Enabling Withdrawals

Ethereum’s next hardfork, Shanghai, is anticipated in the late first quarter or early second quarter of 2023. Although several Ethereum Improvement Proposals (EIPs) were initially considered for integration, including numerous EVM object format upgrades and EIP 4844, commonly known as Proto-Danksharding, these proposals were deferred until the subsequent hardfork, Cancun. At present, the Shanghai hardfork will be composed solely of EIP 4895, which pertains to Beacon Chain withdrawals.

Beacon Chain withdrawals complete the three part process of Ethereum’s transition to a proof-of-stake consensus mechanism:

December 1st, 2020 the Beacon Chain launches, running alongside Ethereum’s proof-of-work system.

September 15th, 2022 the execution and consensus layers are merged, and blocks begin to be validated under Ethereum’s new proof-of-stake system.

In Q1 or Q2 of 2023 withdrawals will be enabled, allowing validators to queue up to exit their stake; the last stage in Ethereum’s transition.

Currently all staking revenue is theoretical yield; it cannot be realized. Risk averse players, including those with large amounts of capital, are likely hesitant to stake significant portions of their Eth without a way to realize their gains. The availability of withdrawals is anticipated to address this issue and incentivize greater participation in staking.

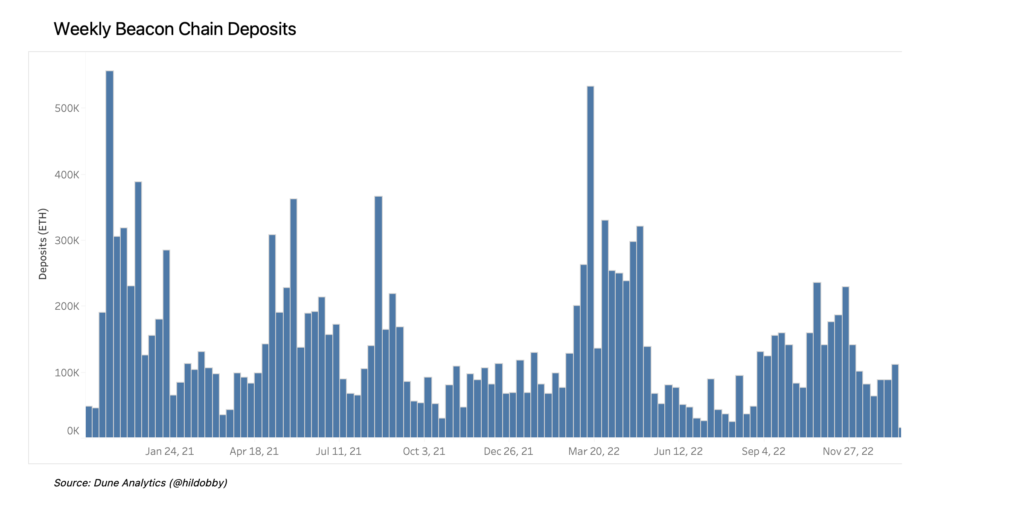

The above chart shows weekly Beacon Chain deposits. To date, the largest week for staking deposits remains the Beacon Chain launch, with the second largest occurring in March of 2022 after Aave allowed uncapped, deep leverage on Lido’s stEth.

Additionally, we can see that the successful merge on September 15th, and subsequent staking risk reduction, had no visual impact on staking demand.

A full two years after launch, less than 14% of Eth has been deposited onto the Beacon Chain; compared to Binance Smart Chain with 97% of their native token, Cardano with 72%, Solana with 71%, and Avalanche with 63%. Because Eth has more utility, evidenced by Ethereum’s significant blockspace demand and protocol fees, we don’t expect the percent of stake to reach similar levels as alt L1s. However, some significant increase should be expected.

LSDs

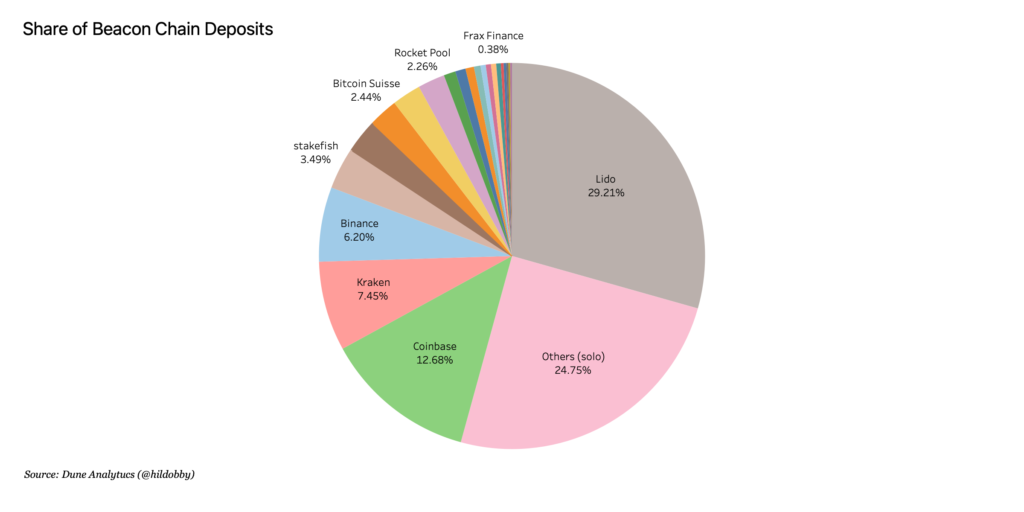

Currently, the majority of staked ETH is split across Lido, solo operators, Coinbase, Kraken, and Binance. Some of this staked Eth is represented as liquid staking derivatives, while some is abstracted away as passive yield.

