前言

由于分片技术搁置,以太坊 2.0 升级最令人期待的就是共识机制从 PoW 变更为 PoS。尽管合并会带来诸多好处,譬如节约能源、使 ETH 进入通缩、为进一步扩容打下基础,但 PoW 共识机制下的矿工何去何从仍然是必须要面对的问题。日前,随着合并临近,以太坊硬分叉的预期也越来越强。本文将介绍 PoS 合并进展以及以太坊后续发展路线,并对目前备受关注的、可能会发生的硬分叉各方力量抗衡。

本系列第一篇《进击的巨人:深入浅出,玩转以太坊 PoS 合并》分析了以太坊 2.0 出现的始末,合并后矿工职能转变,以及各方参与者的变化。

01

合并进展与以太坊后续发展路线

Merge 的现状与历史进程

7 月 14 日,以太坊核心开发者 Tim Beiko 在电话会议上表示,预计以太坊的共识算法迁移到 PoS 的合并升级实施日期为 9 月 19 日。合并并不是瞬时完成的,将持续 6 个月以上时间,在 2023 年上半年全部完成。

此前被广泛称为以太坊 2.0 第 0 阶段的 PoS 信标链于 2020 年 12 月上线,旨在管理协调扩展的分片和 PoS 网络质押,以太坊用户可以将其 ETH 锁定在智能合约中以帮助保护网络。截至 2022 年 8 月信标链 ETH 总质押数超过 1388W,验证者数量超过 40W 人。(数据来源:https://launchpad.ethereum.org/)。

以太坊基金会也在 2022 年 1 月宣布,将“ETH 2.0”更名为“共识层”。The Merge 将启用信标链作为以太坊出块的共识层网络,将信标链(共识层)与现存主网(执行层)合并,进而完成共识机制从 PoW 到 PoS 的转变。

此前,以太坊合并公共测试网 Kiln 于 2022 年 3 月上线,最终成功的过渡升级到了 PoS 共识机制。之后,以太坊测试网 Ropsten 和 Sepolia 先后成功合并,以太坊最后一个测试网Goerli 也将于 8 月 11 日进行合并。

为什么要使用 PoS

此次合并,将大大减少以太坊的能源消耗和碳排放,预计将使得以太坊的能源消耗减少 95% 以上。同时 PoS 也将为网络提供更高的安全性,V 神在《为什么要进行 PoS 》一文中论述道:

PoW 中攻击网络的成本仅仅是租用足够的 GPU 赶超现有矿工的成本,只需要花费少量的成本和时间就可以进行攻击工作。而在权益证明中,几乎全部是资本成本,即运行节点的成本。随着质押率的提高,攻击成本预计非常高。

在 PoW 网络中,如果遭到 51% 攻击,唯一的应对措施就是 “等到攻击者主动撤销攻击"。PoS 的情况会好很多,对于某些类型的 51% 攻击(特别是回滚最终确定的区块),在权益证明中有一个内置的惩罚机制,通过这个机制,攻击者的大部分质押(并不包括其他人的)将被自动销毁。

此次合并升级也是为之后的分片链上线做准备。分片链的验证者将由信标链随机分配,一条分片链上的验证者难以进行串谋作恶,据以太坊团队介绍,作恶的可能性小于万亿分之一,分片链的安全得以保障。

