Author: Think AI, Aaron

The surge in artificial intelligence stocks has been going on for three and a half years now, with no signs of stopping;

Those who started predicting a US stock market crash and an AI bubble last year have fallen into deep thought.

South Korea's stock index has triggered circuit breakers 19 times this year. The main board index has quadrupled since last year. SK Hynix is up 260% year-to-date, either hitting new highs or on the way to new highs;

US memory giant Micron broke the trillion-dollar market cap, joining the top 10 US companies by market value, with gains of over 200% year-to-date and more than 10x in a year;

In Japan, SoftBank, which previously invested in Alibaba, is seeing its stock price rise continuously due to its heavy bets on AI, and it has already become Japan's highest-valued company.

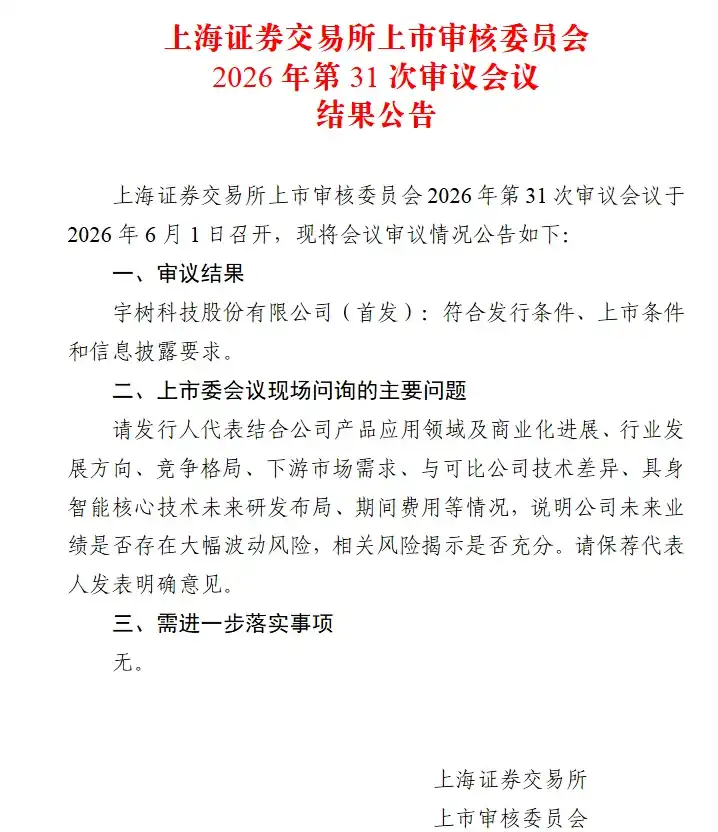

Domestically, Yushu and ChangXin have already passed listing reviews. ChangXin's market cap starts at 1.5-2 trillion yuan, directly placing it in the top 5 of A-shares;

Meanwhile, AI companies like Nvidia and Google are always rising amidst fear; there's even news that housing prices in Shenzhen and other Chinese cities are warming up, as executives from semiconductor and AI companies, buoyed by超预期收益, are starting a batch property-buying spree.

But there is another scene: those who took out loans to buy gold at the beginning of the year are still underwater, domestic consumer stocks continue to slide quietly, and many netizens say they have completely missed this AI bull market, feeling anxious every day. What should they do now?

Profits Are Always for the Minority

First, look at the data. In 2025, only about 18.9% of A-share retail investors made a profit, while a staggering 81.1% incurred losses, with an average loss of about 21,000 yuan. For small散户 with less than 100,000 yuan, the loss ratio was close to 98.7%.

This happened in 2025 when the大盘指数 closed up nearly 20%, the STAR 50 index saw a maximum intra-year gain of 80%, and the market overall rose last year. Wind data shows 500 stocks doubled in 2025, with over 120 rising more than threefold.

When the大盘 corrected from January to April 2026, faith in AI collapsed, and institutions cut their losses at the lows.

During the decline, AI stocks saw a wave of减持. Ingenic's (optical module) controlling shareholder and executives减持 4.914 billion yuan, after which the stock price rose another 35%; Kunlun Tech's major shareholder Li Qiong planned to减持 35.86 million shares. After the减持 announcement, the stock price fell 20%, but then rebounded 40% within a month, with some减持 shareholders "selling at the bottom."

A专题报告 by Securities Times on the AI sector减持 pointed out that in the AI computing power板块 in 2026, potential收益损失 caused by institutions减持ing too early exceeded 200 billion yuan (calculated based on average gains post-减持).

Meanwhile, institutions that firmly held onto AI often bet on the wrong方向.

At the end of 2025, institutions bet on vertical applications like AI education and AI healthcare. These vertical applications failed to爆发, and in 2026, these板块平均跌幅 over 20%, while the computing power板块 rose over 50%;

Looking abroad, missed opportunities and premature selling are everywhere.

The globally renowned fund Bridgewater大幅减持ed Nvidia (nearly two-thirds), Alphabet (over half), Amazon (9.6%), and Microsoft (35%) in Q3 2025. Subsequently, from Q4 2025 to Q1 2026, these stocks平均涨幅 over 80%;

There are even many short sellers. Short interest in the US stock market recently hit its highest level since 2012.

Data shows hedge fund total leverage has risen to about 293%. Short exposure and the Days-to-Cover indicator for the S&P 500 both hit records.

