Author:Lucas, former Bankless member

Compiled by:Saoirse, Foresight News

Core Summary:

- All assets will be tokenized in the future;

- Ethereum becomes the settlement layer for various tokenized assets;

- ETH is used for network security staking, capturing all value generated by settlement business;

- The global financial system is transitioning towards asset tokenization;

- Relying on security, stability, and long-accumulated ecosystem barriers, Ethereum will capture a significant market share in the tokenization track.

The ‘Ethereum is Dead’ Narrative is Rampant

Currently on crypto social platforms, market pessimism towards Ethereum has hit a historical low. Many colleagues I've worked with for years have gradually faded from the Ethereum scene, some have even left the crypto industry entirely, and the vast majority no longer hold significant ETH positions. The core reason is they no longer recognize its investment value. This is not targeting any individual or circle, but a common phenomenon I've personally witnessed within the industry.

The large-scale capital outflow is partly because cryptocurrency is no longer cutting-edge hot technology, with AI, robotics, and longevity research taking over as capital darlings; but the poor returns from ETH's weak price action are the key driver for market bearishness. To put it bluntly, holding ETH over the past few years has been a terrible experience.

However, I remain steadfastly bullish on Ethereum and ETH, with even more confidence than at any previous stage, and I recommend readers to be bullish together. In fact, Ethereum is entering the most promising adoption and growth cycle in its own history.

