Africa's payments market exhibits distinct characteristics, boasting the world's highest mobile payment penetration rate and the fastest growth in cryptocurrency adoption. This is not a market-level coincidence, but a necessity arising from the long-term evolution of macroeconomic structures.

This article analyzes the two deep-seated structural drivers behind this necessity: (1) Africa's long-term reliance on resource exports, trade circulation, and remittances has created immense demand for cross-border settlement and transfers; (2) Africa's domestic financial infrastructure is underdeveloped, suffering from international bank de-risking and poor foreign exchange management, leading to a persistent absence of commercial banking and stubborn inflationary pressures.

These two forces jointly create a vacuum where mobile payments and cryptocurrencies have flourished: mobile payment platforms have replaced banks as daily payment channels, while cryptocurrencies assume the role previously held by local fiat currencies or the US dollar in emerging economies, acting both as a store of value against currency depreciation and a low-cost medium for cross-border exchange.

The key dividing line on this continent is the Sahara Desert: North of the Sahara integrates into the Middle East and North Africa (MENA) framework, anchored by oil and aligned with the Middle East; while Sub-Saharan Africa (SSA), plagued by severe dollar shortages and fragmented currency systems, has fostered a vast market with a natural demand for mobile payments and cryptocurrencies. SSA countries like Nigeria, Kenya, and South Africa rank among the world's highest in mobile payment and cryptocurrency adoption rates.

