Author: Prathik Desai

Compiled by: Chopper, Foresight News

Today's global salary system harbors a hidden layer of foreign exchange risk. Freelancers in India, Argentina, and Turkey who work for American companies are paid in US dollars, but their rent, daily purchases, and taxes require using their local fiat currency. The current logic of salary disbursement defaults to the requirement that funds must be converted into local currency immediately upon receipt. This model does not align with the actual needs of most people; if the local currency depreciates rapidly against the US dollar, workers can suffer unintended property losses.

If workers could save in dollar-denominated assets and spend locally for daily needs, the problem would be solved. Stablecoin salary solutions happen to achieve precisely that.

An example: A designer in Mumbai converts their entire monthly salary into rupees upon receipt, holding no dollar assets thereafter. If the rupee continues to weaken in the following months, they cannot benefit from the dollar's value preservation, and the purchasing power of their local currency holdings shrinks continuously. Over the past year, this Indian designer lost over 10% in purchasing power simply because they couldn't retain dollar income. Conversely, if they could retain part of their salary in dollars or dollar-pegged stablecoins, they could avoid the asset erosion caused by local currency depreciation.

In this article, I will explain why global workers are increasingly choosing to be compensated in dollars or stablecoins and what they stand to gain by doing so.

Ubiquitous Foreign Exchange Loss

Workers who live in one country but are employed by companies in another earn income in one currency but spend in another. How they handle currency conversion determines whether they quietly incur losses or gain benefits.

