合并或许是迄今为止以太坊网络升级最重要的「催化剂」之一,也将在多个方面影响网络,比如:

显着降低以太坊的能源消耗,减轻批评者对其环境影响的担忧;

在协议级别为以太坊网络优化扫清道路,包括分离「proposer-builder」,将区块生产与区块验证分开;

大大增加资产 ETH 的吸引力,因为 ETH 的发行量将减少约 90%,可能会导致通货紧缩,同时质押者也能获得收益。

那么对于更广泛的投资者来说,还有没有其他利用以太坊合并的投资机遇呢?这里我们给大家带来四个利用以太坊合并的投资策略——

1️、流动性质押 Token

示例:LDO、RPL、SWISE

流动性质押服务将会是以太坊合并最直接的受益者,预计在以太坊过渡到权益证明后的几个月内,非托管协议会经历一次显著增长。

实际上,流动性质押的理念非常简单,它允许用户同时进行以下所有三种操作:持续托管抵押品,获得质押奖励,通过发行流动性质押衍生品(LSD)部署 DeFi 资产。

由于以太坊通过合并可以消除此前的技术和执行风险,因此抵押风险大大降低,相应地也会推动一波协议的发展。

此外,以太坊在完成合并后也将有助于降低 LSD 交易中和 ETH 有关的折扣。目前,DeFi 流动性巨头 Lido 上的 stETH 价格约为 0.963 ETH,但在六月份 Cessius 开始暴雷时, stETH 价格曾一度出现脱锚,来到了 0.933 ETH 的低点。

预计在「上海」网络升级之前,信标链不会回撤,而是要等到合并后的 6-12 个月。不过,合并带来的影响是巨大的,由于折扣将会进一步减少,因此质押人承担的价格风险也会更小,从而使这些质押协议更具吸引力。

此外,由于预计质押收益率会增加,因此流动性质押协议中的抵押品也可能会增多。现在,信标链验证者仅仅只能获得区块奖励,而在合并之后,质押者可以通过 MEV 策略(指矿工或验证者根据其在以太坊区块链上确定交易顺序的能力从交易区块中提取的最大价值)获得交易费用和其它收入。预计这一转变将使质押收益率从目前的 4% 左右大幅提升到 6-12% 。

随着更高收益率以及更高 ETH 价格的到来,流动性质押协议的收益将会持续增加,质押者的收入也将进一步得到提升。

到目前为止,市场上共有三种支持公开交易 Token 的流动性质押协议,分别是: Lido(LDO) 、 Rocket Pool(RPL)和 Stakewise(SWISE)。

其中,不同 Token 在投资组合中扮演着不同的角色:

投资者如果寻求蓝筹敞口,那么可以选择 LDO ,因为它是信标链上最大的质押实体,拥有 31.2% 的质押份额。此外, Lido 在流动性质押行业拥有最大的控制权,占 90.3 % 的市场份额。目前,该 Token 的市值(MC)为 14.8 亿美元, 完全稀释估值(FDV)为 27 亿美元。

投资者如果比较看重 Token 经济学,那么可以关注下第二大流动性质押协议 Rocket Pool(RPL),它在信标链质押中占有 1.6% 的份额,在流动性质押行业占有 4.5% 的份额,市值为 4.6752 亿美元,完全稀释估值为 5.1973 亿美元。事实上, RPL 中蕴含着独特的 Token 经济学,这是由于迷你池的运营商或是通过 Rocket Pool 进行验证的实体需要为每个新验证器购买价值 1.6 ETH 的 RPL,因此 Token 需求与 RPL 增长就紧密地联系在了一起。

投资者如果想要最大化风险并且优化 beta 系数,则可以选择 StakeWise(SWISE),其市值为 2666 万美元,完全稀释估值为 1.9845 亿美元。虽然该协议的信标链和流动性质押份额分别只有 0.4% 和 1.3%,但由于其规模较小且浮动性较低,SWISE 可能是三者中 beta 系数最高的 Token。

2️、DeFi 投资

当然,购买 Token 并不是利用合并赚钱的唯一途径。精明的市场参与者可以通过 DeFi,以各种不同的方式来进行投资,以此反映出不同的市场在以太坊合并之前、之中和之后是如何做出反应的。

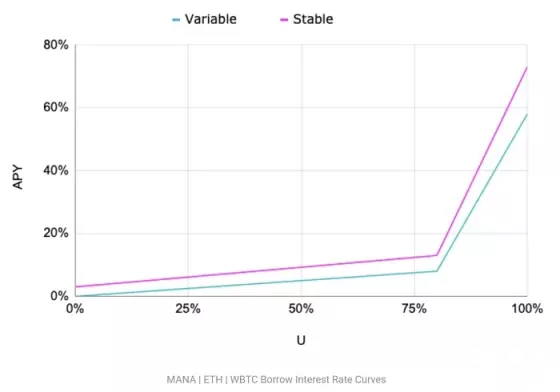

其中有一种方法就是在 Aave、Compound 和 Euler 等货币市场借出 ETH。这是由于投资者希望能够积累尽可能多的资产,以便在基于权益证明的以太坊分叉 (ETHPOW)中获得「空投」的机会,因此在以太坊合并期间,市场对于借入 ETH 的需求可能会大幅增加。