1 Africa's Macroeconomic Panorama: A Vast, Young, Yet Commodity-Dependent Primary Economy

1.1 Demographic Structure

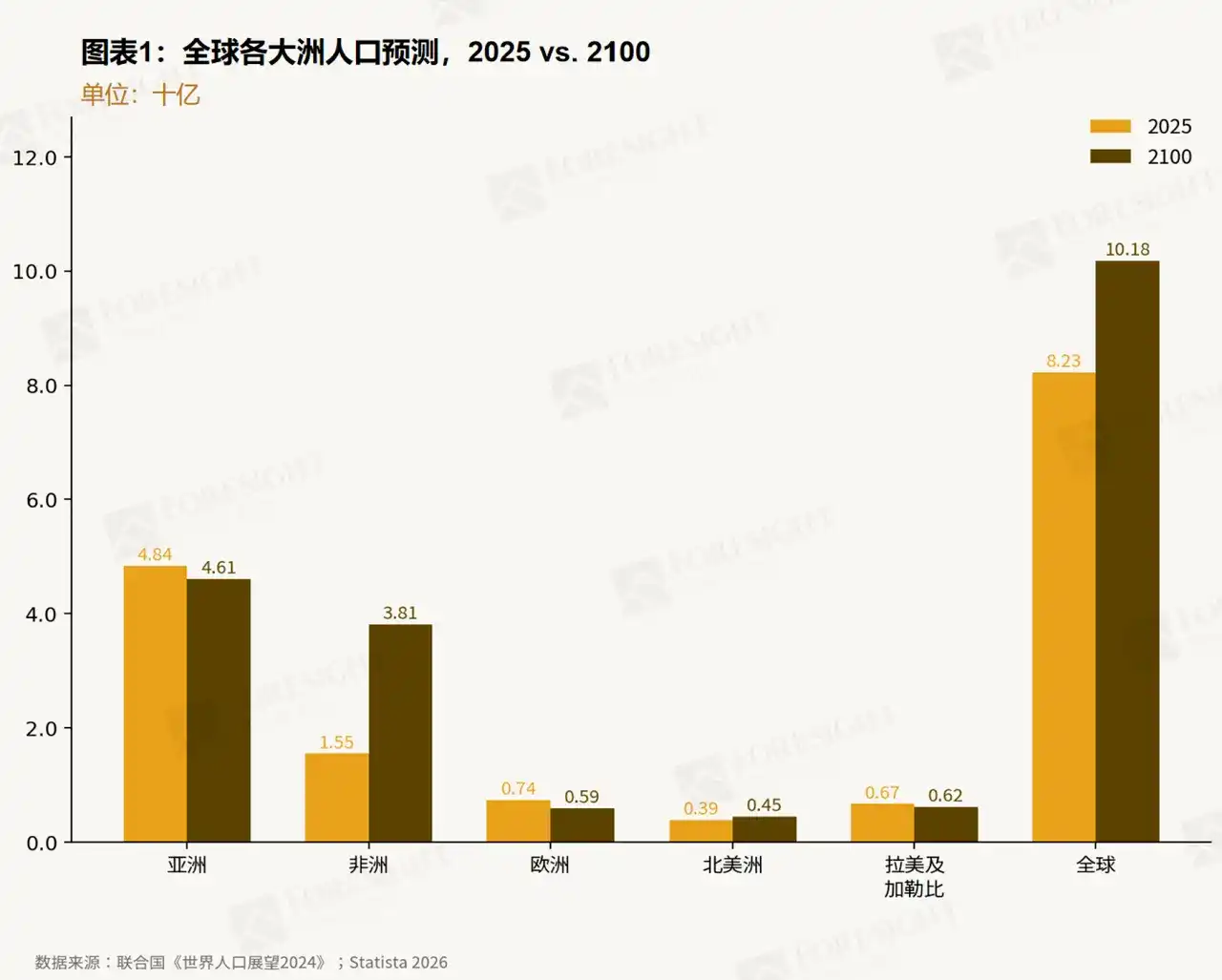

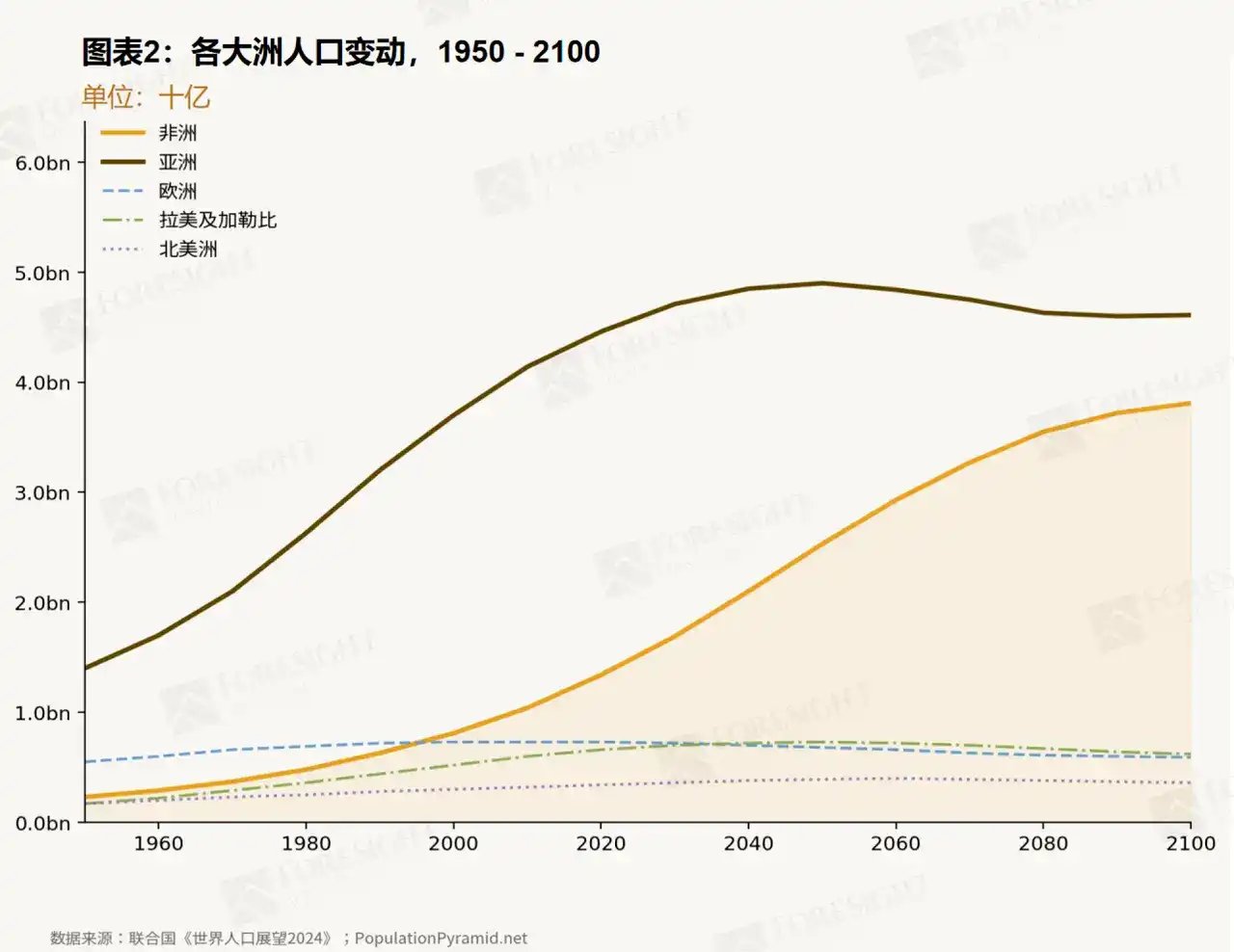

By 2025, Africa's population will reach about 1.55 billion, accounting for approximately 19% of the global total. It is the youngest continent globally, with a median age of just 19, and also the fastest-growing continent, with an annual growth rate of about 2%, unmatched by other continents.

By 2100, Africa's population is projected to nearly triple to 3.81 billion, constituting 37% of humanity by then. In stark contrast, Asia's population is expected to peak and decline by mid-century, Europe and Latin America face absolute contraction, while Africa alone will sustain substantial growth throughout the century (see Figures 1 and 2).

This demographic trend has profound implications for payments infrastructure. Against a backdrop where traditional banking coverage remains low, a large, young, urbanizing, mobile-native cohort is entering the labor market and consumer economy at scale. Consequently, demand for convenient, low-cost financial services (including payments, savings, credit) will only intensify.

1.2 Resource Endowment and Industrial Structure

Africa possesses extremely rich natural resources. According to OPEC's Annual Statistical Bulletin, as of 2024, the continent's proven crude oil reserves were approximately 119.4 billion barrels, accounting for about 7.6% of the global total, with the largest reserves concentrated in Libya, Nigeria, Algeria, and Angola. Beyond hydrocarbons, Africa's mineral resources also hold significant global importance and dominate several categories: the continent is the world's most crucial diamond producer, holds about 49% of global cobalt reserves, and is the absolute source of platinum group metals (PGMs), with South Africa alone controlling about 78% of global PGM reserves. These endowments make Africa a critical node in the global commodity supply chain.

However, much of this wealth is still extracted and exported as raw materials with little downstream processing or value addition. Simultaneously, local manufacturing and agriculture are underdeveloped, infrastructure is severely lacking, and refined fuels, processed foods, etc., remain import-dependent. This economic structure of being 'large at both import and export ends' locks the continent into the trade dependency pattern discussed next.

