Autor: neira, Arquitecto de productos financieros tokenizados en Tempo

Compilación: Jiahuan, ChainCatcher

La mayoría de la gente cree que las stablecoins están replicando la función del eurodólar e impulsando una mayor expansión del sistema del dólar extraterritorial.

Pero no es así. Las stablecoins sustituyen principalmente sólo parte de las funciones del sistema existente, especialmente los saldos en dólares necesarios para las operaciones diarias y la liquidación; en algunos aspectos cruciales que la Reserva Federal vigila de cerca, incluso podrían reducir el efecto multiplicador de la expansión crediticia.

Lo que realmente vale la pena preguntar es: ¿Qué sucede cuando los intermediarios financieros, sobre la base de las stablecoins, crean una nueva capa de pasivos en dólares sobre ellas?

Este artículo explicará cómo funciona este nuevo canal de financiación garantizada, qué condiciones necesita para escalar, y por qué su comportamiento bajo estrés tiene una estructura fundamentalmente diferente a la del sistema tradicional del eurodólar.

Resumen

Las stablecoins introducen un pasivo en dólares privado tokenizado. Incluso si el emisor, los activos de reserva y el banco de liquidación principal permanecen dentro de los límites legales de EE.UU., o dependen de la infraestructura bancaria y de liquidación de valores conectada a EE.UU., este pasivo puede volverse "extraterritorial" en sustancia económica por su circulación y uso como garantía.

El control exigible sobre la garantía abre un canal de crédito garantizado, pero no crea por sí solo un pasivo monetario. El verdadero evento monetario sólo ocurre cuando otro balance proporciona financiación, renueva este pasivo creado contra el token controlado, o lo acepta a un precio cercano a su valor nominal.

El descuento (haircut) marca el precio de la distancia entre el "control efectivo sobre el token" y su "conversión fiable a dólares bancarios". La fuente de elasticidad es diferente: proviene del balance que emite el pasivo contra el token, y de la disposición de terceros balances a tratar este pasivo como un activo cercano al valor nominal incluso bajo estrés.

Las variables decisivas incluyen: quién tiene el control efectivo sobre el token, a través de qué ruta legal y operativa se convierte en dólares bancarios, cuál es su costo real, su plazo, y si el pasivo resultante puede seguir siendo financiado a un valor cercano al nominal cuando esas rutas se bloquean.

El dólar de garantía no es la stablecoin en sí. Es el pasivo de segunda capa que otro balance está dispuesto a emitir, financiar y mantener a un nivel cercano al valor nominal, respaldado por un saldo de tokens controlado.

1. El sistema del eurodólar es una jerarquía de pasivos

En sentido estricto, un eurodólar es un pasivo bancario denominado en dólares registrado fuera de la jurisdicción directa de la Reserva Federal: es una promesa privada de entregar dólares, emitida por una institución bancaria cuya ubicación legal, tratamiento regulatorio y acceso a la liquidez difieren de los de un banco estadounidense nacional.

El sistema del dólar extraterritorial en un sentido más amplio también incluye los pasivos en dólares emitidos por dealers e intermediarios de mercado, respaldados por garantías y derivados. La unidad de cuenta sigue siendo el dólar, pero los balances que emiten estos pasivos están fuera de la jurisdicción directa del banco central.

Este mercado constituye un sistema de balances privados en dólares. Una institución extraterritorial puede crear un pasivo en dólares simplemente registrando simultáneamente un pasivo y un activo coincidentes. La liquidación final aún puede pasar por el sistema de pagos estadounidense, pero la "creación" y la "liquidación" están separadas en el espacio institucional.

Esta separación permite a las instituciones no estadounidenses financiar posiciones en dólares, cubrir riesgos y liquidar sin depender constantemente de dinero del banco central nacional. Pero también crea dependencia: dependencia de la capacidad de renovación, del crédito interbancario, de la intermediación de los dealers y de la conversión a pasivos de mayor jerarquía cuando aumenta la presión de liquidación.

