Author: Zhou, ChainCatcher

According to RootData market data, over the past year, BTC has fallen by 46.12% cumulatively, yet Bitcoin mining stocks have not declined in sync. Among them, HUT is up 363.26%, WULF up 268.95%, IREN up 121.14%, RIOT up 59.90%, and CLSK up 12.41%.

This round of gains is not built upon an improvement in the fundamentals of mining. June operational data shows that, despite consecutive downward adjustments in mining difficulty, CleanSpark, BitFuFu, and Canaan still saw month-on-month production declines ranging from 9% to 29%.

It is not difficult to see that the market's focus has shifted. Since July, CleanSpark signed a 20-year infrastructure lease with an initial period contract value of $6.6 billion, TeraWulf planned to raise $3.5 billion to expand a data center campus, and MARA acquired a Texas project company with a planned power capacity of up to 2 GW for up to $600 million.

Mining stock prices no longer revolve solely around coin prices, production output, and hashrate; the market has begun valuing them by a different set of logic.

The Source of Mining Stock Volatility Is No Longer On-Chain

At the beginning of the month, a typical dislocation occurred in the market, with mining stocks experiencing an overall pullback of about 20%, while BTC remained stable around $64,000.

On the production side, in June, CleanSpark produced 614 BTC, lower than 671 BTC in May, down 9% month-on-month. Its nominal hashrate was 50 EH/s, while its average operational hashrate was only 42.6 EH/s. The gap widened from 3.8 EH/s in May to 7.4 EH/s, indicating downtime or load reduction.

BitFuFu produced 125 BTC, down 29.4% month-on-month. Its total hashrate dropped from 19.5 EH/s to 15.3 EH/s, primarily dragged down by a reduction in third-party hosted hashrate from 16.3 EH/s to 11.8 EH/s.

Canaan produced 64 BTC, down 29% month-on-month, attributing part of the reason to grid maintenance at mining facilities.

