Produced by | Miaotou APP

Author | Ding Ping, Huxiao APP

Cover Image | Visual China

Warsh is not the storm itself, but he might make the market realize that when the storm comes, the Fed is no longer standing in the same position as before.

Over the past two years, tech giants like Nvidia, Microsoft, and Meta have continuously set new market cap records. AI has almost redefined the entire market's risk appetite, lifting the S&P 500 and Nasdaq indices.

But if we dissect this market rally, AI is merely the story on stage. The real factor propping up U.S. stock valuations is a more crucial premise: that long-term interest rates will ultimately come down.

Only if this premise holds true does the market dare to continue paying high premiums for future earnings, to discount the growth narratives of a few tech giants all the way to the present, and to chase stocks at 30x, 40x, or even higher P/E ratios.

But now, this premise is becoming shaky.

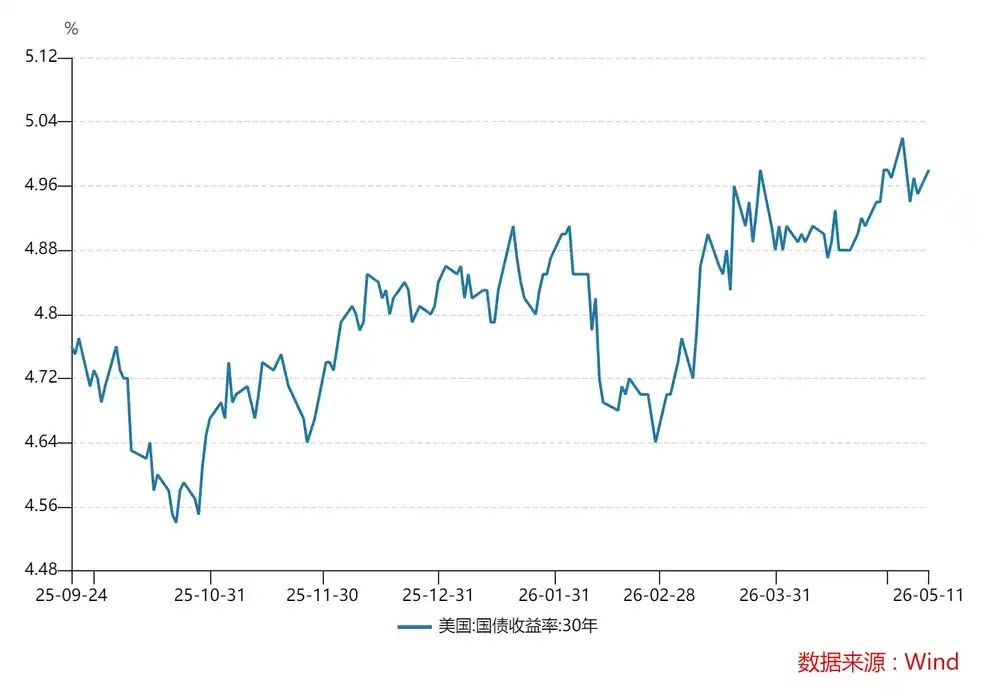

The yield on the 30-year U.S. Treasury note continues to climb, recently breaking through the high level of 5%. For a highly concentrated, expensive, and forward-earnings-narrative-dependent U.S. stock market, the longer long-term rates stay elevated, the more fragile the valuation system becomes.

What's more troublesome is that this pressure is likely to intensify.

On May 15th, Jerome Powell, after serving eight years as Fed Chair, formally stepped down. Kevin Warsh became the next Chairman. Compared to Powell, Warsh may be more tolerant of market pressure, more committed to balance sheet reduction, and less inclined to provide implicit Fed support for financial markets.

Once long-term yields move persistently higher and the Fed no longer soothes the market as quickly as before, the prosperous logic that has supported high U.S. stock valuations may begin to lose its foundation.

The Current Fragility of U.S. Stocks

It's that long-term rates refuse to come down.

For some time now, the market has focused excessively on whether the Fed will cut rates, overlooking a problem: long-term rates are no longer moving in sync with monetary policy.

In theory, central bank rate cuts directly lower short-term rates; if the market believes future rates will stay low, long-term rates should follow suit. But an anomaly has occurred. Even without the Fed hiking, the 30-year Treasury yield continues to rise, hitting a high of 5.13% on May 15th. This indicates the market does not believe long-term U.S. risks will diminish and therefore demands higher risk compensation.

This is precisely where U.S. stocks are most vulnerable right now.

The reason long-term rates are stuck at high levels has at least three layers.

First, inflation has not eased as smoothly as the market hoped.

The latest data shows U.S. April CPI rose 3.8% year-on-year, hitting a nearly three-year high. Core CPI accelerated to 2.8%. More troublingly, U.S.-Iran conflict risks haven't been truly resolved, with persistently high oil prices constantly reinforcing market concerns about imported inflation. As long as inflation expectations can't be firmly suppressed, long-term rates will struggle to fall smoothly.

Second, U.S. fiscal issues are also eroding market confidence in its long-term fiscal discipline.