Talking About the Poor Price Performance

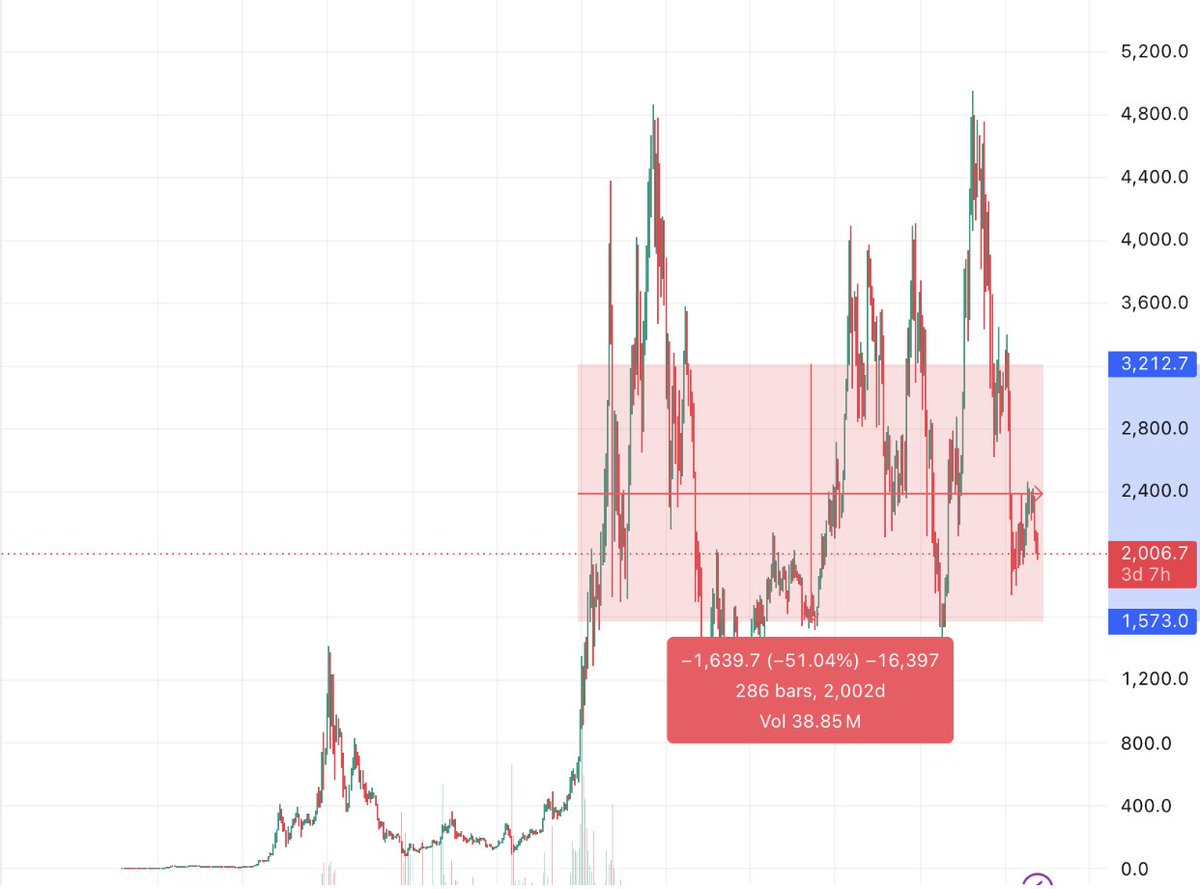

First, let's address the most obvious issue: the price performance of ETH has been quite poor over the past nearly five years. Investors who entered and held positions in 2021 are, at best, breaking even, with most being deeply underwater. Even with the recent market correction, Bitcoin's current price still stands firm above the 2021 bull market high, with its 2025 peak directly doubling that high; in contrast, ETH's current price has plummeted about 60% from its previous all-time high, failed to set a new all-time high in 2025, and couldn't even break through the $5,000 mark.

During the same period, the S&P 500 index almost hit new all-time highs daily, with hot Wall Street sectors like AI, semiconductors, and energy seeing stocks surge across the board, making ETH's performance even more embarrassing in comparison.

The good news, however, is that when looking at a longer cycle, ETH's chart is merely stuck in a multi-year range-bound consolidation. Ethereum's current market cap exceeds $200 billion, with its price holding the $2,000 level for years, firmly placing it among the top 100 global assets by market cap. Looking at the development patterns of capital markets, it's quite normal for high-quality growth assets to experience years of sideways consolidation and bottom grinding before launching a long bull run.

Ignore the percentage change values; focus mainly on measuring the length of time the price stayed within that range.

Global giants like Amazon, NVIDIA, Apple, and Microsoft have all walked the same path:

- Amazon: Led by Bezos, the company consolidated sideways for nearly a decade in the 2000s after the dot-com bubble burst, weathered the industry winter, and grew into a global top-tier enterprise;

- NVIDIA: Experienced seven long years of consolidation in the 2010s, then saw an epic stock price surge riding the AI wave, joining the global top tier by market cap;

- Apple: Was in long-term迷茫 (confusion/consolidation) throughout the 80s and 90s, only taking off after Jobs returned to the company in 1997;

- Microsoft: Its stock price consolidated sideways for about 15 years after 2000; investors who entered in 2000 didn't break even until 2015, and now it's the world's second-largest company by market cap.

It's not hard to summarize the pattern: most of the world's top-tier assets undergo long, boring consolidation periods. Some assets briefly spike to new highs before pulling back again, then wait for industry catalysts to start a new bull cycle. Moreover, during the consolidation/bottom-grinding phases of these companies, the broader US stock market was often still making new highs. Within this logic, ETH's weak performance over the past five years is not abnormal in financial history.

Setting aside the chart price, Ethereum's current fundamentals are actually at their historical best.

On-Chain Ecosystem Data Continues to Improve

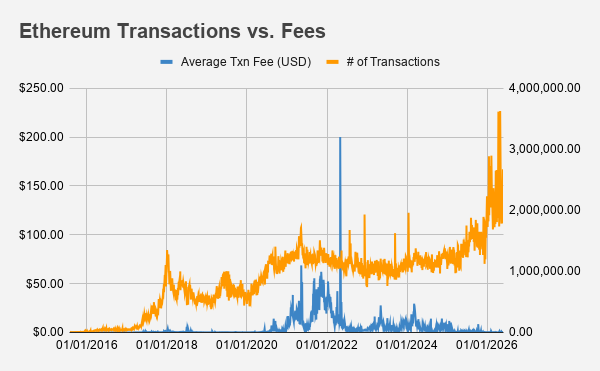

According to the market's bearish narrative, weak price action must be accompanied by a decline in on-chain activity: decreasing transaction volume, high fees, and stalled practical applications. However, the actual data is completely opposite. Ethereum's on-chain transaction volume is steadily climbing, fees are hitting new lows, and the pace of asset tokenization is continuously accelerating.

Data source: Etherscan

Based on Etherscan data: In May 2026, Ethereum's average daily transaction count reached 2.27 million, setting a new historical peak for the network. During the same period, the average transaction fee per transaction was only $0.27. Compared to the high gas fees of $50~$100 during the 2021 bull market, costs have significantly decreased despite transaction volume doubling.