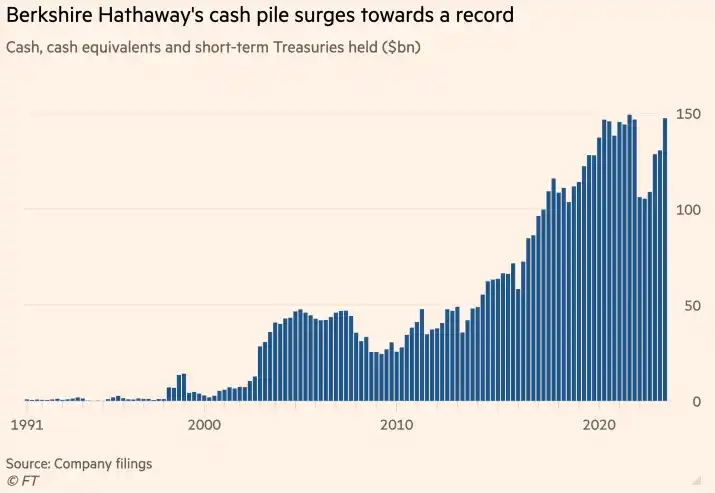

Even the mighty Warren Buffett started减仓 early. His cash reserves reached a record $397.38 billion in Q1 2026, completely missing the AI行情 and the surge in US tech stocks.

Multiple Waves Rising Simultaneously

But it's undeniable that AI remains the most certain and revolutionary opportunity in the current market.

AI is not a short-term concept, but a底层基础设施革命 akin to electricity and the internet. Historical experience shows that many who missed the first wave of tech stocks found opportunities in the application layer or the next round of infrastructure upgrades.

China also has unique空间 in AI self-research, application落地, and补短板ing the industrial chain.

When we feel迷茫 and anxious, perhaps we should look at how the best in the industry see it. This might give us some guidance and启示.

Ma Huateng of Tencent, long considered lagging in the AI era, has been catching up fiercely since last year. His remarks at this year's May shareholders' meeting sparked heated讨论.

Regarding AI, he said, "A year ago, we thought we had boarded the ship, but later found it was leaking. Now it feels like we're standing on it, but can't sit down yet. We still hope the ship can go faster."

Regarding "how to proceed next," he pointed out, "We can't just跨过去 and抢 others'地盘 because we see them doing it there. We've抢ed before but mostly failed later."

Indeed, the AI era offers vast opportunities. Combining one's own strengths and characteristics to find the most suitable opportunity is the best choice.

Now retired from the front lines but having had deep洞见 into AI 10 years ago, Jack Ma said AI is a once-in-centuries, industrial revolution-level opportunity comparable to the invention of electricity. The AI era has just begun, and now is the time to布局; there's no such thing as missing out;

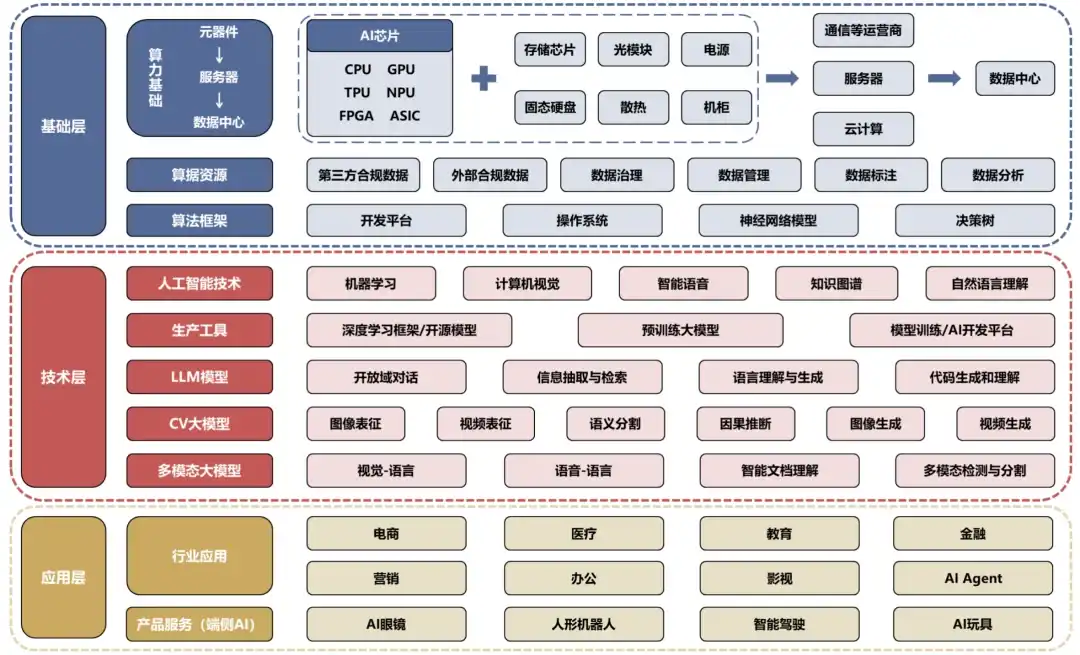

From computing power infrastructure and large model platforms to industry-specific AI applications, the entire产业链持续释放s long-term investment opportunities.

From this perspective, the entire产业链 offers无限 opportunities. Whether in work, investment, or entrepreneurship, digging deep along the产业链, coupled with段永平's long-termism and本分思想, will eventually yield results.

Large models are now smart enough, but only Claude has率先 achieved profitability in the coding agent赛道. AI+ is still on the way.

The next round of structural opportunities will definitely be留给 those who are well-prepared and maintain a stable心态.