合并即将发生,以太坊将按预期转移到 PoS,可能会出现短暂的混乱,一切都会好起来的。

以太坊合并即将到来,可能会带来经济混乱。随着我们越来越接近合并,以太坊工作量证明(我们称之为 ETH POW)硬分叉的传言正在浮出水面。

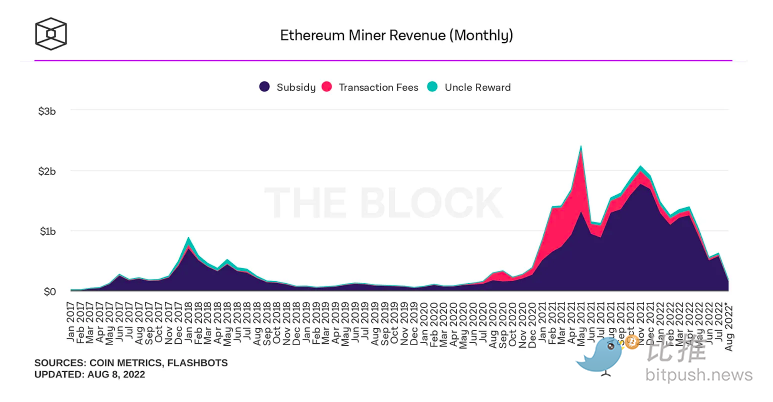

这有很多原因,以太坊挖矿是一个价值数十亿美元的行业,每月为硬件矿工创造数亿美元的收入(有时数十亿美元)。对他们来说,不幸的是,一旦合并完成,矿工就会变得无用。他们将为维持业务而奋斗,将分叉以太坊并推动 PoW 替代方案。事实上,这已经在发生了,已经有一个以太坊 PoW 阵营在 Twitter 上出现并发声。

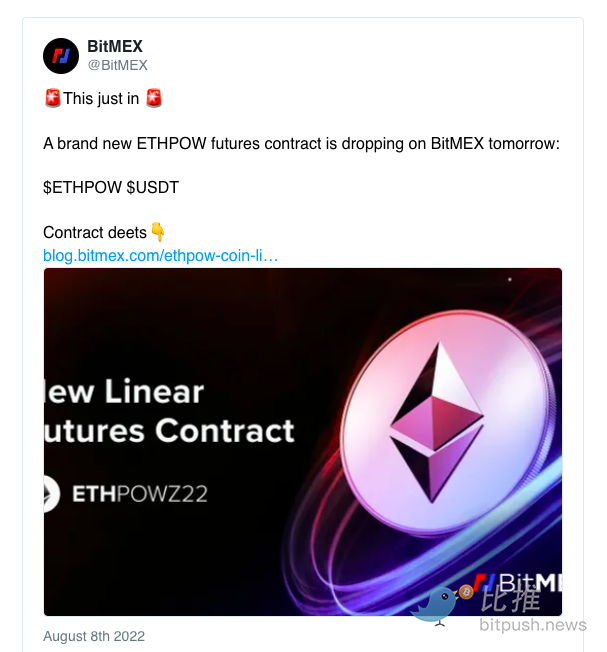

我们看到 Bitmex 在 ETHPOW 上推出了期货合约,让投资者可以推测这些代币的未来价格。以太坊 PoW 是否有价值是一个问题,但这个硬分叉确实为以太坊生态系统呈现了一种非常独特(并且可能是混乱)的动态。

为每个人免费赚钱

早在 2017 年,比特币出现了继比特币现金之后的无数硬分叉,其中相当一部分比特币社区不同意增加网络区块空间的 SegWit 提案。结果,比特币区块链被分叉,比特币持有者以 1:1 的比例收到每条新链的代币。

尽管这些链中的大多数已经变得无关紧要,但它们确实为比特币持有者创造了数十亿美元的财富。人们收到了这些具有市场价值的新代币,要么选择抛售他们新铸造的代币以换取更多 BTC,要么决定根据愿景继续持有它们。

因此,以太坊也会发生同样的事情,对吗?

