Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

No confidentiality request! No complete liquidation! The newly crowned "AI Stock God," Leopold Aschenbrenner, and his fund Situational Awareness LP officially released their 13F filing this evening.

- Odaily Note: For details on Leopold Aschenbrenner's personal story, please refer to "SBF's Junior, Turned $225 Million into $5.5 Billion in One Year."

This means our first hypothesis from this morning's article, "Could Be Revealed Today, the Internet is Awaiting the Version Answer from the 24-Year-Old 'AI Stock God'," is confirmed. Situational Awareness LP submitted its filing quite late on the May 15th deadline, preventing the SEC from publishing it on its website that day. As a result, the market had to endure another weekend, finally seeing the fund's holdings disclosure after the SEC resumed work on Monday.

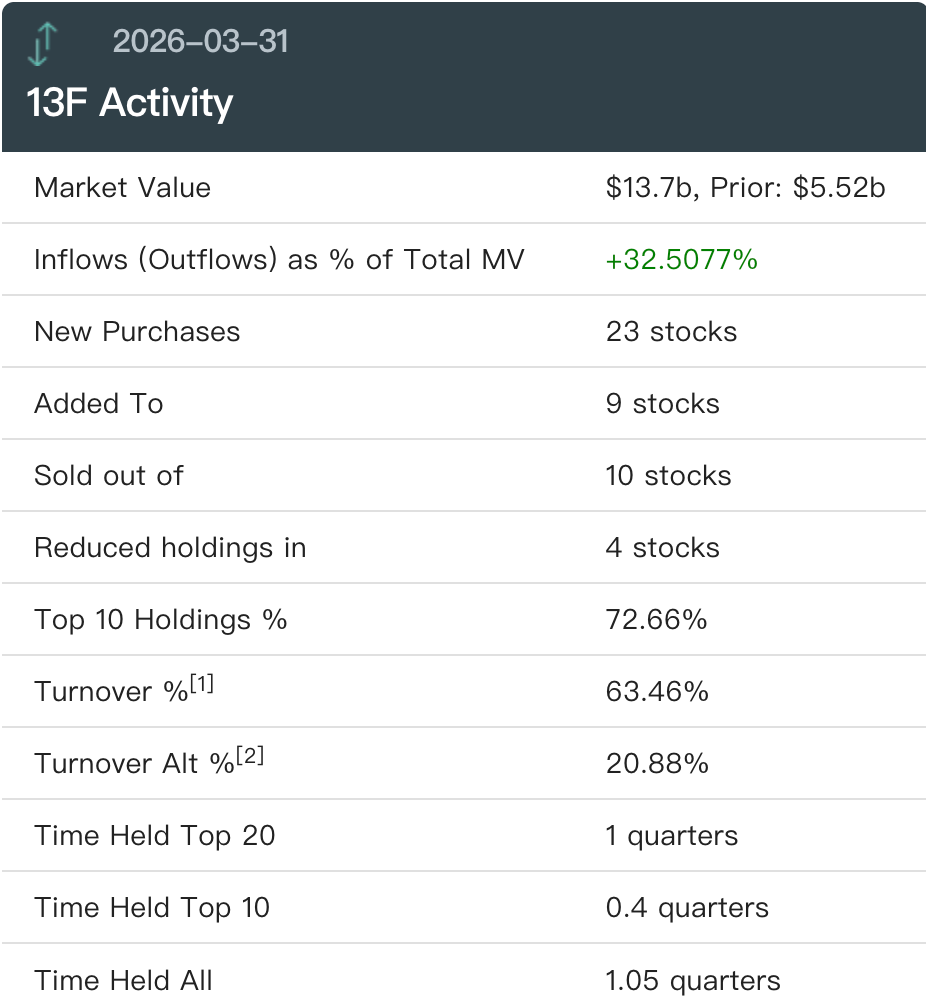

According to this latest 13F filing, as of March 31, 2026, the nominal total value of Situational Awareness LP's holdings has increased to $13.7 billion, more than doubling (up 148%) from $5.52 billion on December 31 of last year.