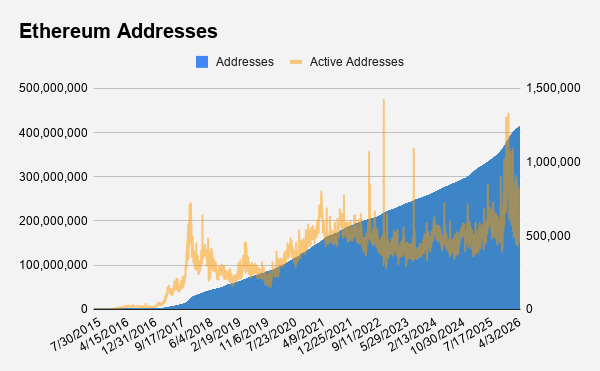

The total number of on-chain addresses has exceeded 400 million, with a daily growth rate of about 0.08% in 2026. Daily active users on-chain have stabilized above 1 million in recent months. At the current growth rate, without major industry catalysts, Ethereum's total address count may break 1 billion around mid-2029.

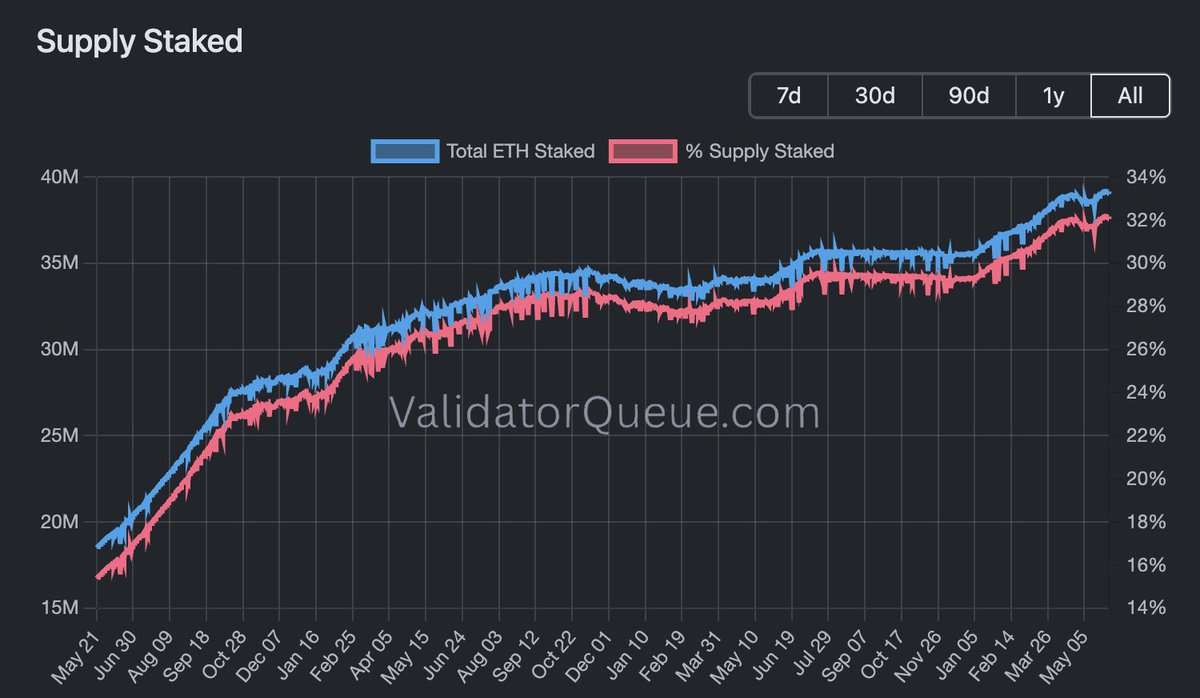

Staking is also continuously setting new records: over 32% of ETH supply is staked and locked, continuously underpinning network security.

Data source: validatorqueue.com

In summary, Ethereum has completed its scaling iteration while maintaining the bottom line of decentralization and security. It has never experienced a full network outage in over a decade of operation. Relying on its extremely neutral, secure, and programmable block space, it has secured the core chips to compete as the underlying infrastructure for global finance, which is also a prerequisite for subsequently hosting the massive tokenization of traditional assets.

