Цена Ethereum снизилась на 18,5% за последние 30 дней и на 5,2% за неделю. Актив удерживает позиции немного лучше биткоина на недельном графике, но о восстановлении говорить рано. Ключевой ончейн-сигнал показывает, что у большинства трейдеров почти не осталось причин для фиксации прибыли.

В обычных условиях это способствовало бы формированию дна. Однако, если давление со стороны продавцов уже иссякло, возникает вопрос: почему цена Ethereum по-прежнему не демонстрирует отскок.

Стимулы к фиксации прибыли снизились. Но дно не подтверждено

Индикатор чистой нереализованной прибыли и убытков (NUPL) упал до 0,23. Это самый низкий показатель с 1 июля. NUPL отслеживает психологию инвесторов, измеряя объем нереализованной прибыли или убытков на рынке.

В последний раз NUPL опускался еще ниже 22 июня, достигнув 0,17. Это движение предшествовало ралли Ethereum на 106,3%, которое помогло индикатору перейти из фазы «капитуляции» в фазу «веры/отрицания».

Сегодняшнее значение (0,23) находится выше того минимума. Это означает, что у ETH есть пространство для дальнейшего падения, если рынок продолжит слабеть.

Для полного совпадения условий, которые предшествовали предыдущему крупному развороту, требуется более низкое значение NUPL. Таким образом, хотя стимулы к фиксации прибыли минимальны, сигнал о дне еще не полностью сформирован.

