Written by: Prathik Desai

Compiled by: Block unicorn

Small annoyances can sometimes save lives.

Think about that incessant beep in your car that reminds you to fasten your seatbelt. This constant reminder is annoying, and many people have complained about it. But it is this persistent beep that has prompted countless people to buckle up. The result? According to the Insurance Institute for Highway Safety (IIHS) in the United States, these constant reminders save approximately 1,500 lives each year in the U.S. alone. A true lifesaver.

Small irritations can also save you a lot of money.

One of the annoying aspects of modern banking is when you think you've completed a wire transfer, only to be interrupted. You've entered the account number, routing number, and recipient's name. Instead of processing the transfer immediately, the bank pauses to confirm whether the recipient's name matches the account information. This adds an extra click, disrupting the flow. In product team terms, this is considered friction. However, this pause has become one of the most effective security measures for payments globally.

The "Confirmation of Payee" service provided by Pay.UK enables individuals and institutions in the UK to make transfers, currently covering over 99% of transactions across various payment channels. The volume of checks has grown from 14,000 per month in June 2020 to over 70 million per month by July 2025. It has reduced "incorrect account" transactions by 59% and decreased end-user financial losses by 20% to 40%.

This is crucial at a time when the financial industry has been striving for over a decade to make transactions seamless. We've seen efforts like "one-tap," "one-swipe," and "click-to-trade," all attempting to make funds flow silently in the background. The industry's instinct is often to view every pause as a flaw. As finance evolves, it has become increasingly obsessed with seamlessness. But this evolution has repeatedly reminded us that certain so-called "frictions" are actually necessary brakes that prevent the system from collapsing.

Traditional Finance's Need for Brakes

Today, the financial industry has embedded these safeguards into every new piece of infrastructure it builds.

In the United States, broker-dealers with market access must implement risk controls to limit their financial exposure and ensure regulatory compliance. When the Securities and Exchange Commission (SEC) adopted Rule 15c3-5, it stated that the rule was designed to address the risks posed by automated high-speed trading and to prevent unfettered access to exchanges.

The reason the industry repeatedly relearns this lesson is simple: when brakes fail, the damage often exceeds what institutions can bear and recover from.

In 1987, on Black Monday, the Dow Jones Industrial Average plummeted 22% in a single day. The Brady Commission recommended adding a pause button in the form of "circuit breakers," which mandate a 15-minute trading halt when market declines reach a certain percentage. Without these limits, Black Monday alone wiped out $1.7 trillion in global market capitalization. Adjusted for inflation, that loss is equivalent to over $4.7 trillion today, surpassing the current GDP of Germany, the world's third-largest economy.

These brakes taught the financial world that sometimes the only way to maintain speed is to briefly stop the machine. In other cases, a brief pause is all it takes.

In August 2012, Knight Capital Group experienced a software glitch that caused its computers to buy and sell millions of shares of stock in just 45 minutes. The malfunction caused $440 million in losses in less than an hour, pushing the market maker to the brink of bankruptcy. Knight Capital had optimized its system for speed, which is crucial in market trading. But an uncontrolled system without brakes, even the fastest one, can collapse in an instant. The lesson? The faster the system, the more important the braking mechanisms.

Retail finance itself has faced its share of issues.

For years, brokers have worked to make high-risk products easy to use to drive retail user growth. They persevered, only to lose trust. In the 2021 disciplinary action against Robinhood, FINRA noted that the company failed to conduct due diligence before approving customers for options trading and relied heavily on unregulated automated "approval bots." The non-profit self-regulatory organization responsible for investor protection claimed that Robinhood's system approved customers based on inconsistent or illogical information. FINRA stated that the company's system allowed applicants whose risk profiles were clearly questionable to gain approval.

Robinhood's system was optimized to process applications quickly, avoiding potential customer wait times. But what it lacked was a meaningful pause between curiosity and security. Speed, but no brakes.