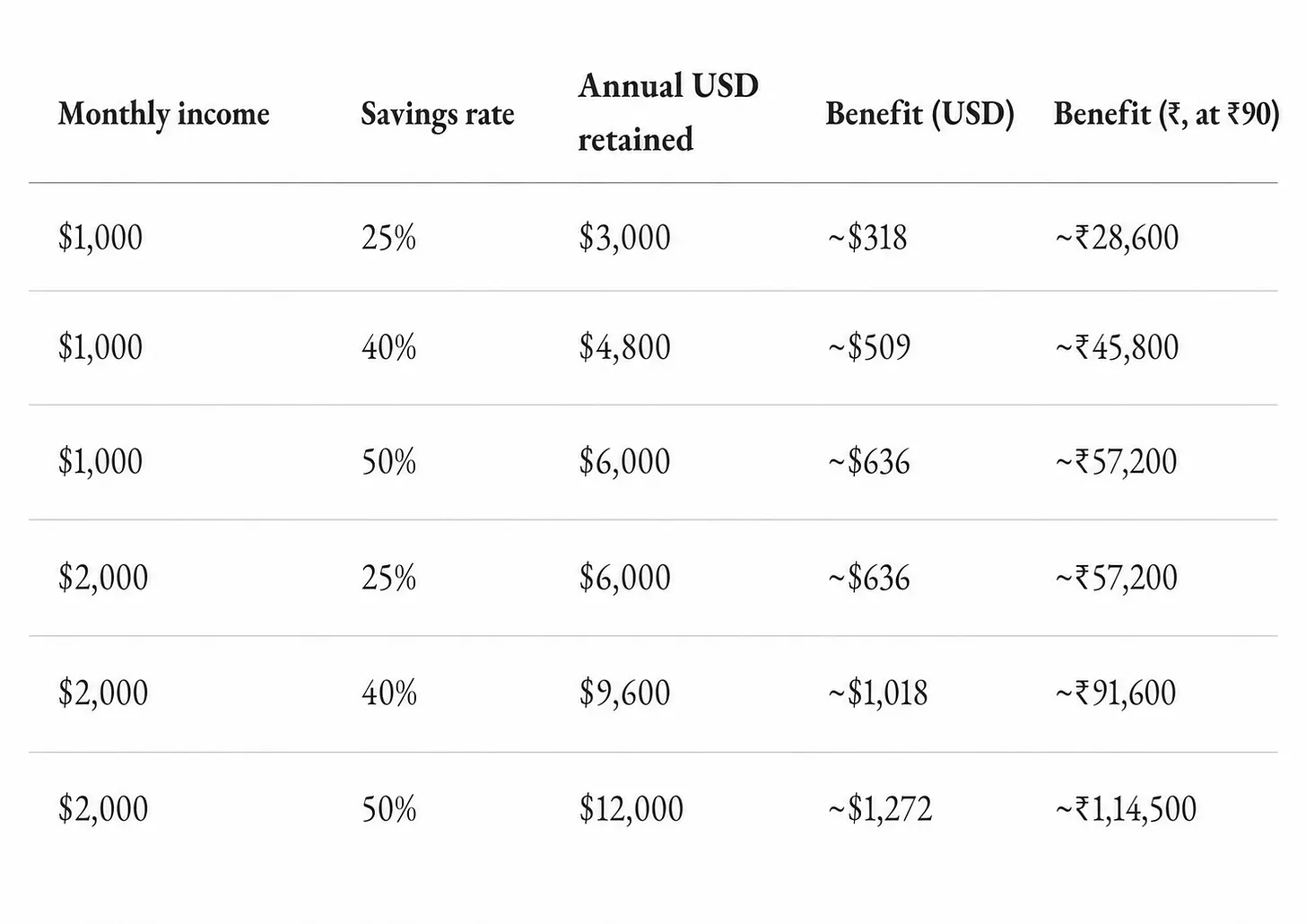

Assume an Indian freelancer earns $2000 per month. If they spend all their income within a few days each month, there is no foreign exchange gain or loss. However, if they save 25% of their income monthly for long-term savings, over time, dollar assets can yield substantial value preservation benefits. How substantial is this potential gain?

Over the past 12 months, the USD to Indian Rupee exchange rate rose from about 85.6 rupees to 94.7 rupees, a depreciation of over 10% for the rupee. Let's calculate the asset loss for an Indian worker across scenarios: Monthly income of $2000, saving 25% for savings, resulting in an annual savings total of $6000. If converted entirely into rupees and held, they would lose $600 in purchasing power over the year. This sum isn't a vast fortune, but in a major Indian city, it's enough to cover a month's rent for a well-furnished two-bedroom apartment.

If monthly savings are all converted and held in local currency, the purchasing power of the assets will continuously shrink as the local currency depreciates.

