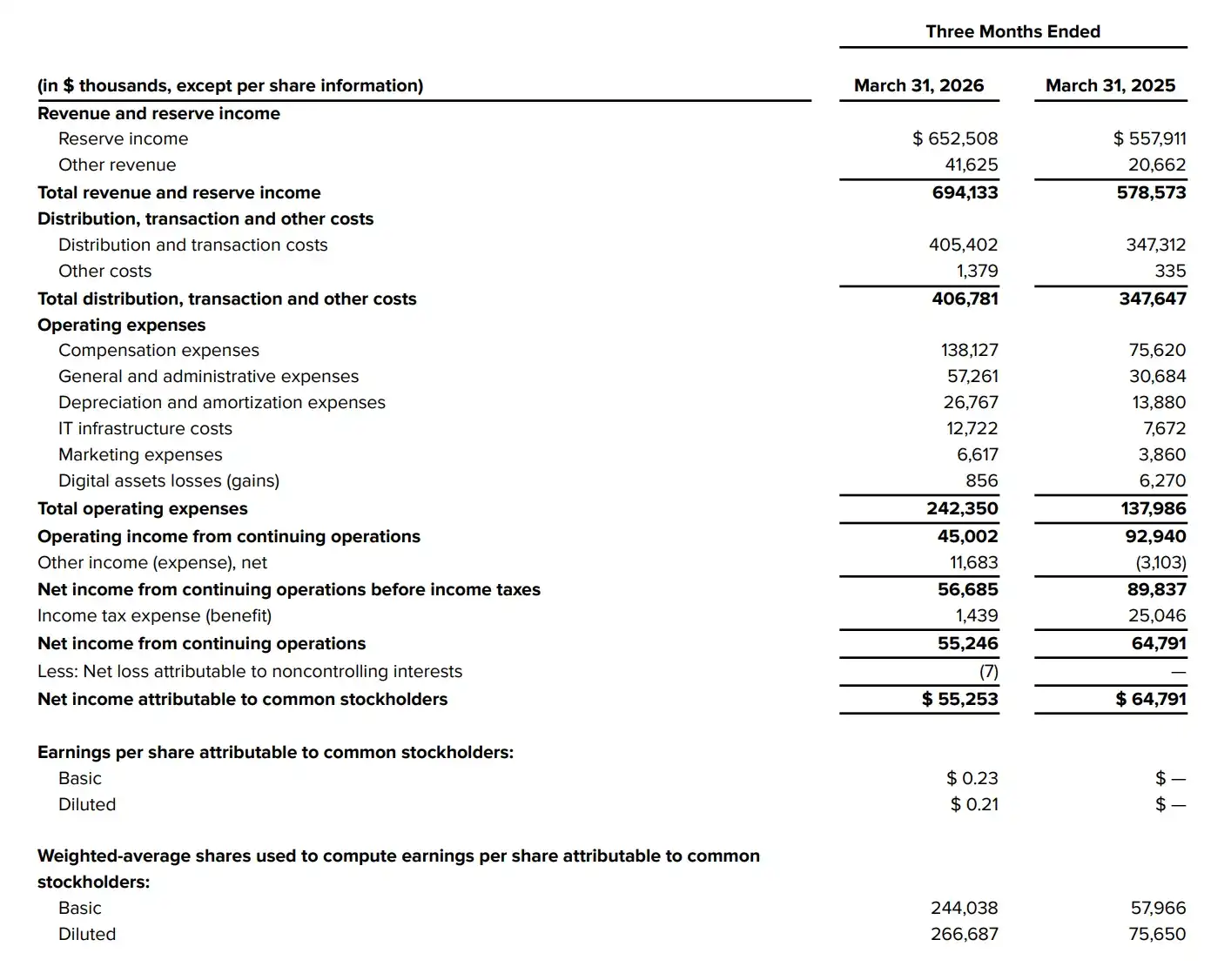

The financial report data shows, Circle's total revenue and reserve income for Q1 was $694 million, slightly below market expectations of $715 million; EPS was $0.21, higher than market expectations of $0.18; adjusted EBITDA was $151 million, a year-on-year increase of 24%; net profit was $55 million, a year-on-year decrease of 15%.

Affected by the earnings release, CRCL experienced significant pre-market volatility, with nearly a 6% pre-market gain gradually being erased amid fluctuations. As of 22:00, after the opening of US stocks, CRCL once continued to plummet but then quickly turned from loss to gain, temporarily quoted at $115.74, with an intraday increase of 2.52%.

