Author: Charlie

Compiled by: Luffy, Foresight News

For a long time, the price movements of the entire crypto market have revolved around Bitcoin. Today, that era is coming to an end.

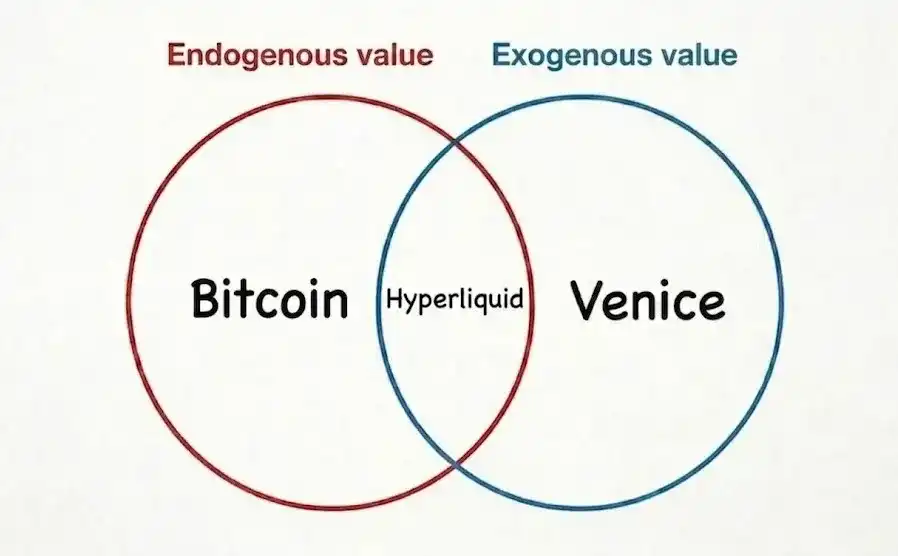

The crypto economy has now diverged into two major camps: endogenous assets and exogenous assets.

The so-called endogenous assets are the traditional crypto categories familiar to the public: the value of these tokens and projects is entirely dependent on the rise and fall of the overall crypto asset market. Exogenous assets, on the other hand, only nominally belong to the crypto track; their value movements are increasingly independent of the crypto market.

Bitcoin's value stems from its inherent attributes and is reflected in its price. Price increases further reinforce the market's perception of its value attributes. At the peak of a bull market, Bitcoin is hailed as 'interstellar universal currency,' the most scarce digital circulating asset in human hands; at the trough of a bear market, it is disparaged as a digital collectible with no cash flow support.

Hyperliquid sits between the two camps. Most of its business still relies on crypto market conditions, but both supply and demand are continuously expanding. Many on-chain financial infrastructures fall into this category, with underlying assets gradually shifting towards tokenized real-world asset categories.

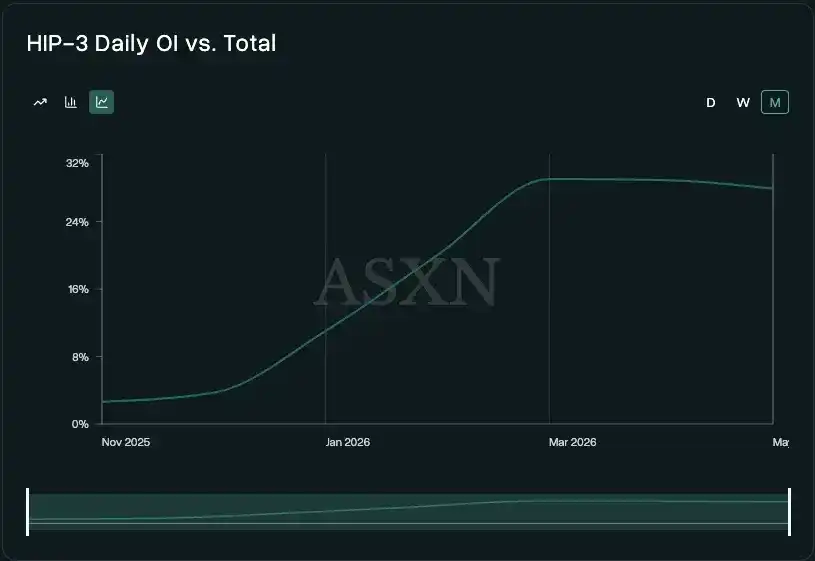

HIP-3 open interest roughly reflects the activity of non-crypto-related trading. Currently, HIP-3 contracts account for about 30% of Hyperliquid's total open interest, whereas in November 2025, this proportion was only 4%. The upcoming HIP-4 prediction market will further drive growth, bringing new trading users and trading targets.