1.3 Trade Dependency and Remittance Flows

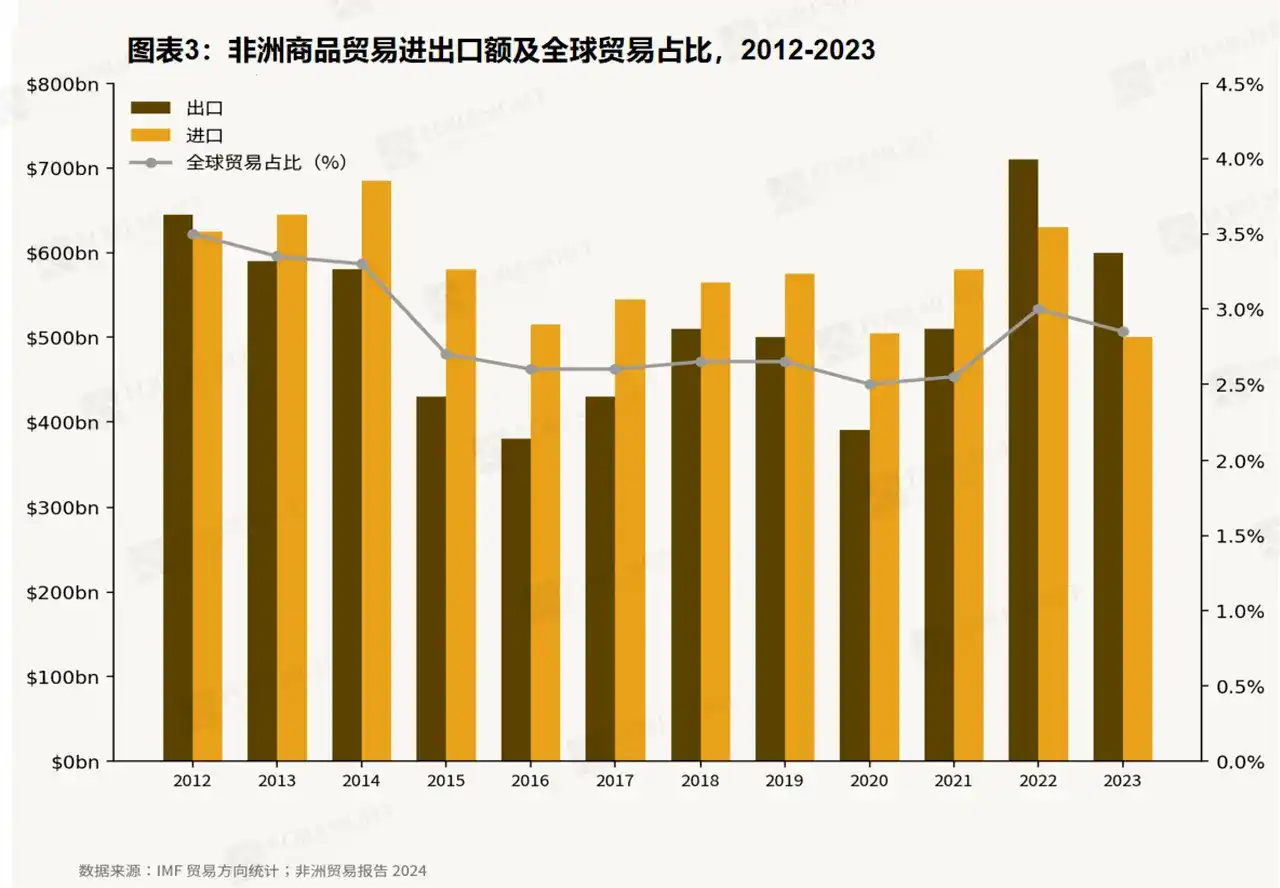

Africa's economy is deeply intertwined with global trade and overseas remittances. In 2023, Africa's cross-border goods exports and imports reached $604.5 billion and $684.5 billion, respectively, while remittance inflows amounted to $52.16 billion. For reference, Africa's total GDP in 2023 was approximately $2.96 trillion. These two pillars of trade and remittances are not only pivotal in Africa's economic structure but also generate massive demand for B2B cross-border trade settlement and C2C cross-border transfers, respectively.

Cross-border trade is a vital pillar of Africa's economy, but the commodity-dependent export structure and persistent trade deficits make it highly sensitive to global macro cycles. In 2023, Africa's total goods exports were $604.5 billion (down 15.1% year-on-year), imports were $684.5 billion (down 1.6% year-on-year), resulting in a trade deficit of about $80 billion (see Figure 3). Over a ten-year trend, Africa is extremely sensitive to fluctuations in the global commodity cycle. The oil price collapse of 2015–2016 pushed Africa's trade volume to a two-decade low, stalling resource-dependent economies (e.g., Nigeria, Angola, oil exporters) while non-resource economies maintained 7%–8% growth, showing a clear divergence. The 2020 COVID-19 shock triggered another collapse: global commodity prices plummeted, African GDP growth fell to -2%, followed by a V-shaped recovery in 2021. More recently, during 2022–2023, driven by a spike in commodity prices triggered by the Russia-Ukraine conflict, African exports briefly surged. However, simultaneously, the aggressive US Federal Reserve rate hikes pushed up the US dollar and tightened global liquidity, subjecting the entire continent to severe imported inflation and currency depreciation.

