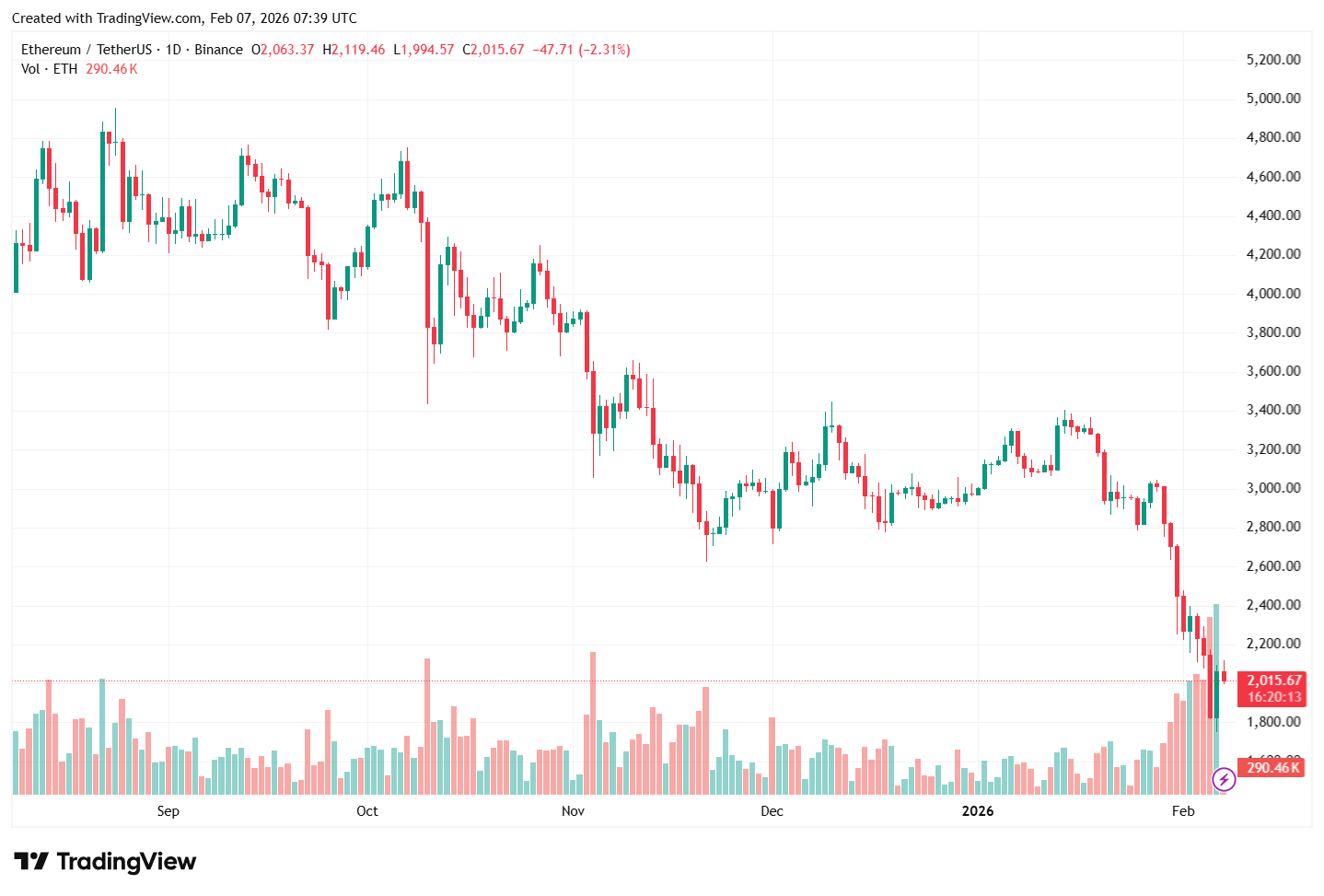

In line with its bearish market structure, the Ethereum price struggled significantly in the first week of February. The cryptocurrency’s value fell by more than 30% over the week, crashing to as low as $1,850 on Friday, February 6. Amid the Ethereum market downturn, a significant development has emerged — one which could make or mar the world’s second-largest cryptocurrency.

