A new Bitcoin Policy Institute (BPI) report argues that nation-state engagement with Bitcoin has moved beyond legal-tender experiments into a broader set of “exposure” pathways—from strategic reserves and sovereign mining to pensions, sovereign wealth funds and tax acceptance—marking what the authors describe as a game-theoretic race among governments.

Nation-State Bitcoin Adoption Accelerates

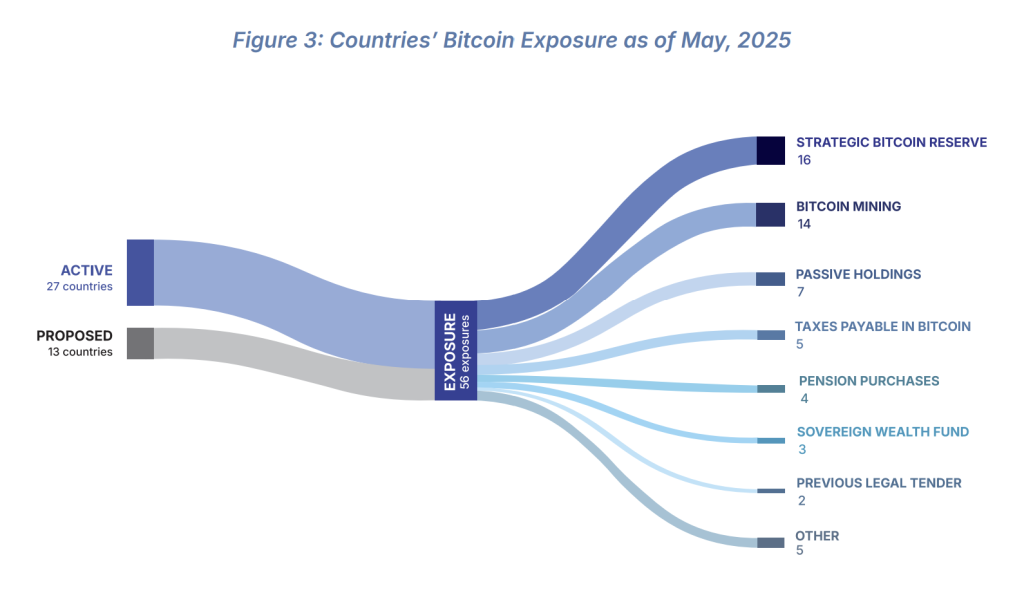

The study, authored by Jake Langenkamp and Renee Sorchik and on September 22, 2025, concludes that “27 countries currently have some measure of exposure to bitcoin—approximately one in seven worldwide,” with a further “13 countries [that] have proposed adoption measures through legislation or policy initiatives.”

The report is explicit about scope and definitions. “Exposure was defined as any official path a government may take to own, earn, or generally benefit from bitcoin,” a framework that deliberately looks beyond the narrow question of legal tender to capture the diversity of sovereign approaches now evident across regions and political systems.

The authors treat sub-national pilots—such as state-level reserves or municipal tax programs—as valid instances of nation-state exposure because they can scale into national policy. Data collection closed on June 6, 2025, with first-half 2025 events aggregated as a single period to reflect the late-quarter cadence of announcements.

The topline counts underpin a larger narrative of acceleration. As of end-May 2025, the dataset covers “32 countries—roughly one out of every six nations on Earth—[that] either already had bitcoin exposure or was actively pursuing it through legislation or policy,” subdivided into 27 active and 13 proposed. The authors caution that categories can overlap, with individual countries appearing in multiple modalities; the United Arab Emirates, for example, is noted as combining government-backed mining, sovereign wealth fund ETF purchases, and tax acceptance.