It’s impossible to concretely sort ‘Others’ into minor pools and solo node operators. However, the vast majority are estimated to be independent individuals, as all significant pools have otherwise been accounted for in the data.

Shanghai will enable solo node operators and pool participants to queue up for exit. This will cause a massive reshuffling, as there are now more staking players, and more staking concerns since the Beacon Chain launched in December 2020. As it stands today, there are only a handful of sizeable ERC20 tokens indirectly capturing staking pool value, largely dependent on their liquid staking derivative:

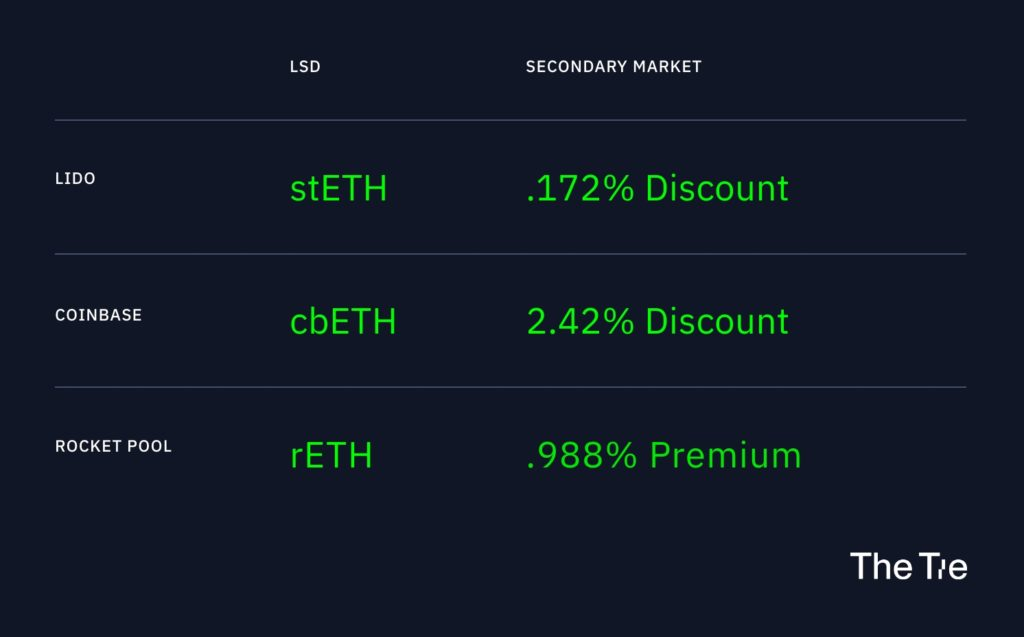

The pools in the Beacon Chain have varying market shares, each with unique business models, token economics, principles, and public perception. It’s worth noting that the demand for LSDs, in part, can be gauged by the premium or discount on the secondary market compared to Eth.

Because withdrawals aren’t enabled and it’s not possible to exit at the protocol level, and because LSDs are freely tradeable on secondary markets, one can measure the market’s desire to enter and exit a given LSD position. The delta between primary and secondary markets is a transitory phenomenon that is expected to converge towards zero after the implementation of the Shanghai Upgrade.

Furthermore, one must consider the protocol’s fundamentals and how they onboard Eth.

Scaling and Reshuffling

At present, holders of liquid staking derivatives can only adjust their positions on secondary markets. Data from these secondary markets can provide insight into where the market wants to go, given withdrawals are enabled.

For instance, cbEth trades at a significantly larger discount compared to all other LSDs. Is this due to a comparatively greater risk profile or are there other factors at play? Why, for instance, doesn’t cbEth’s discount resemble stEth’s, given their similar centralization risk factors?

Coinbase does not have a native token, and is unable to incentivize liquidity and adoption of its LSD token across Ethereum DeFi in the same way Lido is. Given that stEth Curve pools payout significant LDO rewards, it’s not surprising that a user with a tolerance for centralization risk would prefer stEth over cbEth.

By this logic, we have at least two factors influencing current LSD discount and premium values:

1.Perceived Risk

2.Temporary Liquidity Incentives

Enabling withdrawals will impact LSD providers in vastly different ways. Of all the major players, only Rocket Pool allows for permissionless onboarding of node operators and will be poised to significantly benefit from the migration of solo node operators.

Below, we’ll show several token specific factors that further influence these prices.

