Abstract

The most mentioned topic in the crypto industry for the month of May 2022 must be the algorithmic stablecoin. Since May 10, UST, the prestigious algorithmic stablecoin with the largest volume, encountered its Waterloo: an intense depeg from US dollar. This upheaval triggered massive depegs to various extents for other algorithmic stablecoins. The sum of the Top 5 algorithmic stablecoins by market cap has shrunk from US$23 billion to less than US$4 billion before May 22, a sharp 82.6% decrease in merely 2 weeks. The market is shrouded in panic, and all eyes are on the stablecoin industry.

In this article, types of algorithmic stablecoins will be briefly introduced: an algorithmic stablecoin is defined as a “stablecoin with sufficient cryptocurrency as full collateral”. The significance of proposing the concept of algorithmic stablecoin is to mint stablecoins efficiently by crypto assets with high price volatility. As a critical asset class, an algorithmic stablecoin is necessary in the crypto world.

Mainstream stablecoin design scheme will be discussed in this article, and 4 elements, as barricades to the success, will also be explored:

1. Full-backing assets If the algorithmic stablecoin is backed by endogenous assets, when they both decrease, the whole system could fall apart once and for all. Whereas if the algorithmic stablecoin is backed by exogenous assets, as risks are comparatively isolated, the price would be more inclined to correct after a depeg. The intention for burning an algorithmic stablecoin is to mint extra assets for collateral, resulting in an intensive depreciation of underlying assets, even a collapse of the whole system. The collateralized ones have a default risk, as some of the users may not retrieve collateralized assets, in part or in full.

2. Robust stabilization scheme A healthy scheme should consist of an independent stabilization scheme without the status of the protocol, fully functioning when the price falls below 1 USD and hedging the risk of depeg for the system. The stabilization scheme will bring about considerable selling pressure on underlying assets, increasing the probability of entering a death spiral. The degree of openness for redeem venues will reflect different portions on the selling pressure between underlying assets and stablecoin.

3. Flexible asset management strategy A reserve utilization could be beneficial for both the protocol and the users. Two types of strategies are most commonly seen: an AMO strategy absorbs profits from market-making activities in DeFi protocols with the reserve, whereas an auto treasury management strategy profits from the market by “buy low and sell high”.

4. Abundant application scenarios. Having more application scenarios shall increase the demand for algorithmic stablecoins. A stablecoin must have high liquidity and numerous agreements with other protocols, so that it could be competent and compatible in various scenarios in different environments.

This article ranks algorithmic stablecoin according to the above criteria from high to low: USDD>UXD>FRAX >FEI>USN>USDN.

1. An overview of algorithmic stablecoin

1.1 Redefine algorithmic stablecoin

Stablecoin is namely an equivalent cryptocurrency with low price volatility with the price pegged to the value of commensurate fiat. Developers strive to maintain price consistency between the token and the pegged fiat - and away from the price volatility of the market. In short, only stablecoins pegged to US dollar will be discussed.

It is commonly acknowledged that stablecoins are classified to 3 categories by the existence of collateral and the type of collateral:

Fiat as collateral

Over-collateralized with crypto assets

Algorithmic

Stablecoins with fiat as collateral cannot be issued with the commensurate fiat collateralized in full. Assets in full collateral includes cash, treasury bonds, commercial notes or other assets with high liquidity. It is so far the largest in terms of volume issued; and can be seen as a reflection of fiat money from the brick-and-mortar to the crypto world.

Over-collateralized stablecoins must receive crypto assets with the value greater than the face value as collateral prior to issuance. For instance, a new issuance of 100 DAI cannot be issued without 150 dollars of ETH in collateral. This type of stablecoin has its origins in the crypto world.

A collateral is not necessary in algorithmic stablecoins; an adjustment on the supply and demand could achieve price stabilization. When the market is in symmetry, the price of a stablecoin is 1 US dollar; when the market is not in equilibrium, the algorithm would adjust the supply by the demand to correct the price of the stablecoin to 1 US dollar.

Algorithmic stablecoins have evolved and are represented by several projects, such as AMPL, Basis Cash, Empty Set Dollar, etc., which share a common characteristic: they have all failed at the fundamental mission to maintain the price as 1 USD. One of the reasons to explain this failure is the absence of collateral: when the price falls under 1 USD, users lose confidence completely.

The all-new algorithmic stablecoin has learnt some lessons from the past. In the issuance scheme, some crypto assets must be either burnt or entered into full collateral. Doing this adds stability while sustaining innovation, but has somehow changed the inherent nature of the algorithmic stablecoin. So here we redefine the algorithmic stablecoin as stablecoin with crypto assets in full collateral. To be more specific, when users burn or deposit assets worth 100 USD, 100 1 USD stablecoins can be minted. In this article, all the burnt or collateralized assets are defined as the underlying, or backing, assets.

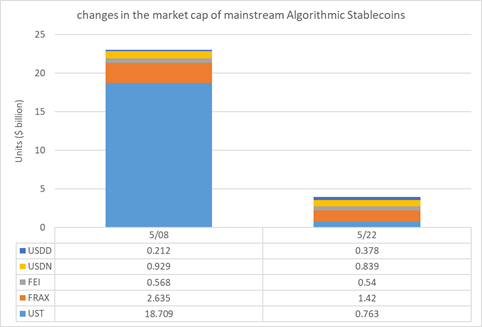

With eyes on the scale of algorithmic stablecoins, the collapse of UST decimated a considerable portion of the market cap. According to CoinGecko, the market cap of the top 5 algorithmic stablecoins have seen a sharp 82.6% decrease in less than 2 weeks: from US$23 billion on May 8 to less than US$4 billion on May 22.