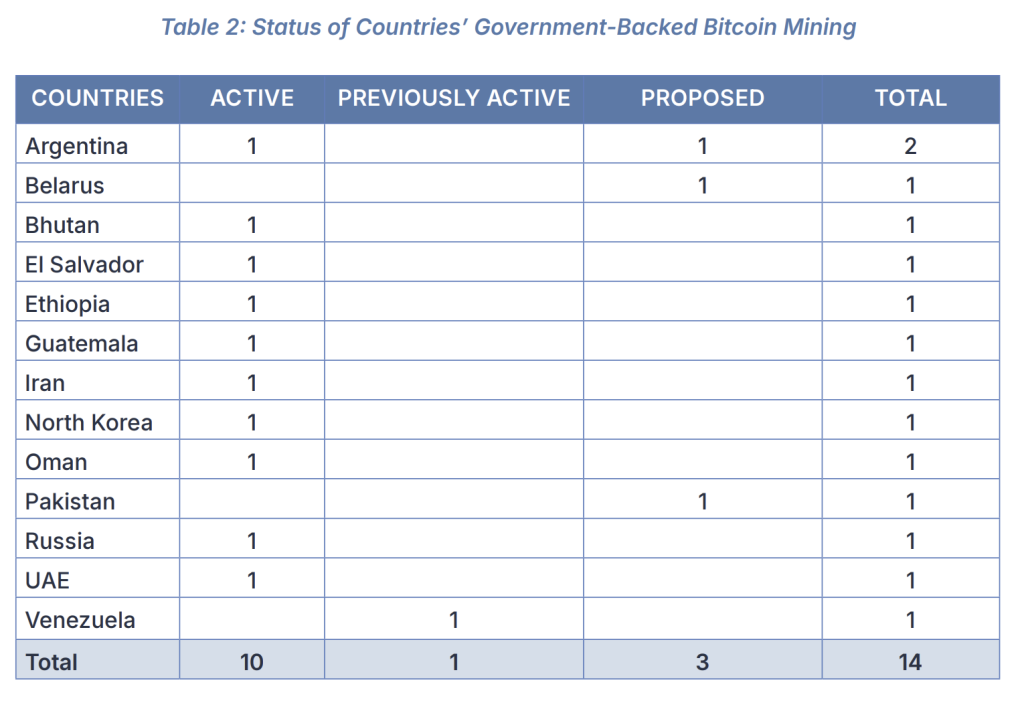

Modalities cluster around a few dominant channels. Counting both active and proposed, the most common is a Strategic Bitcoin Reserve (SBR), identified in 16 countries, followed by government-backed mining (14).

Passive holdings—typically seized assets that authorities have elected not to sell—are recorded in seven countries, while five countries accept certain taxes in bitcoin. Government money managers appear on both sides of the balance sheet: four pension systems and three sovereign wealth funds show direct or indirect exposure, including via equity in BTC-treasury companies.

Two countries are recorded for prior legal-tender status (El Salvador and the Central African Republic), and a handful of country-specific outliers include a government-backed crypto exchange pilot (Russia), a special economic zone recognizing bitcoin as a unit of account (Honduras), and the use of seized BTC for public debt (North Korea).

