FOMO in altcoins isn’t always about the price action or technical strength.

Instead, stablecoin flows often set the tone, and Solana [SOL] seems to be following that pattern. Its network fundamentals are holding up well, even though the price has lagged, hinting at potential undervaluation that the market may be overlooking.

Looking at Q1, SOL was one of the bigger losers among high-cap altcoins, falling by nearly 35%. And yet, beneath the price weakness, its stablecoin market cap actually grew by around 5% – A sign of clear divergence between on-chain activity and market performance.

Backing that up, Solana’s on-chain signals are pointing to growing network usage too.

Total transaction volume on the network recently crossed 500 billion, well ahead of the next 13 blockchains combined, making it clear that Solana is still the go-to for on-chain activity. Unique addresses on the network have also been dominant, further proving that the ecosystem is active even if the price isn’t keeping up.

In short, when you compare network activity to market performance, Solana’s fundamentals remain strong. That kind of divergence usually points to undervaluation, hinting that SOL could be gearing up for a rebound.

The real story, though, is stablecoin flows. Naturally, the big question is – Could liquidity be the main FOMO trigger for SOL this cycle?

Stablecoin inflows are supercharging Solana’s DeFi this cycle

The pace of growth in DeFi is really showing through a few key sectors, and stablecoins are at the forefront.

The logic is simple – When on-chain liquidity is high, capital naturally starts moving across the network, powering activity and usage. Building on that momentum, the Real World Asset (RWA) sector continues to outperform most other areas, and Solana is no exception.

From a technical standpoint, even with Q1 price weakness, Solana closed the quarter with its total RWA value hitting a fresh all-time high of $2 billion – Marking more than a 40% QoQ jump. Add in the recent partnership with SoFi, and it’s clear Solana may be strategically leaning into this DeFi momentum, potentially supercharging network activity and capital flows even more.

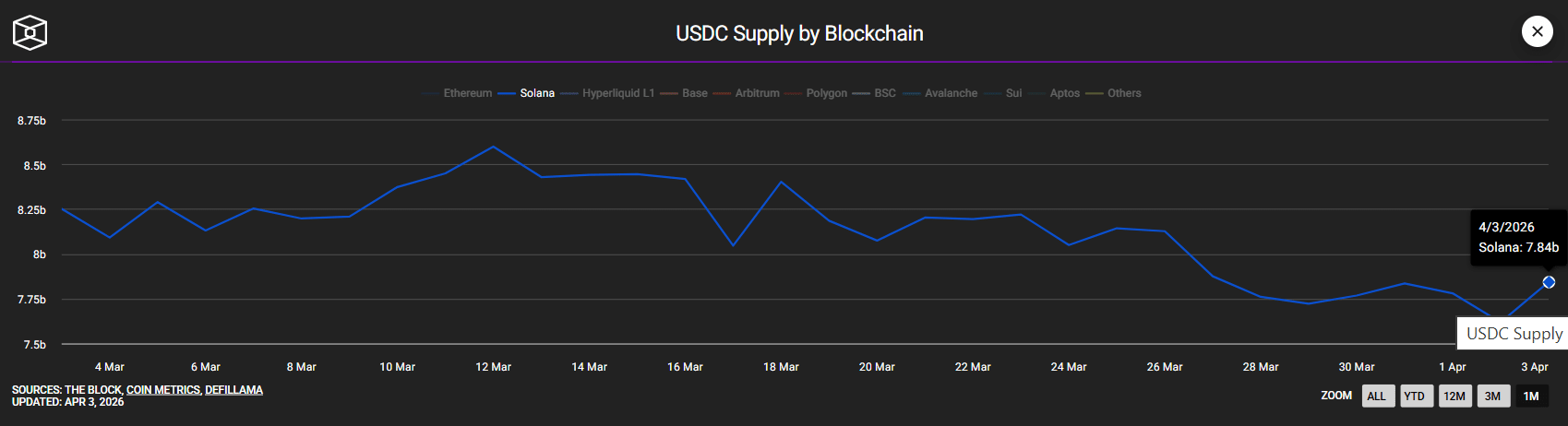

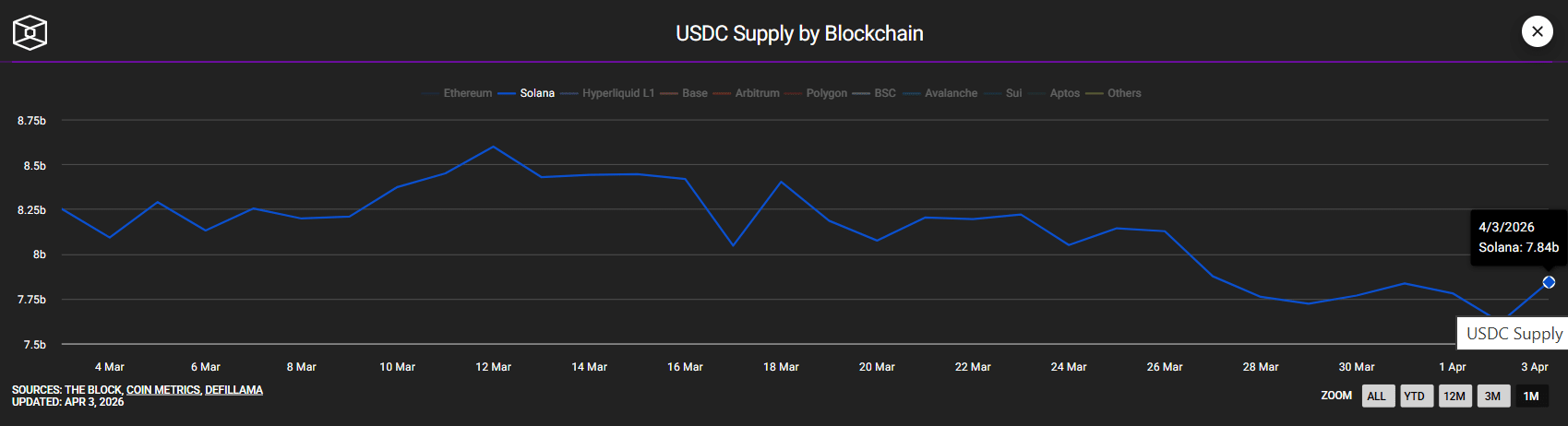

Against this backdrop, the recent USDC supply mint on Solana doesn’t feel like a random event.

Instead, with strong network fundamentals, usage outpacing other chains, partnerships expanding stablecoin use cases, and healthy capital flows across key growth sectors, it’s clear that Circle is positioning USDC as a central driver of activity on Solana.

Consequently, this could make liquidity (not price action) the main FOMO trigger for SOL in this cycle.

Final Summary

- Despite price weakness, strong on-chain activity, rising USDC supply, and growing network usage highlight Solana’s fundamentals and potential undervaluation.

- RWA value hitting $2 billion, plus strategic moves like the SoFi partnership, position USDC liquidity as the likely key FOMO trigger for SOL.