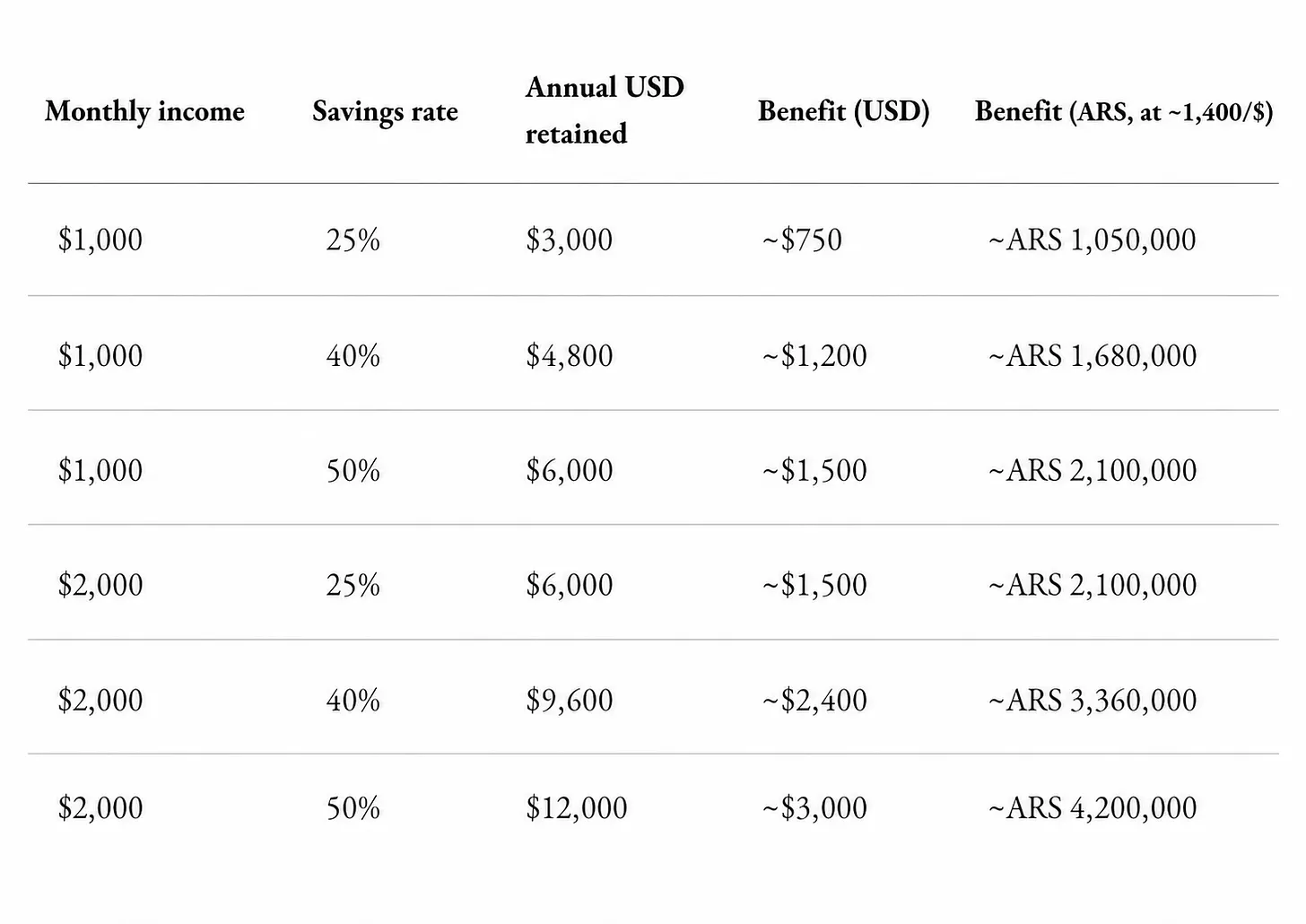

The higher the depreciation of the local currency against the dollar, the more pronounced the contrast. Take Argentine workers as an example: Even if salaries are paid in dollars, converting them entirely into pesos and holding them means their assets would have shrunk by a quarter over the past year, given the peso's 25% depreciation against the dollar.

Data from financial service provider Wise shows that if income is retained in dollars, workers' asset purchasing power can increase by one-third. This isn't mere speculation; it reflects the real situation of many freelancers in Buenos Aires. Research from the human resources platform Deel's "State of Global Hiring Report" indicates that among surveyed Argentine workers, about 85% prefer to receive salaries in US dollars rather than their national currency.

However, the value preservation advantage of dollar salaries depends entirely on how the funds are handled: The dollar's value preservation value manifests only if funds are retained long-term; the higher the retained amount and the longer the holding period, the greater the difference in gains from foreign exchange.

For Indian workers, holding dollars is a means of optimizing income through financial management; for Argentine citizens, holding dollars is more like a safeguard against local currency inflation. The same demand exists in most economies worldwide with high inflation and continuously depreciating local currencies.

Stablecoins: Breaking Down Barriers to Dollar Holdings

All the logic above is based on holding US dollars, but the barrier for ordinary individuals to open dollar accounts with foreign banks is extremely high.

Every bank takes a cut of fees before dollars reach you. Before an international wire transfer arrives, fixed wire transfer fees, correspondent bank commissions, and currency exchange spreads—which most workers are unaware of—must be paid.

The average comprehensive cost of global cross-border transfers is about 6.5%. For a worker earning $2000 per month, cross-border fee losses could even exceed the depreciation losses avoided by holding dollars. Stablecoin transfers can bypass most of these fees: costing only a few dollars and settling in seconds, whereas wire transfers take 3 to 5 business days.