Los pasivos se ordenan jerárquicamente según: la fuerza de la promesa de valor nominal, la calidad de los activos subyacentes, el plazo, la liquidez de mercado y la inmediatez del acceso a dinero de mayor jerarquía. En condiciones normales, la creación de mercado (market-making) y la renovación comprimen esta estructura jerárquica. Bajo estrés, esta compresión se invierte: los límites de contraparte se estrechan, los plazos se acortan, los descuentos aumentan y la estructura jerárquica reaparece a través de diversas restricciones operativas.

La elasticidad proviene de aquellos balances dispuestos a expandir sus pasivos en dólares antes de que las duras restricciones de la liquidación final se impongan.

En el canal no garantizado, los bancos extraterritoriales emiten depósitos, certificados de depósito o pasivos interbancarios, e invierten los fondos obtenidos en activos en dólares. En el canal garantizado, un dealer emite un pasivo en dólares contra una garantía, donde el descuento determina cuánto financiamiento puede soportar dicha garantía.

En el canal de derivados, los swaps y forwards de divisas generan financiación en dólares no a través de un depósito inmediatamente visible, sino a través de compromisos a lo largo del tiempo. La pata a plazo (forward leg) permite a bancos y no bancos convertir capacidad de balance en el plano monetario en capacidad de financiación en dólares. Un saldo de stablecoin transferible es sólo un pasivo a la vista, sin ningún mercado de financiación a plazo detrás, por lo que no puede replicar esta función en absoluto.

En el contexto del eurodólar, "extraterritorial" se refiere principalmente a la ubicación legal y del balance desde donde se emite el pasivo. La ruta para que una stablecoin adquiera atributos "extraterritoriales" es diferente: lo hace a través de su uso económico: incluso si el emisor y sus reservas permanecen en EE.UU., o dependen de infraestructura bancaria y de liquidación conectada a EE.UU., sus cadenas de circulación, custodia, staking y apalancamiento pueden operar fuera de los límites legales estadounidenses.

Por lo tanto, lo que realmente vale la pena comparar es el contraste entre dos cadenas: la cadena de garantía de las stablecoins frente a la cadena de financiación del dólar extraterritorial. Comparar directamente "token" con "depósito en eurodólares" es una comparación desajustada.

Un depósito en eurodólares, desde su nacimiento, se asienta en un balance bancario capaz de expandir el crédito: tiene elasticidad desde el primer asiento contable. Una stablecoin nace en el balance de un emisor que promete respaldo de reservas, por lo que en su nacimiento sólo aporta "sustitución"; la elasticidad aparece más tarde, en otro lugar.

Sólo cuando otro intermediario emite contra ella un pasivo financiable, y más balances aceptan ese pasivo a un precio cercano al valor nominal, la stablecoin se relaciona con la elasticidad.

2. Las stablecoins interrumpen niveles específicos del sistema del dólar extraterritorial

Las stablecoins alteran la composición de los pasivos dentro de ciertos niveles específicos del sistema del dólar extraterritorial. El sistema en sí permanece en su lugar.

La sustitución más obvia ocurre en este caso: el tenedor quiere un saldo en dólares transferible, no acceder a un balance completo en dólares. Los exchanges, brokers, empresas de pagos y algunos departamentos de tesorería corporativa pueden mantener stablecoins como inventario de liquidación. En este uso, el token asume parte de la función que antes cumplían los depósitos operativos extraterritoriales.

El cambio en el balance aquí es directo. El usuario sustituye un pasivo contra un banco extraterritorial por un pasivo contra el emisor de la stablecoin. El banco pierde ese pasivo, y el emisor adquiere un nuevo pasivo en tokens, emparejado por su cartera de reservas.

La composición de estas reservas determina dónde reaparece finalmente la demanda de fondos desplazada. Si las reservas permanecen como depósitos bancarios, el sistema bancario recupera parte de esos fondos. Si las reservas se trasladan a letras del Tesoro o repos, la presión se desplaza al mercado de garantías soberanas y a los intermediarios dealers. Esta sustitución sólo redirige la "dependencia de los bancos", no la elimina.

