Amundi, Europe’s largest asset manager, is launching the Spiko Amundi Overnight Swap Fund (SAFO), a tokenized fund on Ethereum and Stellar starting with about $100 million in committed assets.

A Traditional Fund With A Tokenized Wrapper

Institutions historically related to TradFi have found a way to not to be left behind on the crypto curve in tokenized assets. In a statement published on Amundi’s website, the investment fund announced its collaboration with Spiko, a French-law regulated specialist tokenization platform, to launch SAFO as a tokenized sub-fund of SPIKO SICAV.

LIVE: Europe’s largest asset manager Amundi (€2.3 trillion AUM) & Spiko launch new tokenized mutual fund (SAFO) powered by Chainlink.

Chainlink is how the world’s leading institutions & tokenization platforms are unlocking the issuance & distribution of tokenized funds. pic.twitter.com/2GQshwqCrC

— Chainlink (@chainlink) March 19, 2026

Structurally, SAFO it’s a traditional fund, just with a tokenized wrapper: it’s designed for corporate treasury and collateral management, an “on‐chain cash parking” with low risk and overnight liquidity. The fund invests using fully collateralized total return swaps with top‐tier banks, aiming to deliver stable yields slightly above risk‐free rates while still letting investors get their money back on an overnight basis. It supports multiple currencies (EUR, USD, GBP, CHF) and can be subscribed from as little as 1 unit, which is unusually low for institutional‐grade cash products.

The firm highlighted that the fund enables almost immediate settlement, supports multiple ways to hold assets, provides live visibility into the shareholder register, and allows fund shares to move globally around the clock, with automated access through APIs or smart contracts.

In the statement, Jean-Jacques Barbéris, Head of Institutional and Corporate Clients, and ESG at Amundi, said:

SAFO provides professional investors with a fast and transparent access to cash management solutions. This initiative is part of our ambition to contribute to the rise of tokenized solutions.

Where Ethereum Comes In

The shareholder register and fund shares live on Ethereum and Stellar, with Ethereum chosen for its smart‐contract and DeFi composability, while Stellar supports faster, lower‐cost transfers and 24/7 transferability of fund units. Chainlink’s network of data providers puts SAFO’s fund value directly on the blockchain and acts as the connector between Ethereum, Stellar, and traditional systems. This gives tokenized funds a secure, standardized way to share information, building on tests Chainlink has already run with DTCC and other major institutions.

SAFO is Amundi’s second tokenized fund in a few months. Back in November, the fund rolled out a tokenized share class of a money market fund on Ethereum, working together with CACEIS, one of Europe’s top asset-servicing providers and transfer agents, as reported by Bitcoinist.

Amundi’s new venture adds to a growing universe of tokenized money‐market products from players like BlackRock, the world’s largest asset manager, and Franklin Templeton, and reinforcing Ethereum’s position as the primary settlement layer for institutional RWAs.

A €2.3 trillion incumbent plugging into Ethereum and Chainlink cements the thesis that the next leg of the crypto cycle is driven by tokenized cash, bonds, and funds rather than purely speculative DeFi.

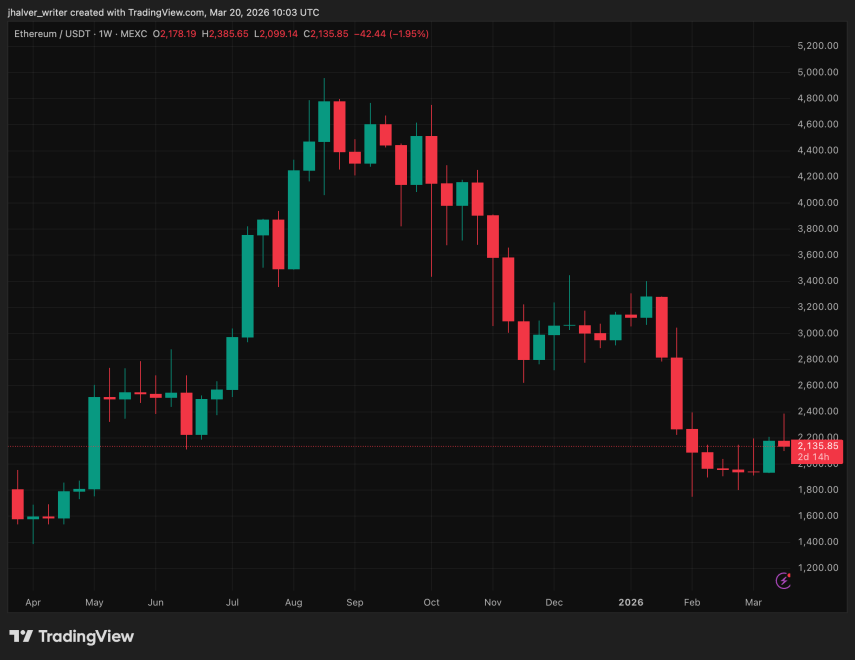

ETH trades for $2k on the daily chart. Source: ETHUSDT on Tradingview

Cover image from Perplexity, ETHUSDT chart from Tradingview