“We are witnessing the birth of Bretton Woods Ⅲ.”

Recently, Zoltan Pozsar, a well-known analyst at UBS, made a surprising statement, believing that under the background of the Russian- Ukrainian War and sanctions in western countries, that the global commodity crisis is brewing and the new global monetary system- Bretton Woods Ⅲ is coming.

More interestingly, Zoltan made a point at the end of his report: “Bitcoin will probably benefit from all this.”

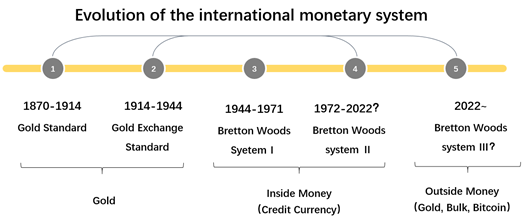

In fact, once the hot words terms such as “Russia- Ukraine War” and “the hegemony of dollar” are linked with the grand historical proposition of Bretton Woods attention from the market is sure to follow. From an international monetary system evolution perspective, the global monetary system experiences a small cycle in search of a currency anchor every 40 years and a large cycle every 80 years. Each collapse of the currency anchor triggered severe economic turmoil and political crises around the world, and there is a 10-20 year boom period after the anchor search ends. We now seem to be at the crossroads of a “sea change” in the global monetary system. Therefore, we could explore the future of The Bretton Woods system and cryptocurrency from the historical evolution of the international monetary system.

Figure 1. Evolution of the International Monetary System

1 The establishment and collapse of the Gold Standard(1870-1944)

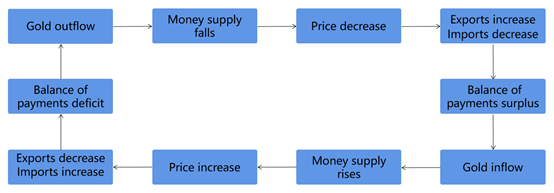

Since the middle of the 19th century, Britain, the United States, Germany and other major economies began to implement the Gold Standard, and the international Gold Standard was formally established. Under the Gold Standard, gold is the anchor of all national currencies, and exchange rates are set according to the ratio of the gold content of each currency. The

existence of gold anchor limits the fluctuations of international exchange rates within a limited range, resulting in the stability of exchange and the automatic adjustment of international balance of payments. During the period from 1870 to 1914, the world economy showed a high degree of exchange rate stability, low inflation and stable economic growth.

Figure 2. Automatic balance of payments adjustment under the Gold Standard

This period was also called the “Golden Age” and “Industry Age” of the American economy and saw the start of the rise of modern America. During this period, the American economy showed spectacular growth: in the mid 1880s, America’s GDP reached US$11 billion. By the end of World War 1, it had reached US$84 billion, an eightfold increase. On the industrial side, by the beginning of the 20th century, the combined output of American manufacturing exceeded the sum of the UK, Germany and France combined. At this point, the United States became the largest industrial nation and the richest country in the word.

Figure 3. 1869 The Pacific Railroad was completed

However, the outbreak of the First World War devastated international trade and the Gold Standard began to collapse. After the end of First World War, the European economy was severely damaged and the main capitalist countries such as Britain and France changed from creditor countries pre-war to debtor countries post-war, while the United States became the largest creditor of European countries. In this case, the original Gold Standard was difficult to restore, as European countries had to use Gold Exchange Standard to save the use of gold. Under the Gold Exchange Standard,bank notes in circulation could not be exchanged for gold — only foreign currency was allowed.

However, the Great Recession of 1929 and the subsequent Second World War devastated the global economy. In order to cope with the depletion of gold reserves and the speculative impact of currencies, all countries stopped exchanging gold and allowed their currencies to float freely. At this point, the world’s major economies abandoned the Gold Standard.