合并后,每个 ETH 持有者将按合并时持有的每个 ETH 1:1 获得 ETHPOW 代币。

不过,以太坊和比特币之间有一个关键的区别。硬分叉比特币很简单,它只是存在于网络上的本地代币。

相比之下,以太坊有一个完整的经济基础。网络上有数千种资产和数百种协议。如果它是硬分叉的,那么从技术上讲,所有这些相同的代币和协议现在也存在于新的 PoW 链上,而不需要得到在其上构建的实体 / 社区的直接支持。

如果发生这种情况,可能会导致合并前后市场的大幅波动。

经济混乱

如前所述,当以太坊硬分叉时,网络上的所有内容都会被复制。

问题是,并非所有资产、协议或基础设施都将得到构建它的每家公司的支持。当然,你可以复制链上的代币和合约,但你不能复制支持它们的链下事物(人类、基础设施等)。

这里有两个主要的例子:

法币稳定币(USDC、USDT 等)

像 USDC 和 USDT 这样的法定稳定币将被一对一复制,就像其他所有代币一样。问题是,USDT 和 USDC 银行账户中的现金并没有翻倍,两家发行商都不会兑现 PoW 链上的任何稳定币。也许他们将来会,但会在 PoW 链上重新发行稳定币。

旧的稳定币代币将被扔进垃圾桶。你在以太坊 PoW 钱包中收到的所有 USDC 和 USDT 实际上都是毫无价值的。

鉴于 USDC 变得一文不值,DAI——一种由 40% USDC 支持的去中心化稳定币——也失去了大量支持它的抵押品。

流动质押代币(stETH、rETH 等)

另一个主要影响是流动性质押代币(Lido 的 stETH 和 Rocketpool 的 rETH)。

鉴于这条新的以太坊链打算永久运行在 PoW 上,ETH 质押将永远不会发生。

这将使以太坊 PoW 上数十亿美元的流动质押代币归零,因为它们实际上永远无法兑换任何东西。

这只是两个关键的例子,还有很多其他可能发生的事情。

那 DeFi 协议呢?哪些将支持 PoW 版本,哪些将继续与以太坊 PoS 保持完全一致?

您可以假设已经具有强大的多链协议将支持新的 PoW 链。但即使他们愿意,事情也会变得复杂,因为还有另一种代币(即 AAVE 和 AAVE-POW),其中 POW 代币实际上拥有网络协议的权利——无论是治理、经济还是两者兼而有之。

一个具体的例子是 Sushiswap。如果 Sushiswap-PoW 的交易量很大,那么 SUSHI-POW 持有者会从质押中获得收入,而不是 PoS 持有者。

鉴于 Sushiswap 的多链方法,这里存在一些冲突。根据 Sushiswap 的记录,他们肯定会支持 PoW 链并将所有收入分配给 xSUSHI 持有者。

相反,如果 Sushi 社区决定采用这个版本,现在必须有治理流程来解决这个问题。

多米诺骨牌开始倒下

这里出现的一个大问题是合并前后的 5-10 个区块。当数千亿美元的资本应该在一条链上归零,而不是在另一条链上时,矿商可提取价值 (MEV) 的数量是未知的。

将会出现混乱。

MakerDAO 依靠 USDC 来维持 DAI 的挂钩。

Aave 有数十亿美元的 stETH 被用作贷款的抵押品。

鉴于以太坊的可组合性水平,很容易想象会有大量的清算、波动和因此而发生的事情。

市场机遇

您可能想知道的问题是:「我怎样才能从混乱中获利?」

从表面上看,你可能正在考虑做空 USDC 或 stETH 或任何会失去价值的代币。

做空 stETH 或 USDC 并将您的任何抵押品置于风险之中可能是不值得的。未知数太多,您很可能会输给机器人。

为了利用潜在的分叉,最简单的方法就是在合并之前堆叠尽可能多的 ETH( 请以安全的方式 )。

这是因为虽然不清楚每个单独的代币在 PoW 链上的表现如何,但合法版本的 ETHPOW 可能会保留一些价值——至少在中短期内是这样。

很多人想摆脱以太坊 PoW 链。

如果有一个分叉成功地成为所有矿工的聚焦点,那么 Ethereum-PoW 网络将变得非常去中心化和安全,为用户提供高结算保证。

事实上,以太坊 PoW 链实际上将成为仅次于比特币和 Ethereum-PoS 的第三大安全区块链。这并没有使链本身具有价值,但它确实为它提供了重要的基础,特别是当它已经经过实战考验时。

以太坊工作量证明有着悠久的成功历史。在过去的 7 年里,它一直支持着数万亿美元的经济活动。我们知道以太坊 PoW 有效——这是有证据的。

因此,如果合并确实因任何原因失败,以太坊 PoW 将继续前进,不会失败。如果您有任何疑虑,几乎可以将 ETHPOW 视为对合并的对冲。

这是加密行业中前所未有的独特事件,有很多变量需要考虑。

合并即将发生,以太坊将按预期转移到 PoS,一切都会好起来的。可能会出现短暂的混乱。