- Odaily Note: It's important to note that in the statistical methodology of US stock 13F filings, the market value displayed for option assets is typically the "notional value" of the underlying stocks, not the actual premium cost paid by the fund. This means that although the fund has built a "semiconductor hedge wall" with nominal assets of hundreds of billions of dollars, the actual cash cost (maximum potential loss) consumed is much smaller, representing a typical high-leverage macro hedge.

Additionally, this quarter, net capital inflows accounted for 32.51% of the fund's total holding value, indicating that the fund's explosive growth is not only due to portfolio appreciation but also involves substantial external new capital subscriptions (i.e., fresh capital injections).

Frenetic Portfolio Adjustment in Progress

The filing also shows that Situational Awareness LP executed substantial portfolio adjustments in the first quarter of this year.

- New Purchases: 23 stocks (including options);

- Added To: 9 stocks;

- Sold Out Of: 10 stocks (including options);

- Reduced Holdings In: 4 stocks (including options).

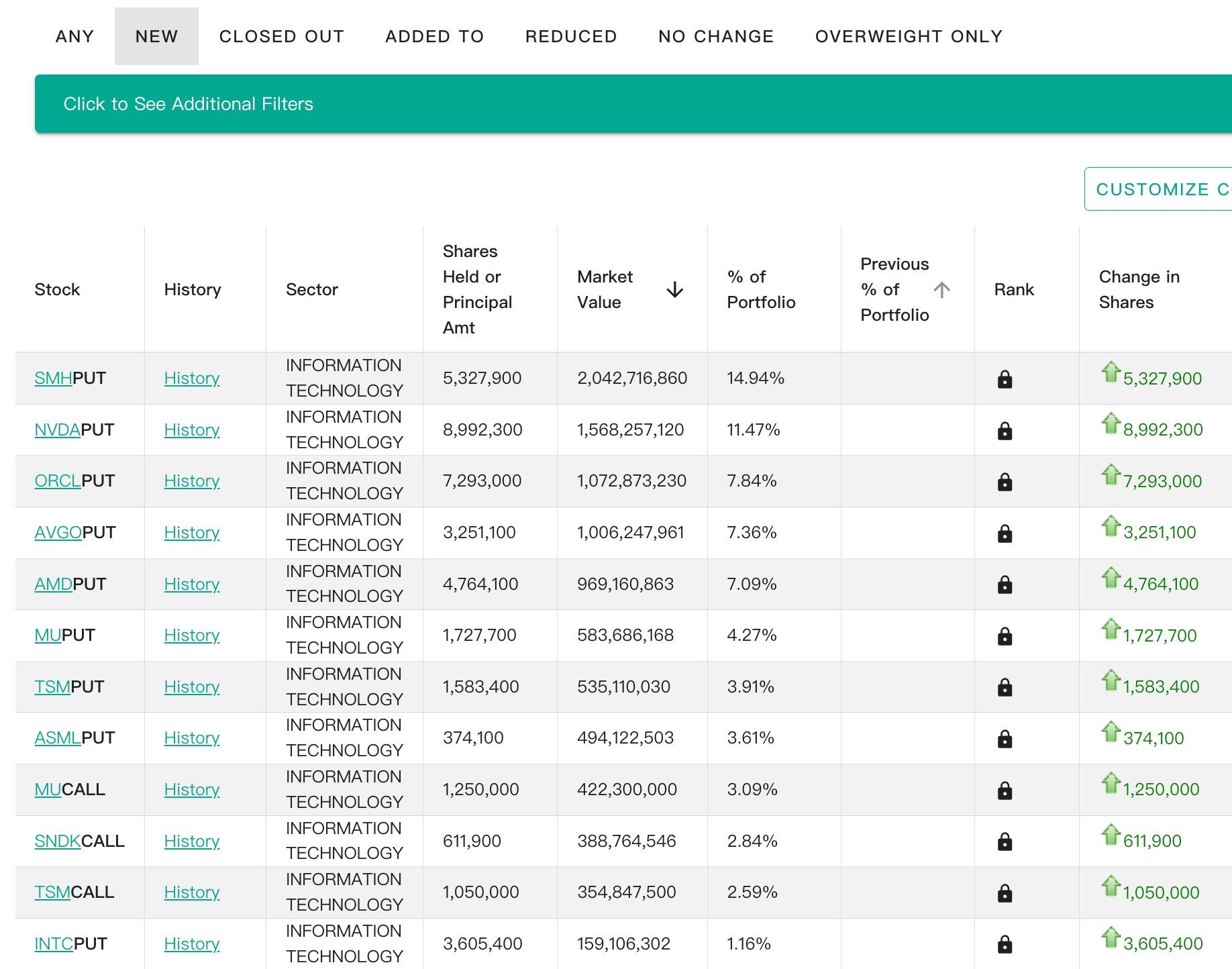

New Purchases: 60% Allocation Hedges Semiconductor Downturn

- Odaily Note: The chart above only covers new stock purchases with values exceeding $100 million. For the complete list of all 23 new purchases, click the "Portal."

First, looking at the new purchase actions, this is the most shocking information in Situational Awareness LP's entire 13F report — in the first quarter, the fund systematically hedged risks for the AI semiconductor and computing hardware sector through large-scale put option positions.