2 The First Search for Anchor: Post-war Global Economic Recovery and the Establishment of the Bretton Woods System (1944-1971)

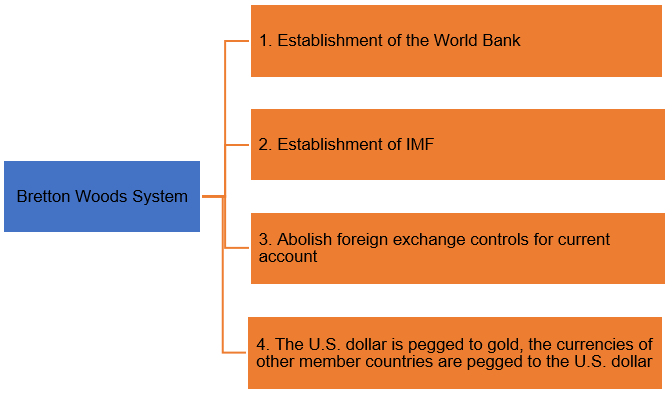

After World War II, the United States became the most powerful country in the world, accounting for 50% of global GDP and 63% of global gold reserves. Across the Atlantic, Europe was devastated by the war and heavily indebted. In order to rebuild the international financial order, 44 allied countries around the world held a meeting in Bretton Woods, to make arrangements for the exchange of currencies, the adjustment of the balance of payments, and the composition of international reserve assets. At this point, the Bretton Woods system was formally established.

Figure 4. The Content of Bretton Woods

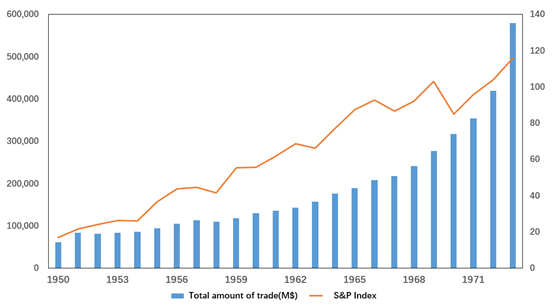

Under the Bretton Woods system, the US dollar was pegged to gold and other countries’ currencies were pegged to the US dollar. Therefore, the US dollar has become the "nominal anchor" in the global monetary system and contributed to the recovery and prosperity of the global economy for a long time after the war. In 1950, the global export amounted to US$62 billion. By 1973, when Bretton Woods was removed, it had reached US$580 billion, with a compound annual growth rate (CAGR) of 15.5%. The US stock market also ushered in a boom era, with the S&P rising from 17.5 in 1950 to 116.03 in 1973, with a CAGR of 8.6%.

The establishment of the Bretton Woods system played a positive role in global economic growth and asset price stability during a significant period in history, but it has serious flaws: under the Bretton Woods system, the US dollar, as the world currency, needs to be continuously issued to meet the needs of the US dollar. Therefore, the demand of the world economy and trade requires the United States to maintain a long-term trade deficit. However, as the currency anchor of the global monetary system, the US dollar must maintain a stable price, which requires the United States reducing the supply of US dollars and maintaining a trade surplus. Otherwise, if foreign holdings of US dollars exceed US gold reserves, it will shake investor confidence in the free exchange of US dollar to gold, which is known as the “Triffin Dilemma.”

Figure 5. The Content of Bretton Woods

Indeed, as the postwar economy recovered, international trade rose rapidly. While the United States was exporting US dollars, its current account deteriorated rapidly. The United States’ external debt began to exceed its gold reserves, which shook investors’ confidence in the smooth exchange of dollars for gold and accelerated the run on American gold. According to statistics, in 1950 after the end of World War II, the United States still held 20,279 tons of gold, accounting for nearly 2/3 of the world's gold reserves; By 1970, the United States held only 9,839 tons of gold, a 51% drop in gold reserves.

In addition, due to the free flow of international capital after the war, the fixed exchange rate system was often attacked by international speculators. In May 1971, a large-scale speculative activity against the US dollar broke out. A large number of speculative capital sold the US dollar and rushed to purchase gold and European currencies. This currency speculative activity aggravated people's expectations for depreciation of the US dollar. In the face of pressure from European central banks and speculators to purchase gold, US President Richard Nixon was forced to announce the closure of the gold exchange window and the termination of the obligation to exchange gold to foreign central banks, which decoupled the US dollar and gold.

Figure 6. Nixon announced the closing of the Gold Window on TV in 1971

In the following two years, the United Kingdom, Switzerland, Japan and other major OECD countries successively announced the implementation of floating exchange rate system, which marked the end of Bretton Woods System I and the beginning of the search for an anchor for the global monetary system.

3 The Second Search for Anchor: Free Floating Exchange Rate and the Bretton Woods System Ⅱ (1971-present)

After the collapse of the Bretton Woods system in the 1970s, in order to maintain the US dollar’s status as the world’s currency, the US government reached an agreement with major oil producing countries such as Saudi Arabia to use US dollars for denomination and settlement in the oil market. In return, US would provide military protection and sell weapons to Saudi Arabia.

