• The trading volume and active user base of Polymarket have generally risen in tandem, indicating the platform is not solely reliant on a few large players to inflate data, though retention remains noticeably impacted by hype cycles.

• The increase in fees and revenue stems both from trading demand and from the gradual expansion of feeable categories and changes to the fee rate structure since Q1 2026.

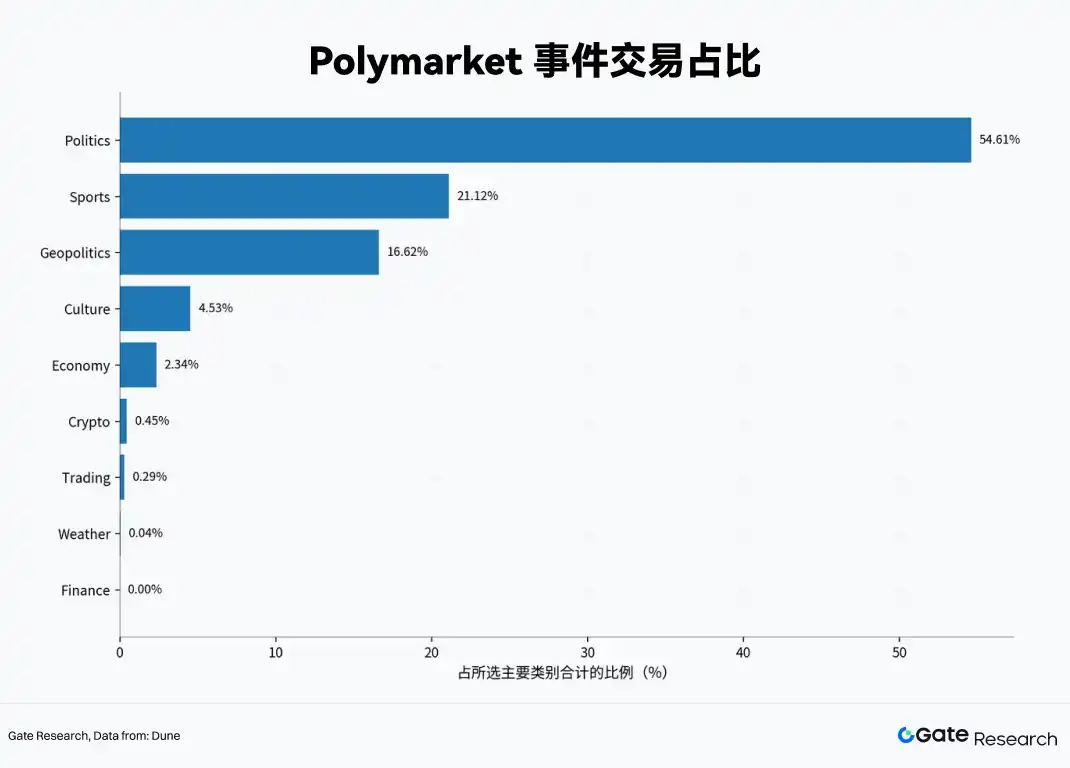

• Trading on the platform is highly concentrated in a few high-attention categories such as politics, sports, and geopolitics, with long-tail categories still struggling to independently support overall liquidity.

• Polymarket possesses attributes of both an information market and a sentiment market, but currently functions more as an event-driven trading venue activated during high-attention windows.

• Gate's prediction product is not a weaker copy of the on-chain version but rather addresses different issues related to account integration, entry friction, user conversion, and product distribution.

Introduction

As of April 2026, Polymarket's trading volume and fees are at historically high levels. The platform has evolved from an early on-chain experiment into an event market capable of handling large-scale trading flows around political, sports, macro, and geopolitical events.

The core of this article is not to reiterate what prediction markets are, but to answer four more specific questions: First, is Polymarket's growth truly structural? Second, is the expansion in fees and revenue driven by demand or by rule changes? Third, what are users actually trading? Fourth, why are leading exchanges like Gate beginning to incorporate prediction products into their trading ecosystems?

Based on these questions, this article will re-analyze the prediction market Polymarket through data, comparisons, explanations, and judgments.