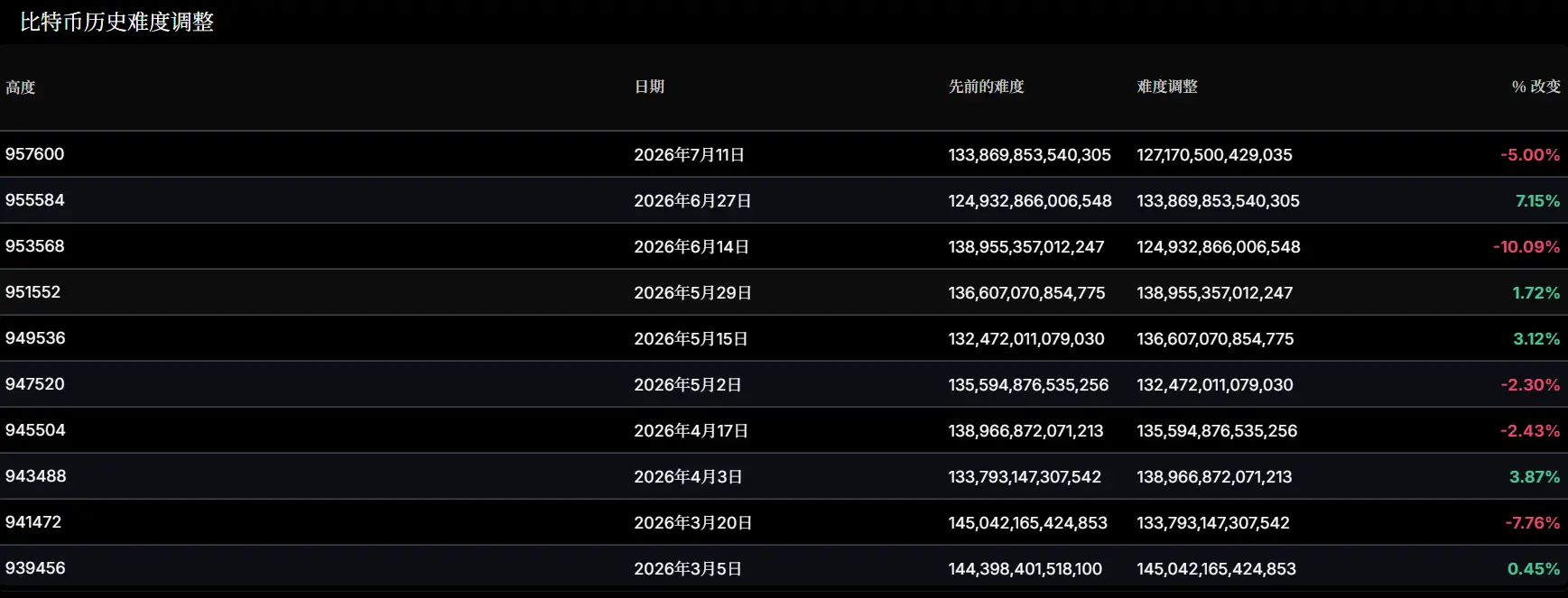

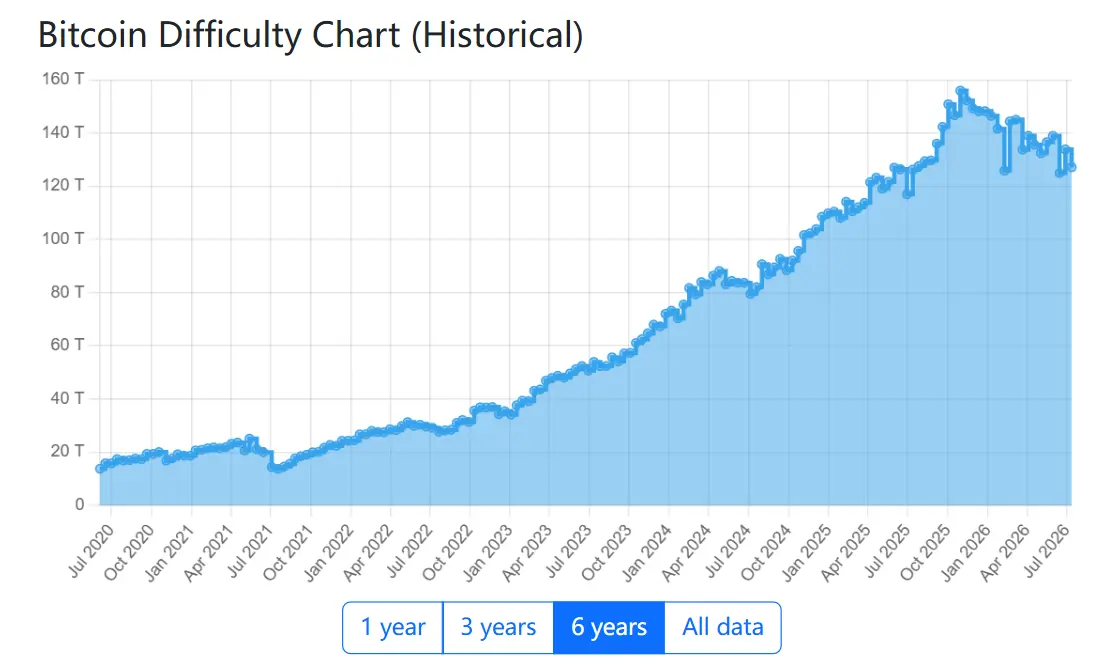

This round of production decline occurred after consecutive difficulty reductions. On June 14th, the Bitcoin network difficulty decreased by 10.09%, the second-largest negative adjustment in 2026. On July 11th, it dropped another 5% to 127.17 T, a cumulative decline of about 18% from the high point of around 155 T in November 2025.

A decrease in difficulty should allow miners remaining in the network to mine more coins per unit of hashrate, yet production output continues to decline.

On the other hand, amidst market downturn and pressure on profitability, some miners are continuously exiting the network or shutting down equipment. Galaxy Research states that miners are entering a capitulation period, representing the largest drawdown since China's comprehensive crackdown on Bitcoin mining in 2021.