Looking directly at the data:

- SMH PUT (VanEck Semiconductor Core ETF Put Options): 14.94% of portfolio (market value $2.04 billion) — Largest new position;

- NVDA PUT (NVIDIA Put Options): 11.47% (market value $1.56 billion) — Second largest new position;

- ORCL PUT (Oracle Put Options): 7.84%;

- AVGO PUT (Broadcom Put Options): 7.36%;

- AMD PUT (AMD Put Options): 7.09%;

Just these top five put option holdings account for 48.7% of Situational Awareness LP's $13.7 billion nominal total holding value. Adding subsequent put options on Micron (MU), TSMC (TSM), ASML (ASML), and Intel (INTC), the fund has over 60% of its nominal portfolio betting on or hedging against declines or severe volatility in core AI hardware stocks.

It's also notable that Situational Awareness LP purchased both call and put options on the same stock, such as buying Micron put options (MU PUT, 4.27%) while also buying MU CALL (3.09%), and buying TSMC put options (TSM PUT, 3.91%) while also buying TSM CALL (2.59%).

This is a two-way bet strategy commonly used by hedge funds. It suggests the fund believes that Micron (memory chips) and TSMC (foundry) could experience stock price volatility far exceeding market expectations in upcoming 2026 earnings or industry cycles, possibly due to geopolitics or extreme supply-demand imbalances — profits can be made on both sides as long as the unidirectional move is large enough.