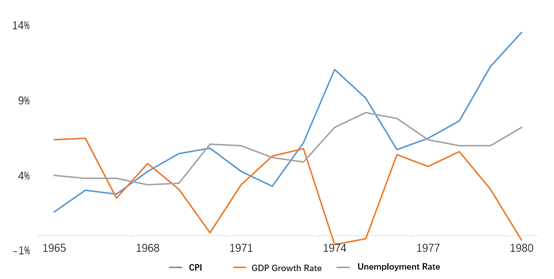

Although the US dollar maintains the status of the world currency through oil trade, due to the loss of the gold anchor, the world's major currencies have fallen into severe fluctuations, which has had a serious impact on the global economy and asset prices. Due to the continuous devaluation of currencies, global commodity prices soared and the western capitalist camp fell into a quagmire of "stagflation" throughout the 1970s.

igure 7. "Stagflation Era" in the US

In order to solve stagflation, Paul Volcker, the new Chairman of Federal Reserve, implemented a strict policy to control high inflation. Since 1980, the money supply was tightened in just five months, and the federal funds rate has risen from 9.5% to 20% during successive interest rate hikes. Eventually, this deflationary monetary policy paid off, with US inflation falling back to 2.5% in July 1983.

Solving the inflation problem, however, only achieves the internal stability of the value of the US dollar. In order to "seek the anchor" successfully, the stability of the external value of the currency, i.e. exchange rate stability, needed to be achieved. To solve this problem, payments imbalances that had plagued the US for years needed to be addressed.

To maintain US’s dominant position in the international currency, the dollar cannot be easily devalued. How then could the US balance of payments be improved while keeping the dollar stable in foreign exchange markets? -- Force the currencies of other countries, especially those with major trade surpluses with the United States, to appreciate. To this end, the United States and Japan and Germany reached the "Plaza Agreement" and "Louvre Agreement", requiring Japan and Germany to strengthen the "intervention coordination" in the foreign exchange market to ensure the stability of the dollar.

Figure 8. Finance Ministers of five countries during plaza Accord

The signing of "Plaza Agreement" and "Floating Palace Agreement" improved the international balance of payments of the United States and maintained the stability of the US dollar’s exchange rate. The US dollar achieved stable inflation at home and a stable exchange rate abroad, and maintained basic stability throughout the 1990s. At this point, the Bretton Woods system II dominated by the US dollar was formally formed, and the global monetary system found a new anchor.

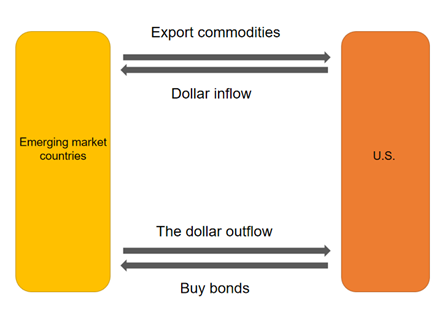

In this system, the dollar acts as the dominant currency, forming a currency basket with currencies such as the yen and the euro, and acting as the monetary anchor for many emerging market countries. Therefore, countries with emerging markets have to continue to hold down the exchange rate in order to obtain favorable exchange rates, increase exports to the US, and invest huge foreign exchange reserves in the United States to buy government bonds (to achieve foreign exchange preservation and appreciation), thus providing financing for the U.S. trade deficit. As a result, the circulation of the dollar in the world was formed.

Figure 9. The global circulation of US dollars under Bretton Woods II

4 The Third Anchor Search: Global Imbalances and the Bretton Woods System III (2022?)

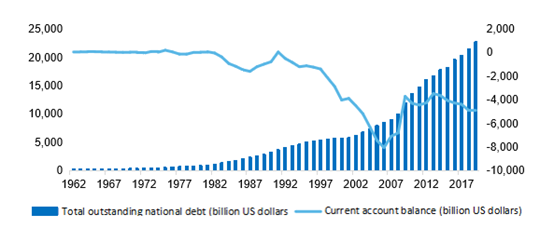

Although the global economy has ushered in a golden age after the second anchor search, the real problem has not been solved. Even if the United States can use its power to force the appreciation of the currencies of Japan and Germany, it has never been able to completely solve the U.S. trade balance issue. Because the international monetary system dominated by the US dollar has a fundamental flaw: The dollar's role as both a sovereign and a world currency would throw the global economy into a state of extreme imbalance.