Trading and Activity

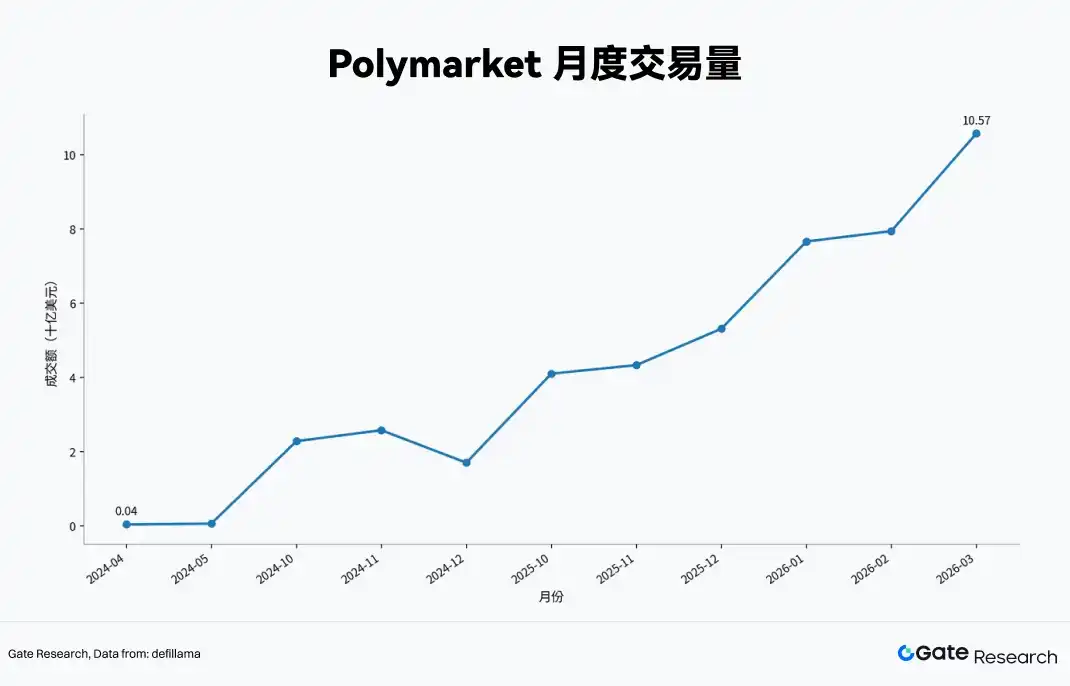

Polymarket's trading volume shows a clear stepwise upward trend. Monthly trading volume was only $38.9 million in April 2024, rising to $59.2 million in May. By October 2024, it had jumped to $2.28 billion, further reaching $2.577 billion in November. Although it retreated to $1.7 billion in December, it remained far above mid-year levels. Entering Q4 2025, the platform entered another acceleration phase, with monthly trading volume climbing from $4.1 billion in October 2025 to $10.57 billion in March 2026. In terms of scale alone, Polymarket is no longer an experimental, marginal on-chain product but has become an event-driven trading market comparable to some mature trading scenarios.

Polymarket's growth curve is a typical result of the combined effect of event-driven surges and the platform's capacity to absorb them. The significant rise from October to November 2024 highly correlated with election-related trading. The new wave of volume growth from Q4 2025 to Q1 2026 was driven jointly by sports, macro, finance, and geopolitical themes. The platform has shifted from "going viral due to one major event" to "multiple high-attention themes taking turns driving activity."

The expansion of active users has grown in sync with trading volume. Monthly active trading users were only 41,300 in July 2024, rising to 293,700 by November 2024, and reaching 462,600 in January 2025. After a mid-2025 decline, monthly active traders rebounded to 477,900 in October 2025, with recent months reaching 764,700. This indicates that Polymarket's trading volume growth has been accompanied by a continuous broadening of its user base. However, the activity data also clearly shows that user expansion remains strongly cyclical: when hype subsides, platform retention declines, indicating that while the base has thickened, loyalty and daily necessity are not yet strong enough to fully offset major event cycles.

