Author: EX

Franklin Templeton's $1.5 trillion AUM CIO says "prices are decoupling from fundamentals." The same week, BlackRock joined the UK's 54-member Tokenization Alliance, Robinhood Chain surged into the top 5 DEXs, Hyundai settled cross-border trade with USDT, and Bolivia prepared to integrate USDT into its national payment system. While BTC struggles at $62K, infrastructure is experiencing a silent bull market. The question is not "Will BTC fall further?" but rather "Who will own the toll booths when the infrastructure is complete?"

I. Seven Signals, Occurring in the Same Week

In the second week of July 2026, the crypto market received seven seemingly unrelated pieces of information that actually point in the same direction:

1. Franklin Templeton CIO: Prices and Fundamentals "Decouple"

On July 13, Seth Ginns, CIO of Crypto at Franklin Templeton, stated unequivocally in a CoinDesk interview: "There's a big disconnect between where prices are and real fundamentals."

This isn't some crypto KOL shilling. Franklin Templeton manages $1.5 trillion in assets, and Ginns directly manages the Franklin Crypto portfolio. When he chose to publicly say this with BTC at $62K and amid market panic, Ginns chose to speak out at a moment of market fear—the timing itself is noteworthy. As for Franklin's position changes, the Q3 13F filings will provide the answer.

He mentioned several key signals: - Robinhood's blockchain plans prove traditional financial distribution is migrating to crypto rails. - Tokenized money market funds allow investors to earn yield on-chain. - Revenue-driven token buyback models from DeFi protocols are making fundamental investors pay attention to tokenomics.

2. UK Government Tokenization Alliance: BlackRock, Goldman Sachs, JPMorgan Simultaneously Join

The same day, the UK Treasury-backed Tokenization Taskforce officially announced its list of 54 members. This isn't a proof-of-concept sandbox—it comes with a 2-year roadmap: to put repos, gilts, and funds on-chain. The report also lists Ripple under the "Fusion Model," targeting £44 billion in annual output by 2035.

The list includes the world's largest asset managers, top-tier investment banks, and core UK financial infrastructure operators. When BlackRock, Goldman Sachs, JPMorgan, and Morgan Stanley appear simultaneously on a government tokenization roadmap, this is no longer a "crypto narrative"—it's an upgrade plan for traditional financial infrastructure.

3. Robinhood Chain: Born for Stock Tokenization, Taken Over by Meme Coins

Launched less than two weeks ago, Robinhood's blockchain has already surged into the top five in DEX trading volume (confirmed by Bernstein), with TVL exceeding $135 million, attracting 800,000 addresses. Although meme coins are currently active, not tokenized stocks, the infrastructure is already there—Robinhood's 23 million user base is incomparable to any crypto-native DEX.

4. Hyundai Uses USDT for Real Trade Settlement

South Korea's Hyundai Motor completed a treasury settlement pilot using the USDT stablecoin for cross-border trade between the US and Mexico. This isn't a proof-of-concept statement—it's a global manufacturing giant using stablecoins to replace traditional cross-border banking channels.

Hyundai's annual revenue exceeds $200 billion. If this pilot expands to its global supply chain, it will change the infrastructure landscape for global trade settlement.

5. Bolivia Considers Integrating USDT into National Payment System

Facing a dollar shortage, the Central Bank of Bolivia is considering formally integrating Tether's USDT into the national payment system. Annual transaction volume has already reached $430 million. This is a typical case of a developing country using stablecoins to replace dollar liquidity—continuing El Salvador's path for national cryptocurrency but more direct in practical terms.

6. BTC ETFs End 8 Weeks of Consecutive Outflows

After 8 weeks of continuous outflows, BTC ETFs recorded a net inflow of $197 million last week. This is not a small number—but it occurred against a backdrop of BTC price testing $62K, escalating Middle East military conflicts, and renewed Fed rate hike expectations. Capital chose crypto exposure in a "risk-off" environment.

7. SBI Fully Pivots to Solana + Yen Stablecoin

Japanese financial giant SBI Holdings pivoted its entire blockchain strategy to Solana, including tokenized issuance and yen stablecoin plans, and launched a retail payment pilot in partnership with Lawson convenience stores. This is Asia's "first shot" of institutions deploying stablecoins in real-world payment scenarios.