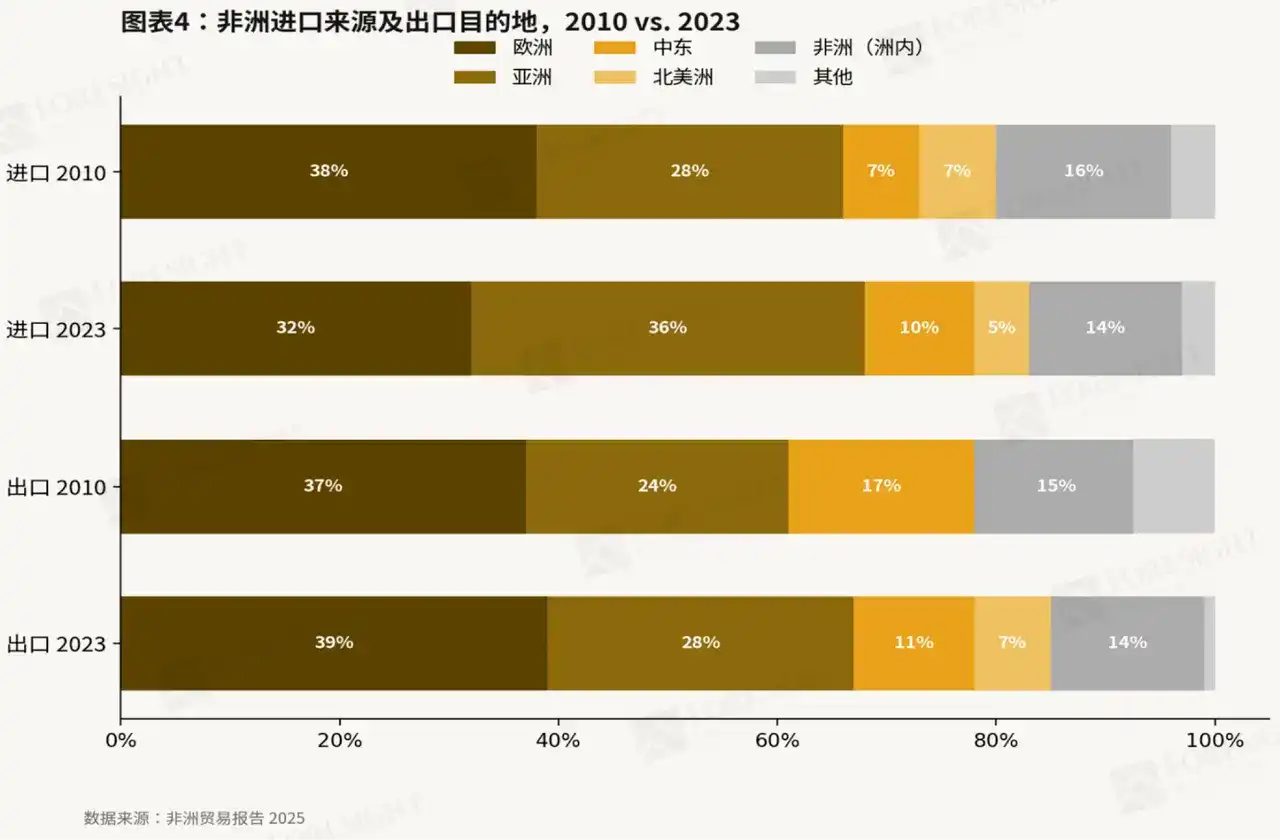

Africa's trade partner structure has changed significantly over the past decade (see Figure 4). Asia, led by China and India, has surpassed Europe to become Africa's largest source of imports—its share of total African imports rose from 28% in 2010 to 36% in 2023, while Europe's share fell from 38% to 32%. On the export side, Europe remains the top destination with a 39% share, but Asia's share has grown from 24% to 28%, and the Middle East has expanded sharply from 3% to 11%. North America's role has contracted on both import and export ends. These changes reflect the deepening commodity trade corridor between China and Africa and the Gulf states' growing importance as energy buyers and investment partners.

Beyond intercontinental trade, 'Intra-Africa Trade' among African countries is also growing rapidly, but barriers like currency and language remain bottlenecks to be overcome. Intra-African trade reached $192.2 billion in 2023, growing 3.8%. However, intra-African trade accounts for only 18% of Africa's total exports, compared to 70% for Europe and 52% for Asia. This reflects persistent obstacles like tariff fragmentation, currency inconvertibility, and weak cross-border infrastructure to intra-African trade growth. Against this backdrop, the African Continental Free Trade Area (AfCFTA) began operations in 2021, aiming to increase intra-African trade by 52% upon full implementation, but progress has been slow.

Remittances are another lifeline for Africa's economy and a source of massive C2C payment demand. According to World Bank data, Africa received $52.2 billion in remittances in 2023. The top five remittance corridors are Saudi Arabia→Egypt, UAE→Egypt, US→Nigeria, Kuwait→Egypt, France→Morocco. African labor exports to the Gulf, North America, and Europe form continuous reverse income flows to households. These corridors constitute one of the largest sources of cross-border C2C transfer demand and are also where the pain points of the traditional financial system in cross-border transfers—high costs, long time, and opacity—are most acutely felt, a key issue discussed in the next section.

2 The Deep Mismatch Between Foreign Trade/Remittance Demand and the Backward Financial System

2.1 Low Banking Coverage, Huge Unbanked Population Gap

Africa's formal financial system only covers a minority. According to the World Bank's 2021–2022 global Findex database, only 49% of adults in Sub-Saharan Africa had a financial account; by 2024, this figure rose to 58% but remained among the lowest globally. Beyond low coverage, African banking outlet density is also lagging. IMF's Financial Access Survey shows Kenya has only 4.4 bank branches per 100,000 adults, Morocco 22.2, and even South Africa, with Africa's most developed banking system, has just 38.7, all far below global averages. The result is a massive unmet demand for basic financial services: payments, savings, credit, insurance.

2.2 International De-risking and Correspondent Banking Retreat

Africa's second major hurdle comes from the retreat of the international financial system itself. Driven by concerns over anti-money laundering (AML) and customer due diligence (KYC) compliance risks, compounded by local realities like lack of formal ID, no fixed address, incomplete tax records, and a high cash economy share, major global banks have engaged in a de-risking wave. Since 2016, correspondent banking relationships have shrunk dramatically. According to SWIFT data, South Africa lost over 10% of its overseas correspondents, while Angola's decline reached 37%. This retreat directly raises the cost of legitimate cross-border transactions and marginalizes smaller African financial institutions from the global system.

2.3 Poor Foreign Exchange Management and Chronic Inflation

Currency system fragility further amplifies these structural defects. Due to fiscal deficits and a weak tax base, many African central banks resort to printing money to finance government spending, causing persistent imported inflation. Prices for food, fuel, and raw materials for manufactured goods surge as the local currency depreciates. Simultaneously, shallow capital markets, highly concentrated banking systems, and a historical deficit in central bank independence lead to ineffective monetary policy transmission, making interest rate hikes ineffective at curbing inflation or stabilizing exchange rates. In 2024, Africa's overall inflation rate hit 20.1%, the highest among major global regions, severely eroding the real value of local currency savings.