Figure 1: Changes in market capitalization of mainstream algorithmic stablecoins

Source:CoinGecko,Huobi Research

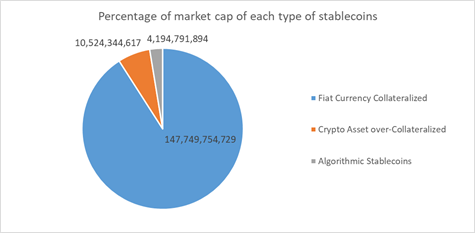

According to date from CoinGecko, on May 22, the top 30 stablecoins accounted for US$162.5 billion dollars in market cap. Specifically, 11 are stablecoins with fiat as collateral, 11 are stablecoins with over-collateralized crypto assets, and 8 are algorithmic stablecoins. The market cap of algorithmic stablecoins is roughly US$4.2 billion, accounting for 3% of the total stablecoin market cap.

Figure 2: Supply of various types of stablecoins

Source:CoinGecko,Huobi Research

1.2 Significance of algorithmic stablecoin

Why do algorithmic stablecoins exist? Is arbitrage and short-term profit the final destiny for algorithmic stablecoins? The questions could be answered by the comparison with the two analogical precedents.

Table 1: Comparison of the pros and cons of two types of stablecoins

Source:Huobi Research

Stablecoins with fiat as collateral have barely seen any fluctuations as the backed assets are fiat, which is traditionally safe. In this case, collateral only has to be in full instead of in excess, thus, capital efficiency is enhanced. Nonetheless, they are all issued by highly centralized institutions, namely Tether and Circle. Users must assume that these institutions have sufficient reserve and liquidity. Although audit reports are published quarterly, suspicions towards the stability of the underlying assets are never fully erased. Besides, custody expenses are incurred when dealing with such large amounts of fiat assets, imposing extra costs for the maintenance of the system, and also incurring extra risk exposure on both the assets in custody as well as the trustee.

A stablecoin with over-collateralized crypto assets is comparatively stable. As the collateral is in crypto, no centralized institution can interfere with the issuance, nor is KYC needed. Such degree of decentralization equips the stablecoin system with anti-glitch capabilities for single point of failure. Users have to deposit excess crypto assets as collateral in order to receive this type of stablecoin, as the crypto assets in collateral are subject to severe price volatility. This results in capital inefficiency: liquidity extracted from the market for collateral is greater than the new issuance of stablecoin pegged to be injected into the market.

With comparison of the two, a paradox remains: decentralization and capital efficiency. Algorithmic stablecoin was born for the purpose of minting stablecoins with highly volatile crypto assets in an efficient manner. Apart from price consistency, it aims to issue stablecoins while balancing decentralization and capital efficiency.

The ideal algorithmic stablecoin should be minted with price consistency without a mass sacrifice in liquidity. It should be deemed an acceptable medium for exchange and price unit, flow smoothly through the blockchain network and various dApps and be free from the manipulations of centralized institution.

Stablecoins are an outstanding medium for exchange, and as a fundamental element in the crypto world, it carries out the responsibility to accelerate the cycle of the system by promoting transactions. For the crypto world, such crucial infrastructure cannot be solely in the hands of centralized institutions, otherwise severe systematic risk would be incurred, endangering the independence of the system. On the other side, the development cannot thrive or be sustained at the cost of compressing the scale of crypto assets. As a result, algorithmic stablecoins are the inevitable solution with continuous evolution, and has yet to become a critical asset class. The collapse of UST may be the most market-shaking of the year for the crypto world, but it will have negligent impact on the development path of algorithmic stablecoins in the future.

2. Necessary Success Elements for Algorithmic Stablecoins

Through close scrutiny and in-depth analysis, this article has identified 4 essential elements for stablecoins to achieve success:

1. Full-backing assets

2. Robust stabilization scheme

3. Flexible asset management strategy

4. Abundant application scenarios.

2.1 Full-backing assets

First of all, it has been a consensus that full-backing assets lay the foundation for the the current generation of algorithmic stablecoins. Only full-backing assures the buttress to resist market price fluctuation and maintain the pegs over time. Therefore, whether sufficient collateral is found in the system becomes the single most critical determinant in the success of an algorithmic stablecoin.

Next, how the issuance scheme and reserve allocation could influence the abundance of underlying assets and the stability of the system will be analyzed.

2.1.1 Issuance scheme of algorithmic stablecoins

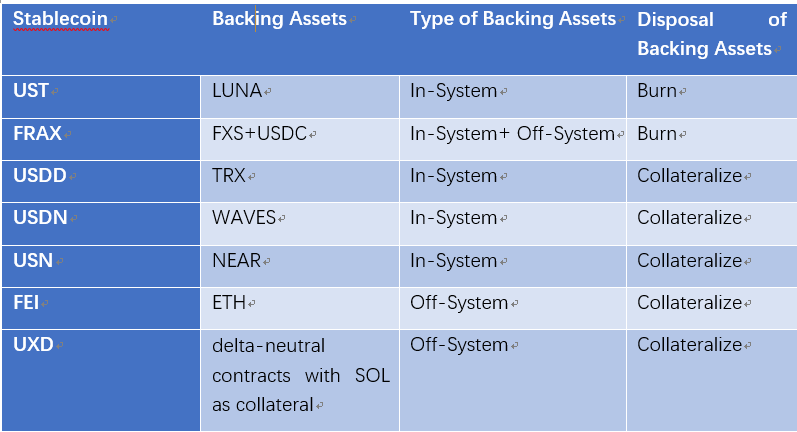

Current mainstream stablecoins requires certain types of crypto assets to be in collateral or burnt before minting stablecoins with equivalent value. The table below shows the issuance scheme of the mainstream algorithmic stablecoins. The issuance schemes are rather simple and homogeneous.

Table 2: Summary of the issuance schemes of mainstream algorithmic stablecoins

Source:Huobi Research

The difference between in-system and out-of-system assets is the relationship between the assets needed to mint the stablecoin and the stablecoin itself, and whether they are essentially issued by the same team. If the issuance source is the same, the price volatility will be transferred from the stablecoin to the backing assets: the two exert force on each other, and especially prices of both drop, the whole system will be subject to a severe collapse that is extremely hard to recover from. On the contrary, if the issuance source is not the same, the status of stablecoin is not exposed to the price volatility of the exogenous assets. Thanks to the comparatively better risk isolation, the stablecoin will be more inclined to repeg after a depeg in short time.