II. The Essence of the Great Divergence: The "Price Narrative" Can't Keep Up with the "Infrastructure Narrative"

Over the past decade, the core narrative of the crypto market has always been "price": when will it rise, how much, when to sell. This narrative framework made BTC's price volatility a proxy for the entire industry's "confidence index."

But a fundamental change is happening in 2026: infrastructure construction no longer depends on BTC price.

• When Franklin Templeton launched tokenized funds, it didn't wait for BTC to return to $100K.

• When BlackRock joined the UK Tokenization Taskforce, it didn't wait for market sentiment to improve.

• When Hyundai tested USDT for cross-border settlement, it didn't wait for the SEC to clarify the regulatory framework.

• When SBI deployed Solana tokenization, it didn't wait for yen depreciation pressures to ease.

The decision clock for these moves is the 5-10 year structural change in the market, not the 3-6 month BTC price cycle. This is the core of the "Great Divergence": the decision frequency of the leading infrastructure indicators and the fluctuation frequency of the lagging price indicators are not on the same time dimension.

In the words of Franklin Templeton's CIO: the current depth of institutional participation is at its "years strongest." But price does not reflect this—because price is still driven by retail sentiment and macro liquidity, while infrastructure is driven by institutional strategy and regulatory roadmaps.

III. This Is Not a Cryptocurrency "Valuation Repair" Story

A common market interpretation framework is: "Fundamentals are good, and price will eventually catch up." This is an overly simplified and dangerous conclusion.

What is truly worth paying attention to is not "whether the price will repair," but "Who will charge for using this infrastructure when it's complete?"

Characteristics of the current infrastructure wave:

1. Shifting from "Decentralization" to "Traditional Infrastructure Upgrade": The goal of the UK Taskforce is not to create new DeFi protocols, but to make repos, gilts, and funds run on the blockchain. This means blockchain is becoming a "Layer 2 operating system" for financial infrastructure, not an alternative.

2. Coexistence of Permissioned and Public Blockchains: The tokenization alliance of 54 institutions cannot run on permissionless public chains. The more likely scenario is: permissioned chains handle compliant clearing, public chains handle circulation and programmability. This means the middle layer of infrastructure—compliance bridging, custody, KYC/AML—becomes a critical chokepoint.

3. Sovereign States and Real Businesses Enter Faster Than Expected: Bolivia's national payment system, Hyundai's trade settlement, SBI's retail payments—these are not "crypto-native" stories. They come from real-world demand for more efficient financial pipelines, and crypto happens to provide the technical solution.

4. Stablecoins Evolve from "Trading Tools" to "Real Economy Pipelines": Hyundai's cross-border settlement isn't using USDT for speculation, but to replace SWIFT. Bolivia isn't using USDT for DeFi, but to replace dollar cash. This fundamentally changes the TAM (Total Addressable Market) for stablecoins.