The Curious Case of Cryptocurrency

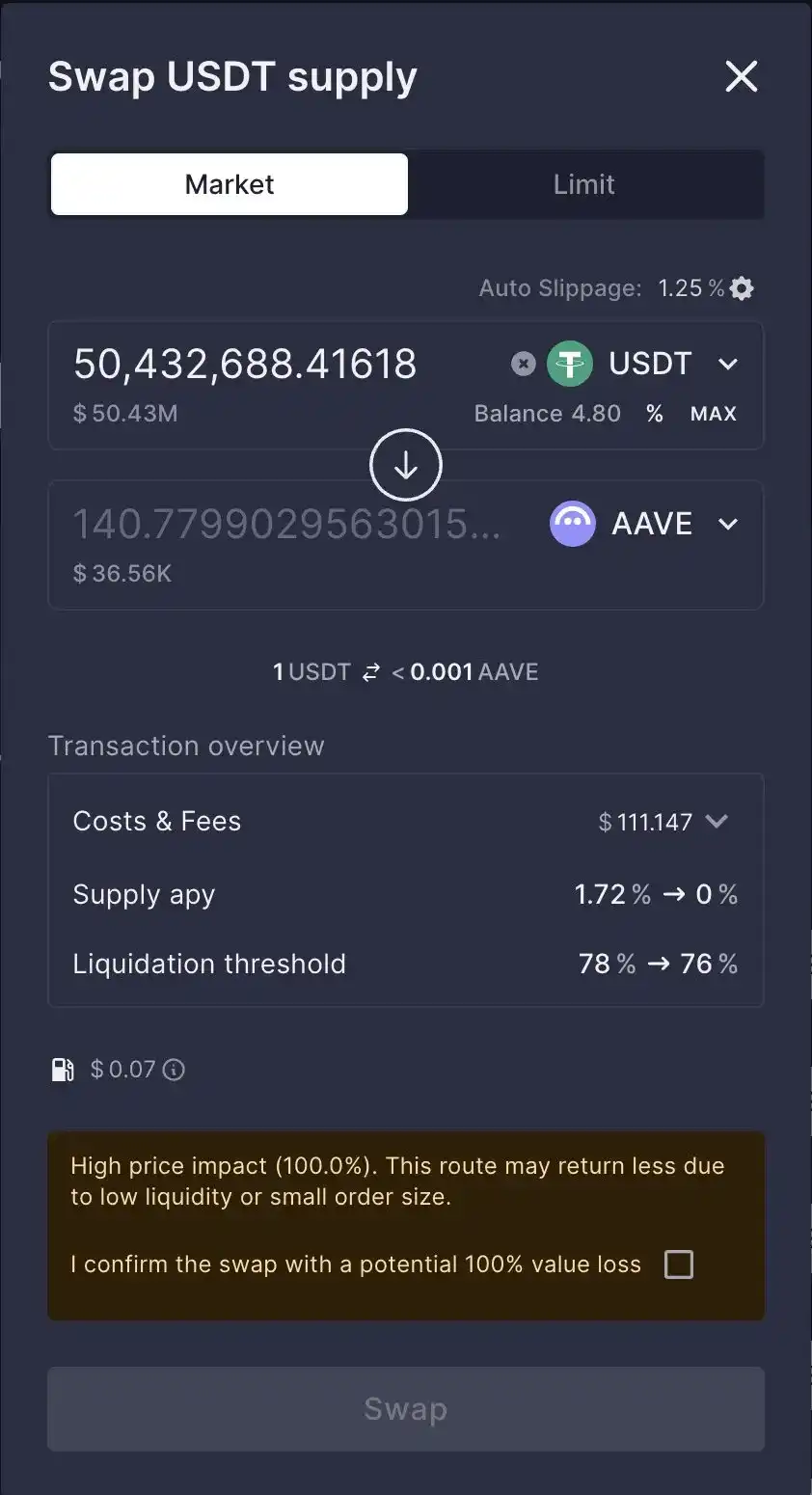

The recent Aave-CoW incident in the cryptocurrency space has elevated the need for brakes in finance to a whole new level.

