The altcoin market could be in for yet another decline in price action.

Alameda Research, the now-defunct trading firm linked to the collapse of FTX, is making moves for the second time in less than a month. The firm recently hinted at a possible sell-off in Ethereum [ETH] and Solana [SOL]. Historically, its distribution events have resulted in massive sell-offs in associated assets, but will that happen again this time?

Examining Alameda Research’s selling pattern

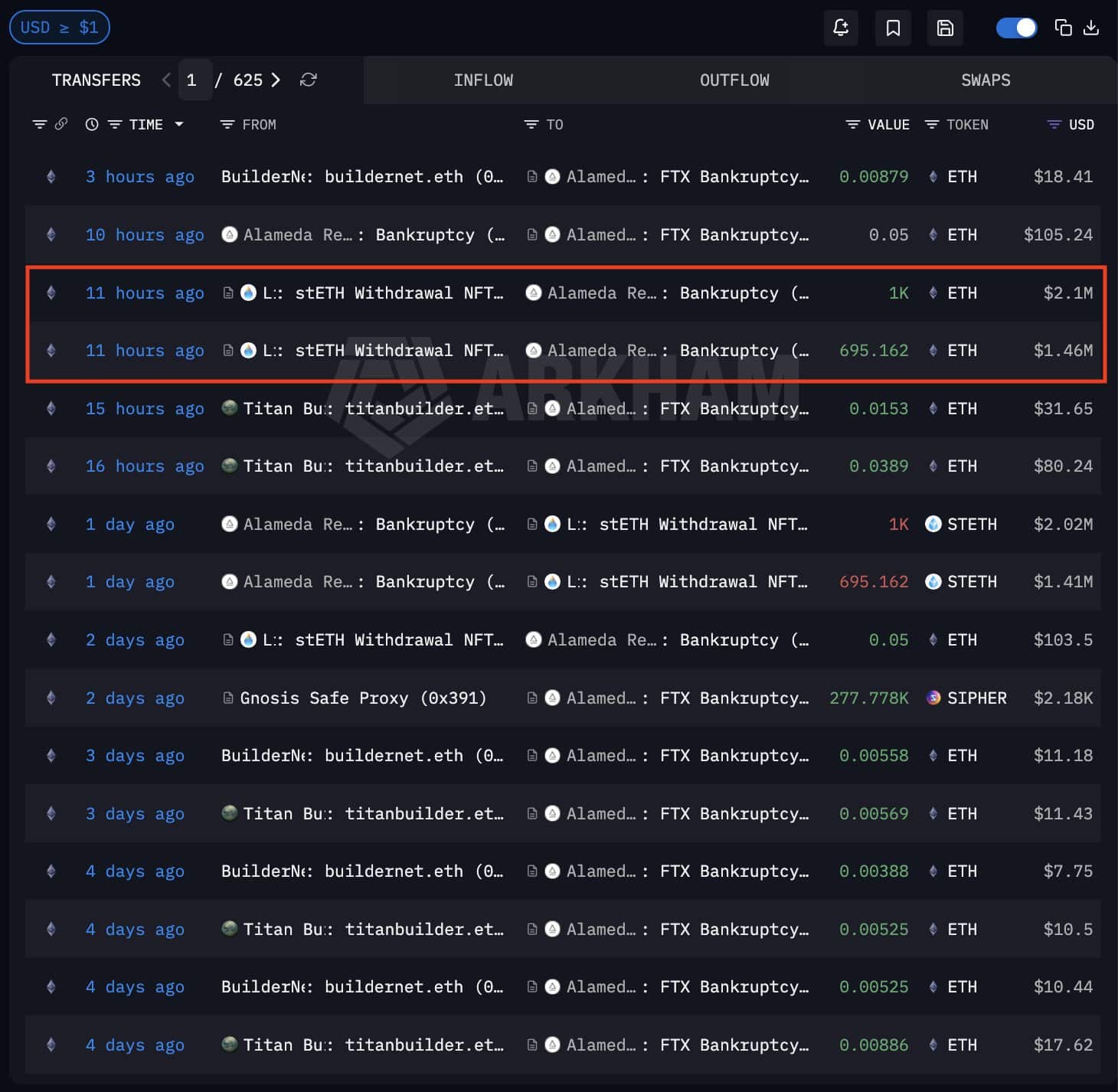

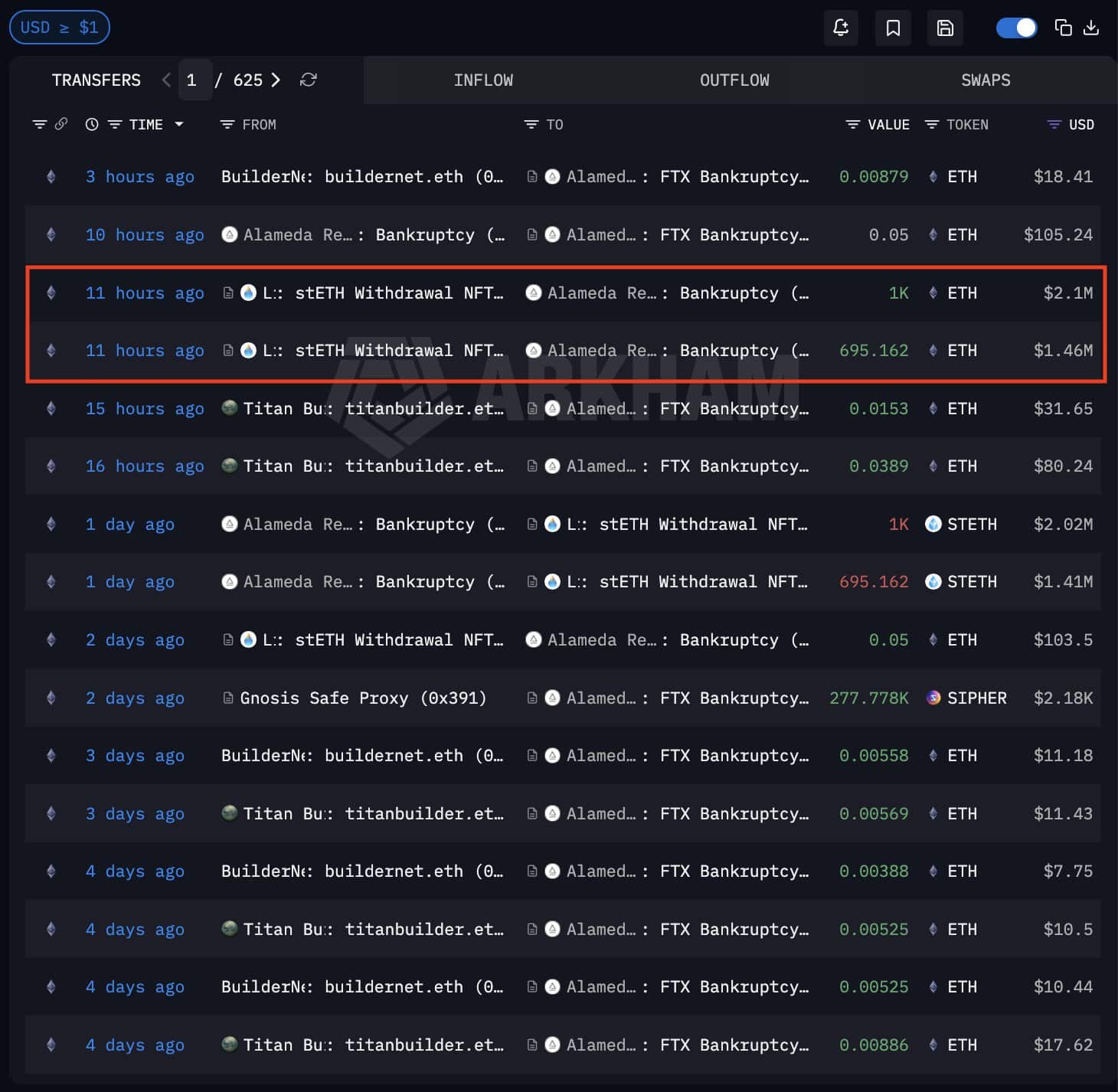

According to Arkham data, Alameda unstaked more than 1,695 ETH, worth more than $3.56 million. This move seems to be following a familiar pattern. That is, three weeks ago, they sold more than $17 million of SOL tokens.

The firm still holds about $300 million worth of SOL, $35 million worth of Bitcoin, and $20 million worth of USDT. Therefore, there may be impending selling pressure on ETH and SOL as a result of the firm’s liquidation events.

In addition to Alameda Research’s selling, other institutions are also shorting the largest altcoin. For instance, a trader linked to Fasanara Capital sold $45 million worth of ETH. Moreover, selling pressure rises amid long liquidations, particularly on big-cap altcoins.

How are ETH and SOL prices positioning?