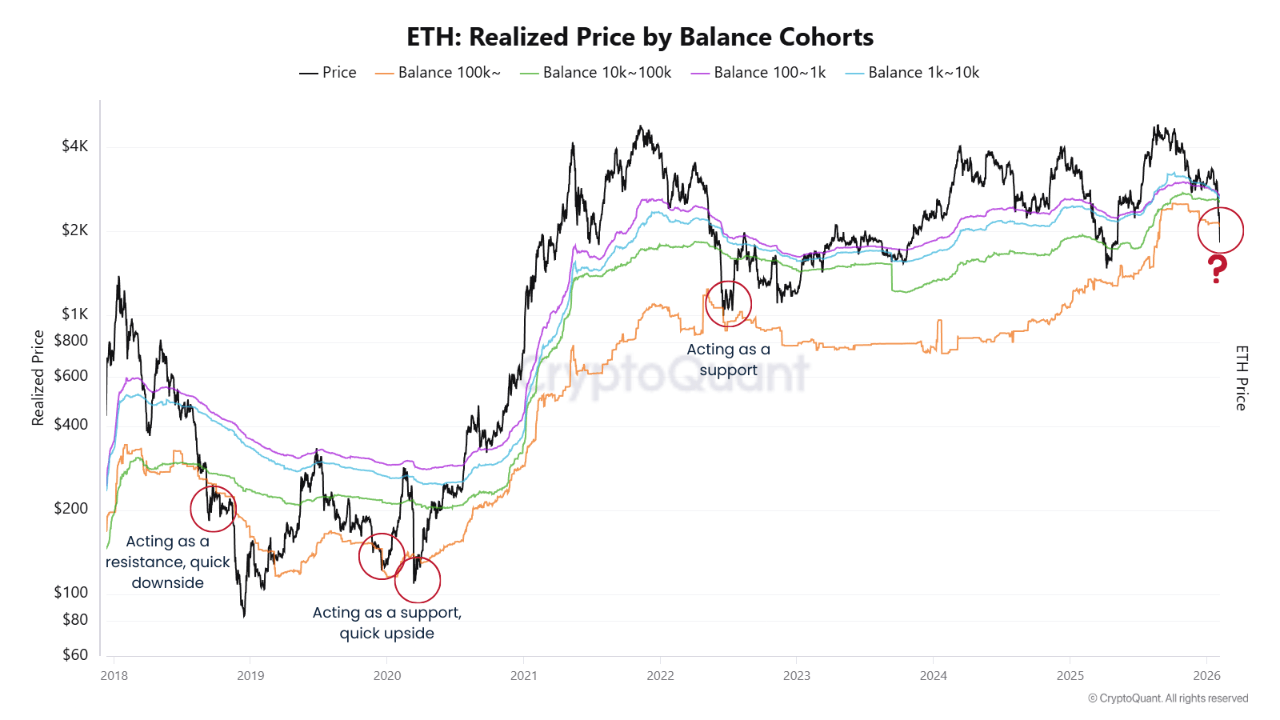

Ethereum Breaches Realized Price Across All Investor Cohorts

In a recent post on Quicktake, on-chain analyst MorenoDV shared a shocking development within the Ethereum network. The analyst highlighted that the Ethereum price recently slipped below the cost basis of multiple investor groups.

The revelation is based on the Realized Price by Balance Cohorts metric, which monitors the average on-chain cost basis of Ethereum holders. The metric groups these investors by wallet size, showing where these cohorts are holding profitably or running at losses.

In the chart above, we see the Ethereum price break beneath multiple cost bases (represented with yellow, green, blue, and purple lines). The most striking, however, is the loss of the realized price of the largest holders (with 100k ETH and above stored), which stands at around $2,074.

Historically, the realized price of this investor class (with more than 100k ETH in holdings) has taken on dual roles for the Ethereum price, depending on its trajectory. According to data from 2019, mid-2020, and late 2022 price actions, whale realized price typically takes on a role of formidably resisting price during downtrends; during uptrends, it interestingly acts as reliable support.

Hence, at periods where the Ethereum price stabs through the whale realized price to the downside, MorenoDV explained that two potential paths typically emerge. In his words: “either a violent snap-back rally as the level flips to support (2020, 2022), or further capitulation into multi-year lows (2018-2019).”

Major ETH Price Levels To Watch

Because the Ethereum price went through all investor cohorts’ realized prices at the same time, there is something worth noting here. MorenoDV pointed out that smaller holders collectively have their realized prices between the $2,534 – $2,675 range.

Thus, should the Ethereum price attempt to recover previous legs, the $2,534–$2,675 price range will pose significant resistance to that effort. However, the aforementioned range is not the most critical one for the Ethereum price.

The analyst highlighted the whale cohort’s realized price, which is approximately $2,074 — to be the most critical for the Ethereum price. Following previous extrapolations, a reclamation of this level would likely follow historical trends and push prices upwards, while failure to retake this level within a period of 30 – 45 days would precede significant drawdowns.

In the event that the latter scenario holds true, the Ethereum price could swiftly fall to $1,800, or even lower. If price breaks beneath $1,800 and is sustained below this level, MorenoDV hypothesizes that this could lead Ethereum to the $1,600–$1,300 levels.

As of this writing, Ethereum stands at a valuation of $2,030, reflecting an over 7% jump in the past 24 hours.

The price of ETH on the daily timeframe | Source: ETHUSDT chart on TradingView