Interpretation of Core Data

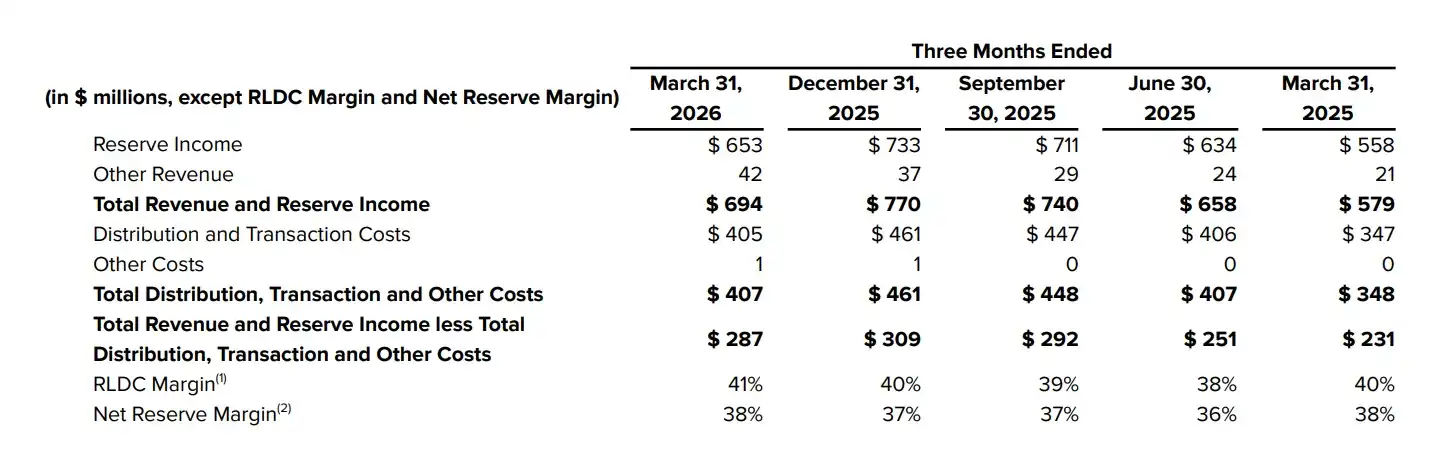

As shown in the report, Circle's total revenue and reserve income for this quarter was $694 million. Although it increased by 20% year-on-year, it broke the growth trend of previous consecutive quarters ($579M → $658M → $740M → $770M → $694M) and also fell short of market expectations.

Circle attributed the slowdown in revenue growth to a decline in the Reserve Return Rate. On December 10, 2025, the Federal Reserve lowered the federal funds rate target range by 25 basis points to 3.5%-3.75%, thereby compressing the yield of Circle's primarily US Treasury-backed reserve assets.

However, despite the relatively weak revenue, this earnings report from Circle still reveals some locally optimistic data.

First, Circle's Other Revenue, excluding Reserve Income, reached a new high of $42 million, showing a growth trend over multiple consecutive quarters ($21M → $24M → $29M → $37M → $42M).

As we mentioned in this afternoon's article "Earnings Report, Bill, Federal Reserve... Circle Faces Three Major Tests This Week", this means Circle's revenue sources are becoming more diversified. Its platform services, API tools, and payment products are generating tangible commercial returns, and reliance on interest income is decreasing.

Another noteworthy data point is RLDC Margin, the profit margin after revenue minus distribution costs. This reflects the core business profitability after deducting distribution expenses and is widely regarded as Circle's most crucial profit metric. This quarter, Circle's RLDC Margin reached 41%, achieving growth for four consecutive quarters (36% → 39% → 40% → 41%). This means Circle's control over distribution costs is becoming more efficient.

Now let's look at the expense situation. Distribution and Transaction Costs remain Circle's largest expense item, reaching a high of $405 million this quarter, a 17% year-on-year increase. This expense is mainly tied to the USDC distribution contract with Coinbase. This contract is set to expire in August this year. How it is renewed (primarily looking at whether the revenue-sharing ratio will be adjusted) will greatly impact Circle's subsequent expenses and profit status.

Apart from distribution costs, Total Operating Expenses also surged from $138 million last year to $242 million, a year-on-year increase of 76%. The primary increase came from Compensation expenses, which nearly doubled from $75.62 million to $138 million—Circle explained this was mainly due to IPO-related stock-based compensation expenses and related taxes.

Affected by the surge in expenses, Circle's operating profit for this quarter dropped to $45 million from $92.94 million in the same period last year; net profit attributable to common shareholders decreased from $64.79 million to $55.25 million; earnings per share (EPS) were $0.23, diluted to $0.21.

Other Operational Highlights

In addition to core financial data, Circle disclosed several operational highlights in its Q1 earnings report.