Esta sustitución es más fuerte en el nivel de los saldos operativos: inventario de exchanges, saldos de liquidación de brokers, flotantes de pagos y fondos de rotación empresarial. Se debilita en el nivel de financiación bancaria mayorista, donde los depósitos a plazo, certificados de depósito y préstamos interbancarios construyen una estructura de plazos.

En los swaps de divisas, apenas tiene presencia: los compromisos a plazo y la capacidad de balance transmmonetaria generan conjuntamente financiación en dólares, y el token a la vista no tiene ningún papel. En el nivel del dealer, la stablecoin puede ser un activo elegible, pero sigue sujeta a las restricciones que realmente importan: capital, capacidad de liquidación, límites de contraparte, inventario de garantías. No sustituye ninguna de estas restricciones.

Una stablecoin aceptada como garantía puede respaldar un pasivo adicional en dólares. Pero hasta que otro balance esté dispuesto a financiar, renovar o mantener ese pasivo a un valor cercano al nominal, seguirá siendo sólo crédito garantizado.

3. Un saldo en dólares no crea capacidad de balance en dólares

El sistema del dólar extraterritorial sirve a dos necesidades distintas.

Una es la necesidad de "saldos en dólares": un pasivo que se puede almacenar y transferir para pagos. Las stablecoins encajan bien en esta necesidad donde la fricción en las transferencias es la principal restricción.

La otra es la necesidad de "capacidad de balance en dólares": la capacidad de obtener financiación, margen, cobertura o transformación de plazos. Esta capacidad reside en bancos, dealers y fondos. Consume capital, liquidez y límites de contraparte, y se retira cuando las condiciones se endurecen.

Hay una tercera necesidad, por encima de las dos anteriores: la necesidad de un tipo de pasivo que otros balances estén dispuestos a tratar como un activo cercano al valor nominal, sin tener que auditar la garantía subyacente desde cero cada vez. El usuario necesita un saldo en dólares. Los fondos apalancados necesitan capacidad de financiación. Y los pools de efectivo o los proveedores de fondos de segunda capa necesitan un pasivo que puedan mantener a un valor cercano al nominal. El canal de garantías sólo importa realmente cuando toca esta tercera necesidad.

Tres pruebas distinguen estos niveles.

Transferibilidad. El tenedor puede transferir este pasivo en dólares. Las stablecoins pasan esta prueba fácilmente.

Capacidad de financiación. Un intermediario está dispuesto a prestar, proporcionar margen o otorgar crédito contra este pasivo. Las stablecoins sólo pasan esta prueba bajo restricciones de elegibilidad, control y descuento.

Aceptación monetaria. Si el pasivo creado por ese intermediario puede, a su vez, ser financiado o mantenido a un valor cercano al nominal. Las stablecoins sólo adquieren significado sistémico en este paso.

La sustitución a nivel corporativo también sigue este gradiente: más fuerte para el inventario de liquidación, más débil para la banca relacional. Un saldo en tokens puede sustituir la parte de los depósitos operativos utilizada para transferir valor. Pero no sustituye nada de lo que hay detrás de la mayoría de las posiciones de efectivo corporativas: líneas de crédito, límites de divisas, bancos corresponsales, proveedores de liquidez intradía, interfaces de cumplimiento de sanciones, relaciones crediticias.

Los tokens transfieren pasivos. Los balances proporcionan elasticidad.

4. De la elasticidad del depósito a la elasticidad del descuento

En el canal extraterritorial tradicional, la elasticidad se origina en un pasivo bancario.

(Banco extraterritorial)

El depositante posee un pasivo cuasi-monetario, y el banco obtiene fondos utilizables. La elasticidad nace en el lado del pasivo de un balance expansible.

La emisión de stablecoins produce una estructura más estrecha.

(Emisor de stablecoin)

El tenedor obtiene un pasivo transferible, el emisor posee las reservas. Mientras el emisor se mantenga "estrecho" (narrow), no se crea un segundo pasivo privado en dólares: sólo cambia la forma y ubicación del primer pasivo.