Becoming the Underlying Infrastructure of the Global Financial System

Since entering the industry in 2017, my long-term logic for Ethereum has never changed:

- Eventually, all valuable assets in the world will be tokenized;

- Ethereum becomes the unified settlement layer for all types of tokenized assets;

- ETH captures the entire value increment brought by the settlement layer's business.

In its first decade, Ethereum primarily served as a testing ground for crypto-native assets, with sectors like DeFi, NFTs, and meme coins born and developed on it, solidifying its foundational ecosystem. In the upcoming development phase, Ethereum will embark on a new journey towards a trillion-dollar market cap.

For veteran crypto-native players, traditional finance going on-chain might seem somewhat dull, but it is an indispensable step for blockchain to go mainstream, worthy of the entire industry's promotion. In the future, the vast majority of the world's $700 trillion worth of traditional physical assets will ultimately be tokenized on-chain, and Ethereum will become the preferred hosting network.

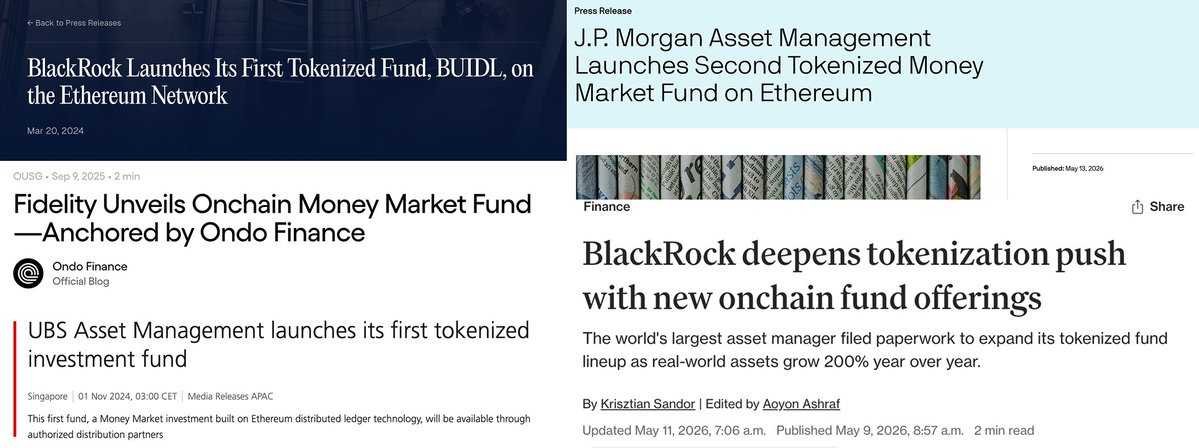

Many counter: Ethereum's scaling capacity is insufficient to handle massive assets; other public chains will carve up the market. But current implementation data already disproves this view: traditional financial institutions are onboarding the Ethereum ecosystem in large batches.

A series of news headlines from the past ~2 years, notice they have one thing in common.

The core demand of institutions entering is certainty: for banks, asset managers, and clearinghouses, choosing a blockchain to custody trillions in assets is a major strategic decision. They need to capture the tokenization红利 (dividend/benefit) while avoiding career risks from decision-making mistakes.

Of course, public chains like Hyperliquid and Solana can also get a piece of the pie. The tokenization track is large enough to accommodate multiple public chains developing together; it cannot be monopolized by one. However, traditional institutions pursuing stability will prioritize Ethereum when implementing RWA.

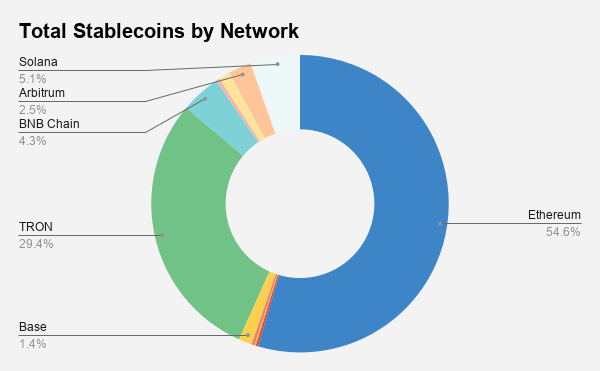

Implementation data supports the view: Stablecoins are the first tokenized real-world asset to achieve product-market fit, with a total circulating market cap exceeding $300 billion. Tom Lee called stablecoins the "ChatGPT moment" for the crypto industry, with Ethereum holding a 54% market share of the total stablecoin market cap.