The US uses cheap US dollars to buy commodities from developing countries, and developing countries use these US dollars to buy US treasury bonds, thus forming a return of US dollars; however, as long as the Federal Reserve starts the money printing machine, developing countries face the risk of shrinking foreign exchange assets. Correspondingly, the developed countries represented by the United States are also facing serious challenges: due to the high quality and low price of commodities in developing countries, the domestic manufacturing industry in the United States has been hit, and a large number of American workers have lost their jobs, resulting in the emergence of the famous "rust belt". In contrast, the financial services industry represented by Wall Street has made a lot of money in the process of globalization.

Figure 10. Changes in U.S. current account deficit and outstanding national debt

Source. Wind

It is the serious flaws in today's global monetary system that have caused the imbalances and unequal distribution of the global economy, triggering the current "de-globalization", the rise of populism, and the transfer of international political and economic power - The inauguration of Donald Trump, the rise of the Right in Europe, the sino-US trade war and the Russia-Ukraine war, all these are not accidental. There are profound economic reasons behind them.

Bretton Woods II is now facing another major challenge: the destruction of the global monetary system by the geopolitical crisis. As the Russian-Ukrainian conflict erupted, the US imposed financial sanctions on Russia - freezing the Russian central bank's foreign exchange reserves. This measure is just like a unilateral default on creditors, seriously shaking global trust in the dollar, which is the cornerstone of Bretton Woods II. In the long run, the abuse of financial sanctions by the United States will prompt some countries to reconsider the structure of foreign exchange holdings, which will gradually weaken the hegemony of the dollar and its status as the world's reserve currency.

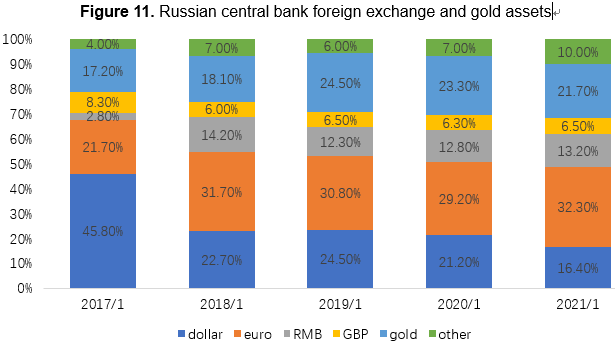

The Russian-Ukrainian war can be traced back to the Crimean crisis eight years ago, and the disintegration of the Bretton Woods System II may have also appeared earlier. As recently as after the Crimean crisis in 2014, Europe and the United States had already imposed economic sanctions on Russia. After the sanctions, Russia's gross national product plummeted, and the Ruble’s exchange rate also depreciated sharply. So far, the Russian government has begun to implement de-dollarization in a planned way: in terms of the foreign exchange reserves of the Russian central bank, the share of U.S. dollar reserves has dropped from 45.8% in 2017 to the current 16.4%; in terms of sovereign wealth funds, as of 2021, Russia’s Sovereign wealth funds have completely eliminated US dollar assets.

Source. BOR

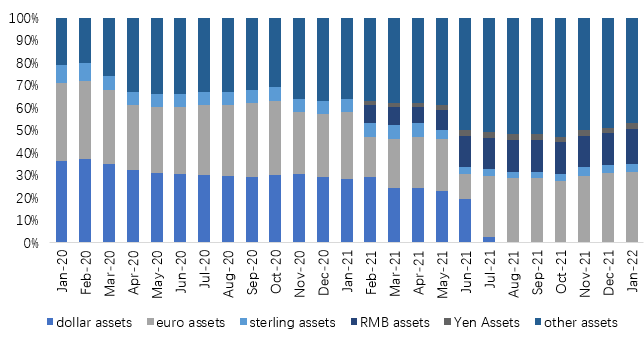

Figure 12. Changes in assets held by Russian sovereign wealth funds

Source. Haver

So what does Zoltan mean when he says Bitcoin will probably benefit from all this? After the outbreak of the Russian-Ukrainian war, the sanctions imposed by Europe and the United States on Russia mainly reflect two major problems: First, the financial system rooted in Europe and the United States is not secure. As long as the European and American countries freeze Russia’s bank accounts in their own countries and remove Russia from the SWIFT system, they can freeze Russia's own assets and hinder Russia's cross-border payment activities; secondly, "Inside Money" dominated by European and American countries is not safe. To ensure the safety of domestic wealth, "exogenous currency" (or Outside Money)) became one of the options.

Cryptocurrencies, such as Bitcoin, can solve this problem.