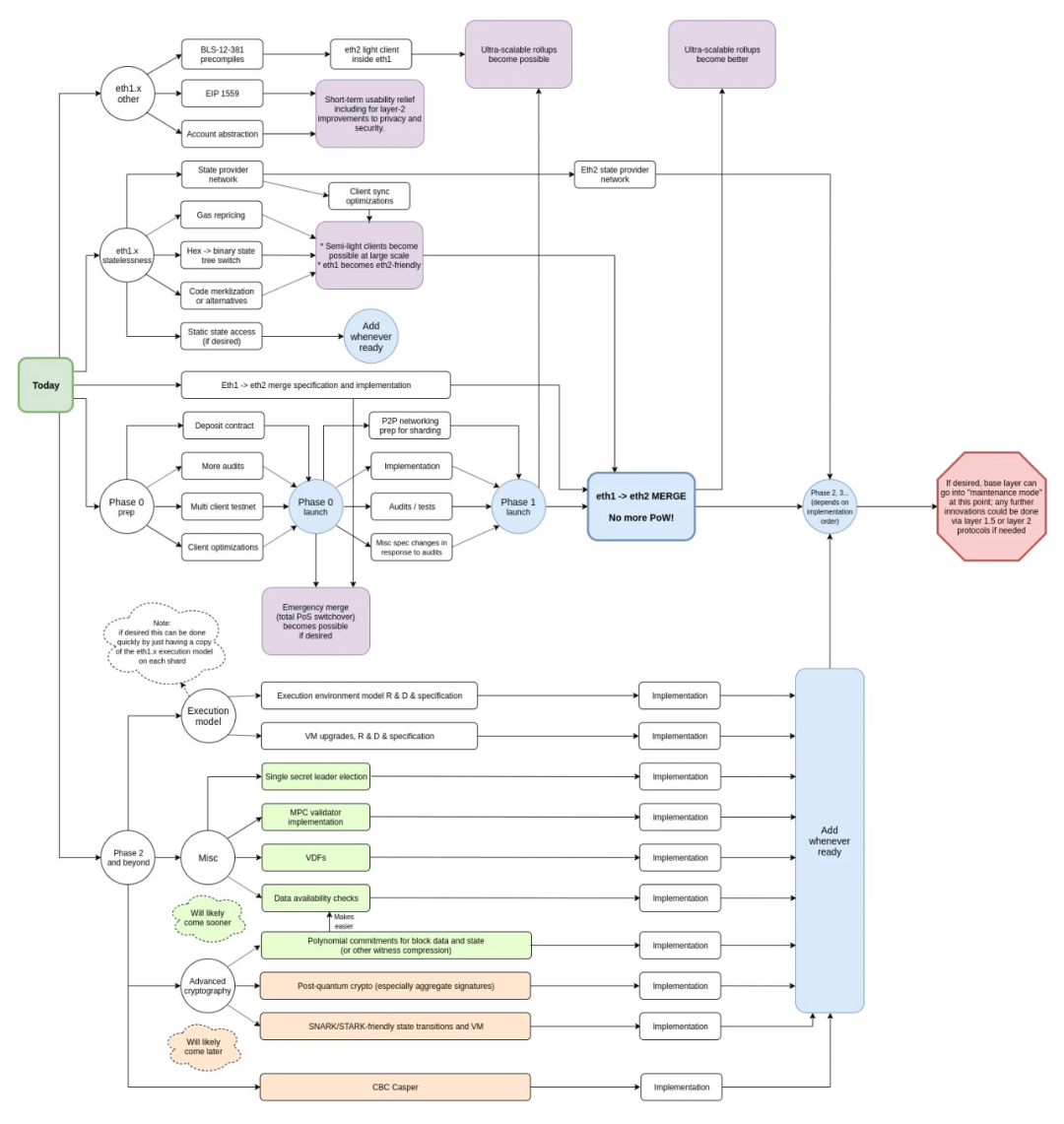

以太坊后续发展路线图

合并仅仅是以太坊全面升级的开始,V 神在参加以太坊社区会议(ETHCC)时,也介绍了以太坊未来发展路线图。

The Merge :实现后将使 ETH 成为通缩性资产,并减少 99% 的能源消耗。

The Surge :预计 2023 年合并完全实现后启动,在以太坊上引入分片,进而显著提高网络的可扩展性。

The Verge:引入 Verkle 树,优化以太坊上的存储并帮助减小节点大小,进而帮助 ETH 提升可扩展性。

The Purge :减少验证者所需的硬盘空间。消除历史数据和坏账。通过存储简化减少网络拥塞。

The Splurge :确保网络在前 4 个阶段之后平稳运行。

Vitalik 也表示,Merge、Surge、Verge、Purge 和 Splurge 这五个不是分阶段,而是同时发生并推进的。这个路线图全部实现后,以太坊将成为一个更具可扩展性的系统,能够每秒处理 100,000 笔交易。