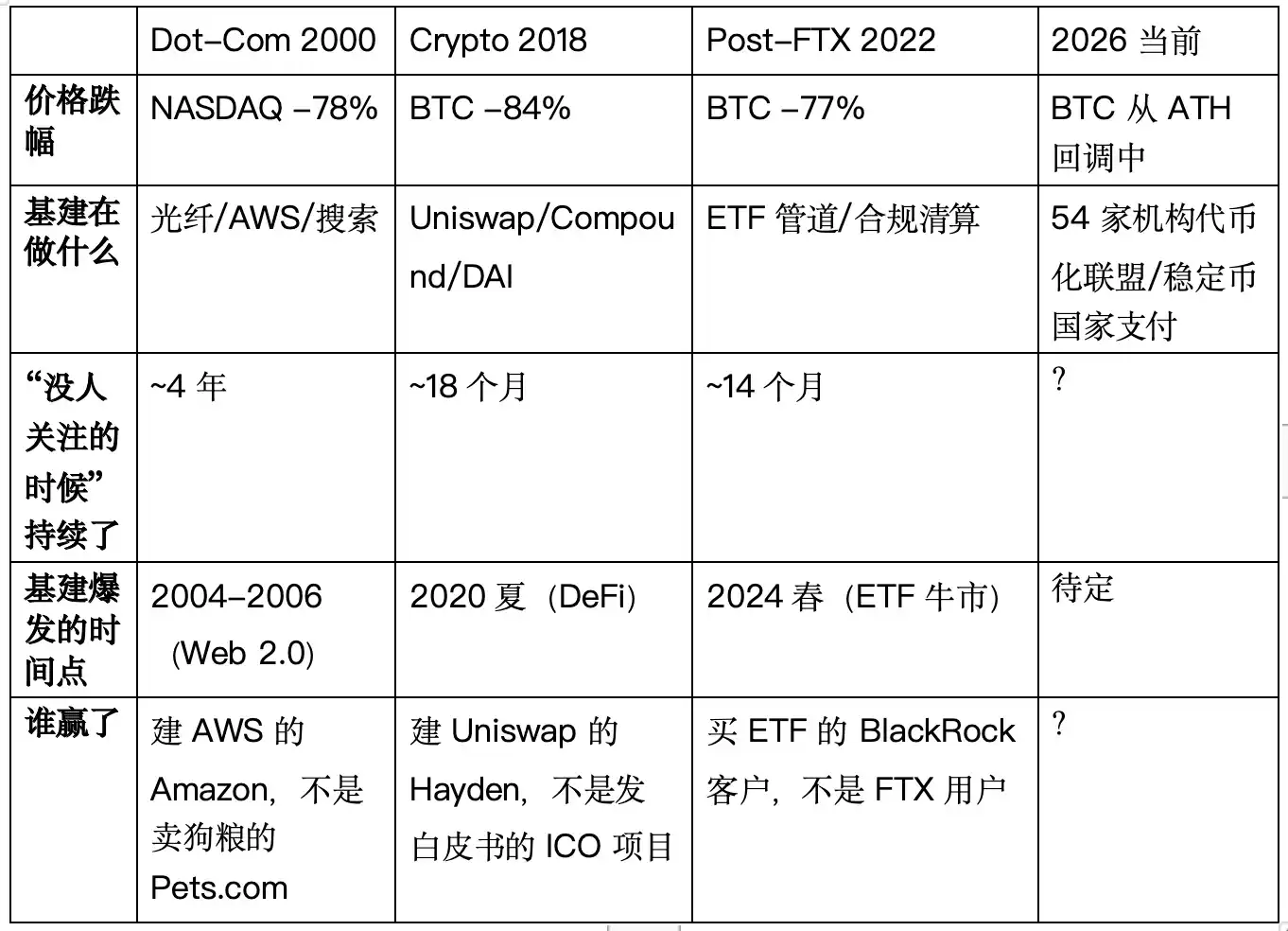

IV. History Doesn't Repeat, But It Rhymes: The Endings of Three "Price-Infrastructure Divergence" Periods

If the "Great Divergence" of 2026 feels unfamiliar, history has its echoes. Over the past 25 years, at least three highly similar cycles have occurred—each time, price collapse masked accelerated infrastructure construction. And each time, the victory of infrastructure occurred 12-24 months after prices bottomed.

📉 Cycle One: 2000-2002 Dot-Com Bubble → Birth of AWS

What happened: The Nasdaq fell from 5,048 points to 1,114 points, a 78% drop. Pets.com and Webvan went bankrupt. Yet during the same period, Amazon's stock fell from $107 to $7 (a 93% drop), but Jeff Bezos did not stop investing—he was secretly developing an internal project called "Amazon Web Services." Google launched AdWords in 2002, laying the foundation for search advertising infrastructure.

Infrastructure vs. Price Divergence: Fiber optic broadband deployment reached historical peaks between 2001-2003 (during the bubble, Global Crossing laid 100,000 miles of fiber, which was acquired for 10% of the cost after bankruptcy). Server infrastructure, e-commerce logistics networks, search engine algorithms—all this "Web 2.0" infrastructure was completed when the stock market crashed and no one was paying attention.