On March 12, 2025, a user executed a $50 million swap through CoW Swap, a decentralized exchange (DEX) aggregator designed to protect users from bot front-running. The transaction was integrated into the front end of the DeFi protocol Aave. Due to insufficient liquidity, the user ended up receiving tokens worth only $36,930, while paying $50 million.

Although Aave explained in its post-mortem that the user ignored explicit high-price impact warnings, its founder and CEO Stani Kulechov posted on X that the Aave team "will look into how to improve these safeguards."

Jargon aside, the takeaway is clear: a fast interface allowed a catastrophic trade to proceed too far before the system could react. While one might question the user's judgment and disregard for warnings, treating this as an isolated incident is both convenient and counterproductive for the development of new financial infrastructures like blockchain.

If cryptocurrency wants to avoid repeating past mistakes, the solution lies in building smarter execution layers. Some decentralized finance (DeFi) trading protocols are already moving in this direction.

For example, Definitive.Fi argues that large on-chain transactions should not simply be processed along the technically possible path. They should be simulated before submission, tested against actual market conditions, split into smaller lots if necessary, and routed through broader liquidity pools. Thus, a good trading system should not only check if it *can* execute the trade but also determine the *best* path to fulfill the order.

For any emerging infrastructure, trust and additional security are not optional features, especially in finance. A product that makes trading, lending, or transferring funds easy and convenient can help it grow rapidly, but when it fails, the consequences are severe. We've seen this pattern in all the traditional finance cases above. Systems try to minimize visible points of friction—even when those frictions are necessary limits—mask their complexity, and hope that a smooth operation will win more consumer trust.

But confidence in finance is rarely built this way. It often comes from financial institutions identifying critical moments that require intervention and taking some unpleasant but necessary steps to stop the action. This is the case with Pay.UK's Confirmation of Payee. While repeatedly being asked to confirm a bank account name is certainly not a pleasant experience, it does stop the action at a point where a mistake could be costly and irreversible.

Aave's Stani understands this well. That's why he acknowledged that customers aren't always clear about the order flow, who they are paying, or if there's a better channel for the trade. This understanding is especially important in emerging industries like cryptocurrency and blockchain, where few users understand the technical flow of a transaction and the consequences of each click. In such contexts, acknowledging pain points and taking steps to address them is crucial for building consumer trust.

The tricky part is that the line between a braking mechanism and random inconvenience or friction is thin. Good brakes don't slow things down completely; they apply slight resistance with precise timing. In the case of the Aave-CoW incident, we can imagine a good brake as a kind of economic sanity check. It allows the system to scan more trading venues before routing, prevents order intent from falling into the wrong hands, simulates outcomes before execution, and splits large trades to avoid users being penalized for their size. These mechanisms are key to ensuring financial infrastructure is trustworthy.

This distinction is important because genuine pain points still exist in finance. For example, cumbersome and useless paperwork, inefficient compliance processes that slow everything down, hidden fees disguised as part of the process, and intimidating,繁琐 registration processes that scare away new users.

None of these should be defended. Installing "brakes" is not about defending uglier products or adding more pop-ups; it's about designing a pause when a user is about to make an irreversible decision based on incomplete information. This is especially true when customers are handling large orders in illiquid markets, selling high-risk products, exploring new payment methods, and performing one-click actions where the risk is immediate and speed is not the primary consideration.

There are business implications here too.

The finance industry often talks about building safeguards *after* achieving product-market fit. This gets it backwards. In finance, safeguards are an integral part of product-market fit. When implemented well, safeguards aren't even hindrances. The Pay.UK case further confirms that "Confirmation of Payee" is not just an optional anti-fraud feature but has become a "utility service that customers expect to see" when using the system to transact.

Emerging financial infrastructures, such as blockchain, aim to earn trust and withstand errors, scandals, and market pressures just like traditional finance. But this is not easy. It must think more proactively about how to earn trust *before* winning users, because trust will naturally bring users. The reverse is not necessarily true.

If blockchain can adopt strategic braking measures, its speed will surpass that of any other financial infrastructure.