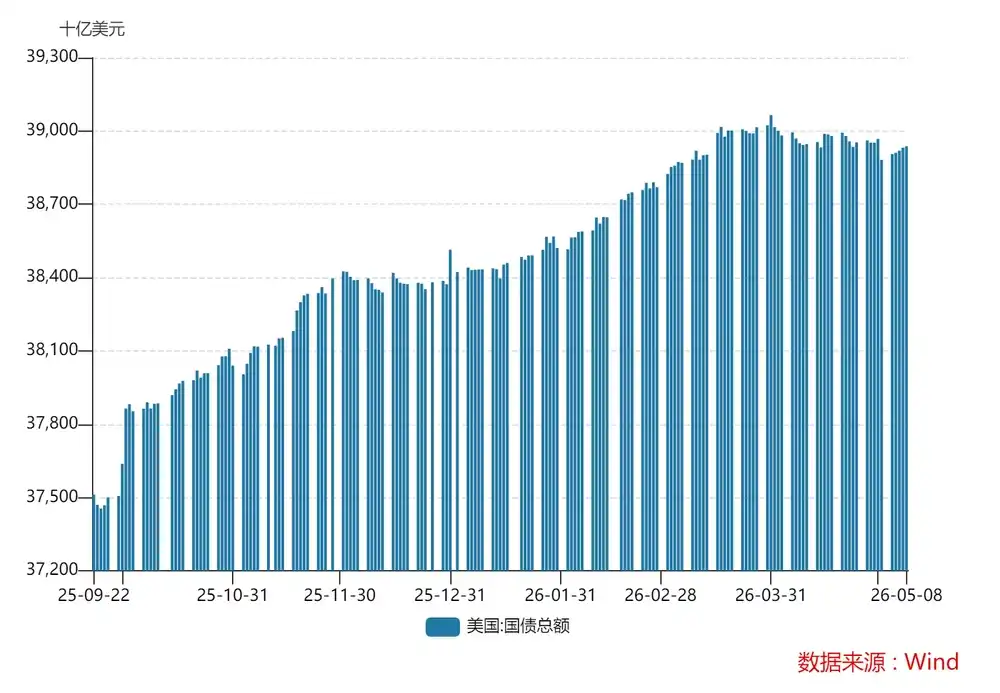

In October 2025, U.S. national debt stood at $38 trillion. Just five months later, that scale breached $39 trillion. Behind this is chronic fiscal deficits (high military and social welfare spending). The Treasury Department issues new bonds to repay maturing old debt, and these new bonds bring higher interest payments, pushing the U.S. into a "Ponzi-like" fiscal debt situation—needing ever-expanding debt to sustain the existing system's stability.

Third, the supply and demand structure for U.S. Treasuries is deteriorating.

On one side, the Treasury continues to increase issuance; on the other, overseas holdings are shrinking due to global de-dollarization. Foreign official sectors are reducing their accumulation, and the U.S. Treasury's share of global reserve assets is in decline, currently at 24%. Supply is increasing while the buying power is weakening, making it increasingly difficult to suppress long-term yields.

When these risks are not alleviated, U.S. Treasuries cease to be just safe assets, and investors naturally demand higher risk compensation.

This is especially dangerous for U.S. stocks.

Because the current U.S. stock market is not a broadly undervalued market relying on gradual earnings delivery. It is a highly concentrated market, supported by a handful of leaders, and extremely sensitive to discount rates.

Once long-term rates stay high, the discounting of future cash flows becomes significantly harsher, and the tolerance range for valuations narrows rapidly. At that point, the first to be hit may not be companies with the worst fundamentals, but precisely those with the best fundamentals but whose valuations are already stretched to the limit.

Bank of America's Hartnett also noted that once the 30-year Treasury yield stabilizes above 5%, rising financing costs and falling risk appetite would first impact high-valuation U.S. tech stocks.

October 2023 demonstrated this once.

At that time, the 30-year yield briefly rose above 5%, and the Nasdaq index corrected about 10% cumulatively over several months. Investors then still believed that once financial conditions worsened further, the Fed would ultimately send soothing signals. But if, after Warsh takes office, this expectation begins to waver, then the market's reaction to a similar long-term rate shock would be entirely different.

Many also like to compare today to 2007, but the truly relevant lesson isn't that rates were high then too. It's that the damage high rates inflict on a financial system never happens instantly. It's more like a chronic erosion: first pressuring financing, then valuations, then balance sheets, finally forcing out the weakest link in the system.

What truly burst in 2007 was real estate, subprime, and shadow banking. Today, what's more dangerous is high-deficit fiscal policy pushing long-term bond supply ever higher, making long-term yields hard to suppress. Banking unrealized losses, commercial real estate tail risks, and risk assets' dependence on liquidity would all be gradually exposed.

Therefore, once long-term rates fail to come down, the valuation foundation for this AI-driven bull market begins to loosen.

This problem will be more severe in the Warsh era.

Why Should Warsh Make the Market Wary?

Because Warsh's inclination towards balance sheet reduction would further push up 30-year Treasury yields, amplifying U.S. stock fragility.

