Author: David Hoffman

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Are most tokens garbage? Bankless co-founder David Hoffman points out that historically, teams have treated tokens far less seriously than equity, and the market has responded to this through token prices.

But 2026 saw a turning point:

MegaETH locked 53% of its tokens in a KPI plan, which only unlocks upon achieving growth targets;

The Cap protocol replaced governance token airdrops with stablecoin airdrops, allowing only real investors to obtain CAP through token sales.

These innovative strategies are ending the era of "spray-and-pray" token distribution, shifting towards precise, conditional allocation mechanisms.

Full text as follows:

The crypto industry has a "good coins problem".

Most tokens are garbage.

Most tokens are not treated with the same legal and strategic seriousness as equity by their teams. Because teams have historically not given tokens the same respect as equity in traditional companies, the market has reflected this in token prices.

Today I want to share two sets of data that make me optimistic about the state of tokens in 2026 and beyond:

- MegaETH's KPI Plan

- Cap's Stablecoin Airdrop (Stabledrop)

Conditional Token Supply

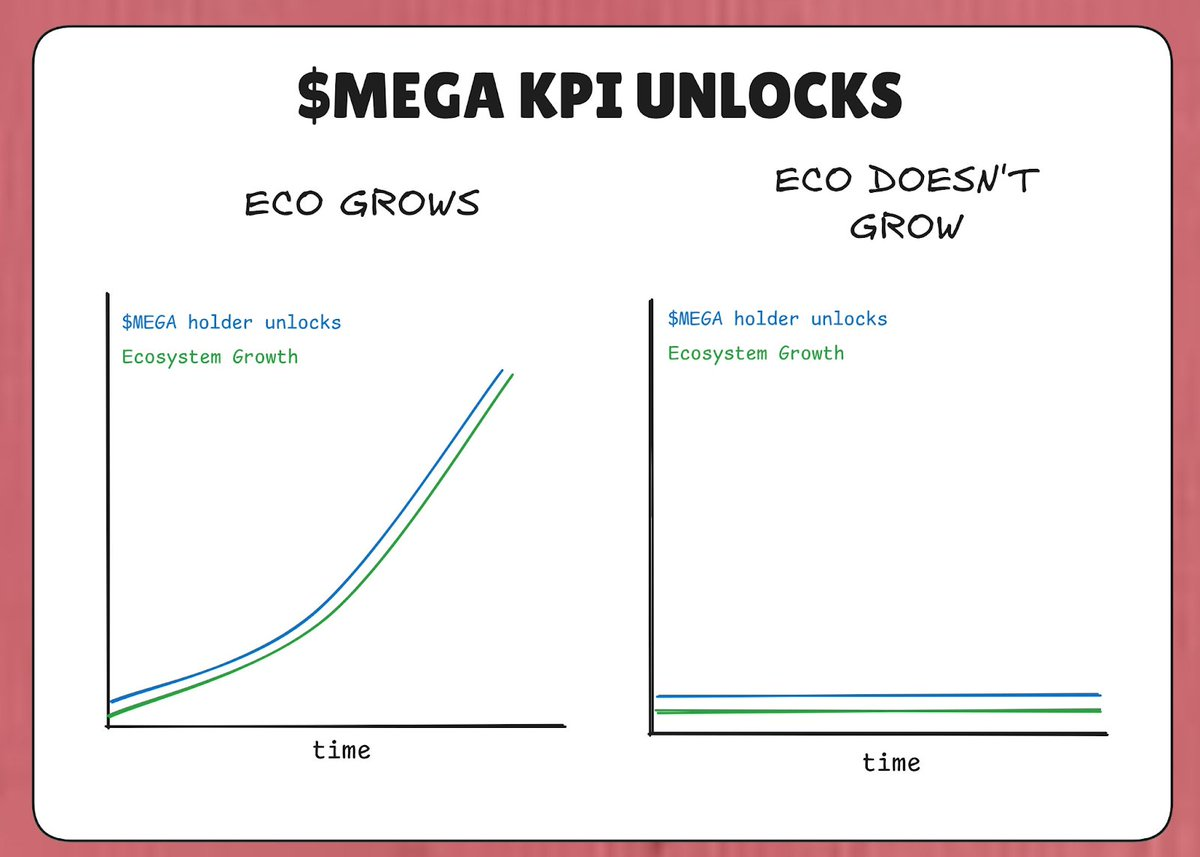

MegaETH has locked 53% of the total MEGA token supply in a "KPI Plan". The logic is: if MegaETH does not achieve its KPIs (Key Performance Indicators), these tokens will not unlock.

