Editor's note: The narrative of AI investments is further expanding from chips and models to the data infrastructure layer.

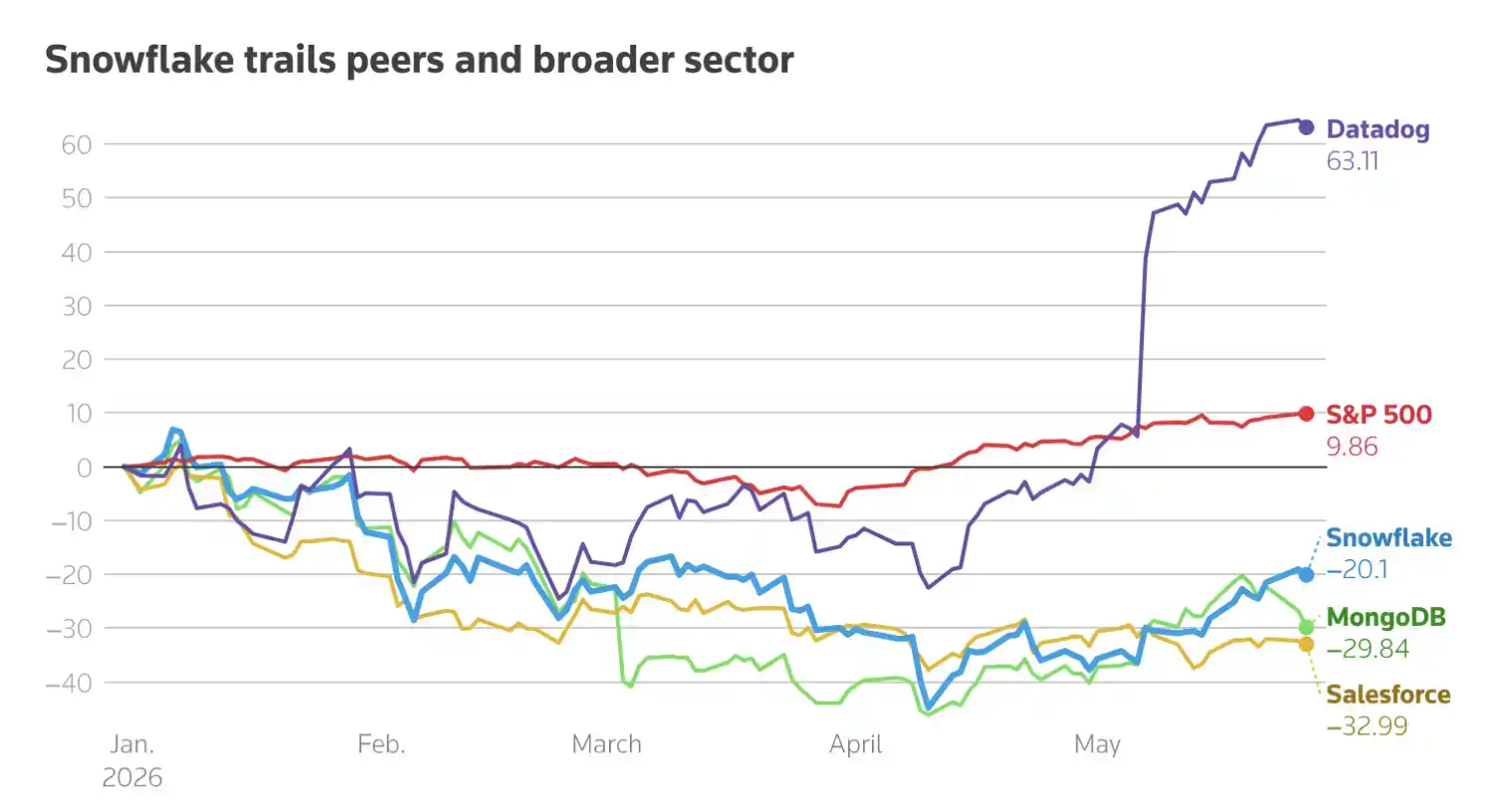

After facing stock price pressure since the beginning of the year, Snowflake saw its stock surge over 33% in a single day after raising its full-year revenue forecast and securing a $6 billion five-year cooperation agreement with AWS. The core of this market reaction isn't just about better-than-expected earnings; it's that investors have started to reassess Snowflake's position in the enterprise AI implementation chain.