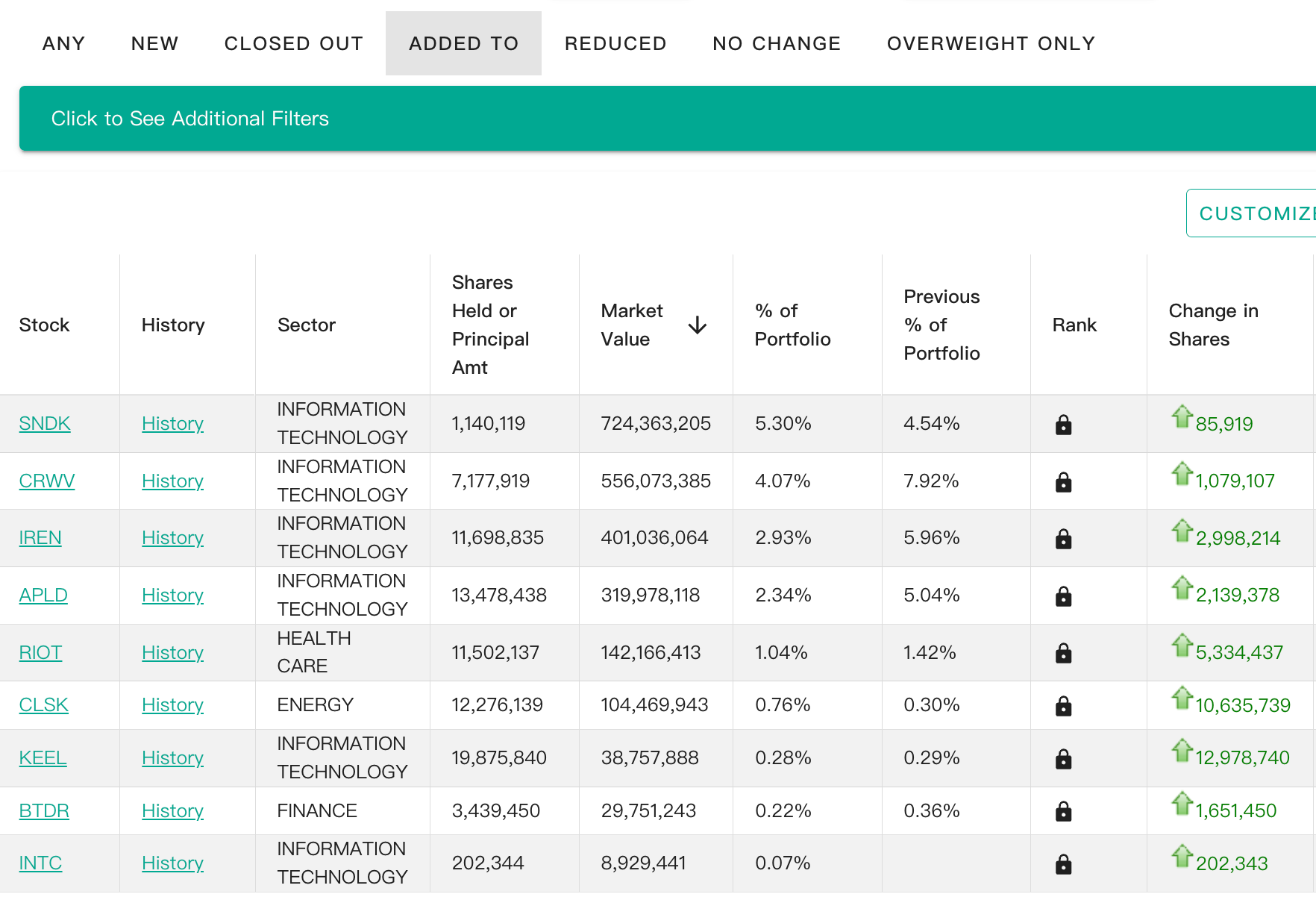

Increased Holdings: Common Stock Still Favors SanDisk, CRWV

Regarding increased holdings, Situational Awareness LP chose not to use options but rather added to 9 stocks via common shares.

In Q1, Situational Awareness LP slightly increased its position in SanDisk (SNDK) by 85,000 shares, bringing its total holdings to 1.14 million shares, with a holding value of $724 million, accounting for 5.30% of the entire investment portfolio. This is one of the very few super-heavyweight holdings in Situational Awareness LP's portfolio that exists entirely in common stock form.

Another noteworthy move is that Situational Awareness LP significantly increased its position in CoreWeave (CRWV) by over 1.07 million shares in Q1, pushing the holding value to $556 million, representing 4.07% of the portfolio. CoreWeave is one of the most closely watched infrastructure companies in the current AI GPU cloud services field and a key partner in the NVIDIA ecosystem. Shortly after its IPO, Situational Awareness LP swiftly incorporated it into its core portfolio and aggressively increased its position. This indicates that while the fund is short-term bearish on NVIDIA's valuation (via PUTs), it remains wildly optimistic about cloud giants that directly convert GPUs into computing power for leasing to large models.

Furthermore, Situational Awareness LP also increased holdings in KEEL, IREN, APLD, RIOT, CLSK, BTDR, and other computing or power infrastructure companies, continuing the logic advocated by Leopold Aschenbrenner that "electricity is the new oil."