Data source: rwa.xyz

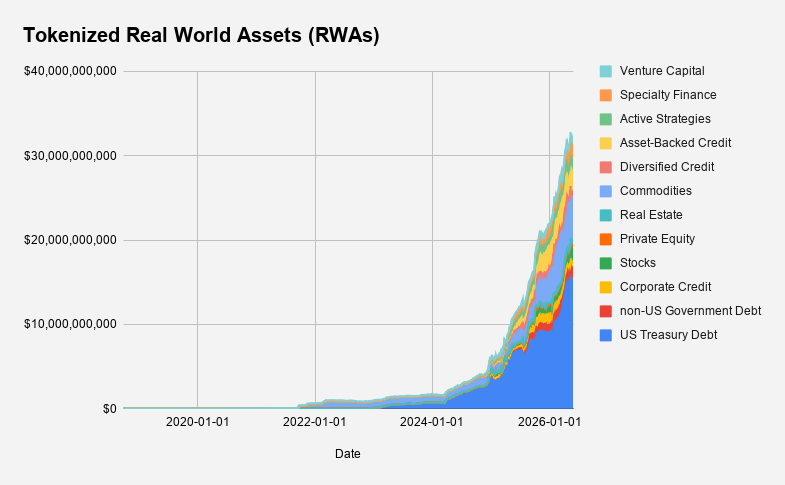

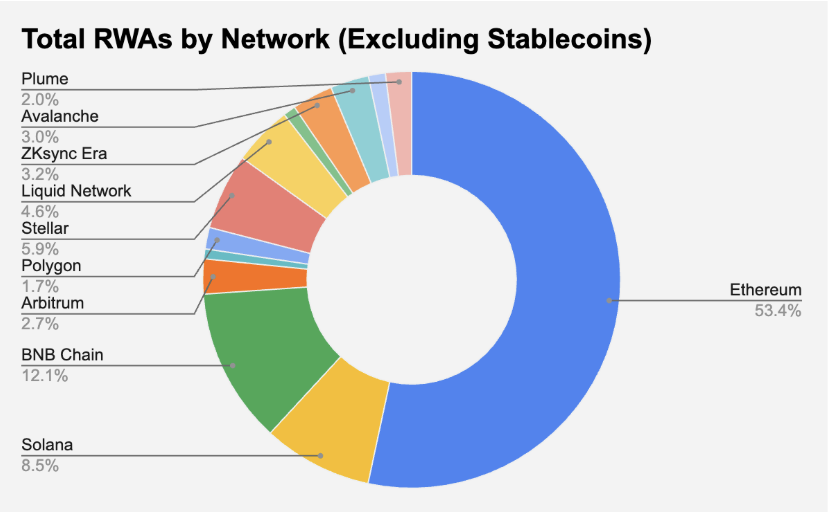

As of June 1, 2026, the total scale of all-category Real-World Asset (RWA) tokenization has exceeded $30 billion, with the growth curve steeply rising; over 53% of these RWA assets are deployed on the Ethereum chain. Even if other public chains start from scratch to compete for non-stablecoin RWA份额 (market share), Ethereum still firmly holds the dominant position.

Data source: rwa.xyz

The current development stage of the RWA track is comparable to DeFi in its萌芽期 (germination/early stage) of 2019~2020: the logic of the new track is clear, and early data is steadily rising. Looking back at DefiLlama's past data, DeFi's total value locked (TVL) saw exponential growth in the first half of 2020, while ETH's chart was also in long-term sideways consolidation at that time.

When the DeFi bull market fully erupted and liquidity mining swept the network, ETH, dragged down by the Covid行情 (market situation), had a market cap of only $20~25 billion, ten times smaller than its current $230 billion market cap. Meanwhile, the newly born BNB Chain once threatened Ethereum's position with its advantage of low fees. It wasn't until the DeFi asset scale reached about 20% of Ethereum's total market cap that ETH launched from $300 to $4000 by year-end, experiencing a super bull run.

Comparing to the present: Excluding stablecoins, the total scale of non-stablecoin RWA on Ethereum is about $16 billion, accounting for only 7% of ETH's total market cap, positioning it similarly to DeFi's early germination stage, but with an overall scale ten times larger than back then: early DeFi started at $3 billion, now RWA starts at $30 billion; early ETH bottom at $200, now ETH bottom at $2,000; early competitor was BNB Chain, now the competitor is Hyperliquid.