Next, the difference between burning and collateralizing, and possible outcomes when the underlying assets are insufficient, will be clarified.

2.1.2 Risks of Burning Algorithmic Stablecoins

Burning is the other end of minting; the actions have to be applied to the same object: endogenous assets, otherwise the system is ineligible for minting. For new issuance of stablecoin at the cost of destruction of certain assets, when users require a redemption, the protocol has to mint certain underlying assets to pay back. For example, users could retrieve LUNA by burning UST.

The problem emerged: Where did the minted LUNA come from? As officially announced, total issuance of LUNA is 1 billion, which was confirmed in 2019. LUNA has been in full circulation, and there was nothing about stablecoins involved in the allocation plan, which left us with nothing but one sole solution: to revitalize the burnt LUNA. In this case, burnt LUNA become the underlying asset for future redemption. Whereas the remaining LUNA carries out the function of alleviating impact on price and is not available for direct redemption.

During the expansion of UST, LUNA was continuously burnt in exchange for the mint of UST, squeezing the circulation of LUNA and elevating the price of LUNA. During the early days of LUNA and UST, many were of the opinion that very few would invest. But as price of LUNA skyrocketed, more investors flocked into the game, pushing the price up even further. With price increase of LUNA, the quantity of LUNA required to mint the same amount of UST became less. As a result, considerable LUNA was burnt to mint UST when the price of LUNA was high. At first glance, the underlying assets was sufficient in LUNA, but this is only so when the price of LUNA continues to be this high. But when the price of LUNA dipped suddenly, the backing assets quickly would become insufficient, more LUNA would be required to mint the same amount of UST in order to pay back the underlying assets in collateral as they are cheaper at redemption, while even more than that amount has been burnt. As long as the stabilization scheme continues, selling pressure would increase with further price drop, and more LUNA must be minted to cover the redemption requests. Ultimately, even the resurrection of all the burnt LUNA would not be sufficient to refund the underlying assets, namely previous LUNA in collateral, thus new issuance of LUNA would become the only available option.

Figure 3: More LUNA Destroyed at High Price Levels

Source: CoinGecko,Huobi Research

Stablecoins with such destruction settings will mint underlying assets in excess, which is risky when the price of underlying assets and the stablecoin itself decreases, leading to a crash in the price of underlying assets with system-wide effects.

New issuance is not impossible in the crypto world; it is only viable when the stakeholders, such as the community or other related beneficiaries, are left with sufficient decision-making time to fully discuss pros and cons with the issuer. In other words, as the pros and cons are discussed and disclosed to any stakeholders who may be involved, every single stakeholder can vote with eyes closed for they have nothing unknown to fear. Otherwise, new crypto issuance could be initiated whenever an incident is encountered, holders would be diluted, network safety would be severely harmed, and liquidity of market makers would be drained. Countless problems will emerge until every single participant in the system is inundated.

LUNA has now completed an enormous new issuance plan, which is some 7000 times more than the initial supply, causing a severe fall in the price of LUNA and UST — nearly zero and below 0.1 dollars, respectively.

FRAX is an algorithmic stablecoin with partial collateral. The algorithm will adjust the collateral ratio (CR) based on the price of FRAX. For example, users must deposit USDC at the amount of CR and burn FXS token at the amount of 1-CR in order to mint 1 FRAX. Upon redemption, the system will return the collateralized USDC according to CR, and the rest with minted FXS. The project started with a collateral ratio at 100%, and has a current rate of around 90%. As the stablecoin minted from the collateral of USDC has no risk, it is defined as an algorithmic stablecoin with destruction in this article. Admittedly, partial collateral could reduce the risk at large, but it would not eliminate the risk at its root. In the event of a death spiral, FXS is exposed to the risk that the price may go down to a certain level that even the retrieval of all burnt tokens will still result in bankruptcy.

2.1.3 Risks of Collateralized Algorithmic Stablecoins

A collateral has to be returned eventually. Whenever the user submits such an inquiry, the protocol must return the underlying assets in collateral. The same applies stablecoin with collateral as with stablecoin with burn policies — that the underlying assets will be insufficient to be returned when the price of underlying assets and the stablecoin decreases. In this case, whoever cashes out earlier is more likely to retrieve the collateralized assets in full, and late claimers may not be that lucky. For loss prevention, late claimers have to dump stablecoins on the secondary market, which drags down the price of the stablecoin. The best part of this type of stablecoin is the incapability for new issuance, ensuring the value of underlying assets is not impacted by any sudden new issuance.

UXD is peculiar in the collateral-backed algorithmic stablecoin category. The underlying assets of UXD is not literal cryptocurrency, but is, instead, a margin of a delta mutual perpetual contract established for collateral by crypto assets mainly composed by SOL. When SOL is entered into a collateral, the system would open a 1x Coin-M short perpetual contract with the collateralized SOL on a DEX, and mint UXD that is of equal value to the collateralized SOL. If the price of SOL increases, the contract will experience a loss, but the collateral per se appreciates, and vice versa. Under the two circumstances, the change in price is triggered as the change in the contract and the collateral share the same amplitude but in an opposite direction. As the value of the contract is not affected by the price change of underlying assets, it is thus called delta neutral. In addition, no clearing would occur in both circumstances thanks to the stability of asset value, unless there is over loss for long positions due to a sudden price drop of SOL in a short time. In this case, even if the profit appears considerable for short positions, they would more likely mere numbers as these gains are not fully accessible because no one will settle the position. Moreover, the insurance fund provided by the UXD protocol ensure a stable reserve is maintained. The graph below illustrates the change in UXD ranges from 0.99 dollars to 1.02 dollars despite a vast change in the price of SOL. According to Arthur Hayes, founder of BitMex, this design philosophy is nearly impeccable despite any degree of price change because the stability of the underlying assets ensure the stablecoin’s price stability.