Additionally, Indian residents cannot hold dollars without limits; regulations restrict the types of dollar deposit accounts and annual holding ceilings, and regular overseas income is defaulted to direct conversion into rupees. A designer wanting to retain three months' salary in dollars must comply with strict foreign exchange controls. Many high-inflation countries with depreciating local currencies, aiming to curb hyperinflation and prevent capital flight, restrict their citizens from holding dollars; countries like Venezuela, Iran, and Afghanistan have all implemented related control policies.

To fill this gap, a series of self-custodial stablecoin wallets have emerged. Taking the Altitude platform, built on the Squads smart account system, as an example: The platform holds user funds in stablecoins issued by compliant dollar issuers like Circle and Bridge, with issuers holding 1:1 dollar reserve backing; assets are held in wallets controlled by the user's private key, with the platform not custodial. Workers autonomously hold dollar-equivalent assets on-chain, and no institution has the authority to interfere with their choice to hold dollars.

However, the self-custody model has pros and cons. If the private key is lost, there is no bank customer service to help recover it, and assets do not enjoy deposit insurance protection.

This type of account supports on-demand conversion to fiat currency, withdrawing only funds needed for daily expenses like rent and utilities, while leaving the remaining assets entirely in dollar stablecoins. This perfectly solves the pain points of dollar account limits and difficult account opening, allowing workers to hold dollar assets without bank approval.

The retained dollar stablecoins are not idle funds; accounts can connect to on-chain lending, short-term US treasury bonds, and other yield products. In contrast, local currency bank deposits only lead to continuous depreciation of assets.

Beyond this, stablecoin balances can be linked to payment cards for direct spending. Regardless of the on/off-ramp channels used by the transacting parties, stablecoin transfers can complete merchant settlements in seconds. Multi-currency accounts, foreign exchange conversion engines, payment channels covering over 150 countries, savings and wealth management, and debit card functions are all integrated into a single on-chain account controlled by the user.

However, this solution is not without flaws. Stablecoin account funds do not yet have the same insurance protection as bank deposits. Tokenized deposit products are gradually addressing this shortcoming but have not achieved widespread adoption. Regulatory boundaries for digital assets and stablecoins are blurry across countries, making it difficult for freelancers to fully understand local compliance requirements. Nonetheless, the industry trend is clear.

The aforementioned "State of Global Hiring Report" points out that freelancers in high-inflation countries increasingly prefer to settle salaries in dollars or stablecoins. Among the top ten mainstream salary settlement currency combinations globally in 2025, five are settled in US dollars.

This is not a new phenomenon. For the past century, people globally have always desired to hold the global reserve currency, the US dollar, but for a long time, it was difficult for ordinary people to achieve: requiring overseas accounts, professional brokers, cumbersome paperwork, and bearing high bank fees. Workers in Istanbul, Buenos Aires, and Mumbai have all wanted dollars but couldn't due to various restrictions. Stablecoin salaries completely reverse this situation: Income is directly disbursed as dollar-equivalent assets, unrestricted by place of residence, and retaining dollars requires no institutional permission.

It's not hard to see that this is a far-reaching industry transformation.

Governments may view stablecoin salaries as a channel for capital flight and attempt to introduce regulatory policies to restrict them, but the value created by the stablecoin salary system is difficult to deny.

Any low-cost, high-efficiency capital flow infrastructure will ultimately gain market recognition and regulatory acknowledgment. The International Monetary Fund (IMF) recently advised Nigeria not to ban dollar stablecoins but to manage related risks. The institution's previous years of strong opposition to stablecoins make this shift in policy stance sufficient proof that stablecoins have gained mainstream financial market recognition.

In the salary field, stablecoin infrastructure has achieved the deconstruction and reconstruction of five major functions: payment currency, asset storage, wealth management returns, consumption payments, and cross-border circulation.

This is precisely the core value that currency should possess: freedom and flexibility.