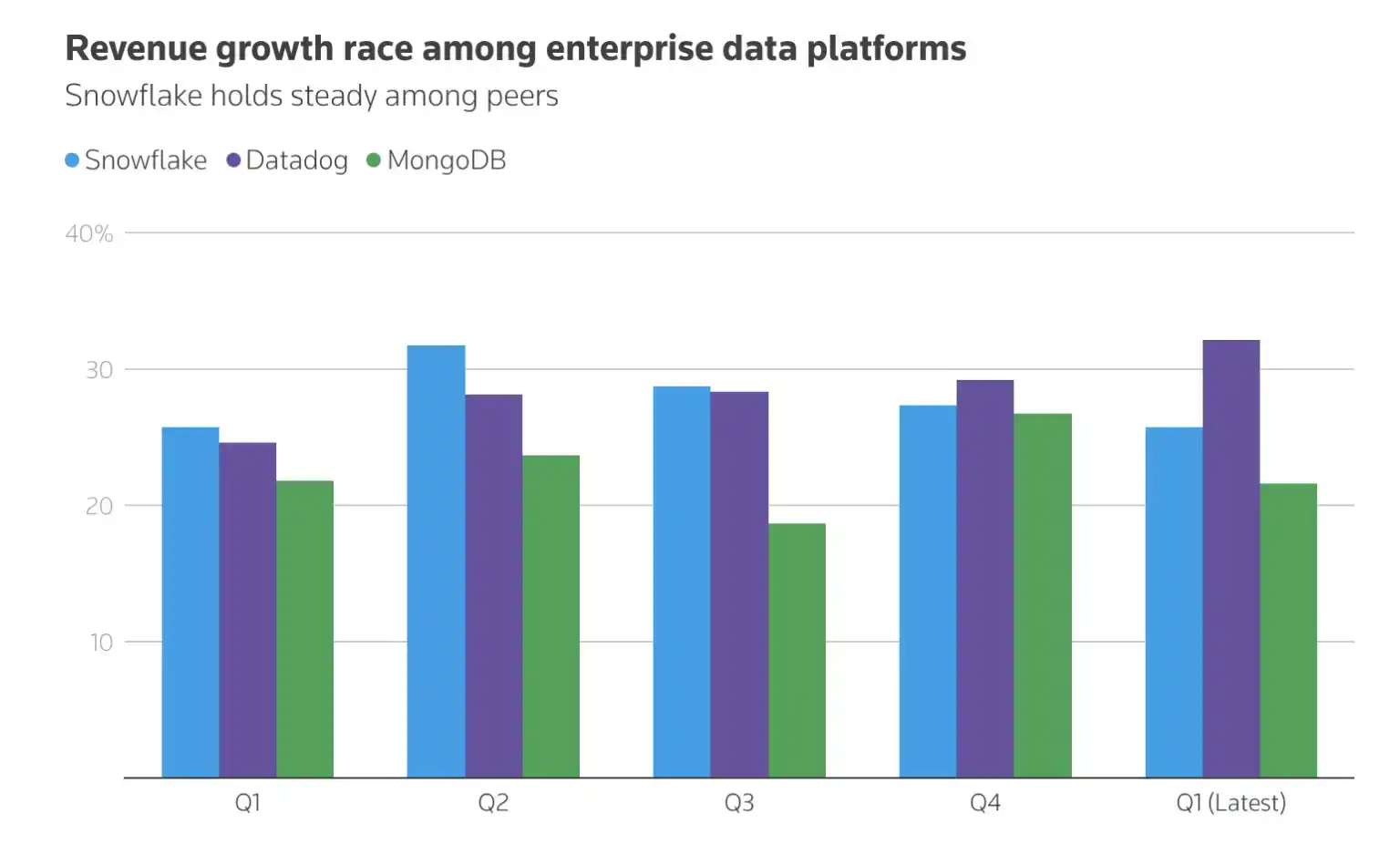

Over the past year, enterprise software companies have generally faced a question: Will AI become a growth engine, or will it undermine their existing business models? Snowflake's latest performance and the AWS partnership provide a relatively clear answer—when enterprises start deploying AI applications at scale, the capabilities for data storage, processing, analysis, and model deployment become even more critical.