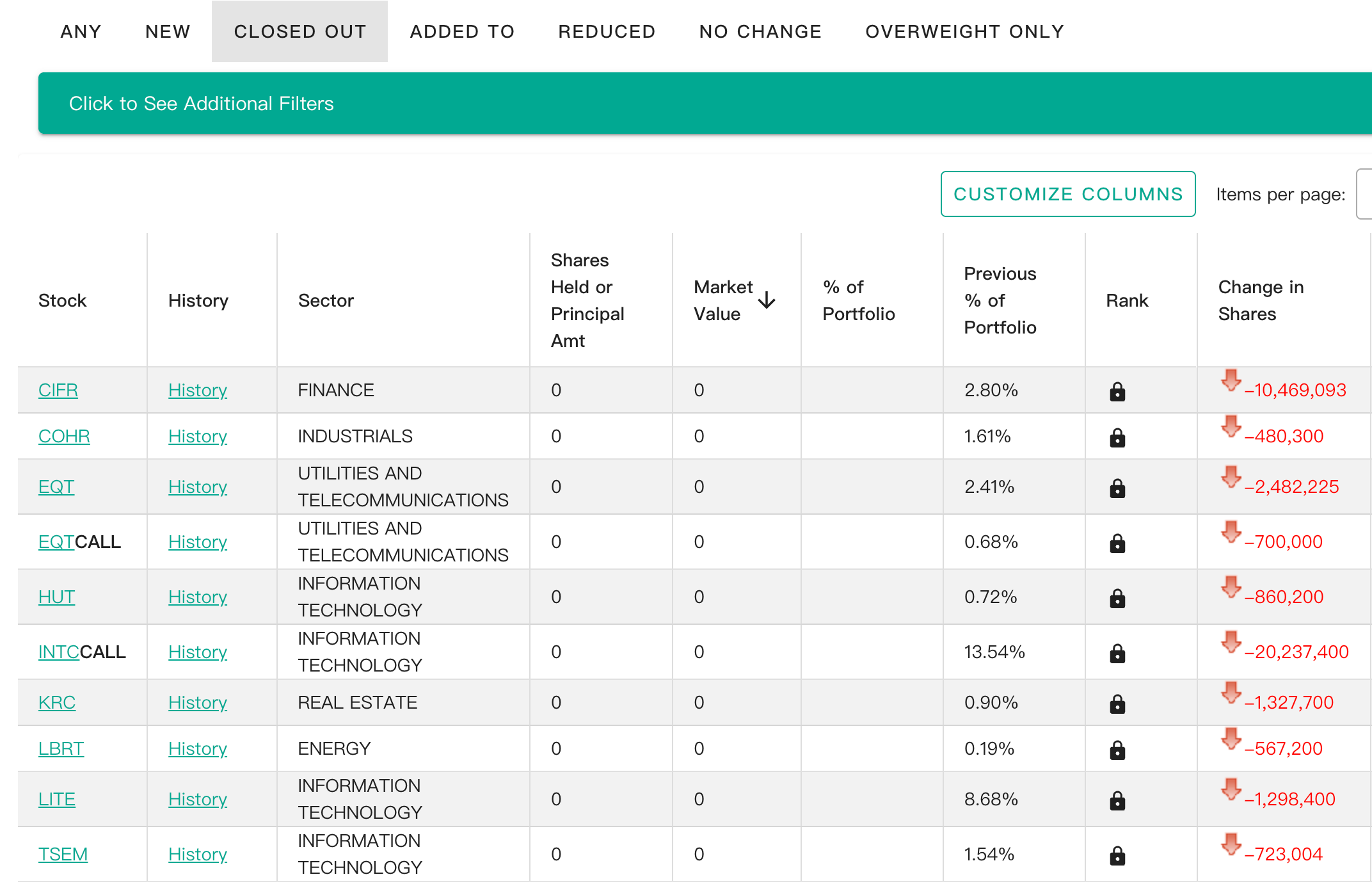

Liquidated Holdings: Unloading Intel Call Leverage, Exiting Optical Communications

Regarding liquidated holdings, Situational Awareness LP's most significant move was completely unwinding the leverage on Intel call options (INTC CALL). In the previous disclosure period, Situational Awareness LP had allocated over 13% of its portfolio to Intel call options (a staggering 2.023 million option contracts), representing an extremely high-leverage directional bet. This quarter, it liquidated this position entirely, shifting to holding a minimal common stock position in Intel (0.07%).