Figure 4: Mechanisms for UXD to maintain stability in underlying asset prices

Source:Huobi Global,Huobi Research

2.1.4 Reserve requirements

It is not sufficient for a stablecoin to be fully asset-backed at issuance; instead, the value must sustain through the whole life cycle of the issued stablecoin, especially when the price of underlying assets fluctuates. The fundamental method is to create a reserve. Whenever there is a depeg, the reserve will reinforce the redemption or maintain the purchase power.

Different opinions have been proposed for asset class designation and reserve value maintenance.

Among them, one proposal involves designating mainstream crypto assets in the reserve. This design facilitates the appreciation of assets in the reserve if the system sustains itself. Thus, the value of reserve is accumulated to a higher level so more stablecoins could become available to be minted. However, the system must be in a rather safe state before the assets in the reserve has the chance to appreciate. If the overall market is bearish, the value of assets in the reserve will also dip and are therefore ineffective as a reserve. Nevertheless, certain actions could be made to remedy the situation and maintain the reserve above safety range.

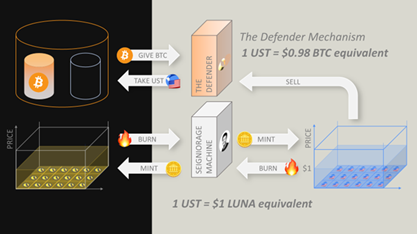

UST once established a reserve with 80,000 BTC that was worth up to US$2.8 billion and nearly 15% of the whole crypto market capital. The number may look low, but for stablecoins with destruction mechanism, the burn should also be taking into consideration. The system made a hypothesis that when the price of UST is below 0.98 dollars, it will authorize a redemption of 1 UST to some BTC worth US$0.98. But the price of UST fell so steeply in the death spiral before the launch of BTC redemption scheme that the reserve was drained within a blink of an eye, and the BTC in the reserve was insufficient to pay off. The confidence in this stablecoin ebbed out with the empty BTC reserve.

Figure 5: BTC as a reserve for UST

Source:Foresight News

FEI obtained ETH worth over US$1 billion for the redemption of FEI stablecoin at Genesis (April 2021). According to the rules, this ETH is deemed as protocol-controlled value (PCV) and therefore non-redeemable. It was a major disappointment that FEI fell to US$0.75 not long after launch. The protocol was updated later and the redemption venue was opened, FEI reacted accordingly and was adjust back to US$1. FEI hence evolved from being an original algorithmic stablecoin without collateral to an algorithmic stablecoin with full collateral in crypto assets. Because the ETH is valued at about US$2000 each, and it has increased over 50% at the beginning of May not long after the redemption venue was opened and hardly fell below US$2000. As a result, the amount of ETH available for redemption is less, and the remaining became part of the reserve. The protocol holds US$413 million in the reserve, and 73% represented by ETH. The collateral rate is 174%; that is to say, 74% of the original issued value could be distributed to hedge market fluctuation and handle emergency. It is a comparatively large number that it is capable of withstanding a 50% pullback of ETH price. If a more pressing situation appears, the protocol would initiate bidding for governance token, TRIBE, for fundraising. The holders of TRIBE became the last line of defense.

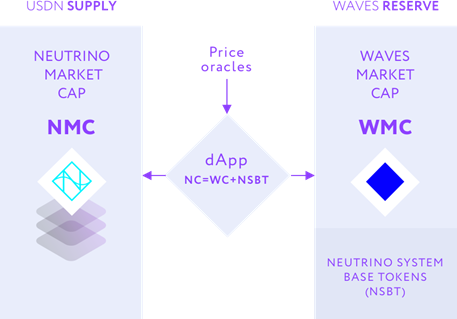

The role of risk bearer is also found in USDN, but in a different setting from FEI. The system would automatically mint USDN and buy back (the system calls it a “liquidation”) NSBT in the system when the market cap of WAVES in the USDN reserve (WMC) is larger than that of USDN issued (NMC); the operation would be called off when no NSBT is in the waiting list to be liquidated. If WMS is less than NMC, the system would sell newly issued NSBT in exchange for WAVES (based on the price from formula) and inject the sum into the reserve. When there is excess in the reserve, NSBT would be purchased again with the automated USDN. NSBT, in this case, is a risk bearer for WAVES that fundraising could be completed with no more WAVES issued.

Figure 6: USDN Systems issues additional NSBT to raise funds

Source:wp.neutrino.at

Based on the formula, when the supply of NSBT increases, the issuance price, namely the price users pay with WAVES for NSBT, will rise exponentially. The rationale behind the design can be explained: the application of NSBT could be diverse, and the official is unwilling to sacrifice NSBT as an asset class with infinite inflation. So, the maximum supply is fixed at 2.8 million. Meanwhile, assurance must be made that newly minted NSBT is sufficient to redeem a certain number of WAVES, and only an exponential price increase can fulfil this. However, the market price may not rise accordingly; it may be sold at discount (the same as current market). If there is no room for arbitrage, the reserve cannot be topped up. Furthermore, the system only issues a buyback with 1 USDN to 1 NSBT, but the market value of NSBT is normally above US$20, which makes it unable to initiate the buyback. It is possible that the system was never intended to buy back NSBT to trim the supply, or it aimed to retain more value in the reserve from the start. The scheme is, de facto, paralyzed: the total supply of USDN is worth US$848 million, while the WAVES in the reserve is only worth US$243 million, which translates to less than 30% coverage. Insufficient reserve is a severe threat; the current two depegs of USDN of over 20% may be attributed to this. The reason USDN has not yet collapsed will be discussed later in this article.

Another proposal is to build the reserve with stablecoin, a conventional but simple approach. The reserve will not shrink when the market is poor. In this case, the coverage is as transparent as it is in numbers. Within the range, the system is considered secured. On the other side, if the market warms up, the reserve cannot enjoy profits from appreciation. No projects establish their reserves solely with stablecoin — a cocktail of both risky crypto assets and the comparative risk-free stablecoin is more widely adopted.