Projects like Venice fall entirely into the exogenous camp; their development logic is completely detached from the crypto market. Although there is some overlap in user base, its business model leans more towards consumer-grade artificial intelligence rather than native crypto products like Uniswap. Uniswap's core business is still users trading various endogenous assets, so its performance naturally fluctuates with asset prices; Venice, however, packages private multimodal inference services and adopts a 'pay-per-use + subscription' fee model.

Venice's only connection to the crypto field is its choice of tokens as a value-carrying medium, and the fact that some of its compute power providers have a crypto industry background. Project lead Erik Voorhees is deeply involved in the crypto industry and believes that, if used properly, tokens can be excellent marketing tools.

Public company Figure is also a typical case. This fintech lending company developed its own blockchain, reducing the approval time for home equity loans to under 5 minutes. For them, blockchain is just supporting technology; the core value lies in the credit business itself.

The large-scale rise of exogenous tracks, whether in the token market or the listed company sector, has profound significance. In the past, because the vast majority of business models were deeply tied to crypto asset prices, pure bottom-up fundamental investing was difficult to implement. The crypto industry has not been without narratives favoring 'blockchain over Bitcoin,' but past cycles always reverted to Bitcoin's performance. The fundamental reason was that these tracks never managed to establish stable demand and generate continuous revenue; even when there was revenue, it couldn't be transmitted to token value. Once token prices stopped rising, the projects lost their support.

This cycle is fundamentally different. Now we can clearly see paying user groups and payment logic. Demand in most tracks is quantifiable and is no longer driven purely by sentiment hype. Simultaneously, the mechanisms for tokens as value carriers are continuously improving. Venice's revenue comes from users genuinely paying for AI inference services; even if the overall crypto market declines, its business won't be significantly impacted because it doesn't rely on token price movements. This cycle possesses two core advantages that previous booms lacked: sustainable real usage demand, and investors beginning to invest based on fundamentals rather than market narratives alone.

The stablecoin track in the private market is similar. In March 2026, Mastercard announced it would acquire BVNK for up to $1.8 billion. This company was valued at just $750 million when it completed its Series B round 15 months prior. Another stablecoin-related company, Bridge, was acquired by Stripe for $1.1 billion in February 2025. According to Stripe's annual report, Bridge's current business is growing at four times per year. The development of these companies is completely decoupled from the crypto industry's bull and bear cycles.

This is not to say we are bearish on endogenous assets. Just as gold and even small gold mining companies have their place in an investment portfolio, Bitcoin and a host of endogenous crypto assets also have their place. But the performance drivers and market correlations of the two asset types have fundamentally diverged, and the data confirms this.