First of all, in the current international clearing system, cross-border payment relies heavily on the account system. Users need to open accounts with banks, and overseas banks need to open accounts with domestic agents and overseas clearing banks, etc. However, cryptocurrencies themselves are based on digital wallets and have the characteristics of loosely-coupled bank accounts, which do not need to be tied to related bank accounts, nor do transaction transfers depend on bank accounts. Thus, as geopolitical conflicts intensify and countries become increasingly concerned about the security of their foreign exchange reserves, cryptocurrencies, especially cross-border stable coins (including CBDCS developed by central banks), have the potential to transform the current cross-border payment landscape based on correspondent and clearing bank relationships scattered across the globe and time zones.

Second, cryptocurrencies are "Outside Money" in a broad sense. Specifically, endogenous money is the "controllable money" belonging to the debts of central banks and other financial institutions (such as cash, bank deposits and mutual market funds), while exogenous money is the "uncontrollable money" belonging to no one's debts (such as gold and bitcoin). Countries may move away from holding reserves in the form of fiat currencies to gold, cryptocurrencies and other commodities (such as oil) as new reserve assets in an effort to keep free from others’ control in the future.

Although it seems like a fantasy that Bitcoin will become a foreign exchange reserve in the future, but from a practical point of view, it is not impossible.

In the current international monetary system, the sovereign currency of a single country, as the currency anchor, has proven to be unstable and unreliable. Because in the context of intensified geopolitical conflicts, the endogenous currency, as a debt-based credit currency, can no longer simply be judged by the country's economic, political, and military strength as the basis for whether the currency is trustworthy. In addition, the conflicts between various countries are continuous, and the notion of a super-sovereign currency as a currency anchor has become an unrealistic fantasy.

As a result, the monetary anchor of the future may revert to a stage dominated by "endogenous currencies". The fundamental reason for the collapse of the gold standard was that gold production grew at a much slower rate than global trade. However, in the 21st century, as the financialization of commodities deepens and cryptocurrencies such as Bitcoin become more and more accepted, it is not impossible for both sides to become an alternative to gold.

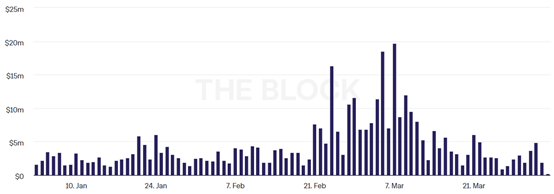

Indeed, shortly after the US and Europe imposed financial sanctions, Russia announced that it was considering accepting Bitcoin as payment for its oil and gas exports, and BTC/RUB transactions began to surge.

Figure 13. BTC/RUB volume surges during the war

Source. The block

Of course, the establishment of any new order does not happen overnight. Historically, the global monetary system has gone through a minor anchor-seeking cycle every 40 years and a major anchor-seeking cycle every 80 years. Although we are currently seeing the collapse of the old order and the birth of a new world, it is difficult to give a more detailed description of Bretton Woods III. Because in this uncertain world, no development can be guaranteed.

Disclaimer

1. The author of this report and his organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report.

2. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment and other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report, unless clearly stipulated by laws and regulations. Readers should not only make business and investment decisions based on this report, nor should they lose their ability to make independent judgments based on this report.

3. The information, opinions and inferences contained in this report only reflect the judgments of the researchers on the date of finalizing this report. In the future, based on industry changes and data and information updates, there is the possibility of updates of opinions and judgments.

4. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the source. If you need a large amount of reference, please inform in advance (see “About Huobi Blockchain Research Institute” for contact information), and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original intent.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the source. If you need a large amount of reference, please inform in advance (see “About Huobi Blockchain Research Institute” for contact information), and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original intent.

About Huobi Research Institute

Huobi Blockchain Application Research Institute (referred to as "Huobi Research Institute") was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain. As the research object, the research goal is to accelerate the research and development of blockchain technology, promote the application of blockchain industry, and promote the ecological optimization of the blockchain industry. The main research content includes industry trends, technology paths, application innovations in the blockchain field, Model exploration, etc. Based on the principles of public welfare, rigor and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms to build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical basis and trend judgments to promote the healthy and sustainable development of the entire blockchain industry.

Consulting email:

research@huobi.com

Official website:

https://research.huobi.com/

Twitter: @Huobi_Research

https://twitter.com/Huobi_Research

Medium: Huobi Research

https://medium.com/huobi-research