由于这些协议的利率是基于利用效率(比如借入了多少资产)的,借贷需求的大幅飙升将导致贷方的存款率非常高。我们看到 Aave V2 上 ETH 的利率曲线开始快速飙升。目前该市场的利用率为 61.56%,但自 8 月 8 日以来开始大幅飙升,并大有持续的趋势。

图源: Aave docs

当然,这种策略并非没有风险。在借贷需求非常高的极端情况下,这意味着 Aave 中几乎没有 ETH 流动性,在借款人偿还或更多存款涌入协议之前,贷方可能暂时无法提取资产。

另一个方法是使用 Voltz 协议,这是一种用于利率掉期的 AMM,旨在押注 LSD 抵押收益率。由于 Staking 的回报可能会在合并后增加,因此市场参与者可以使用 Voltz 通过将 ETH 作为保证金并购买可变利率 stETH 或 rETH Token,用户可以通过利用杠杆来放大他们的回报,但需要注意的是,这会带来更大的清算风险,使用任何形式的杠杆都要非常小心!

3、PoW 空投收益耕作

流动性挖矿中蕴藏着数十亿美元的「质押机遇」,几乎可以肯定的是,合并后以太坊仍会存在一些 PoW 实例,比如孙宇晨和交易所 Poloniex 等众多知名行业人士已经承诺支持这次硬分叉,并计划上架 ETHPOW Token。

虽然目前尚不清楚分叉链是否具有任何长期生存能力,也不知道 ETHPOW 未来能具有多少价值,但用户不必放弃这个「分叉机会」,至少可以多种不同的方式赚取看似大概率会有的空投(小贴士:获得空投资格的最简单方法是将 ETH 保存在非托管钱包中,比如 Metamask、Coinbase 等。)

如果您寻找更高风险的投资机会,这里有一种方法:在货币市场上借入 ETH,如果空投的价值大于借入 ETH 的成本,那么可能是有利可图的。不过,这种策略伴随着相当大的风险。借款利率不仅可能超过空投收益,而且一旦 ETH 价格飙升或抵押品价值下跌,借款人将会被清算。鉴于合并当天极有可能出现大幅波动,投资者需要非常谨慎地进行这种选择。

如果你害怕高风险,也可以在永续期货创建一个 ETH 头寸。在这种情况下,用户可以购买现货 ETH,同时在 CEX 或 DEX 上使用永续合约做空等量的 ETH。通过这种方式,用户既可以获得 ETH 投资敞口,又可以获得空投,同时不会承担持有资产带来的价格风险。如果空投的价值超过资金(保持持仓的成本),这种策略将是有利可图的。

然而,天下没有免费的午餐。这种策略的风险同样很大,因为融资收益略(如借贷利率)可能会随着合并事件而飙升。无论哪一种杠杆策略,加上波动性,都会使用户面临被清算的巨大风险。

所以,请谨慎行事。

4️、其他受益机会

事实上,合并后的以太坊有望对生态经济的其他领域产生变革性影响。

最先受益的应该是 Layer 2,PoS 过渡后,基本上能为以太坊网络可扩展性升级(例如 EIP-4844)铺平道路,终端用户的链上汇总交易费用将得到大幅降低,这意味着会有更多用户被吸引到网络上进行交易,同时也将推动更多 Dapp 创新——费用降低有助于「刺激」Layer 2 的普及应用。

在合并的大背景下,投资者可以(其实已经开始)投资整个 Layer 2 生态系统,比如 Layer 2 基础层(OP)、以及 Synthetix (SNX) 和 GMX (GMX) 等 Layer 2 原生 DeFi 项目,还有一些支持 Layer 2 的基础架构,比如 Synapse (SYN) 和 Hop Protocol (HOP) 等快速桥接服务。

合并后,另一个发生变化的领域将会是 MEV。随着「proposer-builder」逐渐分离,MEV 的竞争动态将发生巨大变化,这将使以太坊区块生产(决定哪些交易进入区块)和区块验证分开。MEV 领域中也有一些值得关注的项目,预计会在合并过程中有所突破,比如 Manifold Finance (FOLD)、 Rook Protocol (ROOK) 和 Cow Protocol (COW),这些 Token 在最近几周运行相当不错,未来也有望成为 PoS 以太坊的长期受益者。

结论:关注风险,做好研究,选择冒险

合并即将到来,毫无疑问,这将是以太坊发展道路上一次重要里程碑,也将给以太坊经济带来重大变化。

如果您担心风险,一个比较安全的方法是直接投资 ETH,但现在与 2018 年熊市有很大不同,我们生活在 DeFi 世界中,因此投资者可以通过多种其他方式参与合并,无论是通过投资 / 交易流动性质押协议、还是探索 Layer 和 MEV,或是使用 DeFi 赚取收益。

但无论选择哪种方式,请关注风险,做好研究,最后再选择冒险。