El canal garantizado comienza cuando el token se utiliza para obtener financiación. El descuento determina cuánta financiación puede soportar el token controlado:

X = V_token × (1 − h)

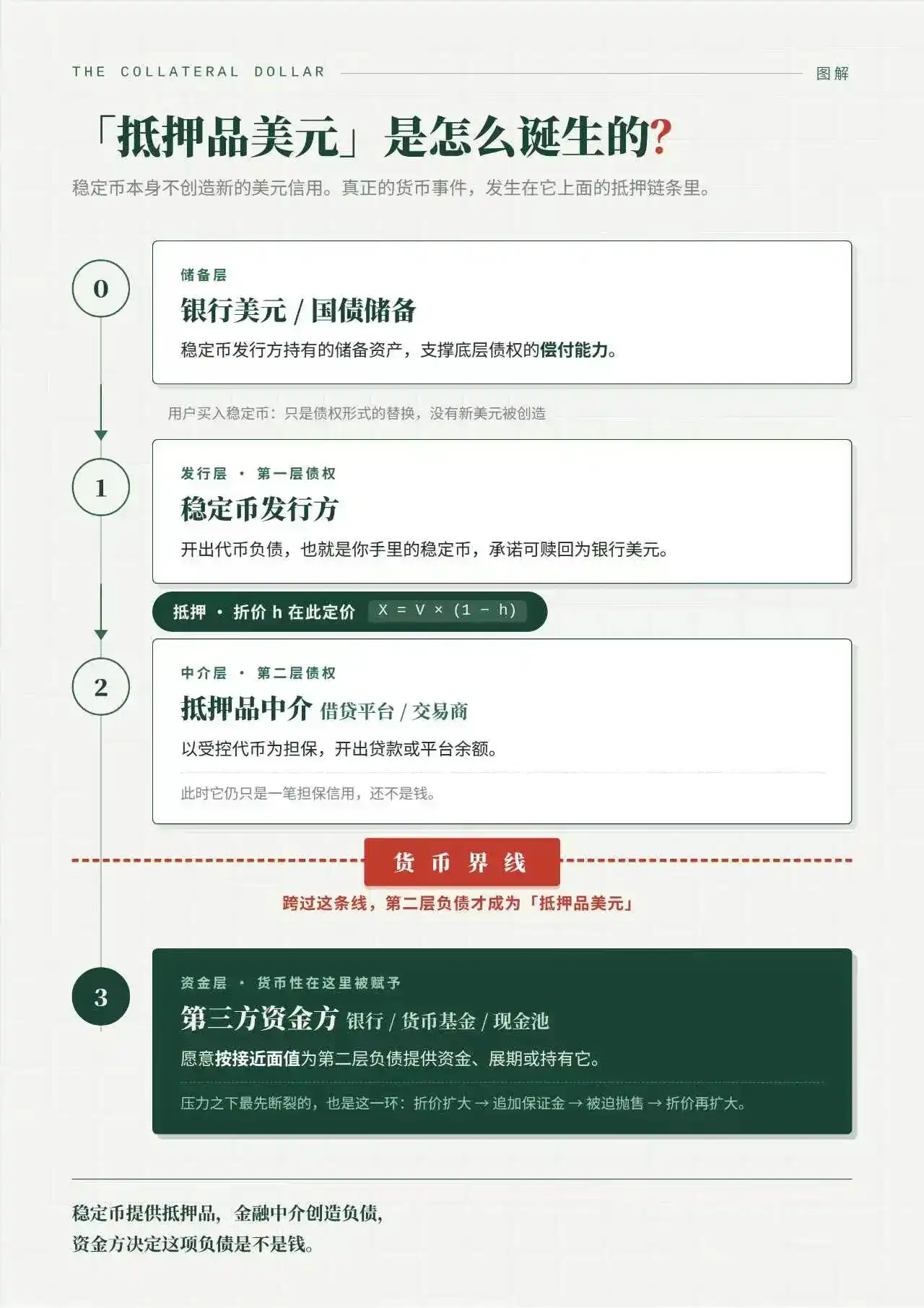

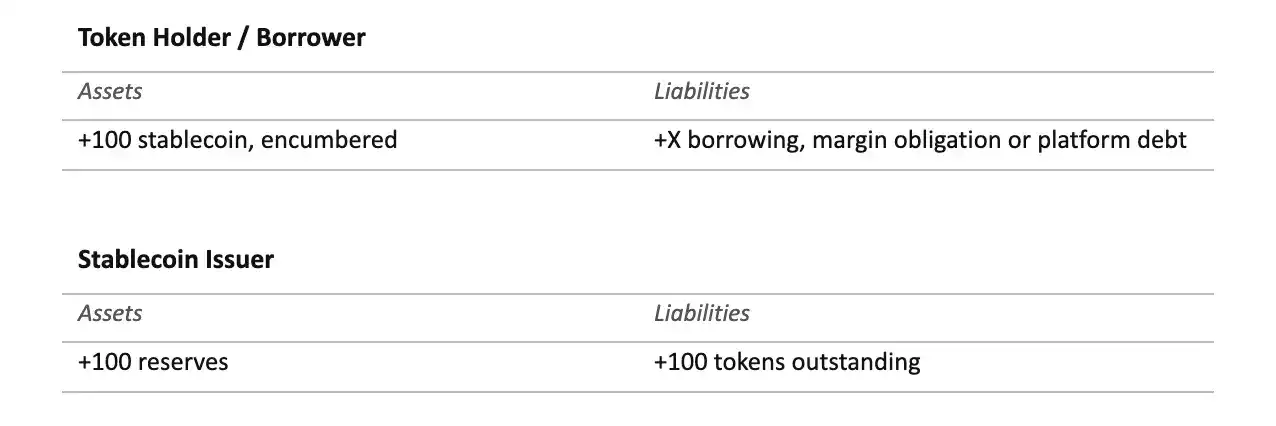

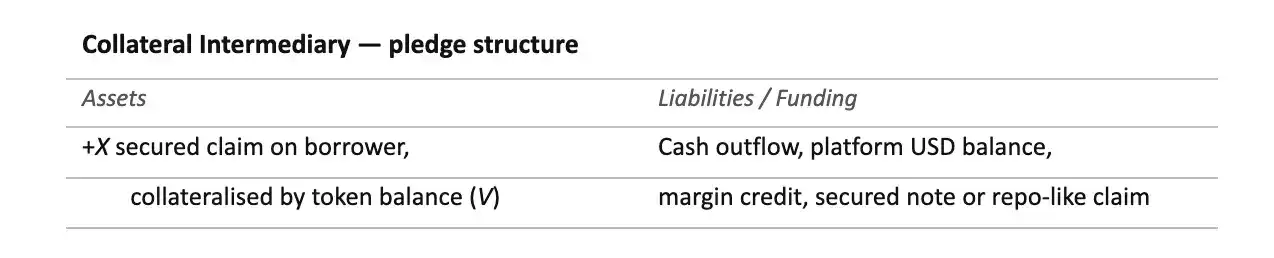

Donde X es la capacidad de financiación de segunda capa, V_token es el valor de mercado del token controlado, y h es la tasa de descuento. La contabilidad aquí debe distinguir cuatro balances.

La situación del intermediario de garantías depende de la forma legal del control. La prenda (pledge) y la transferencia de propiedad (title transfer) no son el mismo balance.

(Intermediario de garantías: estructura de prenda)

En una estructura de prenda, el prestatario sigue siendo el propietario del token. El intermediario no posee el saldo total de tokens; posee un crédito garantizado por un monto X, y tiene control o derechos de ejecución sobre la garantía con valor V. Su exposición en el balance es X, y la protección legal cubre V. La garantía excedente V − X sigue perteneciendo económicamente al prestatario, a menos que los mecanismos de incumplimiento y liquidación establezcan otra distribución.

(Intermediario de garantías: estructura de transferencia de propiedad)

En una estructura de transferencia de propiedad, el intermediario posee el token en sí. Suponiendo que el token vale 100 y el préstamo es 90, el intermediario controla el saldo total de 100 tokens, mientras que el prestatario retiene el excedente económico a través del derecho a "recuperar una garantía equivalente o el valor residual después del reembolso".