2.4 Consequence: Cash Dominance and Payments System Dysfunction

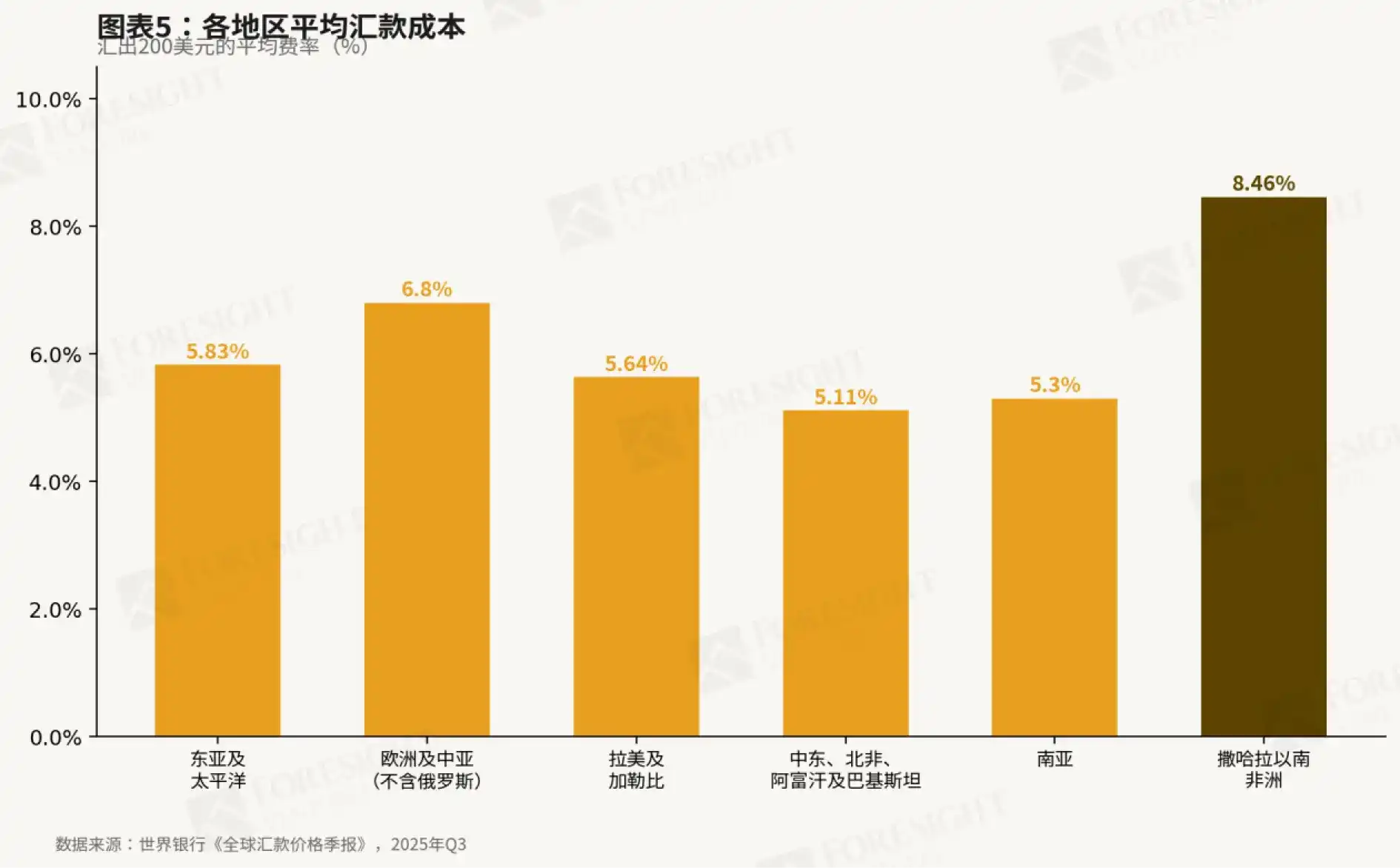

The triple dysfunction of bank exclusion, de-risking, and monetary instability has obvious consequences. Most Africans still rely on cash for daily transactions; remittance costs in Sub-Saharan Africa are the world's highest, averaging 8.46% per transfer according to the World Bank's Q3 2025 Remittance Price Report; ordinary people also lack effective inflation-hedging stores of value. The banking system fails comprehensively in access convenience, affordability, and currency stability, creating a market vacuum rapidly filled by emerging payment channels and cryptocurrencies.

3 Mobile Payments and Cryptocurrencies Thrive in the Vacuum Left by the Traditional Financial System

In the gap left by the absent banking system and under pressure from severe inflation and currency depreciation, Africa has developed the world's most dynamic mobile money and cryptocurrency markets. The emergence of these alternative payment channels is not a matter of choice but of necessity—they solve real problems the banking system cannot address: accessibility, affordability, and stability.

3.1 Mobile Payments: Africa Leads Globally

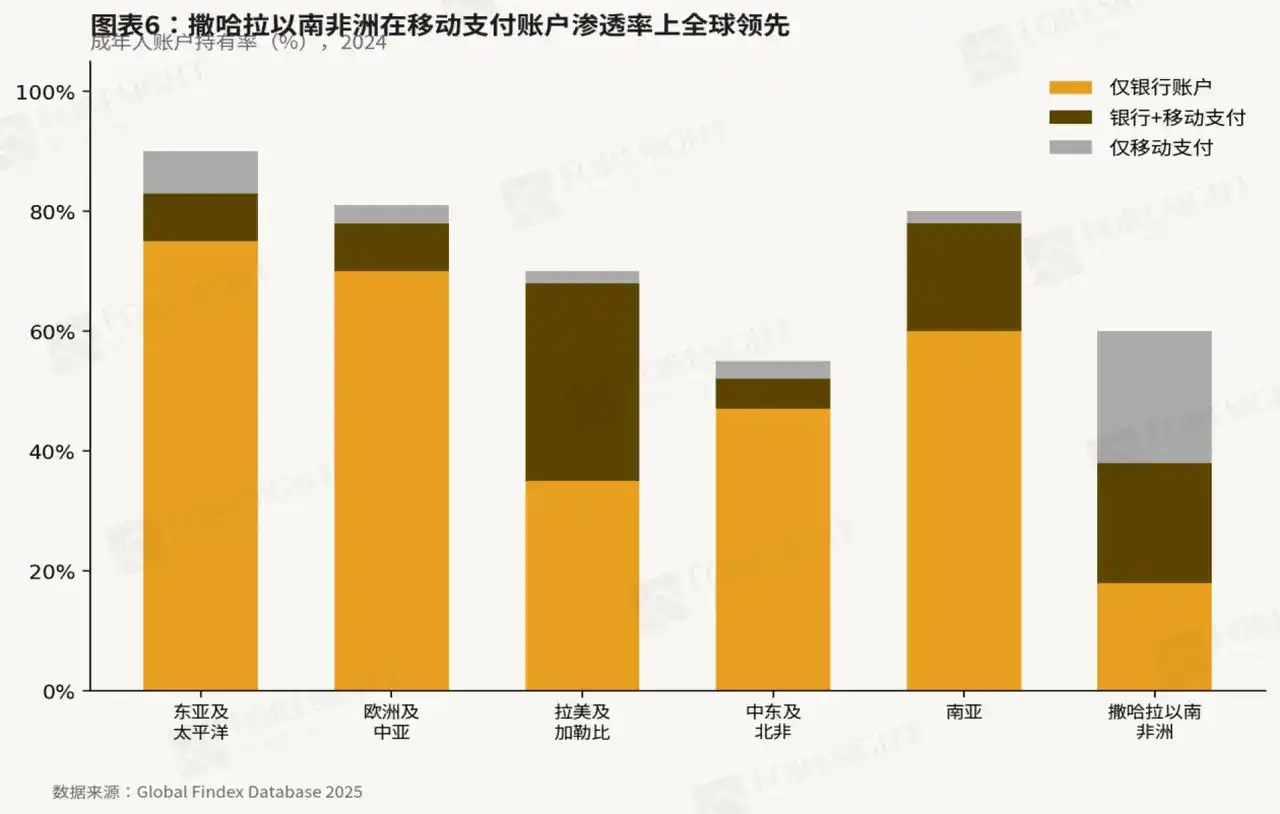

Africa accounts for most global mobile money transactions. According to the 2025 global Findex database, about 40% of adults in Sub-Saharan Africa use a mobile money account as their primary (or only) formal financial service. Kenya's M-Pesa platform exemplifies this model: relying on ubiquitous USSD technology (accessible via basic feature phone keypads), it built a network of millions of offline agent outlets and leveraged universal mobile coverage to capture 90.8% of Kenya's mobile payments market, successfully expanding to seven other African countries like Tanzania, Ghana, and Egypt. This offline agent-based, low-tech barrier architecture has proven far more scalable and inclusive than branch-based traditional banking, amassing a vast user base across urban and rural Africa.