Upon launch, users must mortgage NEAR that is equivalent in value in exchange for the issuance of USN, and the system will automatically put an equivalent amount of USDT as collateral. That is to say, the initial reserve consists of double assets. In initiation phase, even if NEAR is worthless, the protocol still has sufficient funds to pay off the debt, which constructs an extremely risk-proof system. As more USN is issued, the reserve ratio decreases. The protocol is dedicated to developing a dynamic asset management strategy in order to ensure the reserve is always above the issuance of USN, which will be discussed later in the article.

The reserve fund of UXD is mostly used to cover fees when the fund rate for perpetual contract is negative. UXD is therefore constrained to a slow growth rate, otherwise it is unfeasible to cover the expensive fees incurred. Currently, the UXD reserve (called Insurance Funds) is US$59 million dollars. To be more specific, if UXD reaches the ceiling of issuance at US$160 million, the insurance fund is subject to an APR of -36.9% for 1 year, which is unlikely to happen. Considering the current issuance at US$41.5 million, the insurance fund is still exposed to an APR of -35% for 4 years in a row, which is even more unlikely. If the funds run out in the reserve, the protocol would issue more and start a bidding on the governance token UXP in order to refill the reserve.

A stablecoin protocol design could learn from UXD by maintaining a delta neutral: some extra funds are reserved to establish a margin in a death spiral and set off the systematic loss by the profits from contract. Discerning judgement on the market and proper contracts with sufficient liquidity are necessary in this case.

In designing the reserve, capacity and configurations must be through deliberation as this would not be either a “the more, the better” or a “the more stable, the better” case scenario; it could prove a burden to the system. Most projects seek for a balance in the reserve with a combination of crypto assets and stablecoin. The establishment of a reserve is inherently an action that lowers capital efficiency; thus, the balance between security and capital efficiency must be found.

2.2. Robust stabilization scheme

Algorithmic stablecoin in this generation shares common thoughts on the stabilizing pattern that not relied on the protocol status. No matter if the price of stablecoin could rise above US$1, room for arbitrage must be always available as the stabilization process functions.

2.2.1 Evolution of stabilization mechanisms

Represented by BAC and ESD as stablecoin from last gen, a so-called “bond” is sold to users at discount when the price of stable coin went under US$1. When the stablecoin is sold above US$1, the “bond” will be bought back with the market price. In this case, the “bond” holders could profit from the buyback as a reward for providing liquidity to the system. The “bond” is, in fact, an option with the precondition that the price of stablecoin could exceed US$1. Once the price of stablecoin falls below US$1, no interior force can revive it and all algorithmic stablecoins failed in the last generation.

Current mainstream stablecoins operate on similar stabilizing scheme. The primary philosophy is the system always regards 1 stablecoin as US$1 dollar so that actions done by users would trigger an adjustment of the system to control the circulation supply in order that the price of stablecoin remains at US$1.

If the price of stablecoin is over US$1, when the user purchases underlying assets, the system would require the user to mint commensurate stablecoin in quantity according to the price of the underlying assets in dollars (received from oracle machine). Next, the user would sell the stablecoin at market price, which is over US1; the cost is US$1 to mint, and the spread becomes profit. As circulation supply increases, the price would decrease.

If the price of stablecoin falls below 1 dollar, users could redeem underlying assets by purchasing stablecoin at market price. As the system recognizes the value of the stablecoin as remaining at US$1, it pays off the users with underlying asset in equivalent value, and burns the stablecoin. Users, however, could sell the underlying assets for profit, and the profit comes from the premium paid by the system. As the circulation supply shrinks, the price would go up.

The above scheme could function well even the price of stablecoin falls below US$1, which could save the system from a normal depeg.

2.2.2 Flexibility of redemption venues

Various algorithmic stablecoins share common stabilizing schemes, while the degree of openness on redemption venues somewhat differs. As stated above, when the price of a stablecoin falls below US$,1 the above stabilizing pattern could bring a selling climax to the underlying assets, further increasing the possibility of system entering a death spiral. The openness of redemption venue could affect the proportion of selling climax being allocated to the underlying assets or the stablecoin. To be more specific, the more open the venue is, the more democratic the project, which adds more possibility for price recovery.. Under this circumstance, the underlying assets get more distressed, and the path to a death spiral becomes apparent; only external forces could bring the depressed price alive. Whenever more limitations are found, accusations happen to be more on the high degree of centralization, which is true that the host would have plenty of room for some actions. It might alleviate the distress on the underlying assets, while the fall in the stablecoin’s price may be sharper. Users would bear more burden if attempting to escape from the price drop.

The original redemption venue for UST is somewhat in a flux. Before May, the quota for redemption was fixed at US$20 million, which is trivial compared to the total supply of US$18 billion. But when a severe depeg happened, the official team increased the quota to US$80 million, which exacerbated the selling pressure for LUNA and cut down the time for remedial actions, ultimately leading to the devastation of LUNA and UST.

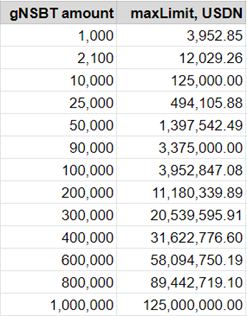

The redemption venue for USDN is far more restrictive. First, only one WAVES-USDN exchange could be done within 24 hours for each address. What’s more, the quota is strict; if a higher quota is desired, you need to have more gNSBT (generated by collateralizing NSBT). For example, an ordinary user must put assets worth US$21,000 just to redeem his or her own assets worth less than US$4,000. It would be a headache for a normal user as the cost is too high. Furthermore, the NSBT in collateral cannot be released at once: only 50% could be retrieved after 6 months. Such strict rule disables short-term arbitrage activities, as they are not cost-efficient per se, and the selling pressure would be is weakened to an extent. Although the reserve fund is insufficient such that two depegs happened in the past two months with over 20% price drop, the price of WAVES did not experience a fall to the bottom as it was unencumbered by USDN.