Overall, Polymarket's growth is relatively genuine, but its authenticity is closer to structural expansion atop event-driven shocks. It has proven it can absorb traffic during major information windows and convert it into trading, but it has not yet fully proven it can maintain the same steep growth slope in the absence of strong narratives.

Fees and Revenue: Interpreting High Income with Caution

Compared to trading volume, Polymarket's fee data requires more careful interpretation. First, the fee framework itself has undergone institutional changes. According to the official fee documentation, Polymarket uses a dynamic fee model that only charges Takers, with different rates for different categories. Geopolitics and World Events currently maintain a zero fee. This means that Polymarket's fee growth is not solely a function of demand growth but is also directly affected by the expansion of feeable categories and adjustments to the fee rate structure. Simply annualizing the fee curve can easily mistake rule changes for permanent improvements in operational capability.

A key inflection point in fees showed a noticeable jump around late March 2026. Publicly verifiable data shows that Polymarket's gross protocol revenue for Q1 2026 was $16.23 million, while the 30-day fees as of early April 2026 had already reached $14.75 million, with 30-day revenue at $10.36 million. After expanding the feeable scope on March 30, the first full week's fees reached $6.8 million, with single-day fees exceeding $1 million on April 1.

The fee volume for the most recent 30 days is close to the revenue level of a full previous quarter. This certainly indicates strong trading demand on the platform, but a more important explanation is that a large volume of previously non-feeable event trading has been incorporated into the monetization system, naturally causing a leap in the revenue curve. This should not be simplistically interpreted as underlying demand suddenly doubling simultaneously.

Therefore, the current high fees are driven by both demand and rule changes. The former is reflected in the platform's own sufficient volume of event-driven trading flow, while the latter is reflected in the gradual "monetization switch" being turned on. From a business analysis perspective, these two should not be conflated. Simply extrapolating billions in annualized revenue from single-day fees exceeding a million dollars overlooks two practical constraints: First, high fee rates may dampen high-frequency trading and market-making enthusiasm. Second, the geopolitical category, which attracts the most attention, remains zero-fee, meaning the platform's hottest traffic pool may not translate proportionally into protocol revenue.

Thus, Polymarket's fee curve truly demonstrates that the platform has proven it can charge fees, signifying the beginning of a viable business model. However, whether the platform has proven that high revenue can be stably replicated over the long term requires more time to observe trade structure, market-making incentives, fee elasticity, and user response.

Market Structure and Event Concentration

Polymarket is far from a uniformly distributed, broad-spectrum market. Just three categories—Politics, Sports, and Geopolitics—account for 92% of the total trading volume in major categories. Comparing these to smaller categories like Culture, Economics, Crypto, Weather, and Finance, it's clear that while long-tail markets exist, their contribution to total volume is extremely limited.

Polymarket's core demand does not entirely come from the universality of "pricing anything," but from a few high-attention, high-controversy, frequently updated information sectors. Secondly, users are most willing to trade events with strong media dissemination attributes and clear resolution timelines. The enduring dominance of Politics, Sports, and Geopolitics is precisely because these three themes simultaneously possess narrative strength, information increment, and settlement clarity. Third, while the platform appears like an open market, it actually functions more like a collection of top-tier event markets. As long as major themes keep emerging, liquidity aggregates; once there is a lack of sufficiently strong event supply, long-tail markets struggle to support overall volume independently.

This may also bring some structural risks. Highly concentrated markets often develop depth and price discovery efficiency more easily for hot events but also exhibit stronger dependence on supply-side themes. Polymarket has room for category expansion, but its actual trading remains heavily reliant on a few thematic pools. This means its sustainability, besides user growth, also depends on whether the platform can continuously launch new, tradable, and resolvable streams of high-attention events.

Trading Behavior and Time Distribution

From an intuitive product perspective, prediction markets are often described as "information markets" because prices compress dispersed information into probabilities. But on Polymarket, this definition may only be partially accurate.