3.2 Widespread Cryptocurrency Adoption Across the African Continent

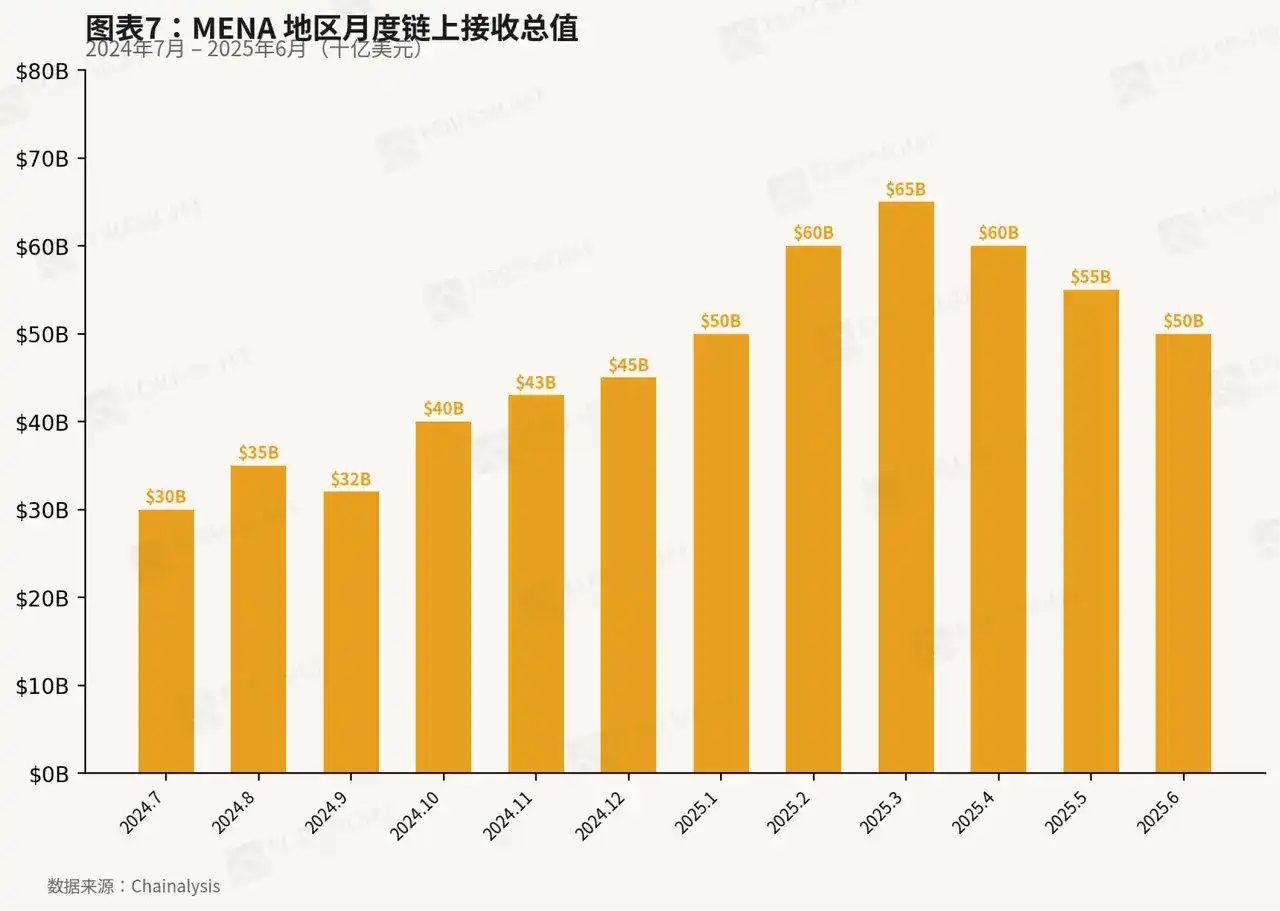

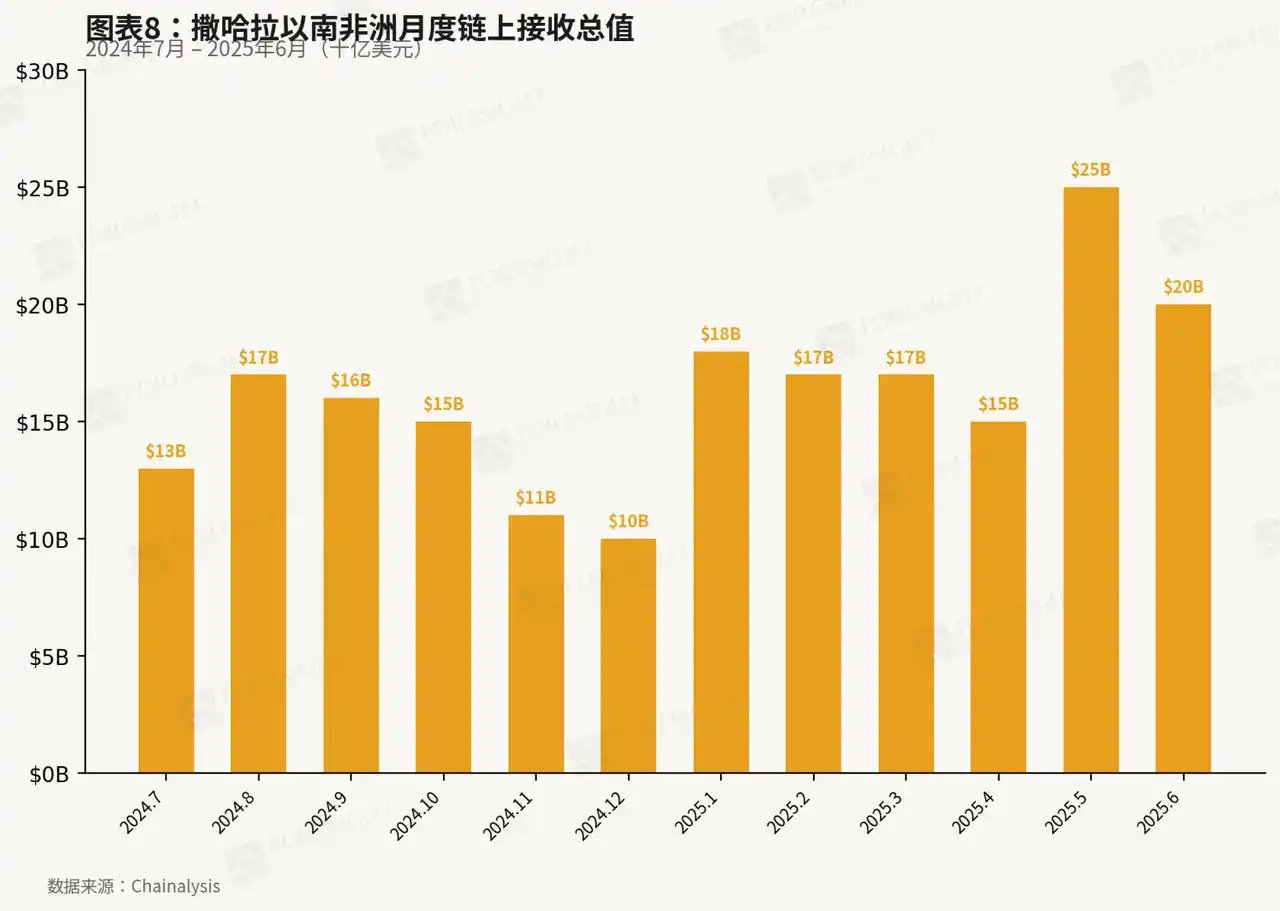

Cryptocurrency adoption rates on the African continent are among the world's highest and still rising sharply. In the Middle East and North Africa, total on-chain value received between July 2024 and June 2025 was approximately $600 billion; Sub-Saharan Africa recorded $200 billion in the same period, with a high growth rate of 52%, driven primarily by retail users and concentrated in a few countries (Nigeria, South Africa, Ethiopia, Kenya). Cryptocurrencies effectively meet African businesses' and individuals' needs for an inflation-hedging store of value and low-cost cross-border settlement—needs that mobile money and formal banking systems cannot fully satisfy.

4 Heterogeneity Within the African Continent

4.1 Why Understanding Internal Divergence in Africa Is Crucial

Africa's 54 countries span 42 different currency systems and belong to multiple linguistic spheres: Francophone, Anglophone, Arabophone, Lusophone, and Hispanophone. This fragmentation in language and currency is not merely a cultural difference but profoundly impacts cross-border trade, financial flows, and regulatory systems: payment networks are disjointed, regulatory frameworks are separate, and market opportunities are highly fragmented. Therefore, after establishing a holistic understanding of Africa's macroeconomic environment, it's essential to recognize internal regional differences in culture, regulation, and financial systems.

4.2 Divided by the Sahara: Middle East & North Africa (MENA) vs. Sub-Saharan Africa (SSA)

The most common analytical framework currently divides Africa into two systems along the Sahara Desert: the Middle East and North Africa (MENA) and Sub-Saharan Africa (SSA).

North Africa is highly integrated with the Arab world culturally, institutionally, and economically, with its economy centered on oil and gas resources and deeply embedded in the global energy market. Accordingly, its financial system and policy frameworks operate more within the MENA ecosystem, with a relatively mature banking system and lower levels of financial exclusion.

In contrast, Sub-Saharan Africa largely falls outside this system. The market driving the explosive growth of crypto and mobile payments is precisely this region, long plagued by deep-seated financial system inadequacy, dollar shortages, and currency instability. SSA currently accounts for nearly 60% of global mobile payment transaction volume and is also the world's fastest-growing region for cryptocurrency adoption.