Different Options For Bitcoin Exposure

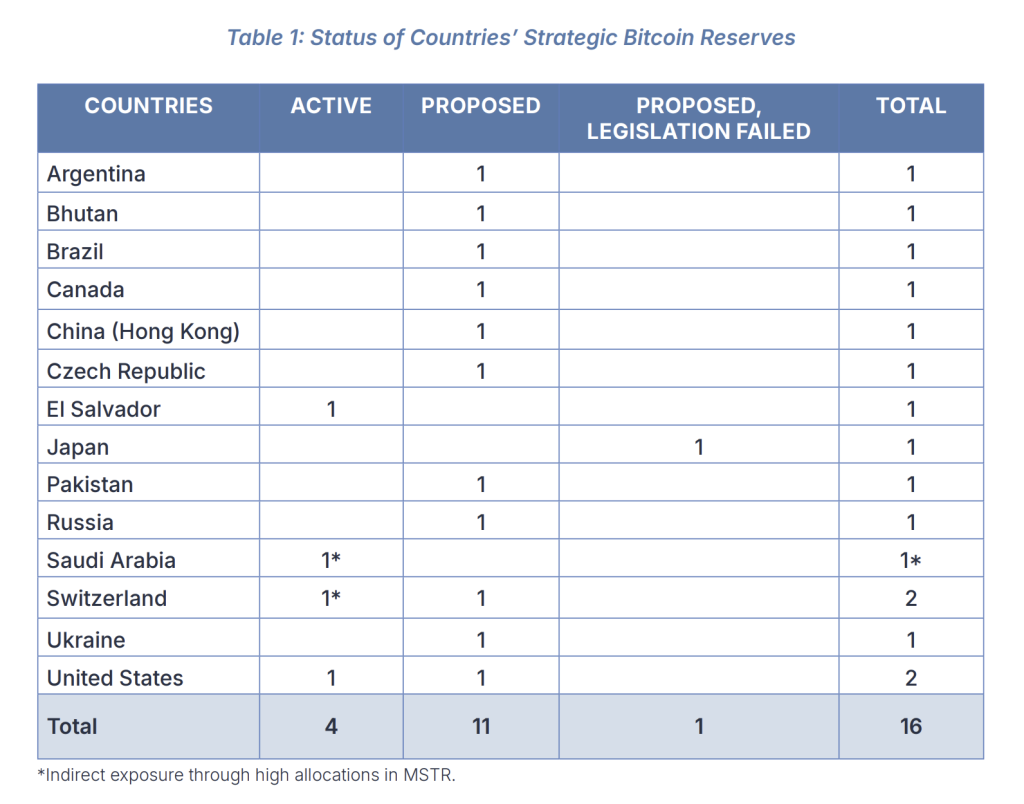

The authors disaggregate what is active today versus what remains on the drawing board. Among active exposures, they identify 11 countries with government-backed mining, seven with passive holdings, four with SBRs, four taking tax payments in bitcoin, and sovereign wealth funds or pensions in a smaller but notable role. Proposed measures skew even more heavily toward SBRs: “12 of the 13 countries” with proposals target a reserve model, alongside limited proposals for mining, pensions and tax acceptance.

A short list illustrates the reserve spectrum the report captures. “Four countries were classified as having active strategic bitcoin reserves.” In the United States and El Salvador, reserves are “more traditional,” with direct holding and/or accumulation. By contrast, the central banks of Switzerland and Saudi Arabia are classified as having indirect reserves through “large positions in MSTR,” reflecting the authors’ broader definition of indirect exposure via equity in bitcoin-treasury companies.

The study situates El Salvador as an early legal-tender mover that subsequently emphasized balance-sheet accumulation. It recounts that El Salvador “has amassed approximately 6,100 BTC,” and notes policy adjustments around merchant acceptance, underscoring the authors’ point that legal tender is only one, and not necessarily the most durable, channel for national adoption. “As these examples show, legal tender status is not the only route for nation state adoption. Sovereign custody, institutional purchasing, and strategic program design may prove more durable paths.”

The United States anchors a separate thread in the dataset. The authors describe US President Donald Trump’s Executive Order that “differentiated bitcoin from other cryptocurrencies and set a policy of retaining, rather than selling, bitcoin holdings,” framing an SBR architecture and, per the report’s executive summary, catalyzing copy-cat proposals abroad. They add that “sixteen nations have now proposed or enacted legislation for SBRs in a similar context to the US,” and that multiple North American municipalities and international cities have moved to accept taxes in BTC.

Passive holdings, while not proactive policy, are treated as policy-relevant because non-liquidation signals an evolving treasury stance. The report lists Bulgaria, China, Finland, Georgia, India, the United Kingdom and Venezuela as countries with seized BTC presumed to remain on government books. “While accumulation through seizure is not a proactive strategy, the noteworthy aspect of passive holdings is that they have yet sold the bitcoin,” the authors write.

The taxonomy is complemented by a methodological note on inclusions and exclusions. Rumors and campaign-only promises are filtered out, and the study introduces a direct versus indirect exposure lens: direct holdings, ETFs or mining on one side; on the other, exposures “such as equity positions in bitcoin-treasury companies like MicroStrategy (MSTR).” This framework allows Switzerland and Saudi Arabia to appear as reserve holders despite the route being portfolio equity rather than on-chain coins.

The report’s conclusion elevates the macro implications. Bitcoin, it argues, is “a new macroeconomic asset, the first of its kind in more than a century.” Early adopters may reap portfolio and financing advantages: the authors discuss “Bit-Bonds,” in which BTC functions as partial collateral to attract institutional demand and potentially lower sovereign borrowing costs, and posit that bitcoin-based settlement bridges could reduce cross-border frictions. The underlying thesis is that momentum in 2024–2025—captured in the study’s timeline and counts—makes a wholesale reversal improbable as more jurisdictions institutionalize bitcoin in public-finance workflows.

At press time, BTC traded at $112,490.

Related Posts