Outcome: AWS officially launched in 2006 and became Amazon's largest profit source a decade later. Google AdWords became the most profitable advertising product in human history. Fiber networks became the transmission layer for YouTube, Netflix, and Zoom. The infrastructure built in the darkest period became the toll booths in the next cycle.

📉 Cycle Two: 2018-2019 Crypto Winter → DeFi Summer 2020

What happened: BTC fell from $19,783 to $3,122 (an 84% drop). The ICO bubble completely burst, and "blockchain" was declared dead in the mainstream media. Yet during the same period—

• Uniswap released its first version (V1) at Devcon 4 in November 2018.

• Compound completed its seed round and began building its on-chain lending protocol.

• MakerDAO's DAI stablecoin achieved scale in 2019.

• Synthetix, Aave (then called ETHLend) all completed core product iterations during this period.

Infrastructure vs. Price Divergence: While BTC was bottoming around $3,000, DeFi's Total Value Locked (TVL) was less than $500 million—almost negligible. But the smart contract infrastructure (AMM models, lending pools, price oracles) was precisely built during this "ignored" period.

Outcome: In June 2020, Compound launched the COMP token, initiating "liquidity mining." DeFi Summer exploded—TVL surged from less than $1 billion to $15 billion (a 15x increase), and the UNI airdrop ($1,200+ per person) became the most famous wealth distribution event in crypto history. Those who understood the Uniswap whitepaper during the 2019 bear market became the winners of DeFi in 2020.

📉 Cycle Three: 2022-2023 FTX Collapse → BTC ETF Approval

What happened: FTX collapsed in November 2022, with BTC falling to $15,599. SBF was arrested, and BlockFi, Celsius, and Voyager filed for bankruptcy. The crypto industry was seen by Wall Street and regulators as a "crime scene."

Yet during the same period— - BlackRock filed its application for a spot BTC ETF on June 15, 2023. - Fidelity, Invesco, VanEck, ARK followed suit. - Traditional financial institutions accelerated the behind-the-scenes construction of crypto custody, compliant clearing, and market-making infrastructure.

Infrastructure vs. Price Divergence: While retail investors capitulated at $16,000, the world's largest asset manager was preparing to build a regulated, institutionally accessible market access pipeline for crypto assets.

Outcome: In January 2024, the SEC approved 11 spot BTC ETFs. First-day trading volume was $4.6 billion. BTC rose from $25K to over $73K within 12 months. ETFs were not the end point for price—they were the starting point for price rediscovering the value of infrastructure.

🔑 The Common Pattern These Three Cycles Tell Us

Core Pattern: Price can drop 80%, but if infrastructure construction doesn't stop, then 12-24 months later, the infrastructure will prove its value through price.

The difference in the current 2026 cycle is: The infrastructure builders this time are not crypto-native entrepreneurs (like Uniswap in 2018), but BlackRock, Franklin Templeton, JPMorgan, the UK government, and Hyundai. This means—

1. Higher probability of infrastructure completion. The balance sheets and regulatory relationships of these institutions mean the tokenization alliance won't dissolve just because BTC falls to $50K.

2. But the beneficiaries of the infrastructure may be different. In 2018, Uniswap was built by crypto-native teams; in 2020, the big money was made by DeFi users. In 2026, the tokenization alliance is being built by the world's largest financial institutions—when the infrastructure is complete, the toll booths may not belong to the community.

3. The time window may be shortening. It took only 14 months from Post-FTX to ETF approval, much shorter than the 4 years of the Dot-Com era. If the UK Tokenization Taskforce's 2-year roadmap is real, we may see the first results in 2027-2028.

⚠️ Past cycle performance does not indicate future results. Current market structure, regulatory environment, and macroeconomic background differ significantly from the aforementioned cycles. The historical comparisons in this article are for analytical framework reference only and do not constitute any prediction or guarantee of future trends.

V. The Separation of Price and Infrastructure Valuation Logic

When BlackRock with its $11.5 trillion AUM joins a tokenization alliance, when Hyundai uses stablecoins for real trade, when Bolivia's sovereign government chooses USDT over traditional banks—the value narrative of the crypto industry is no longer solely dependent on BTC price.