The reason for the shakeout is straightforward. According to CoinShares' Q1 2026 mining report, the average cash production cost for listed miners had risen to about $79,995 in Q4 2025. JPMorgan estimates the current production cost at around $78,000, while BTC is currently trading near $64,000. The price gap has persisted for five months, with about 20% of miners operating at a loss.

According to Hashrate Index data, around March 2026, the hashprice once fell to a post-halving low of $28 to $30 per PH/s per day. It is currently around $32, still within the lowest historical range.

Reclassified into the AI Infrastructure Valuation Framework

The new logic is not complicated. What AI data centers currently lack the most are grid-connected power capacity, contiguous land, cooling systems, and building shells – resources that miners happen to possess.

They have large-scale grid connection capabilities, sites that can be retrofitted, existing operational systems, and are more familiar with the construction pace of high-load facilities.

PJM data shows that AI infrastructure projects put into operation in 2025 took over seven years on average, with about three years to secure an Interconnection Service Agreement and another four years waiting for grid connection. An already grid-connected mining site essentially skips these seven years, and this is where the value of mining companies lies.

Take CleanSpark for example. On July 14th, the company announced signing a 20-year triple-net lease with an undisclosed, highly investment-grade technology company for its Sandersville campus in Georgia. The initial term contract revenue is about $6.6 billion, corresponding to 175 MW of critical IT load, with delivery starting in Q4 2027. The market reaction was strong, with CLSK rising up to 22% intraday.

Also in July, MARA spent up to $600 million to acquire a Texas campus project company with a planned power capacity of up to 2 GW. However, this company holds a Letter of Intent with a power company. The gap between a Letter of Intent and actual power connection is precisely those seven years.

Furthermore, the credit market is also pricing them with new metrics. According to Bloomberg, TeraWulf plans to raise $3.5 billion led by Morgan Stanley, including leveraged loans and high-yield bonds, to expand its Justified Data campus in Horse Cave, Kentucky. This marks its first foray into the leveraged loan market. Lenders are also beginning to examine miners' balance sheets as infrastructure assets.

According to Guosheng Securities research, as of early May 2026, signed site hosting, bare metal, and cloud contracts within the sector totaled approximately 3,201 MW of critical IT load, with a total contract value exceeding $91.4 billion. The agency also found that the market capitalization of companies in the sector showed a clear positive correlation with their AI power capacity reserves in North America and their already contracted AI power capacity.

CoinShares expects that by the end of 2026, up to 70% of revenue for listed miners will come from AI and HPC, compared to about 30% at the beginning of the year. TeraWulf has already arrived first; its Q1 HPC leasing revenue was $21 million, surpassing its mining business revenue of less than $13 million for the first time.

The Cost of Revaluation: Three Layers of Risk

The first layer of risk comes from valuation.

If miners are revalued as AI infrastructure, it also means they must bear the overall volatility of the AI narrative.

A 10x Research report stated that Bitcoin mining stocks have largely decoupled from the coin price trend. Since April 2026, RIOT's stock price has shown increased correlation with the Philadelphia Semiconductor ETF.

Bitcoin mining companies are now deeply tied to the AI theme. Currently, the AI theme revolves more around the global supply chain and competition rather than crypto adoption or financial digitization. Moreover, the performance of Chinese LLM concept stocks and the prospects of the South Korean semiconductor supply chain are directly affecting Bitcoin mining stock trends.

After a significant rally in these sectors, risk appetite is contracting. The Philadelphia Semiconductor Index fell 10.8% over ten trading sessions, with Reuters estimating an evaporation of about $1.3 trillion in market cap across the industry. The root causes identified include doubts about AI infrastructure investment returns, dot-com bubble-level valuations, and a more hawkish Fed.

The second layer of risk comes from return rates.