In this partnership, the supply of AWS Graviton chips addresses the computing power constraint issue, while the deeper integration of the Snowflake platform with AWS AI workloads points to a more profound enterprise need: companies don't simply "use AI"; they need to connect their own data into AI workflows to build operational, manageable, and scalable application systems.

This is also why Snowflake is being re-integrated into the "AI winner" narrative. AI software stocks previously experienced a sell-off, with the market being skeptical about whether "AI can truly contribute to revenue." However, Snowflake's case shows that once AI translates from conceptual demonstrations into real revenue growth, market sentiment can reverse rapidly. The fact that at least 30 analysts raised their price targets illustrates that the capital markets are re-pricing the value of data platforms within the AI infrastructure cycle.

What's even more noteworthy is that this deal also reinforces the presence of AWS's in-house chip ecosystem. From Anthropic, OpenAI, and Meta to Uber, and now Snowflake, Amazon is embedding itself deeper into the AI infrastructure through cloud, chip, and enterprise software partnerships. For Snowflake, this means it is not just an enterprise data warehouse company but is becoming a critical data layer in the process of enterprise AI application implementation.

The original text follows:

May 28—Snowflake's stock surged more than 33% on Thursday. The company previously raised its full-year revenue forecast and announced a $6 billion cooperation agreement with Amazon, bolstering investor confidence in its position as a key beneficiary of the AI boom.

This five-year agreement with Amazon Web Services (AWS) will secure a crucial supply of AWS Graviton chips for Snowflake. Currently, computing resources are becoming increasingly scarce as AI usage grows substantially.

The agreement will also further deepen the integration between Snowflake's data storage, processing, and analytics products and AI workloads on the AWS cloud. As enterprises rapidly scale their AI applications, Snowflake is poised to capture more demand. Currently, most of Snowflake's customers run on AWS.

Following the announcement, at least 30 analysts raised their price targets for Snowflake, pushing the median target price from $230 before Wednesday's earnings report to $280. The stock was last trading at $233.50 in early trading.

