No doubt, over the years, stablecoins have bridged TradFi and DeFi by enabling banks to process payments faster and at lower cost, directly improving efficiency and the overall user experience.

In this context, the critical factor is the Layer-1 network chosen to facilitate this bridge. Notably, Solana [SOL] appears to be strategically positioning itself to capitalize on this opportunity through another key partnership.

Western Union, a global financial services company, has launched USDPT, a new stablecoin on Solana, clearly signaling its confidence in the network’s capability to deliver stablecoin services to users.

At a macro level, the partnership structurally strengthens Western Union’s competitive position in the expanding stablecoin market, as leveraging blockchain infrastructure enables seamless cross-border transactions.

The more consequential question, however, is what this development means for Solana. As stablecoin regulations tighten and competition among Layer-1 networks intensifies, does this partnership reinforce confidence in its long-term fundamentals?

Considering how a recent report by Grayscale highlighted Solana’s growing stablecoin market, USDPT’s launch could not have come at a better time, positioning the network at the forefront of a potential March rally.

Stablecoin surge fuels renewed bullish case for Solana

High liquidity directly drives a network’s long-term growth.

The reasoning is simple. The more liquid a chain is, the easier it becomes to move capital across different sectors like NFTs, RWAs, and staking. This naturally increases on-chain activity and overall network strength.