Therefore, in a pessimistic scenario where the ecosystem does not grow, at least no additional tokens flood the market to dilute holders. MEGA tokens only enter the market when the MegaETH ecosystem actually achieves growth (as defined by the KPIs).

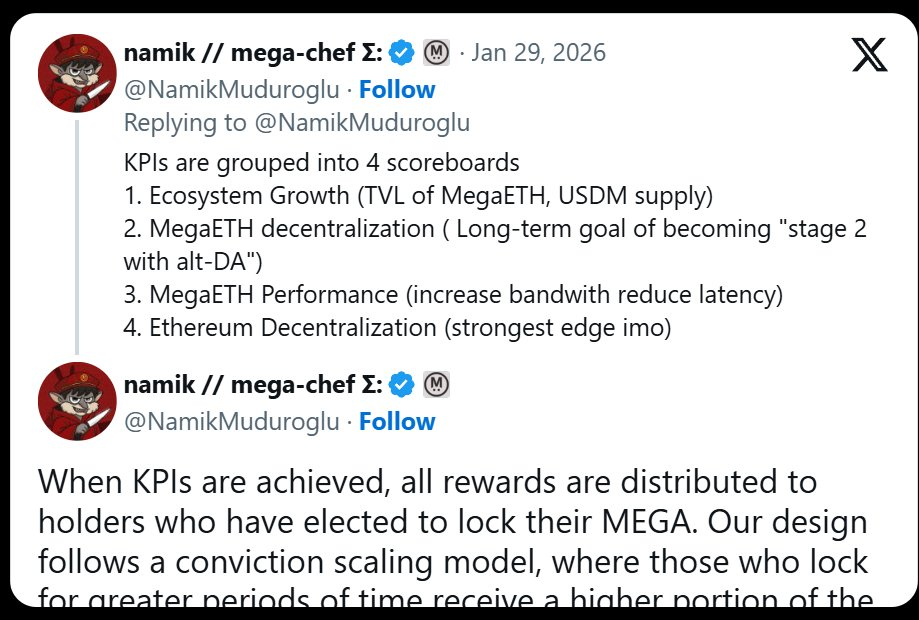

The KPIs for this plan are divided into 4 scoreboards:

- Ecosystem Growth (TVL, USDM supply)

- MegaETH Decentralization (L2Beat stage progress)

- MegaETH Performance (IBRL)

- Ethereum Decentralization

Thus, in theory, as MegaETH achieves its KPI targets, the value of MegaETH should grow correspondingly, mitigating the negative price impact of MEGA dilution on the market.

This strategy is very similar to Tesla's "pay for performance" compensation philosophy for Elon Musk. In 2018, Tesla granted Musk an equity compensation package that vested in tranches, only payable if Tesla simultaneously achieved increasing market capitalization targets and revenue targets. Elon Musk only gets paid if Tesla's revenue grows AND its market capitalization grows.

MegaETH is trying to transplant the same logic into its tokenomics. "More supply" is not a given—it's something the protocol must earn by scoring real points on meaningful scoreboards.

Unlike Musk's Tesla benchmarks, I don't see anything in Namik's KPI targets about MEGA market cap as a KPI target—perhaps for legal reasons. But as a public MEGA investor, this KPI is very interesting to me. 👀

Who Gets the Unlock Matters

Another interesting factor of this KPI plan is: who gets the MEGA when KPIs are met. According to Namik's tweet, the recipients of the unlocked MEGA are those who stake MEGA into the locking contract.

Those who lock more MEGA for longer periods receive a larger share of the 53% MEGA tokens entering the market.

The logic behind this is simple: allocate MEGA dilution to those who have already proven themselves as MEGA holders and are interested in holding more MEGA—those least likely to become MEGA sellers.

Alignment and Trade-offs

It's worth emphasizing that this also introduces risks. We have seen historical cases where similar structures went seriously wrong. Look at this excerpt from Cobie's article: "(content)"

If you are a token pessimist, a crypto nihilist, or just bearish, this alignment problem is what you worry about.