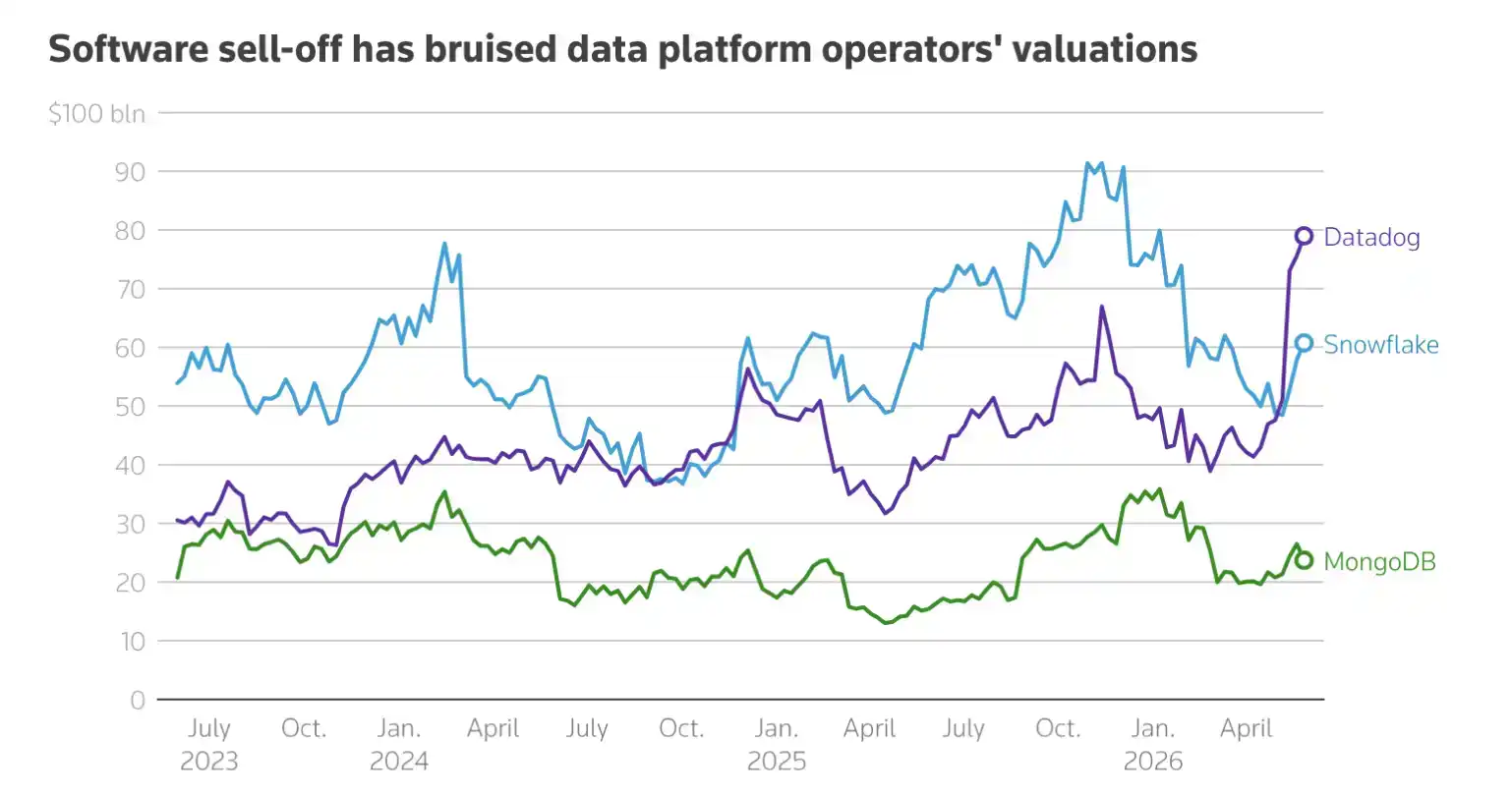

If the current gains hold, Snowflake's market value would increase by approximately $20 billion from its previous $607.5 billion.

Matt Britzman, a senior equity analyst at Hargreaves Lansdown, stated that Snowflake's sharp stock rise—the stock was down 20% year-to-date before the previous trading day's close—"shows how much skepticism had built up during the wider AI software sell-off that hit data names."

"But it also shows how quickly sentiment can turn once a company proves AI is already driving revenue rather than just being PowerPoint filler."

Currently, Snowflake's forward 12-month price-to-earnings ratio is 85.21 times, compared to 85.19 times for Datadog and 47.17 times for MongoDB. A higher P/E ratio typically indicates investors are betting on stronger future growth.

Previously, market concerns that AI would disrupt enterprise software put pressure on Snowflake. Now, the company is embedding AI into its platform, helping businesses integrate data from multiple sources, perform analysis, and build AI tools.

"We believe this set of results puts Snowflake squarely in the 'AI winner' camp and deserves a higher valuation multiple," said Patrick Colville, an equity research analyst at Scotiabank. He added that this clearly indicates Snowflake is benefiting from the growth in enterprise AI adoption.

Snowflake helps businesses store, manage, and analyze all their data on one platform. Its AI tools like Cortex Code and Snowpark are seeing strong adoption. These tools enable enterprises to build generative AI applications based on their own data and deploy machine learning models.

This agreement also serves as another vote of confidence in Amazon's in-house chip business. In recent months, Amazon has secured several significant customers, including Anthropic, OpenAI, Facebook parent Meta, and Uber.