On one hand, weekends do not mean the platform is dormant. One Sunday in January 2026, the daily trading volume across the prediction market exceeded $814 million, with Polymarket accounting for about $127 million that day. During the geopolitical conflict trading window in March 2026, Polymarket, alongside other 24/7 Crypto trading platforms, accommodated risk expression when traditional markets were closed. On the other hand, thinner weekend liquidity is also a reality. In January 2026, there were cases of traders exploiting weak weekend liquidity to impact short-cycle price markets. This indicates that Polymarket's weekend trading tends to exhibit an unbalanced structure: "amplifying sharply with events, remaining shallow without."

Therefore, a more accurate judgment is that Polymarket possesses dual attributes of both an information market and a sentiment market, but at its current stage, the characteristics of a sentiment amplifier remain quite prominent. It can rapidly compress news, opinions, sentiment, and odds into trading prices—this is its information market aspect. However, its high dependence on hot events, media cycles, and collective narratives determines it is not a purely rational information aggregator. In other words, Polymarket's price discovery function is currently primarily activated only in high-attention scenarios.

Polymarket's Position in the Ecosystem

Polymarket is often compared to variants of three existing products: DEXs, sports betting, and perpetual contracts. But it is not identical to any of them.

It is unlike a DEX because the traded objects are not generic assets but conditional outcomes of discrete events. It differs from traditional betting because on-chain positions can be freely traded before settlement, with prices themselves carrying continuous probability shifts. It is also unlike perpetual contracts because its core is not directional leverage and funding rates, but finite-duration probability trading around specific events.

A more appropriate positioning is to view Polymarket as an "event derivatives market" or "information trading market" within Crypto. It transforms traditionally non-standardizable trades on macro, political, sports, and sentiment events into binary or multi-outcome contracts that can be listed, matched, and exited mid-way. It does not replace spot or futures but provides the market with a new type of tradable object: the future state of the world itself. Precisely for this reason, it is particularly adept at attracting attention during macro inflection points, election cycles, major sports events, and geopolitical conflicts, as these scenarios are naturally suited for expressing divergent expectations through "probability prices."

This is also Polymarket's unique role within the Crypto ecosystem. It does not primarily serve asset allocation but serves information expression, attention monetization, and event risk pricing. As long as this function exists, it will not be simply categorized as an ordinary trading platform. But as long as it remains highly dependent on event flows, it will also struggle to form completely stable daily demand like mainstream spot or perpetual markets.

Observation on Gate's Prediction Market Product

Gate's entry precisely indicates that prediction markets have entered the product expansion logic of trading platforms. According to Gate's official announcement, Gate has integrated a Polymarket portal within its App, offering "Prediction Mode" and "Trading Mode" for interaction. It supports participation using USDT within the exchange account system, as well as participation on Polygon using USDC via a Web3 wallet. The key to this design lies in transforming the process—which originally required wallet, network, stablecoin, and on-chain interaction experience—into an account-based experience closer to spot trading.

The centralized platform is not creating a weaker on-chain copy but is solving a different set of problems. The first is custody and account systems. Polymarket's native path emphasizes self-custody and on-chain settlement, with advantages in openness, transparency, and composability. Gate's portal integrates funds, positions, orders, and settlement within the exchange account system, significantly lowering the learning curve. The second is entry friction. For existing exchange users, entering prediction markets directly with USDT and their current accounts is smoother than separately preparing a Polygon wallet and USDC. The third is liquidity organization. On-chain markets' advantage lies in open order matching and external market maker access, while centralized platforms are better at directly migrating their own user traffic, order book interfaces, charting tools, and trading habits to new products, shortening cold-start times.

However, the advantages and disadvantages of on-chain versus centralized are asymmetrical. Polymarket's strengths lie in the verifiability of on-chain positions, higher market openness, easier access for external developers and market makers, and its product being inherently closer to the native form of information trading. Gate's strengths lie in lower educational cost, lower account-switching cost, higher user conversion efficiency, and being more suitable for introducing existing spot and contract users to event trading. Their compliance boundaries also differ. On-chain platforms often emphasize open infrastructure and global liquidity, while centralized platforms emphasize managing product visibility and usage paths according to region and account systems.

Therefore, the significance of Gate's prediction market product should be understood as the beginning of a bifurcation in prediction markets into two distinct product paths. Polymarket emphasizes on-chain openness and native information trading, while Gate-style products emphasize low-friction access, account integration, and conversion of existing users. The two will likely coexist long-term across different user segments and regulatory environments.