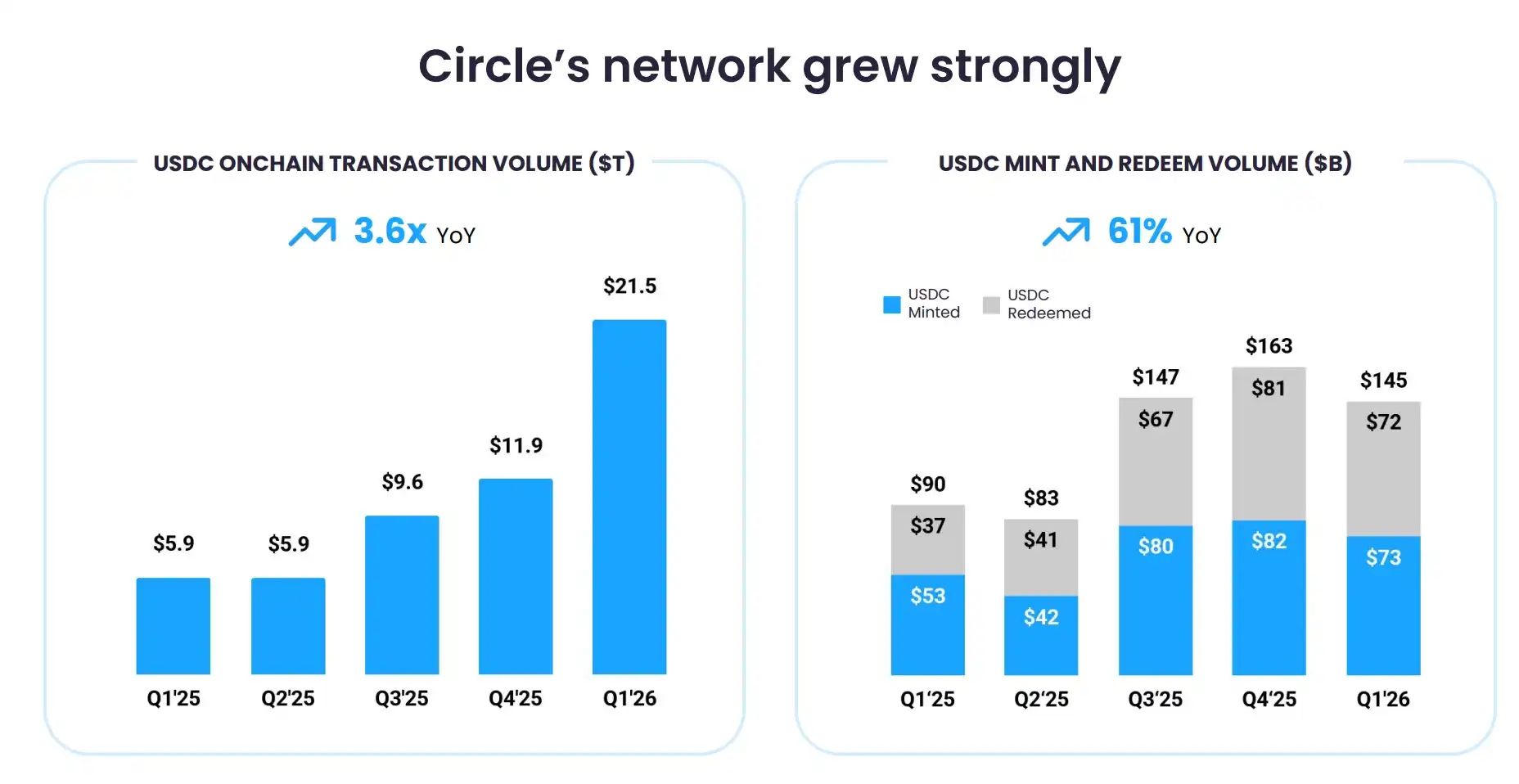

The most crucial data point is that USDC's circulation at the end of Q1 reached 77 billion tokens, a year-on-year increase of 28%. However, at the same time, USDC's on-chain transaction volume in Q1 reached a staggering $21.5 trillion, a year-on-year increase of 263%. Visa Onchain Analytics data also shows that USDC accounted for 63% of the total stablecoin transaction volume in Q1.

The transaction volume growth rate far exceeding the circulation growth rate means that the turnover and application frequency of each USDC token on-chain has significantly increased — USDC is not lying statically in wallets but is being genuinely and frequently used in scenarios like payments, DeFi, and cross-border settlements.