El control legal total del intermediario es V, y su exposición económica neta es X. La diferencia V − X no es patrimonio disponible libremente. Es la protección residual del prestatario, incrustada en la obligación de "devolver una garantía equivalente o liquidar el excedente tras la liquidación".

Si este préstamo se financia con efectivo existente, el intermediario no necesariamente expande su pasivo; simplemente intercambia efectivo por una exposición garantizada o una exposición por transferencia de propiedad. Si el préstamo se financia mediante la emisión de saldos en plataforma, pagarés, pasivos tipo repo u otros pasivos a corto plazo, entonces el intermediario expande su balance.

Por lo tanto, la cuestión monetaria no se detiene en si hay transferencia de propiedad. Depende de cómo se financie el préstamo en sí, y de si el pasivo resultante es aceptado a un valor cercano al nominal.

Esta distinción es importante porque sus mecanismos de estrés son diferentes. En la prenda, la ejecución del prestamista depende de sus derechos de perfeccionamiento, prioridad y realización sobre una garantía que aún está asociada al prestatario. En la transferencia de propiedad, el intermediario puede tener un control más fuerte, capacidad de repledging (reutilización como garantía) o derechos de realización, pero también carga con una obligación más clara: una vez cerrada la exposición garantizada, debe devolver una garantía equivalente o su valor.

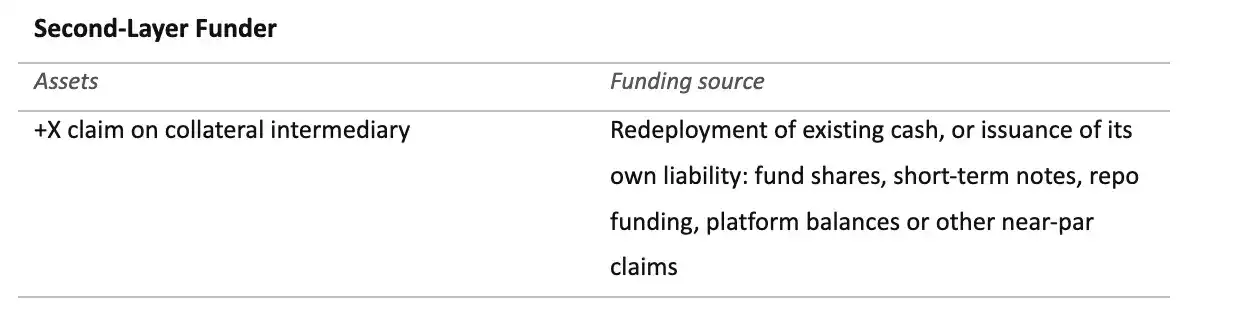

(Proveedor de fondos de segunda capa)

La elasticidad monetaria es más fuerte en el segundo escenario: el proveedor de fondos financia este crédito emitiendo su propio pasivo cercano al valor nominal. En el primer escenario, el sistema simplemente reasigna el efectivo existente a un crédito respaldado por tokens, y la cantidad de pasivos privados en dólares no necesariamente se expande.

La emisión por sí misma no crea nada más allá del token. El crédito garantizado adelanta valor contra el token. Sólo cuando el crédito del prestamista se convierte en un activo que otro balance financia a un valor cercano al nominal, se cruza esa línea hacia la creación monetaria. El paso del préstamo garantizado a la creación monetaria ocurre aquí, nunca antes.

El descuento marca el precio de la distancia entre el "control efectivo sobre el token" y su "conversión fiable a dólares bancarios", transformando el valor de la garantía en capacidad de financiación. Y la elasticidad en sí proviene del pasivo emitido contra el token, y de la disposición de otro balance a financiar ese pasivo a un valor cercano al nominal.

5. Condiciones institucionales del canal de garantías

Cuatro condiciones determinan si un pasivo de segunda capa puede ser financiado a un valor cercano al nominal.

Control legal. Tener una posición prioritaria y ejecutable sobre el prestatario, sus acreedores, custodios, plataformas y cualquier patrimonio concursal interviniente. Frente al emisor, las preguntas son diferentes: elegibilidad para el canje, transferibilidad, derechos de congelación, estado de la cuenta, riesgos de listas negras y el estatus legal del crédito del tenedor del token. El prestamista debe saber si el arreglo es una prenda, transferencia de propiedad, control de custodia, bloqueo por contrato inteligente o un pasivo de plataforma híbrido. Cada forma otorga derechos diferentes en caso de incumplimiento.

