- TVL в протоколах реальных активов превысил 10 миллиардов долларов.

- Ethereum и Solana лидируют в токенизации RWA.

- Аналитики рассматривают RWA и стейблкоины как варианты использования криптовалюты стоимостью в триллионы долларов.

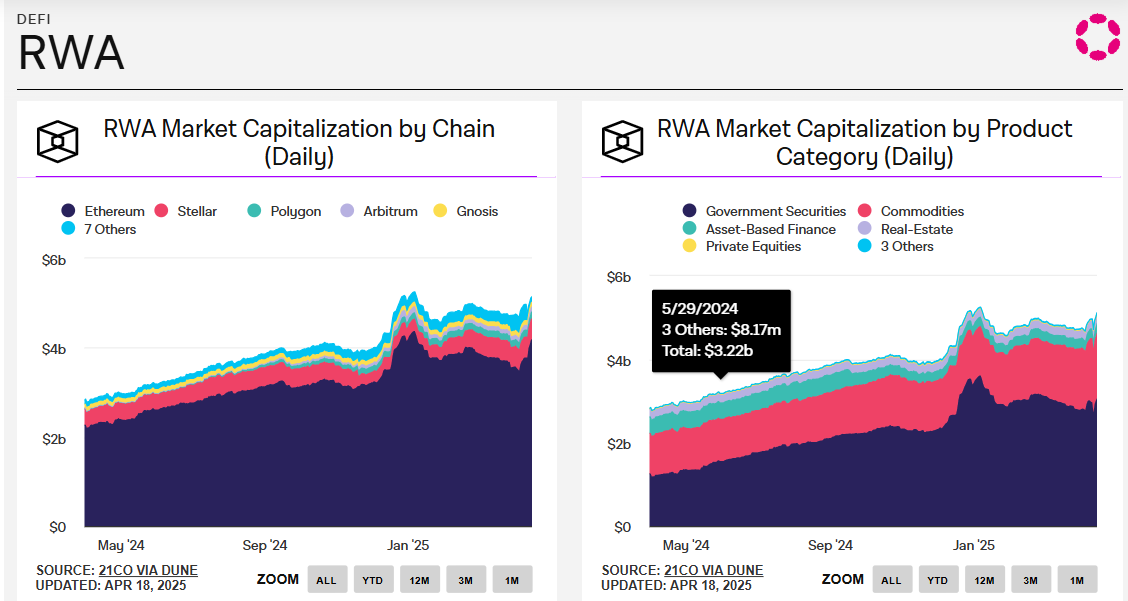

По данным IntoTheBlock, общая заблокированная стоимость (TVL) протоколов реальных активов (RWA) превысила 10 миллиардов долларов.

Эта веха отражает растущий интерес к токенизированным активам, особенно на блокчейнах Ethereum и Solana. Один аналитик рассматривает RWA и стейблкоины как два крупнейших реальных варианта использования криптовалют.

Насколько быстро растет RWA TVL?

Общая стоимость, заблокированная в протоколах RWA, выросла с менее чем 4 миллиардов долларов в мае 2024 года до более чем 11 миллиардов долларов к марту 2025 года. Это значительный скачок в притоке капитала на платформы токенизации.

Данные показывают высокий спрос на он-чейн-версии традиционных активов, таких как недвижимость, товары и частное кредитование.

По теме: «Снижает барьеры»: Дитон о доступе RWA; Армстронг называет это «будущей инфраструктурой»

Движущей силой этого роста являются Ethereum и Solana, которые являются ключевыми платформами для токенизации RWA. Обе сети предлагают возможности смарт-контрактов, которые обеспечивают безопасную и децентрализованную эмиссию, хранение и передачу активов. Ethereum имеет широкое распространение и глубокую ликвидность; Solana предлагает более высокие скорости и более низкие комиссии.

Аналитик видит RWA как вариант использования на триллион долларов

Подчеркивая эту тенденцию, криптоинфлюенсер Martyparty поделился графиком TVL на X, подчеркнув, что «TVL активов реального мира продолжает расти». Он подчеркнул, что токенизация RWA, наряду со стейблкоинами, представляет собой возможности на триллионы долларов для криптоиндустрии. Продолжающийся рост TVL отражает более широкую уверенность рынка в токенизации реальной стоимости.

RWA предлагают мост между традиционными финансами и децентрализованными платформами. Токенизация позволяет пользователям получать доступ к традиционно неликвидным рынкам, одновременно повышая эффективность и прозрачность.

Рост рыночной капитализации RWA и объема за 24 часа

По данным CoinGecko, общая рыночная капитализация токенов RWA выросла до более чем $34,7 млрд — на 1,5% за последние 24 часа. Среди главных претендентов — Chainlink, Stellar, Ondo, BlackRock’s BUIDL и Algorand.

Государственные ценные бумаги занимают самую большую долю рынка RWA, постоянно составляя 45–50% от общей стоимости. Товары и финансы на основе активов также представляют собой значительные сегменты, в то время как частный капитал и недвижимость занимают меньшие, но растущие доли рынка.

По теме: Освоение рынка активов реального мира стоимостью 30 триллионов долларов: 5 лучших проектов RWA

Лидерами, особенно в сфере токенизированных государственных облигаций, являются такие крупные компании, как Franklin Templeton и Ondo Finance, которые лидируют в выпуске токенизированных государственных ценных бумаг, что подчеркивает растущую роль традиционных финансов в ускорении принятия RWA.