But this does not mean BTC price loses importance. BTC remains the core liquidity anchor for the entire industry. Logically, if BTC price remains under pressure, ETFs see continuous outflows, and the macro environment worsens further (Fed rate hikes, oil prices pushing inflation), the pace of infrastructure construction may slow, but is not expected to stop. This is the core meaning of the "Great Divergence": price and infrastructure are two independent variables, and their coupling is weakening.

Adding a note: This article argues that "the valuation logic of infrastructure and price is separating," not that "infrastructure investment is superior to other strategies." Infrastructure construction may also face uncertainties such as regulatory delays, technical risks, and slower-than-expected commercial adoption. All investment decisions should be evaluated independently by the reader.

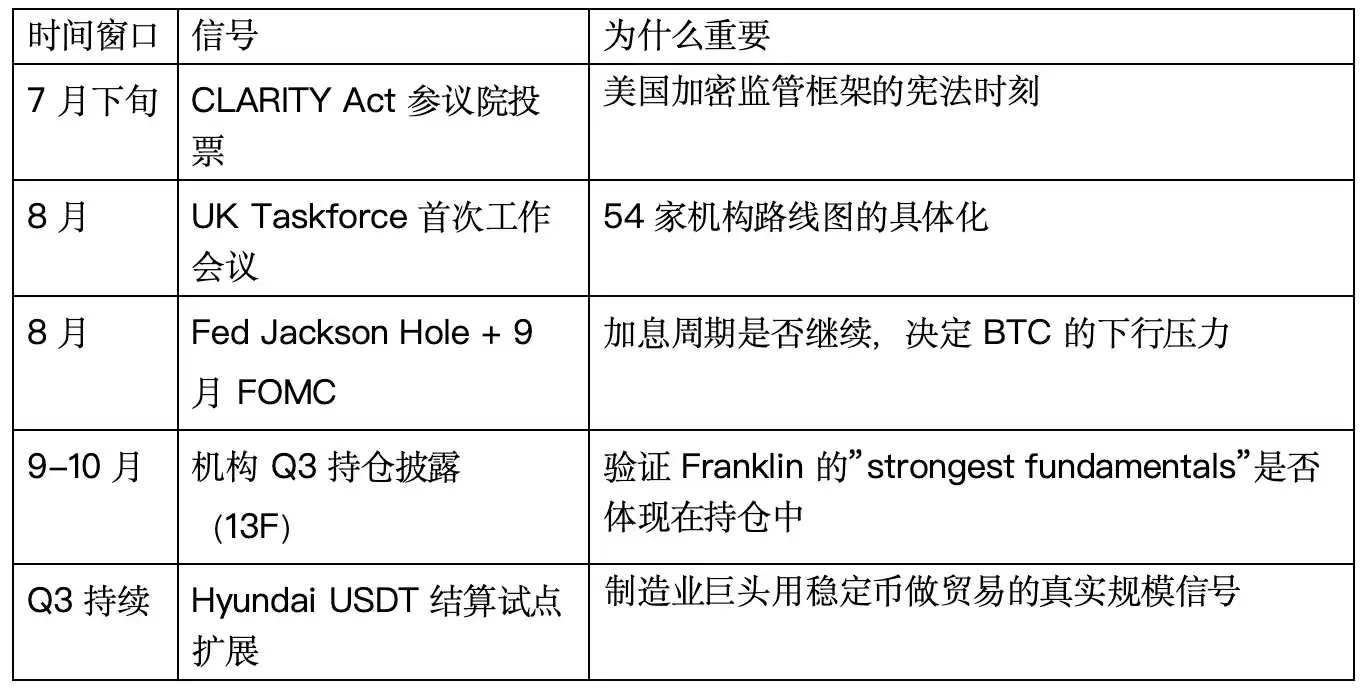

VI. Observation Window: What to Watch in the Next 90 Days?

![How high can MemeCore [M] rally as it leads top 100 with 16% gains?](https://d1x7dwosqaosdj.cloudfront.net/images/2026-07/3d45ef1ea56e45f6a19ae78972d369b7.jpg)