Control operativo. La ruta de realización (venta) y la ruta de canje deben distinguirse. La realización depende de la profundidad del mercado secundario, el balance de los market-makers y el acceso a las casas de cambio. El canje depende de las reglas del emisor, las listas blancas, el banco de liquidación, el horario bancario y el momento del canje. Un descuento que trata estas dos rutas de salida como equivalentes no es riguroso.

Rigor del descuento. El descuento debe cubrir: riesgo del emisor, composición de las reservas, acceso al banco de liquidación, elegibilidad para el canje, estructura de custodia, ejecutabilidad legal, profundidad del mercado, finalidad on-chain, derechos de pausa operativa, riesgo de deterioro conjunto (wrong-way risk) con el prestatario, concentración de market-makers y tiempo necesario para convertir el token en dólares bancarios.

Persistencia de la financiación. Un tercero está dispuesto a financiar el crédito del prestamista sin tener que auditar desde cero el token, el prestatario y la ruta completa de realización en cada ocasión. La comodidad del prestamista original con la garantía nunca es el criterio. Mientras cada proveedor de fondos tenga que analizar individualmente cada préstamo garantizado, el resultado es crédito bilateral garantizado, no un pasivo cercano al valor nominal.

La financiación cercana al valor nominal está ligada al plazo. Un crédito que se puede pedir prestado a un día no es lo mismo que uno que puede soportar retrasos de canje de varios días, retiradas periódicas de fondos o corridas de inversionistas. La monetaridad no es sólo una cuestión de precio, también de momento.

La verdadera prueba es: una vez que el prestatario, el emisor, el custodio, la casa de cambio y el banco de liquidación se convierten cada uno en fuentes de riesgo independientes, si el pasivo emitido contra el token sigue siendo un activo cercano al valor nominal. Que el token pueda usarse como garantía es la parte más fácil.

6. Transmisión del estrés en el canal de garantías

El estrés en el sistema del dólar extraterritorial se manifiesta como un movimiento ascendente en la estructura jerárquica. Las contrapartes más débiles pierden financiación. Los prestamistas de repos amplían los descuentos. Los dealers comienzan a racionar su capacidad de balance. Los pasivos que antes se trataban como cuasi-efectivo ahora necesitan apoyo de liquidez explícito.

En un canal de garantías construido sobre stablecoins, primero fallan los pasivos superiores. El token subyacente es la promesa del emisor de "canjear por dólares bancarios". El pasivo de segunda capa es la promesa del intermediario de "proporcionar liquidez cercana al valor nominal, respaldada por ese token". El primero puede seguir siendo solvente, el segundo ya ha perdido su estatus cuasi-monetario.

En condiciones normales, el token cotiza a la par, los descuentos son bajos, los intermediarios otorgan crédito con normalidad y el pasivo de segunda capa se trata como cuasi-efectivo. Nadie prueba simultáneamente la ruta completa de realización y la ruta de canje. La fragilidad reside en la capa que está sobre el emisor.

Lo que primero se rompe suele ser un ajuste en los términos de la garantía, mucho antes de que ocurra cualquier corrida sobre el token. Un prestamista aumenta el descuento, el prestatario recibe una llamada de margen. Un prestatario que no tiene efectivo ni puede aportar garantía adicional obliga al intermediario a realizar, canjear o financiar internamente esa posición. El pasivo de segunda capa se vuelve inmediatamente muy consumidor de balance.

La aritmética aquí es implacable. Un saldo de tokens financiado con un descuento del 2% puede respaldar 98 de crédito:

100 × (1 − 0.02) = 98

Con un descuento del 15% y un precio de mercado secundario de 99 centavos, el valor prestable cae a 84.15:

99 × (1 − 0.15) = 84.15

Los 13.85 que faltan tienen que venir de algún lado:

98 − 84.15 = 13.85

Ya sea una llamada de margen adicional, una venta forzada, un uso interno de fondos, o un pasivo de segunda capa que se rompe.