02

价值 190 亿美元 PoW 矿工去向:分叉 or 转向 ETC

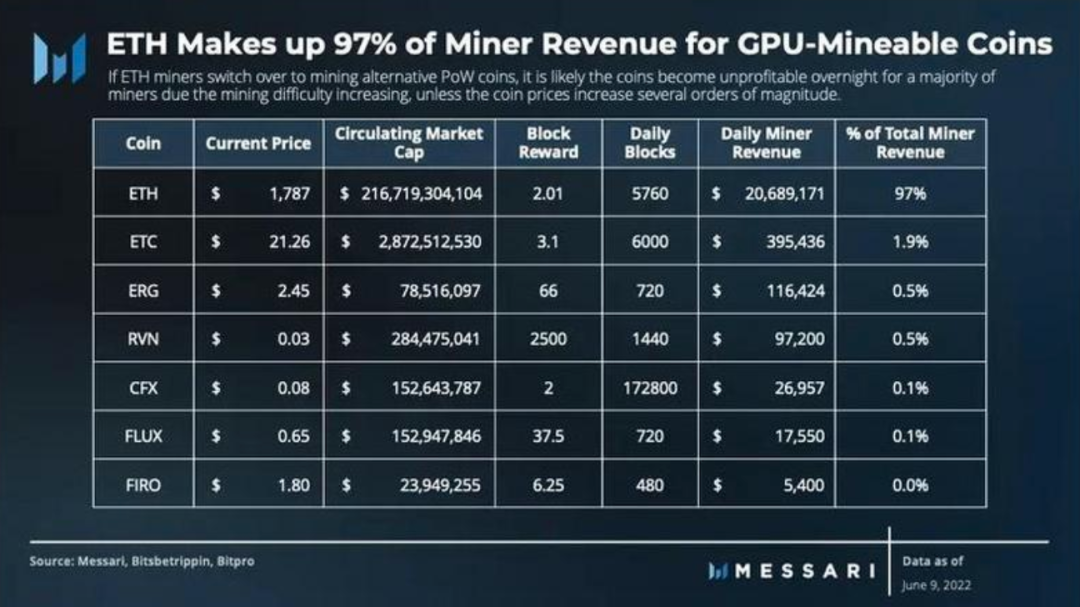

以太坊合并(The Merge)将迫使价值 190 亿美元的 PoW 挖矿从业者另谋出路。大多数现有的以太坊矿工无法在市场上找到具有同等经济效益的 PoW 矿币。除 ETH 之外的 GPU 可开采代币的总市值为 41 亿美元,约占 ETH 市值的 2%。ETH 挖矿收益占 GPU 矿工日收入的 97%。

以太坊矿机分为两种:ASIC 和 GPU。ASIC(专用集成电路)是为特定目的而设计的计算机硬件,以太坊 ASIC 矿机中编写了适用于以太坊的哈希算法。GPU 矿机可以解决复杂的 PoW 计算,也可以用于更通用的应用程序。

可以看出,合并后对于 ASIC 矿机来说影响是巨大的,因为他们除了转向以太坊经典(Ethereum Classic)外,似乎别无他路。而相对于 GPU 矿机来说,情况似乎会稍好一些,那 GPU 矿机有哪些去向呢?Messari 分析了大量 GPU 矿机的再利用方案之后,得出了以下几个可行方案:

挖掘其他 PoW 代币

提供高性能计算的数据中心

为 Web3 协议提供计算

出售矿机并质押已挖出的 ETH 参与 PoS

挖掘其他 PoW 代币,如 ETC

矿工从挖取 ETH 转向其他 PoW 代币的问题在于,这些代币的市场规模远不及以太坊。截至 6 月 9 日,除以太坊之外的 GPU 可开采代币总市值为 41 亿美元,约占以太坊市值的 2%。

由于哈希率不能用于比较具有不同哈希算法的网络的计算能力,因此矿工总收入成为下一个最佳方法。在矿工收入排名前七的 GPU 可开采代币中,以太坊占 GPU 矿工总收入的 97%。以太坊经典占 GPU 矿工总收入的 1.9% 而位居第二。这表明没有以太坊的 GPU 可开采代币市场规模之小。

ETC 算力是25 TH/s,ETH 是924 TH/s,大概是 1:37。而现在 ETC 价格是 32,ETH 价格是 1600,大概是 1:50。如果算力转到 ETC,回本周期会非常长。ETH 显卡矿机耗电没有比特币那么厉害,所以关机币价没有 BTC 那么高,但是挖 ETC 的竞争会非常激烈。

以太坊分叉

在加密行业的历史长河中,我们对区块链网络进行分叉并不陌生,出现分叉的原因多种多样,可能是技术原因、价值观差异等,比如著名的 BTC 和 BCH 分叉、以太坊和以太坊经典分叉等。

与上述分叉相比,此次以太坊合并升级后进行分叉所面临的挑战更多,比如 BTC 主要用于转账支付领域,导致其分叉只需要得到矿工支持即可,即所谓的“算力之争”。作为智能合约公链之王,目前以太坊生态已形成一定规模,其分叉将涉及成千上万个 Dapp 与协议,以及链上数百亿美元的基础资产,所以此次分叉将是整个生态的选择,其复杂度远超过此前任何一次分叉。

单来说,比如以太坊升级后分叉出一条 PoW 机制的区块链 ETH-PoW,那么以太坊生态上的 Dapp 和协议就需要做出选择,而不同 Dapp 和协议之间又是相互关联和嵌套,比如无聊猿等 NFT 项目都需要 NFT 交易平台、DeFi 协议均需要预言机等,那么前者的站队必然跟随后者。同时 DeFi 已经成为整个 Web3 世界的基础设施,也占据整个生态的半壁江山,绝大部分链上活动最终都会依赖于交易、借贷等 DeFi 协议,所以 DeFi 协议的选择也将对其它领域的应用产生重大影响。

8 月 5 日,以太坊创始人 Vitalik Buterin 在 BUIDL Asia 活动上表示,USDT、USDC 等中心化 Stablecoin 可能将是「未来硬分叉的重要决定因素」。

从以太坊经典网络的发展历史来看,失去 V 神这一精神领袖,以及以太坊核心开发者社区的支持后,其生态一直停滞不前。如果以太坊升级后,矿工们分叉出 ETH-PoW 链,那么在没有 V 神和其他以太坊核心开发者的支持下,ETH-PoW 链能走多远,将是一个疑问。在以太坊经典这个前车之鉴下,以太坊上丰富的生态和资产有多少是敢于“豪赌”一把呢?