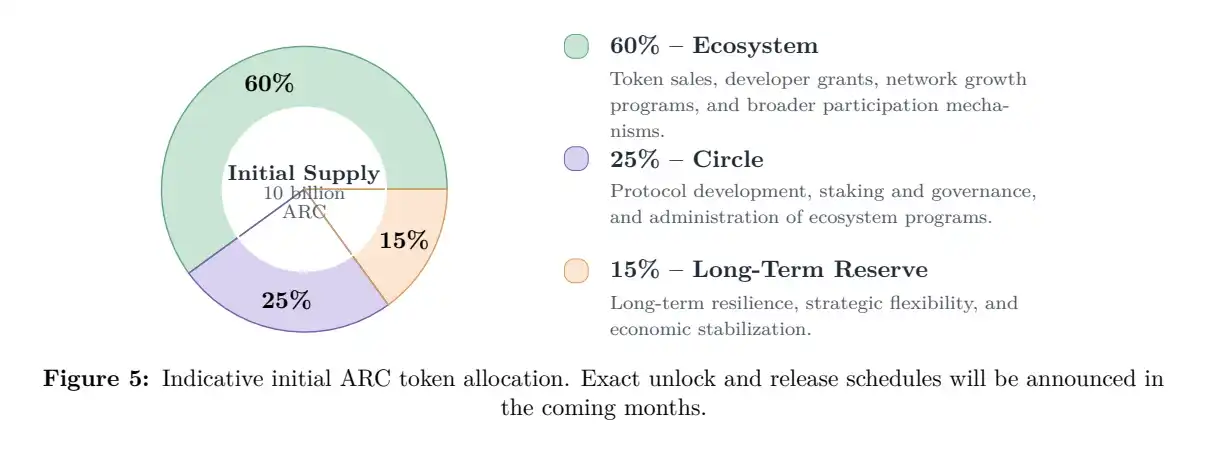

Another important point is that Circle also disclosed that its payment network, Arc Network, has completed a $222 million ARC token pre-sale with a valuation as high as $3 billion. Investors include renowned institutions such as a16z, BlackRock, Intercontinental Exchange, Standard Chartered, and SBI. The ARC token whitepaper disclosed today shows that 60% of the tokens will be allocated to the ecosystem (token sales, developer grants, network growth); 25% will be allocated to Circle (protocol development, staking & governance); 15% will be allocated to a long-term reserve (strategic flexibility & economic stability).

In the subsequent earnings call, when asked how the ARC tokens belonging to Circle would be accounted for, Circle Co-founder and CEO Jeremy Allaire stated: "When ARC tokens are created, they will be recorded on Circle's balance sheet at cost, and their cost is zero. Subsequently, after Circle fulfills its obligations under the token pre-sale agreement, we will recognize the value of these tokens as 'Other Revenue', and this value will then be directly reflected in RLDC and Adjusted EBITDA."

This also means that in a future quarter, Circle's reported revenue data will look "exceptionally good" due to the inclusion of ARC token value.

Furthermore, the estimated annual transaction volume for Circle's institutional payment service, Circle Payments Network (CPN) (extrapolated based on 30-day data as of March 31st), has also reached $8.3 billion; In April, Circle launched the "Managed Payments" product to expand its payment offerings. This product allows financial institutions to launch stablecoin payment services without having to manage digital assets themselves.

To prepare for the AI Agent-driven commercial future, Circle also announced the launch of Agent Stack, a set of infrastructure services and toolkits for the AI Agent economy, designed to provide high-speed, low-cost financial service capabilities for autonomously operating AI Agents. Jeremy Allaire's vision for this is: "With the ARC token pre-sale, the momentum building for Arc Network, and the launch of Agent Stack, we are building trusted infrastructure for AI-native economic activity and a more programmable internet financial system."

Circle's New Chess Game

Against the macroeconomic backdrop of receding high-interest dividends (Warsh is expected to promote a "rate cut + balance sheet reduction" strategy upon succeeding as Fed Chair), Circle clearly does not want to be entirely at the mercy of the Federal Reserve's interest rate policy. Its strategic focus has quietly shifted towards diversified expansion of non-interest revenue.

Judging from the details disclosed in this quarterly report, after successively launching services like CPN, Managed Payments, Agent Stack, and Arc Network, Circle's goal is no longer just to be a "stablecoin issuer." It is attempting to build USDC into the underlying dollar network for the internet era. Under this new vision, Circle's service targets are no longer limited to exchanges or crypto-native users but are extending comprehensively into cross-border payments, corporate settlements, and even the AI Agent economy.

Circle's ambition is now abundantly clear: to transform USDC from a "static reserve asset" into "flowing economic blood." This is perhaps the big chess game Circle truly wants to play.