Давление ликвидаций обьясняет слабость цены

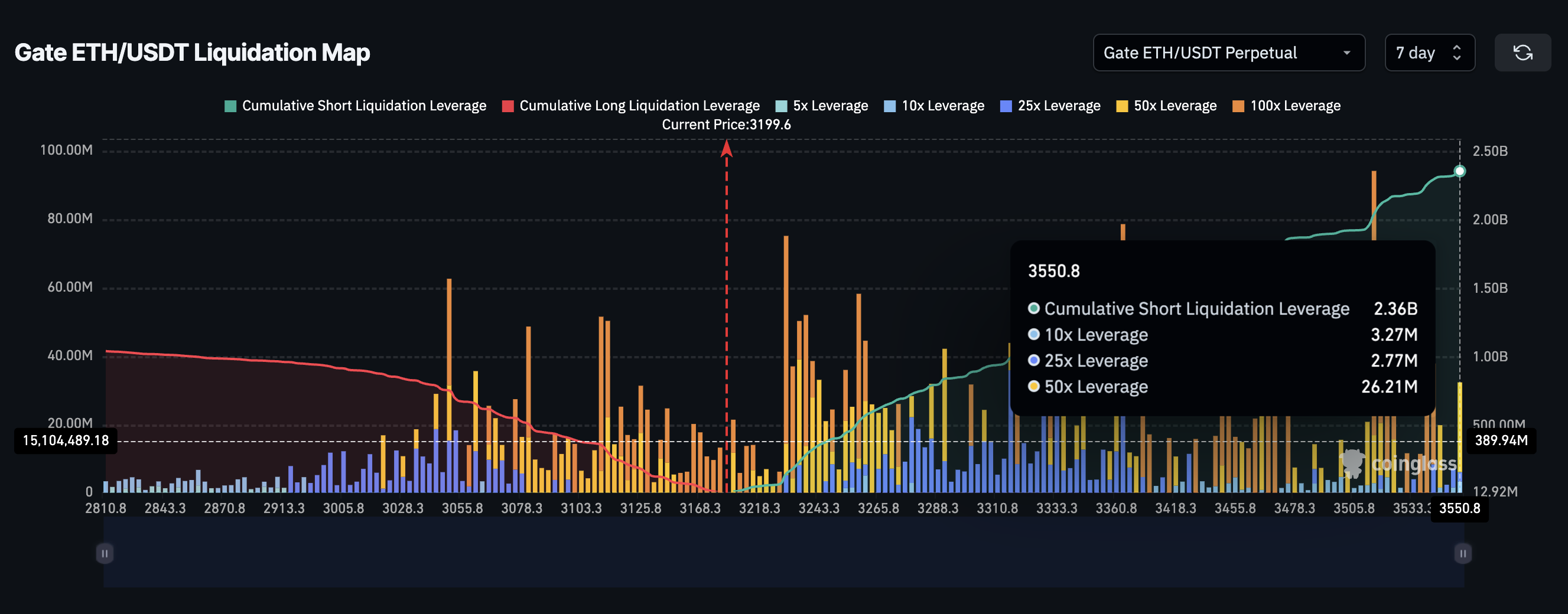

Рынок деривативов дает наиболее ясное обьяснение нерешительности Ethereum. Карта ликвидаций ETH/USDT (по данным Coinglass) показывает значительный обьем коротких позиций ($2,36 млрд), но и длинные позиции остаются существенными ($1,05 млрд).

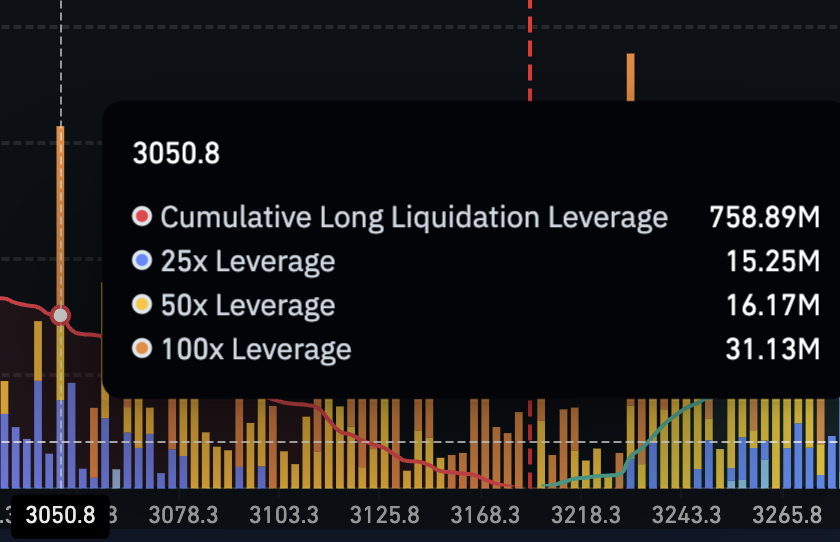

Этот дисбаланс сохраняет давление. Самый плотный кластер ликвидаций длинных позиций простирается примерно до $3050.

ETH торгуется вблизи этого уровня. Это означает, что даже небольшое падение может спровоцировать принудительные продажи со стороны «быков». Ликвидации длинных позиций могут легко нейтрализовать положительный эффект от низкого NUPL. Оставшееся кредитное плечо в длинных позициях достаточно велико, чтобы поддерживать нестабильность рынка.

Технический анализ подтверждает зону риска

График цены Ethereum подтверждает тот же сценарий. ETH по-прежнему торгуется внутри нисходящего канала, а регион $3053 остается важнейшей поддержкой.

Это в точности та зона, где находится самый сильный кластер ликвидаций. Если цена потеряет $3053, резко возрастут шансы на более глубокое падение.

Такое падение соответствует сценарию, при котором NUPL может опуститься к июньскому минимуму 0,17. Это, в свою очередь, будет соответствовать условиям, которые предшествовали последнему значительному росту.

Бычий сценарий существует, но требует подтверждения. ETH должен вернуть $3653, чтобы продемонстрировать реальную силу (рост более 14% от текущих уровней).

Затем преодоление $3795 изменит структуру с «медвежьей» на «нейтральную». Этот шаг также протестирует верхнюю границу нисходящего канала. Если NUPL стабилизируется, «шортисты» начнут закрывать позиции, а цена Ethereum преодолеет эти уровни, станет возможен резкий отскок. До тех пор, пока эти условия не совпадут, ETH остается в ловушке.

The post Ethereum не может восстановиться. Угроза ликвидаций на $3050 давит на цену appeared first on BeInCrypto.