Risks, Constraints, and Future Evolution Path

The primary external constraint Polymarket faces remains regulation. In November 2024, French regulators had already pushed for its geoblocking in France. By April 2026, the CFTC publicly sued three states to assert federal jurisdiction over prediction markets. Viewed together, these incidents indicate that there is still no unified answer regarding whether prediction markets are more like derivatives, gambling, or information tools in different regions. As platforms continue to penetrate mainstream financial scenarios, this classification issue will directly impact reachable users, listable events, and the applicable settlement frameworks.

Internal structural risks also cannot be ignored. The first is resolution and oracle risk. Although Polymarket uses clear rules and the UMA Optimistic Oracle for resolution, complex events, ambiguous statements, and edge cases can still spark disputes. More disputes make it harder for users to adopt it as a low-friction tool for long-term use. The second is liquidity concentration risk. Current volume heavily depends on headline events; once hot themes are insufficient, the depth problem in long-tail markets resurfaces. The third is fee instability. The platform recently demonstrated its ability to charge fees but also exposed the sensitivity of revenue to rule adjustments. If fee rates are too high or incentives insufficient, market-making and high-frequency trading may cool first. The fourth is uncertain user retention. Many users may come for a specific election, conflict, or tournament but not necessarily stay after the hype subsides.

The key to future evolution lies in whether the platform can transform event trading from successive peaks into more stable trading habits. This requires simultaneously addressing three issues: improving market creation and settlement quality, expanding beyond single-burst sustainable themes, and finding a more balanced structure between fees, market-making, and user experience. Only by achieving this can Polymarket potentially evolve from a high-hype application into a more durable product category.

Conclusion: Polymarket's Current Real Value and Boundaries

It is undeniable that Polymarket has proven three things. First, it is not a flash-in-the-pan on-chain experiment but has become an event-driven trading platform with real trading scale, genuine user expansion, and real fee-generating capability. Second, its growth is not purely speculative; active users and transaction volume have indeed risen together, indicating the platform is not solely propped up by a few whales inflating data. Third, it has established a clear and scarce position within Crypto: making future events themselves tradable objects.

But it also has not yet proven three other things. First, high trading growth does not equate to demand becoming de-coupled from events; the platform remains heavily driven by political, sports, and geopolitical events. Second, rapidly rising fees do not automatically prove revenue can be stably annualized, as the expansion of the feeable scope is itself a significant variable. Third, it has not yet proven it has become a universal, low-volatility, high-retention long-term product form; it currently remains a highly efficient market apparatus primarily during high information-density windows.

Therefore, Polymarket's real value lies in making a category of previously difficult-to-trade objects into a truly liquid market and demonstrating commercialization potential. Its boundaries lie in the fact that this market remains highly dependent on event supply, regulatory environment, and user attention. Looking ahead, both the native on-chain path and Gate-style centralized integration paths are likely to persist: the former represents open information trading infrastructure, the latter represents lower-friction productized distribution channels. What truly warrants ongoing observation is who can first transform prediction markets from peak-hype products into normalized trading categories.

References

• DeFiLlama, https://defillama.com/protocol/polymarket

• Polymarket Docs, https://docs.polymarket.com/trading/fees

• Blockworks Analytics, https://blockworks.com/analytics/polymarket/polymarket-overview/polymarket-trading-volume

• Dune, https://dune.com/kosard/polymarket-wallet-tracker

• Gate, https://www.gate.com/zh/learn/articles/gate-integrates-polymarket-prediction-market-a-new-era-of-event-based-trading

• The Block, https://www.theblock.co/post/377214/polymarket-rebounds-kalshi-leads

• RootData, https://www.rootdata.com/news/411172

The Gate Institute is a comprehensive blockchain and cryptocurrency research platform, providing readers with in-depth content including technical analysis, hot topic insights, market reviews, industry research, trend forecasting, and macro-economic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks. Users are advised to conduct independent research and fully understand the nature of the assets and products they purchase before making any investment decisions. Gate is not responsible for any losses or damages resulting from such investment decisions.