Table 3: Restrictions on the redemption of WAVES-USDN

Source: docs.neutrino, gNSBT is a voucher to deposit NSBT

Figure 7: NSBT has to pay high fees to release from collateralization

Source:docs.neutrino

USDD shut the door for average users to redeem; only whitelisted institutions have the right to redeem USDD for TRX. In the scenario that price of USDD experiences a severe cutoff, users would have to sell in the secondary market at high discounts, expediting the price jump, which will leave both parties fighting like Kilkenny cats. If a mutual agreement can be reachedbetween the USSD issuer, Tron DAO Reserve, and the whitelisted institutions, such that institutions will not perform large scale redemptions during extreme moments, only then will the selling pressure of TRX become less lethal: the system could adjust by implementing marketing strategies to recover the peg of USDD after a price drop when the negative emotions tide over.

2.3 Flexible asset management strategies

Reserve funds are quite a fortune for various algorithmic stablecoins. Proper usage of the funds could be lucrative for both the host and users. On one hand, stability of the system could be enhanced; in addition, more users could be attracted to the system.

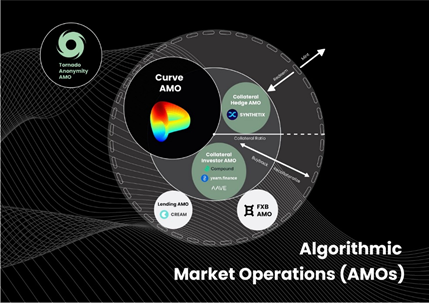

2.3.1 Algorithmic Market Operations (AMO)

The easiest method is to be a market-maker and lender in fundamental DeFi protocols; profits come from market-making and interest. This refers to Algorithmic Market Operations (AMO). Specifically, AMO is controlled by the same party, where the fund cannot enter circulation unless it consents to doing so, so a large selloff would never happen. That is to say, the money may not be bona-fide: the protocol could forge stablecoin for the sake of the improvement of capital efficiency.

To redeem the seemingly true stablecoin in a DEX, users need to pay out of pocket. The bona-fide money paid by users becomes funds in the reserve, and on the balance sheet of the protocol, this amount of money increases the assets and the liability at the same time, therefore, no excess currency issuance will happen. FEI and FRAX employed this tactic. FEI utilized the bona-fide ETH and the immaterial FEI in the market-making activities on Uniswap: not only could profits be extracted, but also the market depth is facilitated, improving user experience overall. Similarly, FRAX founded a FRAX3CRV fund pool on Curve to provide liquidity and make profit by USDC from the reserve and some extra forged FRAX, so did it on other DEXs.

Figure 8: AMO strategy of FRAX

Source:samkazemian.medium.com

For lending, users must always have greater assets in collateral in exchange for a certain amount of stablecoin. In other words, if a user does not expect an unwilling settlement, he or she must maintain sufficient funds in collateral. In the long run, no extra stablecoin issuance will occur. The system is considered safe so long as the scale of lending pool is controlled, otherwise it could become vulnerable to unfriendly shorting activities.

On top of that, staking with assets in the reserve could be a simple but achievable manner to obtain mining rewards from POS, which has been adopted by USDN and USN.

In all, AMO is the most reliable tactic for extra earnings, and it may become a common setting by most algorithmic stablecoin protocols in the future.

2.3.2 Appropriate expectation on market fluctuation

The price of cryptocurrency could rise and fall in seconds, and profit making opportunities lie if “buy low and sell high" trading can be executed properly.

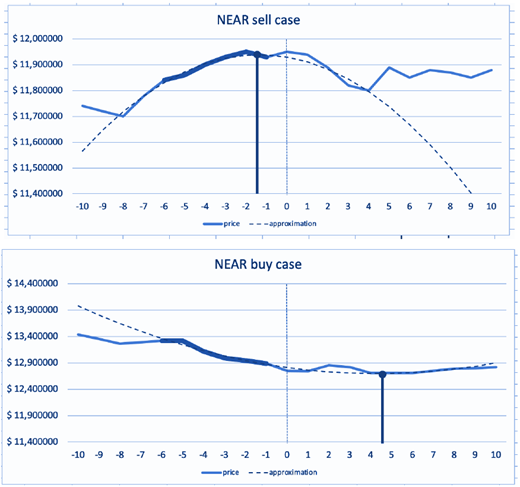

USN has adopted such a tactic and name it autonomous treasury management. A function of y=ax^2+bx+c is generated with regard to price and duration fitting the price of NEAR in 6 preset durations (i.e., 10 minutes as a duration), and a parabola is graphed that selling NEAR at its peak or buying NEAR at the nadir is always desired and executed.

Figure 9: USN's Autonomous Treasury Management

Source:decentral-bank.finance

Although NEAR and USDT are the two pillars of USN, the relationship between the two is not static. For example, for a US$10 million USN issuance, a combination of US$6 million in NEAR and US$8 million in USDT would do just fine. The portion of NEAR and USDT is determined by the system: it will be approved as long as the issuance of USN is backed by over 100% in equivalent value and the portion of USDT and NEAR are within the system settings. As a result, the remaining USDT and NEAR could provide extra room for the system on other operations. The autonomous treasury management tactic would adjust the limit according to price curve of NEAR and the actual amount of USDT.

However, there is a threshold for minimum amount of NEAR in the system to back the price of NEAR. If NEAR continues to depreciate, the treasury will dwindle in size accordingly, which pushes the system to buy in NEAR with USDT to maintain the safety line of NEAR inventory. Therefore, the continuous purchase may drain the USDT inventory and cause the system to lose stability.

Such a system is relatively aggressive, so USN did not adopt this in full. The core problem is the unpredictability of the market. Though the algorithm could simulate the curve according to changes on the market, the price never lingers precisely on the curve. In fact, the system is doing a series of swing trades. That being said, if such a probability of winning is not very high, then it will instead make the system more vulnerable.