4.3 Five-Region Framework: Differentiation in Population, Economy, and Fintech Ecosystems

Further subdivision yields five African regions with significantly different macroeconomic characteristics. North Africa and Southern Africa have the highest GDP per capita; West and Central Africa are relatively less developed; East Africa has the lowest per capita income. However, economic growth rates show an inverse relationship with wealth levels: East Africa grows fastest, followed by Central Africa, North Africa, West Africa, and Southern Africa.

Cryptocurrency adoption patterns show similar features. Nigeria alone (in West Africa) accounts for most crypto transaction volume in SSA; meanwhile, East Africa, South Africa, and North Africa also show high adoption. Central and broader West Africa remain in earlier market stages. This differentiation essentially reflects variations in financial exclusion, dollar shortage pressure, and regulatory environments across regions.

5 The "Dollarization" and "Dollar Shortage" Behind Sub-Saharan Africa's Payments Market

5.1 Dollarization in Sub-Saharan Africa

Sub-Saharan African economies exhibit deep dollarization, far exceeding most other global regions. Dollar deposit and loan shares are key proxy indicators: in Nigeria, dollar deposits once constituted 40% of total deposits, and over 80% of external debt is dollar-denominated; in Ghana, dollar deposit shares have reached relatively high levels of 20%–30%. This dollarization is not accidental but a manifestation of rational economic behavior in the face of long-term currency instability.

5.2 Three Structural Drivers of Dollarization

Dollarization in Sub-Saharan Africa stems from three distinct economic pressures.

First, Store of Value: Due to fiscal deficits and external imbalances forcing central banks to print money, local currencies persistently depreciate, while the US dollar offers a stable unit of account.

Second, Medium of Exchange: Commodity prices (oil, minerals, food) are globally priced in US dollars, and even intra-African trade between two African countries is often settled in dollars—because the dollar is more stable than any single local currency.

Third, Financing Channel: Shallow local capital markets mean businesses and governments must borrow dollars from international creditors; when dollar debt becomes too large relative to dollar income, exchange rate risk becomes acute, driving more funds into dollar deposits.