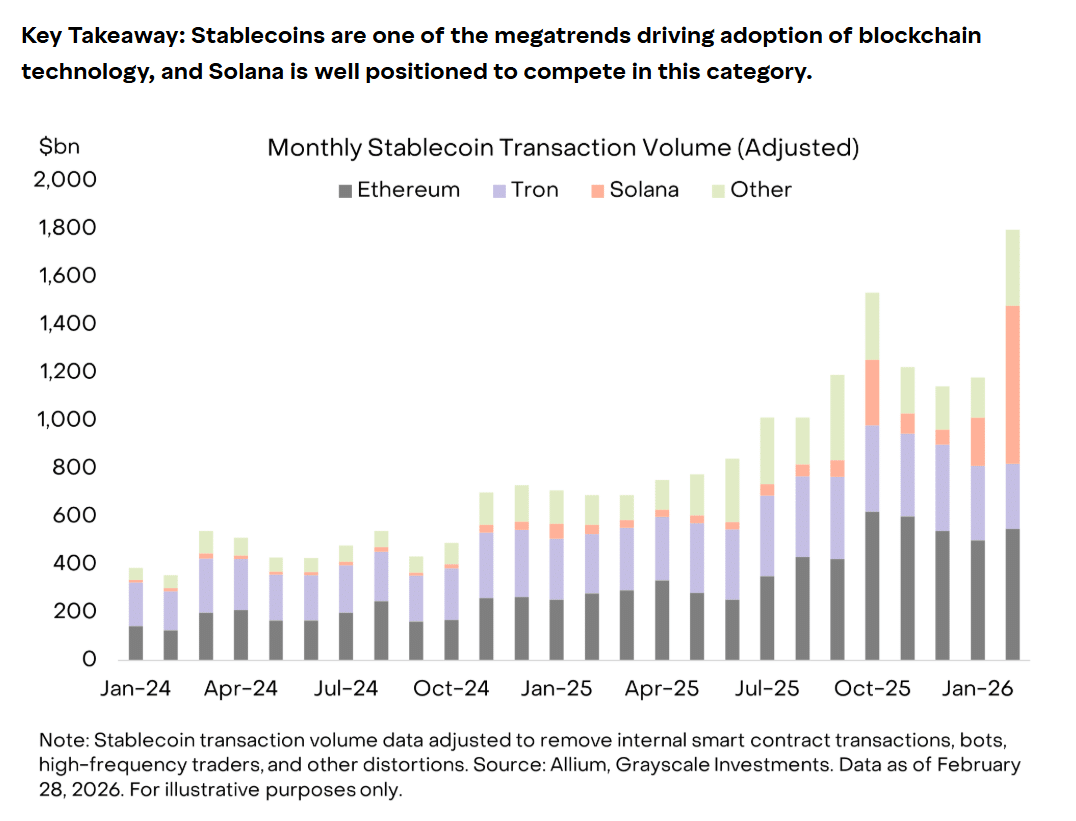

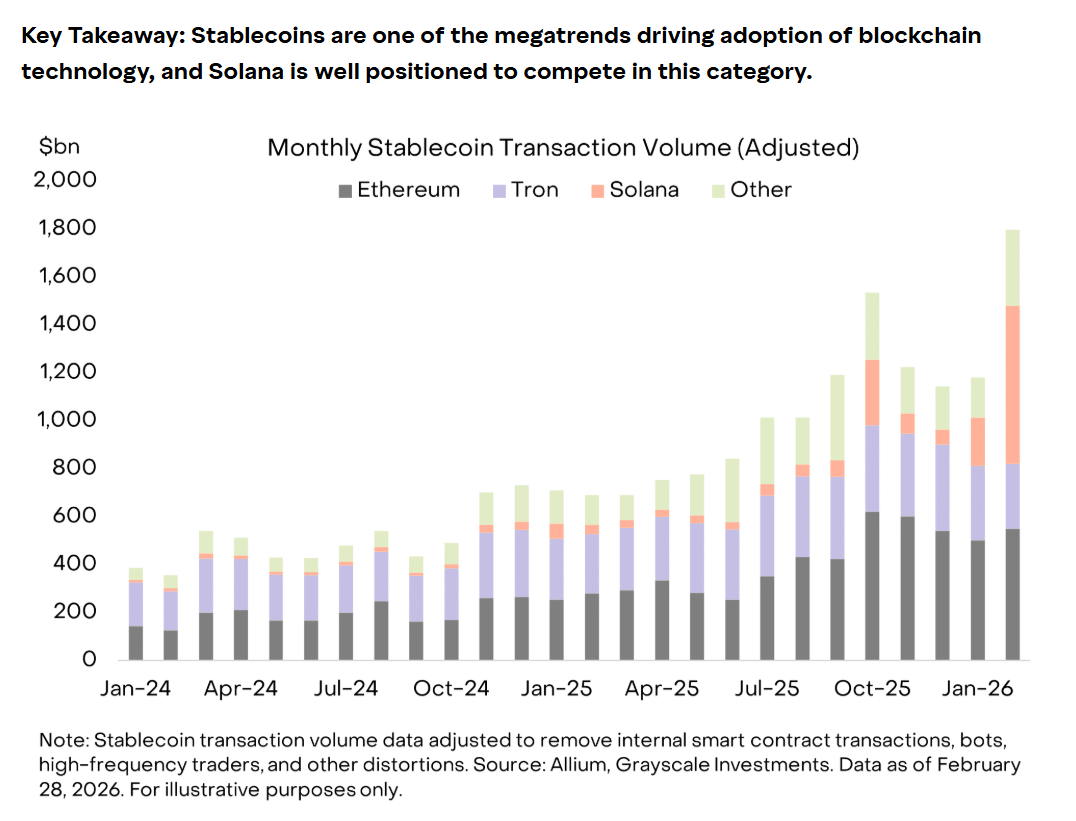

Grayscale’s statement that February was a record month for stablecoins on Solana carries weight in this context. The report noted that stablecoin volume on Solana hit an all‐time high of $650 billion.

Source: Grayscale

Notably, this expansion occurred while SOL saw its weakest monthly run of the year, closing February down 19.98%. This divergence suggests that underlying transactional activity persisted despite price weakness.

Within this context, Circle minting $1 billion in USDC on Solana following the Middle East conflict carries structural importance. Elevated stablecoin issuance during a risk-off phase increases on-chain liquidity depth.

When you add the USDPT launch to the mix, the added liquidity boosts Solana’s capital flows. With Grayscale highlighting strong underlying demand, the setup points to a potential liquidity‐driven repricing.

In this context, SOL’s breakout above $90 may only mark the beginning. With deeper stablecoin liquidity and steady on‐chain activity, Solana appears well‐positioned to lead in March if risk‐on sentiment persists.

Final Summary

- Solana is seeing stronger liquidity and institutional backing, with moves from Western Union and Circle boosting on-chain activity.

- Record stablecoin volume, highlighted by Grayscale, shows solid demand, which could support further upside if market sentiment improves.