According to a Bernstein report, Core Scientific's five-year average return on assets from its cooperation with CoreWeave reached 75%, but the driver was the capital expenditure structure rather than the deal terms, with the tenant covering $750 million of the $855 million total cost through revenue prepayments. Riot achieved a 23% return by retrofitting existing mining sites.

However, these two are not industry benchmarks. The report notes that the industry baseline return rate actually falls at TeraWulf 5%, Cipher 4%, CleanSpark 4%.

A report on July 1st stated that Meta plans to launch Meta Compute, selling excess AI training and inference computing power to enterprise clients. That day, the Philadelphia Semiconductor Index fell 6.3%. The next day, SK Hynix CEO Kwak Noh-Jung announced that the SK Group will invest 100 trillion won in South Korea to build AI data centers in phases, starting with 5 GW and eventually expanding to 15 GW.

Meta, as the largest buyer, saying it has excess capacity, and chipmakers saying they will build their own facilities, while miners sign 15 to 20-year long-term contracts, not realized revenue. That's how the 20% pullback in mining stocks at the beginning of the month occurred.

The third layer of risk comes from execution.

Miners are now priced based on the future, not realized revenue. Taking CleanSpark as an example, the company just signed a $6.6 billion long-term contract, but its current revenue still entirely comes from Bitcoin mining; the AI business has not yet generated substantial revenue, with the first delivery not until Q4 2027.

Valuation has moved ahead first, but realization must overcome three major hurdles:

The first hurdle is financing capability. According to CleanSpark's 8-K filing, the campus construction cost is $10 to $12 million per megawatt. For 175 MW, this corresponds to $1.75 to $2.1 billion in capital expenditure, which has not yet been raised. The filing also explicitly states that failure to meet any of the financing, construction, or delivery milestones will trigger rent reductions or even lease termination.

The second hurdle is regulatory approvals. On July 14th, New York Governor Kathy Hochul signed an executive order suspending the issuance of state-level permits for large data centers, with the threshold being a grid demand of over 50 MW. The New York State Department of Environmental Conservation has suspended all discretionary permits not deemed complete before July 14th. The suspension period is tied to the completion of a Generic Environmental Impact Statement rather than a fixed date, up to one year.

The third hurdle is tenant quality. Bernstein points out that tenant quality directly affects the valuation level of miners. Hyperscale cloud providers bring more stable cash flows and lower financing costs, while small GPU cloud service providers correspond to higher operational risks and capital costs.

Miners' Selling Logic Decouples from Coin Price

With the change in valuation logic, miners' behavior has also changed. However, a more direct impact of this shift on the crypto space is reflected in how miners sell coins.

According to industry reports, listed miners collectively sold approximately 32,000 BTC in Q1 2026, a scale that has already exceeded the full year of 2025. Among them, Riot produced 1,473 BTC in Q1 but sold 3,778 BTC in the same period, more than double its production. Its holdings dropped to 15,680 BTC, down 18% year-on-year.

In the past, miners sold coins mainly based on mining cash flow logic – to pay electricity bills, repay loans, and maintain daily operations – holding back during low prices and waiting for a rebound to sell. Now, there is an additional layer of transformation financing logic. Selling coins also makes room for building stations, acquiring land, covering capex, and longer-term AI construction plans.

Therefore, even if the coin price does not experience extreme volatility, miners may continue selling coins.

The same logic also determines whether the hashrate that has left will return.

In the past, hashrate exiting the network was assumed to return when coin prices rebounded and difficulty dropped. After China's comprehensive crackdown on mining in 2021, difficulty plunged 46% but recovered within half a year. But now, what's leaving may not just be mining machines, but also the supporting power supply and capital expenditure.

Current mainstream AI contracts are mostly long-term agreements of over 10 years. Once miners lock their sites, power, and financing structures into such contracts, these resources are unlikely to return flexibly to BTC mining as they did before.

Therefore, mining companies are moving further away from crypto. More accurately, the capital market has already begun valuing them based on their form after leaving the pure mining framework.

They will still affect the Bitcoin network and still generate revenue from mining, but the pursuit of power, land, and long-term leases is turning them into a different type of company.