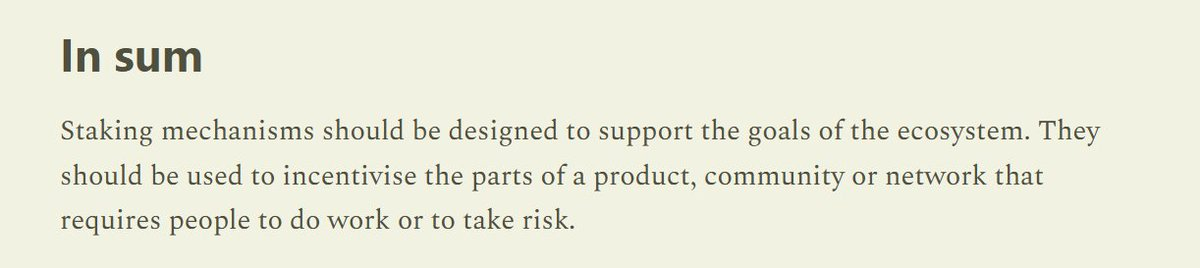

Or, from the same article: "Staking mechanisms should be designed to support the goals of the ecosystem"

Locking token dilution behind KPIs that should actually reflect growth in the value of the MegaETH ecosystem is a much better mechanism than any vanilla staking mechanism we saw in the 2020-2022 liquidity mining era. In that era, tokens were being issued regardless of the team's fundamental progress or ecosystem growth.

Therefore, the net effect is that MEGA dilution is:

- Conditionally constrained by corresponding MegaETH ecosystem growth

- Diluted into the hands of those least likely to sell MEGA

This does not guarantee that MEGA value will rise as a result—the market will do what the market wants. But it is an effective and honest attempt to fix a core underlying problem that seems to plague the entire crypto token industrial complex.

Treating Tokens as Equity

Historically, teams have been "spraying and praying" their tokens across the ecosystem. Airdrops, mining rewards, grants, etc.—teams would not engage in these activities if they were distributing something truly valuable.

Because teams distributed tokens like worthless governance tokens, the market priced them as worthless governance tokens.

You can see the same philosophy in MegaETH's stance on CEX listings after Binance opened MEGA token futures on its platform (historically Binance's attempt to extort teams):

Hopefully, teams will start being more selective with their token distribution. If teams start treating their tokens as precious, perhaps the market will respond in kind.

Cap's Stablecoin Airdrop

The stablecoin protocol Cap introduced a "stablecoin airdrop" (stabledrop) instead of a traditional airdrop. Instead of airdropping the native governance token CAP, they distributed the native stablecoin cUSD to users who earned Cap points.

This approach rewards points farmers with real value, thus fulfilling the social contract. Users who deposited USDC into Cap's supply side accepted smart contract risk and opportunity cost, and the stablecoin airdrop compensated them accordingly.

For those who want CAP itself, Cap is conducting a token sale via a Uniswap CCA. Anyone seeking CAP tokens must become a real investor and commit real capital.

Filtering for Committed Holders

The combination of a stablecoin airdrop plus a token sale filters for committed holders. A traditional CAP airdrop would flow to speculative farmers likely to sell immediately. By requiring a capital investment through the token sale, Cap ensures CAP flows to participants willing to accept full downside risk for upside potential—a group more likely to hold long-term.

The theory is that this structure gives CAP a higher probability of success by creating a concentrated holder base aligned with the protocol's long-term vision, rather than a less precise airdrop mechanism that puts tokens into the hands of those focused solely on short-term profits.

Watch this video:

https://x.com/DeFiDave22/status/2013641379038081113

Token Design is Maturing

Protocols are getting smarter and more precise with their token distribution mechanisms. No more shotgun spray-and-pray token issuance—MegaETH and Cap are choosing to be highly selective about who gets their tokens.

"Optimizing for distribution" is no longer the thing—perhaps a toxic hangover from the Gensler era. Instead, these two teams are optimizing for concentration to provide a stronger foundational holder base.

I hope that as more apps launch in 2026, they can observe and learn from these strategies, and even improve upon them, so the "good coins problem" is no longer a problem, and we are left with only "good coins".