Additional note: Early DeFi催生 (spawned/generated)大量 (a large amount of) ETH buy pressure through抵押需求 (collateral demand), and NFTs further strengthened the "ETH as Digital Gold" narrative. However, Ethereum had not yet implemented Proof-of-Stake (PoS) staking and the EIP-1559 burn mechanism at that time. Now both rules are fully implemented, and every on-chain transaction can directly bring deflation and value support to ETH.

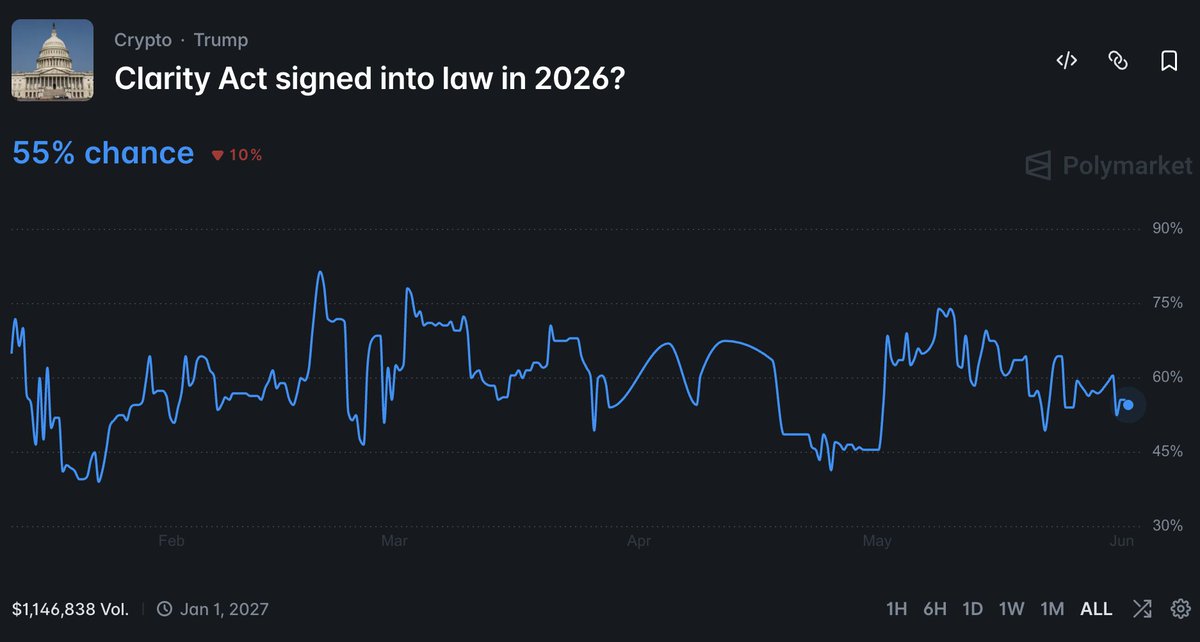

Projecting with a ten-fold space, the overall RWA (excluding stablecoins) scale in this cycle is expected to突破 (break through) $1 trillion. The U.S. "CLARITY Act" becomes a key catalyst. According to Polymarket data, the probability of the法案 (bill/act) being signed into law within 2026 is about 55%. Its passage will open channels for compliant on-chain listing of all U.S. financial assets, becoming a超级利好 (super positive catalyst) for Ethereum.

Ethereum's Vitality Remains Strong

Stocks, bonds, commodities, real estate, art, intellectual property—everything of value will ultimately move towards tokenization. This is the next major innovation in the global financial sector.

The first twenty years of the crypto industry focused on the issuance and innovation of crypto-native assets; the next twenty years will shift the industry's focus towards bringing traditional physical assets on-chain.

Even though the current crypto舆论圈 (discourse/opinion circle) is generally bearish on Ethereum, I am still convinced: Ethereum will become the承载底层 (hosting base layer) for the vast majority of the world's tokenized assets. Relying on its accumulated security, reliability, and liquidity barriers over the years, Ethereum's advantages cannot be短期复刻 (short-term replicated). Once massive global assets land on Ethereum, the market will finally reprice ETH, replicating the past valuation surge行情 (market trend).