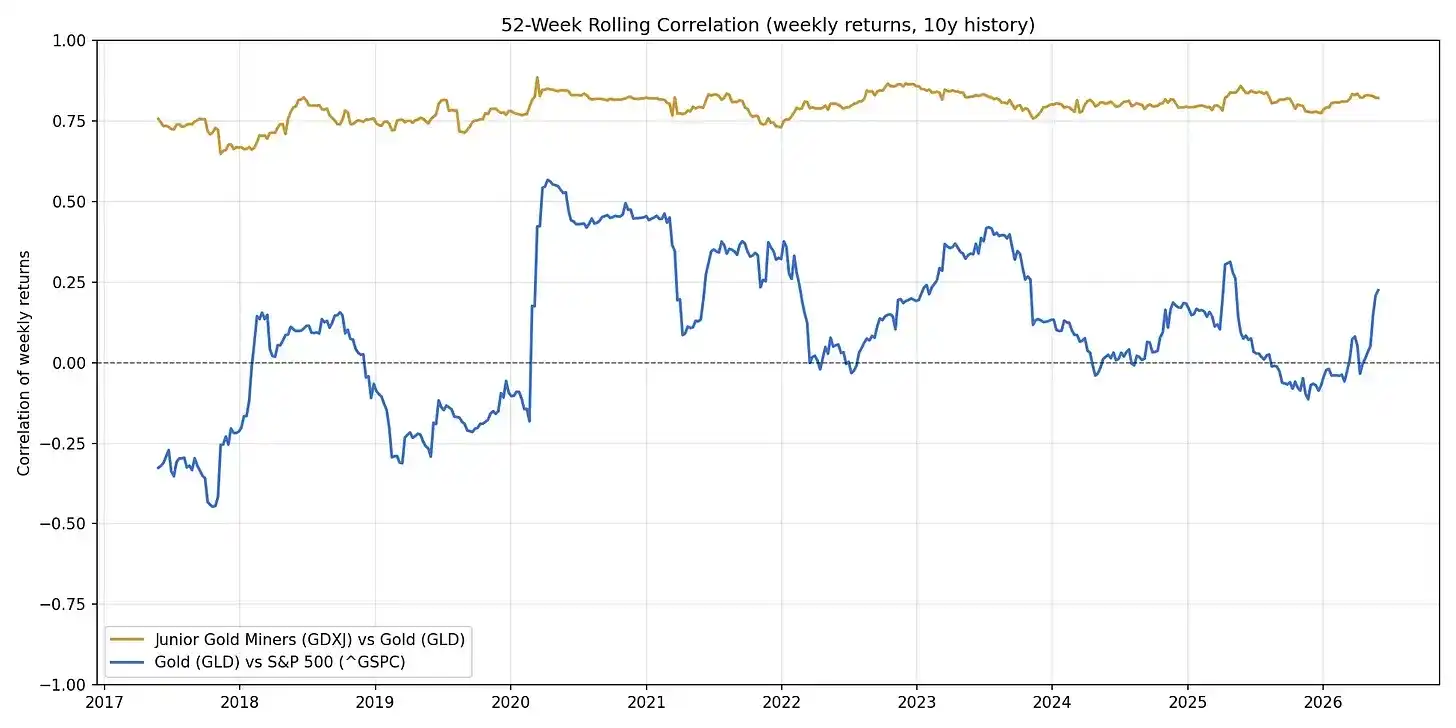

This analogy can be visualized: The correlation coefficient between small gold mining stocks and gold prices remains around 0.75 over the long term. This is precisely the current state of the traditional crypto market — a host of crypto assets are like small gold mines, with Bitcoin corresponding to gold. The entire track is leveraged investment against Bitcoin. The blue curve in the chart represents another relationship: Gold and the S&P 500 index exhibit weak linkage due to macroeconomic influences, but each follows its own independent logic. This is also the future direction for exogenous assets. In the long run, these assets will gradually break free from the 'following Bitcoin's ups and downs' trend.

It should be noted that many exogenous assets themselves issue tokens. This phenomenon both confirms the above trend and represents a special case.