How to understand this?

Fed balance sheet reduction (quantitative tightening, QT) means shrinking the size of the Fed's balance sheet. Previously, to stimulate the economy, the Fed bought many assets like Treasury bonds and mortgage-backed securities (MBS); buying these assets was equivalent to injecting a lot of money into the market. QT is about letting these assets decrease, gradually withdrawing liquidity from the market.

We can simply understand it as: the Fed stops buying newly issued or maturing Treasury bonds from the Treasury Department, and may even sell some of the bonds it holds.

As mentioned above, the U.S. Treasury is currently increasing issuance, and overseas buyers are reducing holdings. If the Fed also reduces its balance sheet, then new and maturing Treasuries can only flow to the market, with the market determining the interest rate level. The result is persistently rising Treasury yields. This also leads to an increasingly heavy interest burden for the government, which is very dangerous for a system relying on issuing new debt to replace old. Once interest costs become too high to support, a Treasury crisis emerges.

Former U.S. Treasury Secretary Paulson also warned that once U.S. Treasuries start losing market buyers, the entire financial system's "risk-free anchor" would be shaken.

If the consequences are so severe, why is Warsh inclined to reduce the balance sheet? This stems from his background.

Warsh served as a Federal Reserve Governor from 2006 to 2011, a period crucial for judging his policy leanings. He experienced the final credit expansion before the financial crisis, the 2008 global financial crisis, and the start of zero interest rates and QE (quantitative easing).

He is not someone who completely denies crisis intervention. On the contrary, during times of strongest systemic risk, he supported the Fed acting as lender of last resort and recognized the necessity of unconventional tools. But later he grew increasingly skeptical: should the prolonged QE post-crisis have persisted for so long?

From his perspective, the post-crisis U.S. economy did not recover in proportion to asset price gains. The real economy's recovery wasn't strong, productivity improvements were limited, but financial asset prices rebounded rapidly driven by liquidity, even surpassing pre-crisis levels.

This likely led Warsh to a very typical conclusion: QE might be good at boosting financial asset prices, but not necessarily equally good at repairing the real economy. Once markets begin to assume "the Fed will ultimately backstop asset prices," the financial system becomes increasingly dependent on liquidity, risk appetite is artificially suppressed long-term, and asset bubbles and misallocations worsen.

So in his logic, if the Fed maintains an oversized balance sheet and suppresses term premiums for too long, markets will ultimately become increasingly unable to function independently of central bank liquidity. In his view, QT is not just about withdrawing liquidity; it's also the Fed proactively withdrawing from its role as a "financial conditions stabilizer."

This is also why Warsh might be more inclined than Powell to advance QT.

Therefore, after Warsh takes office, the high-interest-rate environment will become even more severe, and the Fed may not soothe the market as quickly as before. Once such expectations form, the pressure on the already fragile high-valuation system of U.S. stocks will be further amplified.

The AI Narrative Can't Fully Offset High Rates

Of course, persistently high 30-year Treasury yields are not an absolute negative for U.S. stocks.

If the U.S. economy continues to outperform expectations, corporate earnings are revised upward, and especially if AI genuinely translates into broad productivity gains quickly, then even with elevated long-term rates, risk assets might still hold up. Ultimately, what determines whether the market can digest high rates is economic growth itself.

Over the past year, the reason U.S. stocks, especially tech stocks, continued to rise in a high-rate environment largely relied on this optimistic judgment: AI will significantly boost corporate profits, raise productivity, and open a new growth cycle for the U.S. economy.

But the problem is, the AI narrative currently concentrates more among a few leading companies and capital markets. It hasn't been sufficiently proven to quickly and broadly transform into fundamental improvements for the entire economy.

Take Nvidia as an example. It has indeed created astounding capital returns and market imagination. But such companies share these characteristics: high technological barriers, high profit concentration, limited employment absorption capacity (as of FY2026, Nvidia's global headcount was only about 42,000). Their spillover effects on the overall economy aren't as strong as market sentiment suggests.

In other words, AI can quickly lift valuations for companies like Nvidia and Microsoft in the short term, but it may not equally quickly support broader employment, investment, and expansion in the real economy.

More realistically, the U.S. itself faces problems of insufficient electricity, infrastructure, and industrial support. The faster the AI industry expands, the more it tends to suck capital, energy, and talent further into top tech sectors, making already uneven resource allocation even more concentrated towards leading tech.

This isn't to say AI won't succeed, just to emphasize it hasn't progressed fast enough to fully offset the valuation pressure from persistently high long-term rates.

In other words, the market thinks it's trading AI, but it's actually still trading another thing: low long-term rates and Fed backstops. As long as these two premises hold, high valuations can be justified. Once these premises begin to waver, no matter how strong AI is, it only delays, not cancels, the revaluation.

Warsh is not the source of the risk, but he might be the one who makes this trend harder to reverse.

In summary, while Warsh won't actively create a crisis, he might make the market truly accept for the first time that the high-valuation logic, supported by low long-term rates and Fed backstops, is no longer so stable.