Two take-away points are worth noting at least. First, the reserve could profit from the sale of NEAR when the price is overvalued, securing profits via the receipt of USDT, which is rather stable in price. Meanwhile, the system becomes a little safer. Never a crisis should be wasted, neither should be the prosperity. The acquired USDT at prosperity may be a panacea at unexpected causes. Second, USDT inventory when the system is initiated could boost confidence in early phase, and endow better balancing operability to the system at buying and selling. Besides, professional asset management service is an alternative, feasible but risky as the dependence may be lethal when a black swan event or other unexpected events are encountered; confidence in the system may deviate and losses may incur. That being said, it may not be sustainable to rely solely on a professional asset management team.

2.4 Abundant application scenarios

Having a stable price alone is insufficient to conclude an algorithmic stablecoin as a substantial asset class; demand aside, there must be scenarios for using the stablecoin. With this in mind, an algorithmic stablecoin team must have mutual consent with other projects so that the stablecoin can fit into various scenarios inside and outside other protocols.

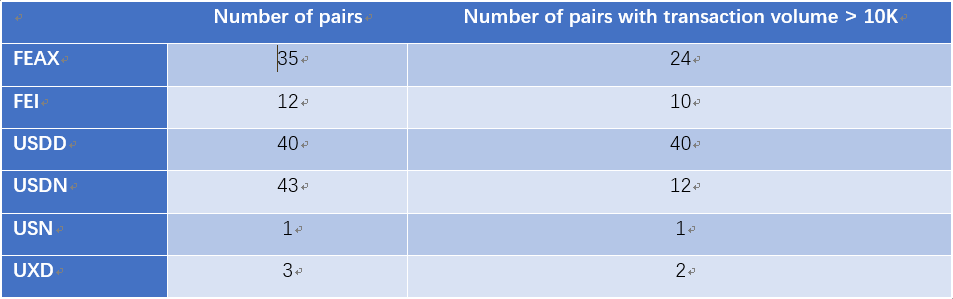

The foundation for the expansion of application scenarios requires the stablecoin to possess sufficient liquidity so that users can redeem it for various coins. That is to say, more funds and more trading pairs must exist in the market, and such pairs must be supported by multiple exchanges. Thus, higher liquidity ameliorates the function of stablecoin as a medium for exchange.

The following table demonstrates the number of trading pairs and associated number of pairs with transactions over US$10,000 for various algorithmic stablecoin. USDN and USDD enjoy freebies from close association with the Layer 1 ecosystem where diverse trading pairs are found in the market. USDN mainly relies on the support of Waves Exchange, whereas USDD receives more support from exchanges — USDD has larger trading volume with 5 trading pairs that are traded with transactions worth over US$10 million daily. Scenarios are broadened in the case of FRAX that FXS will be rewarded to certain pools when trade with other appointed tokens to FRAX, directing more funds in market-making. USN and UXD are weak in issuance volume and duration of issuance, in effect, inactive,

Table 4: Number of trading pairs of mainstream algorithmic stablecoins

Source:Coingecko,Huobi Research

In terms of integration with protocols, official algorithmic stablecoin from the Layer 1 team wins; it originates from the system as an important asset class that it is capable of being integrated with other protocols in the system long before it was born. As an example, UST has a substantial growth thanks to the fixed rate of 20% with Anchor. USDD from Tron also created various scenarios for potential earnings, two venues in short: first, official liquidity pool, including SunSwap, Sun.io, Justlend, Poloniex and Ellipsis; second, liquidity mining from the collaboration with Tron Reserve. USD of NEAR could receive interest from lending protocols such as Burrow, Bastion and Aurigami. Staking and mining on blockchain network with POS consensus is a more viable tactic in the long run. Staking USND on Waves could receive up to 15% (floating rate, actual 0.86%). To stake USDN is to stake the underlying WAVES on Waves Blockchain with LPOS, and earn mining interest thereafter. The system would mint USDN with the earnings and distribute to beneficiaries who stake USDN earlier. Liquidity mining on Waves Exchange is another option where WX could be rewarded.

2.5 Scoring of mainstream algorithmic stablecoin

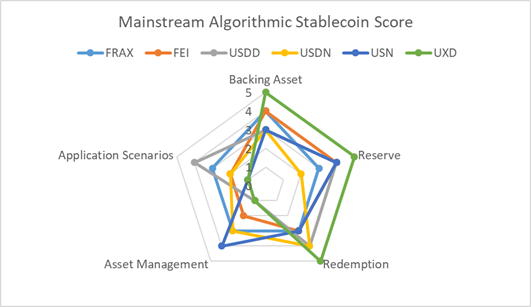

According to the above four aspects, an attempt is made to rank and score various algorithmic stablecoin in the following. The full score for each of the 5 indicators in the chart is 5. With full score in 100, total score is summed after quantifying and weighing each parameter in terms of stablecoin stability and market scalability.

Total score= (Backing Asset* 0.2+ Reserve* 0.3+ Redemption* 0.1 +Asset Management* 0.1+Application Scenarios* 0.3) * 100

Figure 10: Typical algorithmic stablecoin scores

Source:Huobi Research

Backing asset stands for the stability of underlying assets and the degree of risk in the issuing method. UXD ties delta mutual perpetual contract as underlying assets, which is stable most times. FEI is backed by excess ETH and the majority of FRAX is backed by USDC, both of which have a higher probability of keeping the backing assets full at all times. USN and USDD score average on the value of underlying assets and their stability, and are ranked low.

Reserve evaluates the degree of sufficiency in the reserve. The reserve of UXD is to pay for fund fee instead of indemnity, and it remains beyond safety level, ranked full score. FEI has a reserve of 170% in ETH, USN accumulated a reserve of 200% upon issuance; they are ranked lower. USDD is ranked after as the reserve to be established will be in crypto assets composed mostly by stablecoin. USDN has insufficient reserves, so is ranked the lowest.

Redemption evaluates the possibility of rescue from a death spiral and the limiting degree. UXD can be freely redeemed, and the stability is not affected by redemption, so is ranked the highest. Redemptions of any other stablecoin can put pressure on backing assets. USDN and USDD set certain limits on redemption venue, which adds stability to the system, and so are ranked higher.