5.3 Causes of the "Dollar Shortage"

The real pain point in Sub-Saharan Africa's current payments market is the dollar shortage. Limited foreign exchange earning capacity (commodity dependence, weak manufacturing exports), coupled with huge trade deficits and debt service pressures, continuously deplete government forex reserves. Consequently, central banks can only ration official forex through administrative controls. This scarcity fosters a parallel black market where dollars trade at significant premiums—sometimes 50% to 100% above official rates. Residents and businesses unable to obtain forex through official channels turn to informal channels: global remittance companies like Western Union, informal exchange houses, and increasingly, stablecoins and cryptocurrencies. The gap between official and parallel market exchange rates is precisely the crack alternative payment systems exploit.

5.4 Why Cryptocurrencies Thrive in This Vacuum

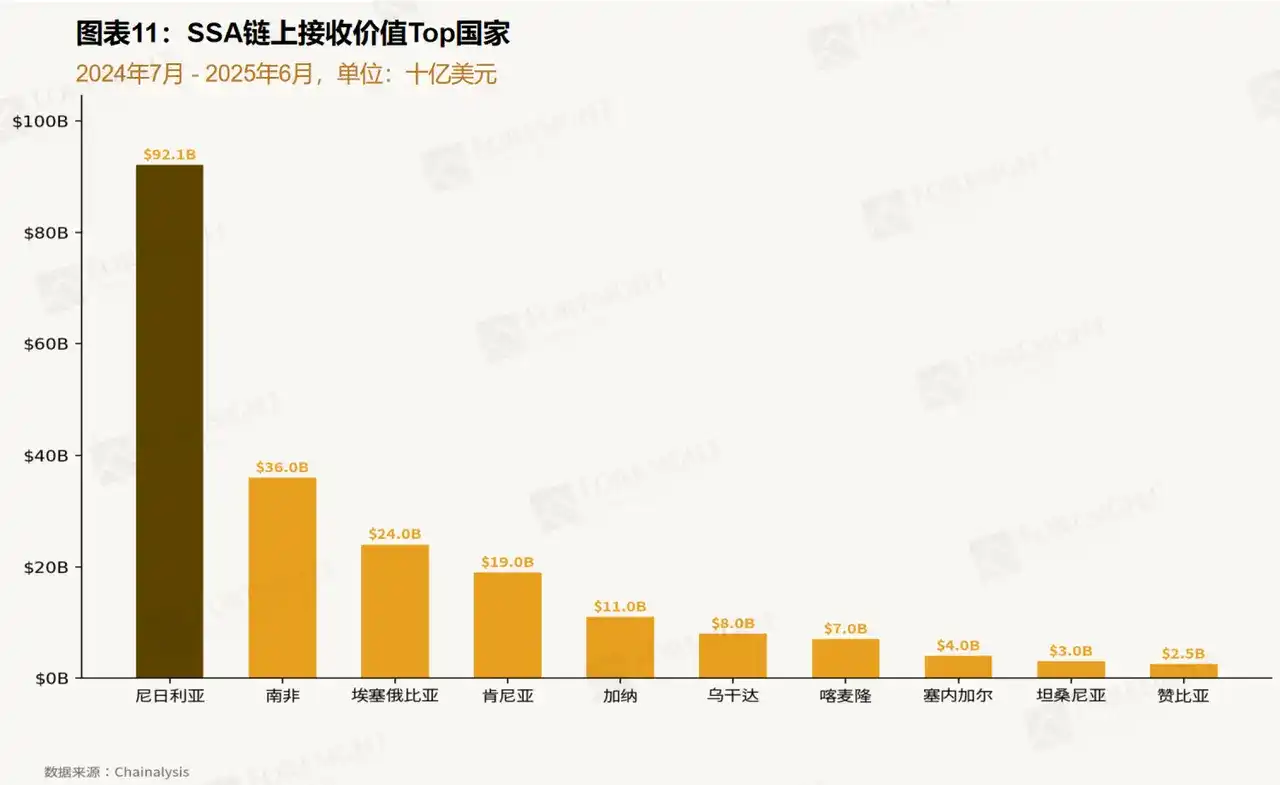

Stablecoins and other cryptocurrencies perform three critical functions missing from the formal banking system. They bypass capital controls, providing access to parallel market dollars; they execute cross-border transactions at lower costs than banks and remittance corridors; they also offer a globally liquid store of value unaffected by local currency risk. Therefore, Sub-Saharan Africa's crypto adoption is overwhelmingly retail-driven with small transaction amounts. As Figure 11 shows, compared to other global regions, Sub-Saharan Africa has a higher share of transfers in the $1,000–$10,000 range, reflecting flows for small remittances, informal business trade settlement, and personal savings. Nigeria dominates the region, accounting for about 45% of Sub-Saharan Africa's on-chain transaction volume (as shown in Figure 12), but Kenya, South Africa, and Ethiopia are also important regional hubs.

5.5 De-dollarization Attempts and Their Structural Limitations

African policymakers and regional institutions have attempted to reduce dollar dependence. The Pan-African Payment and Settlement System (PAPSS) aims to settle intra-African trade in local currencies and reduce forex costs; the planned 'Eco' currency zone in West Africa seeks stability through monetary union; central banks have also employed aggressive interest rate hikes and capital controls. However, all these efforts face a fundamental constraint: Sub-Saharan Africa's structural trade dependency. As long as the continent's imports exceed exports, external accounts remain in deficit, and most forex income comes from commodities, dollar demand will persistently outstrip supply. De-dollarization requires industrialization and trade rebalancing, a decades-long transformation not achievable by policy alone. In the interim, mobile money and cryptocurrencies will continue playing crucial roles, filling the gaps left by the traditional financial system.

Conclusion

Africa's outstanding performance in mobile money and cryptocurrency adoption is not a market coincidence but a macroeconomic necessity.

The continent's young demographic, rich natural resources, and deep integration into global commodity markets generate massive cross-border payment flows. However, its weak financial system, chronic monetary instability, and severe dollar shortages make the formal banking system fundamentally incapable of meeting this demand.

Mobile money solves domestic payments; cryptocurrencies are solving cross-border value transfer and inflation hedging. These are not niche use cases or speculative holdings but critical financial infrastructure filling the vacuum left by structural economic constraints. Crucially, these constraints are not cyclical; they are rooted in Africa's resource dependency, limited industrialization, and underdeveloped financial markets.

De-dollarization requires trade rebalancing and industrialization, both multi-decade transformations. Before that, and likely long after, alternative payment channels and currencies will remain central to Africa's economy.

Original article link