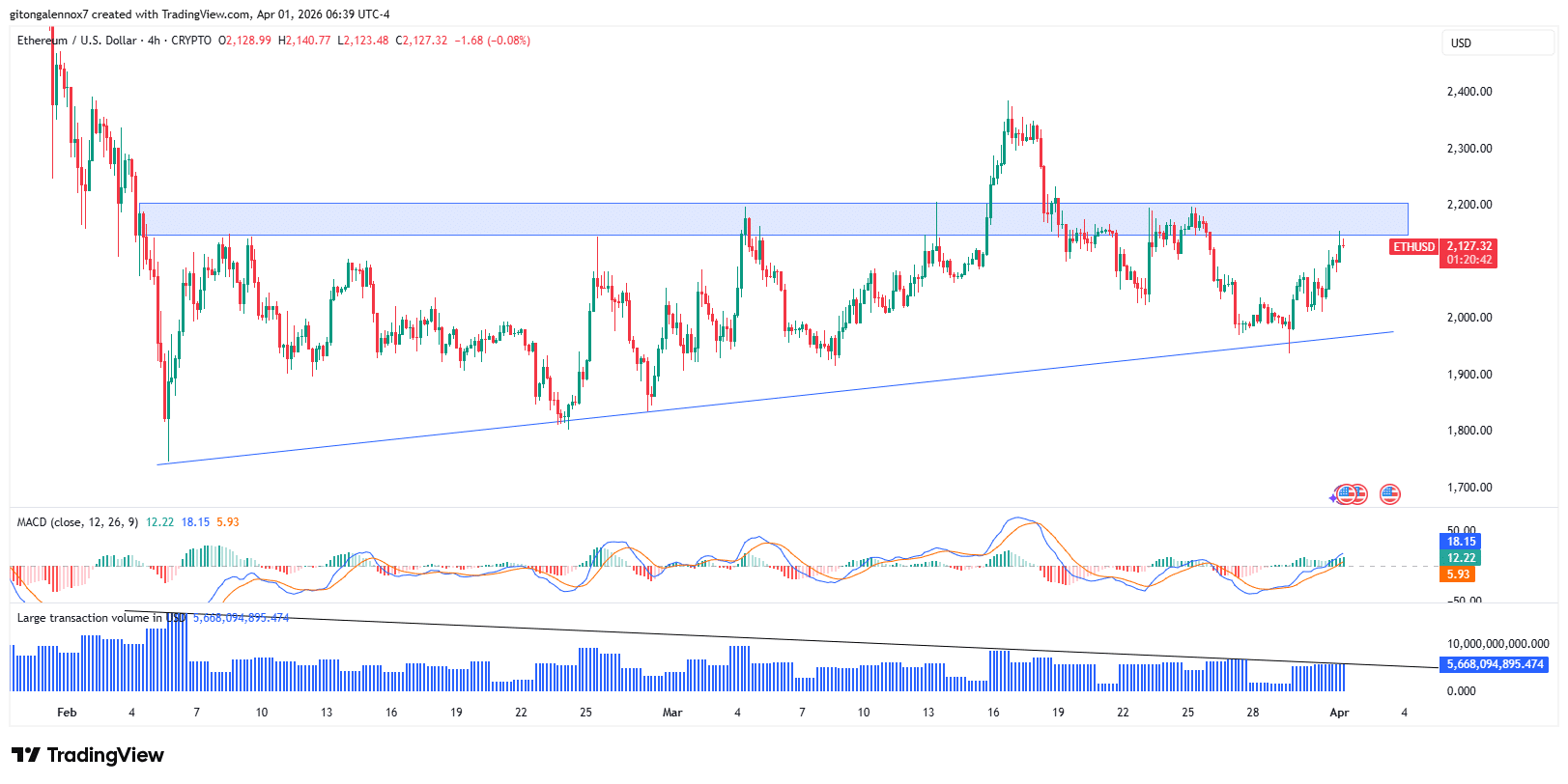

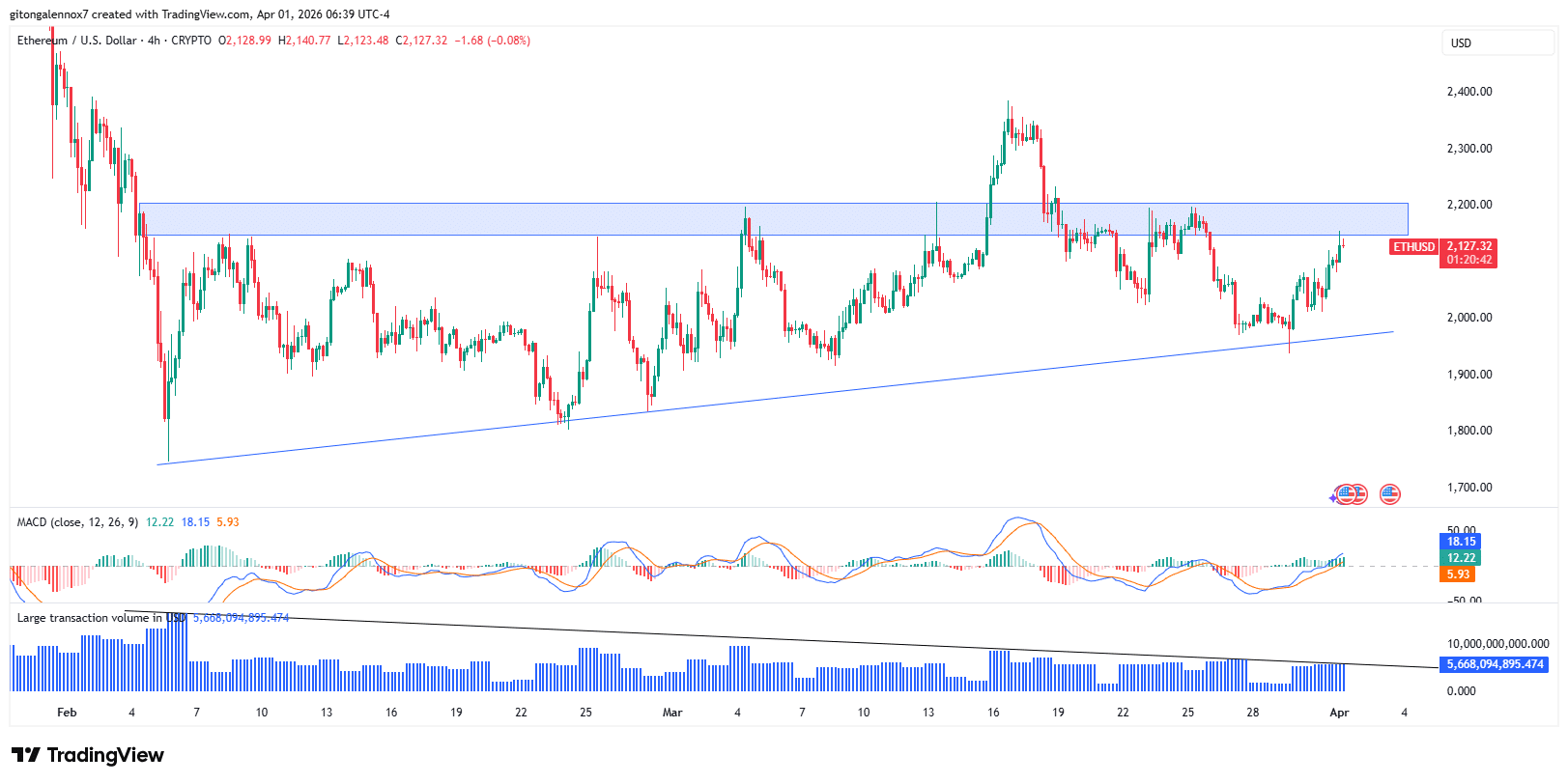

Ethereum price was showing strength at the moment. On the 4-hour chart, the altcoin was trading around a resistance zone that had held price since February.

While the MACD was bullish at press time, the amount of large transaction volume was declining. The Large Transaction Volume declined by 3x, from $17.5 billion to $5.67 billion.

This showed buying was weak at a price zone that has led to bearish reversals previously.

However, a break above would invalidate the signals sent by Alameda Research’s move, at least for now.

Meanwhile, Solana price action was trading in a sideways market, having lost much of its correlation with ETH. The correlation coefficient has dropped from 1 to 0.59.

The altcoin may drop to the support at $76 after trading near the range’s lows. This is due to a decrease in network activity as well; in just two months, the number of active addresses dropped from 7 million to 4.69 million.

The signals above suggested that, should history repeat itself, Ethereum and Solana might experience a short-term decline. However, if SOL maintains its support and ETH surpasses $2,100, it could invalidate the anticipated price decline.

Final Summary

- Alameda Research and Fasanara Capital are betting on Ethereum and Solana prices dropping in the short term.

- Ethereum showed strength but traded below a resistance, while Solana was struggling at the lower band of a price range.