Asset management takes the ability to earn with reserve funds into consideration. USN has the highest rating for managing reserves algorithmically, while combining other approaches to asset management. FRAX utilizes various AMO to create profiting opportunities for the system; USDN profits from staking; FEI has an AMO in effect but smaller in application range than FRAX; the three are ranked equal in the middle. USDD's backing asset is the burnt TRX, which in principle does not earn income. UXD is unstable on earning profits, even incurring loss; the two are ranked at the bottom.

Application scenarios measures the number of available scenarios for application. To be more specific, the degree of liquidity and profiting scenarios are scrutinized. The top two ranked in this criterion are scored at 4, whereas highest ranked in other criteria are scored at 5, there is room for innovation in this criterion, so the scoring is comparatively low.

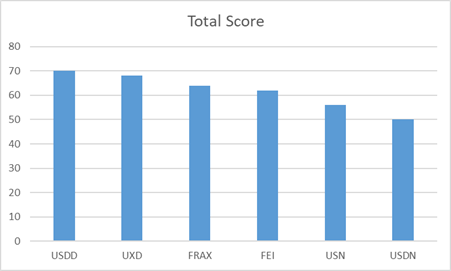

Figure 11: Typical algorithmic stablecoin scoring ranking

Source:Huobi Research

USDD and UXD have the overall higher rankings. Although defects are found in other parameters, USDD has a rather high score due to its diverse and abundant application scenarios (assuming that the scenarios are sustainable). UXD has an extreme stability, but lacks application scenarios. FRAX and FEI are average. USN is also relatively balanced, although the percentage of its reserves will shrink as the size of the stablecoin expands, so its capital management strategy becomes very critical. And because it's only starting out, there are not enough application scenarios to drag down its score. USDN is on the edge of collapse because of insufficient funds in the reserve, and so is ranked the lowest.

3. Other opinions

3.1 Capital efficiency of stablecoin

Some have proposed the trilemma for stablecoin: decentralization, price stability and capital efficiency; of which only two of the three can be achieved at the same time. Based on this theory, while price stability is as prerequisite for stablecoins, is it inevitable that decentralization can only be achieved at the expense of capital efficiency?

At the beginning of this article, the opinion that over-collateralized stablecoin is low on capital efficiency was stated. For the current generation of stablecoin, full collateral has already been a standard setting that higher capital efficiency is provided. On the other hand, if a user overcollateralizes ETH to generate DAI, and if the price of ETH rises, he can enjoy the benefit of asset appreciation. However, if the same thing happens but in algorithmic stablecoin, more stablecoin could be received at the transaction, 30% APR could be desirable in this case (assuming it is sustainable), but the gains from the rise in crypto assets would be off the table. From this standpoint, over-collateralized takes a tradeoff between opportunity for long-term earnings and capital efficiency of issuance, which is an improvement on capital efficiency to some extent. Algorithmic stablecoin achieves short-term capital efficiency, but in the long run, it depends on the profitability of the stablecoin application. Moreover, a reserve is essential, for algorithmic stablecoin that high level of liquidity must be maintained by a certain amount of funds from the reserve. Capital efficiency is lowered in this case, but the protocol bears the burden instead of civilians.

Capital efficiency at issuance and capital efficiency in the long term must be examined separately, and only one can survive at the cost of the other. For users who are more bullish on an asset's potential for appreciation, using it to overcollateralize can preserve the right to future income. If one is more confident about the near-term development and relatively stable returns of a certain ecology, algorithmic stablecoins are a better choice.

3.2 Profitability of algorithmic stablecoin

How profitable can algorithmic stablecoins be? Is it an ideal destination for for enjoying abnormal return?

Algorithmic stablecoin can be deemed as cash or cash equivalent before entering high interest savings plans. Cash is the most liquid assets by all means, and stablecoins literally must be stable in price, therefore, the interest rate should be the lowest as the earnings should be proportional to the risk. If a high-interest savings plan were to be constructed by algorithmic stablecoin, default risk would be the only thing on the table. Risk exposure on different types of algorithmic stablecoin and corresponding ecosystem must be distinguished in order to achieve better investment outcome.

Reference

https://docs.uxd.fi/uxdprotocol/

https://medium.com/fei-protocol

https://docs.neutrino.at/nsbt

https://entrepreneurshandbook.co/luna-brothers-inc-712ec5abe199

https://twitter.com/terra_money/status/1397396984403832835?lang=en

https://twitter.com/terra_money/status/1396780917314621444?s=20

https://samkazemian.medium.com/frax-v2-algorithmic-market-operations-b84521ed7133

About Huobi Research Institute

Huobi Blockchain Application Research Institute (referred to as "Huobi Research Institute") was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain. As the research object, the research goal is to accelerate the research and development of blockchain technology, promote the application of blockchain industry, and promote the ecological optimization of the blockchain industry. The main research content includes industry trends, technology paths, application innovations in the blockchain field, Model exploration, etc. Based on the principles of public welfare, rigor and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms to build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical basis and trend judgments to promote the healthy and sustainable development of the entire blockchain industry.

Official website:

https://research.huobi.com/

Consulting email:

research@huobi.com

Twitter: @Huobi_Research

https://twitter.com/Huobi_Research

Medium: Huobi Research

https://medium.com/huobi-research

Disclaimer

1. The author of this report and his organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report.

2. The information and data cited in this report are from compliance channels. The sources of the information and data are considered reliable by the author, and necessary verifications have been made for their authenticity, accuracy and completeness, but the author makes no guarantee for their authenticity, accuracy or completeness.

3. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment and other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report, unless clearly stipulated by laws and regulations. Readers should not only make business and investment decisions based on this report, nor should they lose their ability to make independent judgments based on this report.

4. The information, opinions and inferences contained in this report only reflect the judgments of the researchers on the date of finalizing this report. In the future, based on industry changes and data and information updates, there is the possibility of updates of opinions and judgments.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the source. If you need a large amount of reference, please inform in advance (see "About Huobi Blockchain Research Institute" for contact information) and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original intent