Frax

Frax is a relatively new entrant into the LSD competition, whose main advantage is ownership of liquidity directing tokens like veCRV. By boosting their LSD’s yield with these liquidity tokens, Frax hopes to replicate their stablecoin success in sfrxEth.

Their LSD competes with their other yield bearing assets and strategies; all reliant on protocol owned liquidity bribing tokens. To that extent, Frax’s ability to onboard additional sfrxEth is largely dependent on its ability to outperform FRAX, its own stablecoin, which earns its yield across many DeFi protocols.

In other words, their success in other aspects of their own protocol could hinder their LSD adoption.

That said, the sticker return on sfrxEth is necessarily higher than any other LSD, as it automatically incorporates some secondary DeFi yield on top; compared to stEth, cbEth, or rEth, who’s DeFi yield must be sourced by the individual after minting.

Rocket Pool

There are two primary reasons rEth trades at a premium. Firstly, the Rocket Pool design limits the issuance of rEth by the number of validators in the network. This technical limitation puts a soft cap on supply, and forces prospective buyers to pursue rEth on the secondary market. Secondly, their decentralized, permissionless, and trustless nature is widely perceived as safer than larger centralized alternatives, resulting in higher demand for their LSD.

In conjunction with Shanghai, Rocket Pool is releasing a protocol upgrade that triples the amount of rEth that may be minted by staked node operator Eth, known as LEB8s, or “lower Eth bonded” minipools. In other words, for every 16 Eth brought in by a validator, Rocket Pool will be able to mint 48 rEth.

Currently, these two values are equivalent, with 16Eth needed to mint 16 rEth. As such, even if Rocket Pool fails to attract additional validator capital, they’re well positioned to substantially increase their rEth supply with little effort.

Before Shanghai, a Rocket Pool protocol upgrade will allow solo node operators to easily transition their validators to Rocket Pool minipools, who will have a monetary incentive to do so in the form of increased Eth commission and RPL rewards.

While it would be unreasonable to expect the majority of the operators to migrate, some significant portion are likely to. As shown in the second figure, solo operators represent nearly ¼ of all staked Eth.

Coinbase & Lido

Coinbase and Lido, on the other hand, face no such onboarding limitations, as they both have centralized operators able to stake effectively infinite Eth. If a user wants to mint cbEth or stEth, these organizations do not need to build out or attract additional node operators; they simply deposit their customer’s Eth onto an existing validator.

Lido had a significant advantage as a first mover and was quickly adopted by major players in the Ethereum DeFi space, including Chainlink, Maker, Aave, Compound, and others. This virtuous cycle, driven by the incentives of its governance token LDO, allowed Lido to solidify its position as a leading provider of liquid staking derivatives.

With near unlimited infrastructure and a discounted staking derivative, it’s uncertain if Lido’s market share has reached its maximum potential. After Shanghai enables withdrawals, will its market share continue to grow or decline?

Importantly, Lido’s governance token does not have a fee intake mechanism nor a method of indirect value accrual. Additionally, the Lido DAO provides staking services across multiple blockchain networks, but the liquidity incentives on these networks are not as substantial as they are on Ethereum. This dilution of LDO’s ability to attract more stEth raises questions about its long-term incentives.

Furthermore, Coinbase is unable to offer any form of liquidity incentives, leaving it with limited options for growth and revenue generation.

Market Maturity

The Ethereum staking market is still in its early stages and, by some measures, has not fully launched yet. When compared to other proof of stake networks, it’s reasonable to anticipate a substantial increase, possibly 2x, 3x, 4x or more, in the total amount of Ether staked.

After withdrawals are enabled, large portions of staked Ether will instantaneously transform from locked, stagnant assets into hyper-liquid commodities. Bots will likely arbitrage away discrepancies in advertised yield across LSDs.

As liquid staking derivatives become commoditized, auxiliary qualities and intangibles will increasingly take priority. Centralization in any one protocol will likely draw attention from the Ethereum community, which has previously shown commitment to overt centralization risks; Prysm dominance among Consensus clients, as an example, was quickly tackled after a successful grassroots campaign.

Lido’s governance token has neither a direct nor indirect method of value accrual. As a pure governance token, it conveys little more than a theatrical vote to all but early investors. The Lido DAO held a vote in response to the community’s desire to limit any one staking pool’s dominance. When asked if Lido should consider self-limiting their share of the Beacon Chain, a whopping 99.81% voted “No”. Of course, the vast majority of these votes were cast by the top dozen holders.

In part the brainchild of Paradigm, Lido’s explicitly stated goal is to capture the majority of the Beacon Chain before more centralized entities such as exchanges are able to. As a secondary benefit, a majority control of the stake would pave the way for LDO to monetize in the form of outsized MEV.

The discourse surrounding the decentralization of Liquid Staking Derivatives (LSDs) has been gaining traction since the Beacon Chain’s launch in late 2020, with the Lido vs Rocket Pool debate at the forefront. As the market has developed and the amount of staked Eth has increased, there have been growing concerns over the health of the network. With no mechanism to alleviate these tensions, the debate has continued to escalate. With the imminent activation of withdrawals, it is likely that the 2.5 years of pent-up market conditions will rapidly unfold over the coming months.