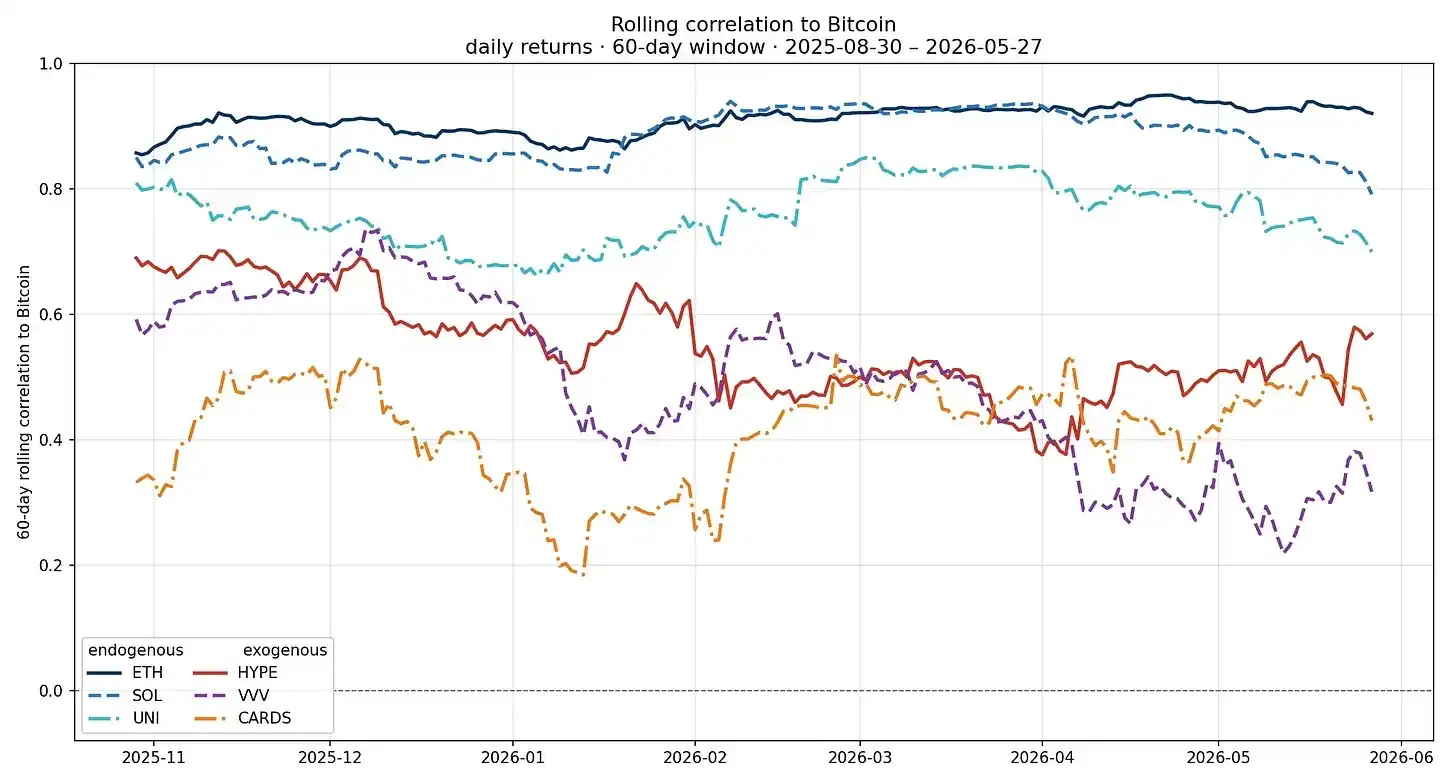

Currently, the vast majority of endogenous assets remain highly correlated with Bitcoin's movements. A few exogenous assets show reduced correlation, but due to their short development cycles, they don't yet offer strong reference value. Industry patterns have always been fundamentals first, followed by changes in market relationships.

This change has also completely rewritten the logic of industry analysis. Researching exogenous assets requires fundamental due diligence like analyzing traditional companies: mapping paying user groups, calculating unit economics, and assessing industry moats. Bitcoin price is no longer the primary reference indicator. Analyzing such projects is more akin to fintech investors making judgments, with the extra step of asset custody.

Here are the currently promising exogenous tracks:

- On-chain exchanges and brokerage service providers

- Settlement and redemption solutions for long-tail asset tokenization

- Deep integration of crypto + AI (private inference, distributed open-source model training like Nous Research's Psyche, etc.)

- New digital banks (Payy and Raycash focusing on privacy protection are worth watching; Aztec and Zama providing programmable privacy infrastructure also have potential)

- Lending track (Morpho has become mainstream in institutional repo markets; smaller projects like Valinor, 3jane focus on private credit niches)

- Stablecoin issuers, real-world asset tokenization service providers

- Payment rails (In general payments, Stripe and Tempo are industry benchmarks; in agent payments, Coinbase currently leads)

- Non-financial crypto consumer products (Represented by Venice, Collector Crypt; these projects imbue tokens with real-world business value, driving product adoption and marketing empowerment)

- Agent economy (Core opportunity lies in the access layer for agents, service providers, and creator collaboration ecosystems, which are less replaceable. Cloudflare is ahead in deployment, but whether it will charge for traffic or merely provide basic functional services remains to be seen)

At this stage, investing in equity of related companies remains the safest way to gain exposure to the above tracks; quality token targets are exceptional cases. The role of tokens will only increase as their value-carrying mechanisms continue to optimize, a process requiring joint efforts from regulators and the entire industry. Progress is being made: on the regulatory front, the CLARITY Act is steadily advancing; on the industry side, institutions like Blockworks are promoting market information transparency. The token mechanism still has a long way to go.

But none of these details change a core trend: The driving forces of the crypto market are shifting from a single factor to multiple factors. The focus of industry research is shifting from interpreting Bitcoin price charts to deep-diving into company fundamentals. In the next decade, there will be no need to wonder why the 'crypto market' no longer moves in unison, because the industry landscape has been fundamentally renewed.