Esta fórmula estática mide la primera pérdida de capacidad de financiación. El mecanismo real de estrés es dinámico. V_token y h no son variables independientes. Un descuento mayor reduce el valor prestable y desencadena llamadas de margen que pueden forzar la venta de tokens. Las ventas forzadas deprimen aún más el precio de mercado secundario del token. Un precio más bajo, a su vez, "justifica" un aumento mayor del descuento, creando así un nuevo déficit de fondos.

X_t = V_t (1 − h_t)

Para cambios pequeños:

ΔA ≈ (1 − h_t) ΔV − V_t Δh

Bajo estrés, estos dos términos se mueven en la misma dirección. Δh aumenta porque los prestamistas exigen más protección; ΔV disminuye porque el propio proceso de llamadas de margen está generando presión vendedora. Por lo tanto, el descuento no es sólo una medida del riesgo, puede convertirse en un mecanismo de transmisión del riesgo.

La ruta de realización transforma un problema de financiación en un problema de profundidad de mercado. La ruta de canje lo transforma en un problema de canales bancarios. La financiación interna lo mantiene como un problema de capital del intermediario, que es donde se vuelve costoso. Transferir el crédito a otro proveedor de fondos sólo funciona si el crédito sigue cotizando a un valor cercano al nominal.

La salida de un dealer o plataforma retira a una institución que previamente había estado "almacenando" el desfase temporal entre la realización y el canje, transformando la garantía en financiación cercana al valor nominal. Esto no es lo mismo que una disminución de la liquidez. Una vez que este almacenamiento se detiene, la estructura jerárquica reaparece inmediatamente.

A diferencia del sistema maduro del dólar extraterritorial, la cadena de garantías de stablecoins no tiene un mecanismo establecido de "último dealer" o una arquitectura de líneas swap de bancos centrales para los pasivos emitidos sobre los tokens. El token subyacente puede tener reservas. El pasivo de segunda capa sólo tiene su propio mercado de financiación.

La calidad de las reservas respalda la solvencia del pasivo subyacente, pero no garantiza nada sobre la "liquidez a valor nominal" una vez que fallan los canales de canje, el banco de liquidación o la profundidad del mercado secundario. El emisor puede tener reservas adecuadas y, al mismo tiempo, el sistema crediticio construido sobre ellas puede colapsar.

7. Conclusión

La analogía con el eurodólar sólo es válida hasta cierto punto. Una stablecoin es un pasivo privado en dólares tokenizado que, incluso si el emisor y las reservas permanecen dentro de los límites legales de EE.UU. o dependen de infraestructura bancaria y de liquidación conectada a EE.UU., su uso puede volverse extraterritorial en sustancia económica.

La calidad de las reservas respalda la solvencia del pasivo subyacente. El apalancamiento, margen, crédito de plataforma y pasivos garantizados construidos sobre ellas responden a otro conjunto de pruebas.

La elegibilidad como garantía no alcanza la aceptación monetaria: hasta que el crédito del prestamista se convierte en un activo cercano al valor nominal para otros, un préstamo respaldado por tokens sigue siendo sólo un préstamo.

El canal de depósitos del sistema del eurodólar comienza con un pasivo bancario y se expande a través de la creación de depósitos, la financiación interbancaria y los mercados de dólares a plazo. El canal de garantías de las stablecoins comienza con un activo tokenizado controlado, y sólo se expande cuando un intermediario emite un pasivo contra ese token y otro balance trata ese pasivo como algo similar al dinero.

El emisor maneja la promesa subyacente, el intermediario de garantías emite la segunda promesa, y los proveedores de fondos deciden si esta segunda promesa tiene atributos cuasi-monetarios. El descuento marca el precio de la distancia entre el "control del token" y su "conversión a dólares bancarios". Y bajo estrés, lo que primero se amplía es precisamente esta distancia.

El dólar de garantía sólo existe realmente cuando el crédito construido sobre la stablecoin sobrevive al salto de la "liquidez del token" a la "liquidez en dólares bancarios".