Additionally, Situational Awareness LP completely liquidated its positions in LITE (previous weight 8.68%) and COHR (previous quarter weight 1.61%) in Q1. LITE and COHR are among the world's leading optical communication chip and optical transceiver module giants. This liquidation suggests Situational Awareness LP is exiting the AI optical module/network hardware sector.

Situational Awareness LP also liquidated its positions in CIFR (previous weight 2.80%) and HUT (previous weight 0.72%) in Q1. Both are cryptocurrency mining companies (including CORZ, which was reduced in the next section). Considering the increased holdings in similar companies like RIOT, CLSK, and BTDR, this might just be a routine portfolio adjustment.

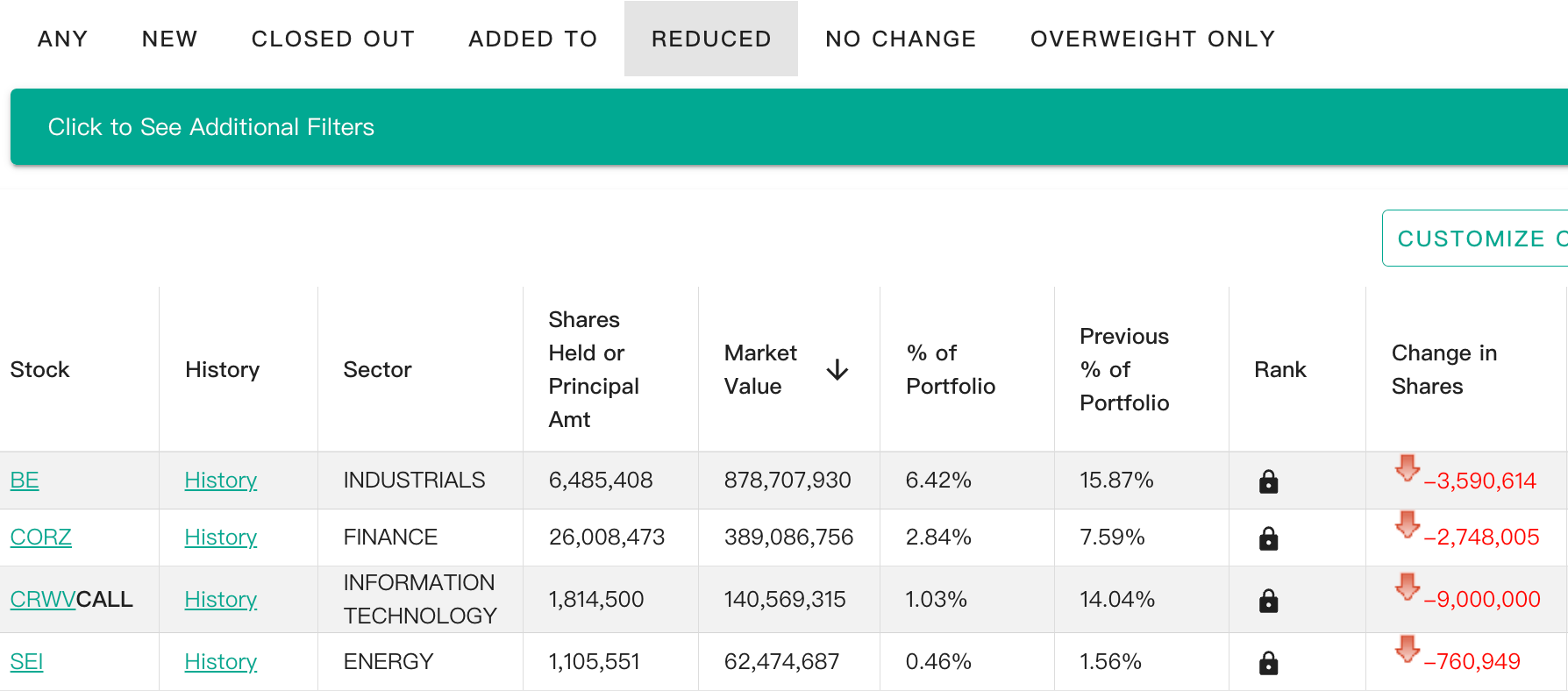

Reduced Holdings: Significant Profit-Taking on BE

Finally, looking at the reduced holdings, Bloom Energy (BE) was the top holding disclosed in Situational Awareness LP's previous 13F filing. In Q1, the fund reduced its position by 3.59 million shares, with the portfolio weight plummeting from 15.87% last quarter to 6.42%.

Bloom Energy focuses on solid oxide fuel cell technology and is a key player in providing "on-site power" for data centers, bypassing traditional power grids for direct supply. Considering the retained position is still substantial, the reduction likely does not mean Situational Awareness LP is no longer bullish on the company, but rather appears to be a routine profit-taking move.

CoreWeave call options (CRWV CALL) were Situational Awareness LP's second-largest reduction (portfolio weight plummeted from 14.04% to 1.03%). As mentioned earlier, the fund has shifted to holding CRWV via common stock, so this is more of a de-leveraging operation.

Situational Awareness LP also reduced its position in Core Scientific (CORZ) by 2.74 million shares, lowering the portfolio weight from 7.59% to 2.84%. CORZ is a leading Bitcoin mining company transitioning to AI computing power hosting. However, given that Situational Awareness LP increased holdings in other mining companies still in the transition phase with more attractive valuations this quarter, reducing CORZ seems more like partial profit-taking.

What Exactly Is the 'AI Stock God' Thinking?

Looking only at the surface data of this 13F, many might draw a simple, crude conclusion — Leopold Aschenbrenner, who once proclaimed "AGI by 2027," has turned bearish on AI.