以数据中心为导向的业务

以太坊矿工的规模从拥有小型矿机的个人矿工发展到经营拥有数千台矿机并公开上市的大型矿企。虽然小型矿工可能会在 以太坊合并之后轻松转型,但对于在挖矿硬件、专用仓库和电力相关基础设施方面大量投资的大型矿工来说,做出下一步决定将非常困难。

Hut 8 和 HIVE Blockchain 是已经公布了其在以太坊合并后战略的两家大型公开上市矿企。Hut 8 和 HIVE Blockchain 都表示,将过渡到高性能计算行业。两家公司都收购了数据中心业务,以便重新定位企业以实现转型。这些数据中心旨在为亚马逊等云计算巨头提供网络服务的替代方案。

Hut 8 和 HIVE Blockchain 大量投资了用于挖掘以太坊的高性能 GPU 显卡,这使它们能够重新将 GPU 显卡用于提供高性能云计算服务。Hub 8 将其 GPU 描述为“GPU 中的法拉利”,他们是 NVIDIA 的三个重要客户之一。Hut 8 专门针对 Web3 行业的项目,为其提供区块链基础设施、游戏渲染和 NFT 存储等云托管服务。

随着游戏、人工智能和电影动画的蓬勃发展,对高性能计算的需求将继续增长。一旦以太坊合并发生,这种增长是大型矿工获得大量新收入来源的机会。

为 Web3 协议提供算力

Web3 的目的是在开放、去中心化和无需许可的协议上重建互联网。为了实现这一点,需要建立分布式的基础设施作为基础层。这包括为视频流应用程序构建基础架构、2D 和 3D 对象的渲染以及云服务器。这些服务的共同点是它们依赖于分布式参与者网络来提供 GPU 算力服务。

矿工可以将其 GPU 算力转向少数 Web3 协议,包括:

Render Network:分布式 GPU 算力市场,允许用户为渲染贡献算力。该网络允许 GPU 矿工将其渲染能力出售给任何有需要的人,例如艺术家、设计师和研究人员。

Livepeer Network:处理视频流媒体的去中心化网络,该网络依靠矿工使用 GPU 提供视频转码服务。

Akash Network:去中心化的云算力市场,为具有额外算力的提供商和寻求算力的用户提供合作平台。Akash 的目标是在 2022 年第二季度将 GPU 市场集成到其平台,使网络能够处理机器学习、人工智能和云游戏等数据密集型的工作负载。

这些 Web3 协议将欢迎 GPU 矿工寻找新的安身之所。值得注意的是,某些协议(例如 Akash)会设置额外的硬件资本门槛才能让矿工成为算力提供商。这个解决方案不仅对小型矿工开放,也对大型矿工开放。

过渡到 PoS 质押

从挖矿中积累了 ETH 的矿工可以选择出售其 GPU 矿机并成为以太坊 PoS 验证者节点。网络要求验证者至少质押 32 枚 ETH 才能运行验证者节点。作为验证交易的回报,验证者以区块奖励、倾斜激励和 MEV 的形式获得奖励。根据质押者的数量和网络活动的水平,收益率可能在 7% 到 13% 之间。对于没有 32 枚 ETH 或不想承担运行验证节点风险的矿工,也可以通过 ETH 2.0 质押服务商参与质押。

小结

在以太坊成功合并主网后,PoW 代币的 GPU 挖矿市场可能会急速萎缩。随着矿工意识到开采其他 PoW 代币只会让少数能够获得廉价能源的矿工保持盈利,那么大部分 GPU 矿机将在二级市场上转售。愿意投入时间和资金的矿工将能够过渡到高性能的数据中心运营商或 Web3 算力协议的节点提供商——这两个市场都在快速增长。

a16z 的交易合伙人 Elena Burger 提醒我们,大多数新技术的进步都需要硬件支撑。“科技领域的所有主要行业——从云计算到计算机图形学、人工智能和机器学习——都已经遇到发展瓶颈,需要更快计算速度和更高效率的硬件。” 虽然以太坊合并似乎是 GPU 挖矿的终结,但它也可能会开启另一个时代,因为流离失所的矿工会在 Web3 中寻找新的机会。