But the reality is clearly not that simple. Within Situational Awareness LP's portfolio structure, there simultaneously exist two seemingly contradictory yet highly unified main themes.

- On one side, there is extreme vigilance toward short-term valuation bubbles in the "chip sector." Situational Awareness LP has used a shockingly large nominal allocation of PUTs (put options) to essentially "buy crash insurance" for nearly the entire AI semiconductor industry chain, including NVIDIA, Broadcom, and others;

- On the other side, there is an almost obsessive optimism about the long-term demand for AI infrastructure. Whether it's CoreWeave, Bloom Energy, or a series of companies related to electricity, transformers, and data centers, they all essentially point to the same deterministic logic — the war for AI computing power has entered a deep-water phase.

This is perhaps Situational Awareness LP's most core judgment at present. What will truly be scarce in the future may not necessarily be GPU chips themselves, but rather the energy, power systems, and data center infrastructure required to sustain these GPUs' continuous operation. GPU production can scale, and advanced process technology will eventually ramp up, but megawatt-level power supply capacity, transformers, transmission systems, and large-scale data center construction cycles are difficult to replicate simultaneously in a short time. Compared to the "selling shovels" logic already fully priced in by the market, Leopold Aschenbrenner seems more focused on where the real potential bottlenecks might emerge in the next stage of the AI industry.

This also explains why Situational Awareness LP would simultaneously buy large-scale semiconductor put options to hedge against severe volatility risks in the AI hardware sector while continuing to heavily invest in GPU cloud services, power, and computing infrastructure assets.

In a sense, this 13F is less a simple holdings disclosure and more like Leopold Aschenbrenner's directional roadmap judgment for the next stage of evolution in the AI industry chain.

When a genius investor who rose to fame by going all-in on AI begins to deploy multi-billion-dollar nominal positions to buy insurance for the AI sector, it at least indicates one thing — even the most steadfast AI bulls of this era have begun to take volatility itself seriously.