In 4-5 months, I expect the US to be in a recession.

Predictions without a timeframe are useless and not actionable.

Now, it seems most analysts ‘‘expect a recession’’.

Ok, but when will it hit and how hard will it be?

The answers to these two questions are very important for asset allocation in 2023.

First of all: shall we agree on what characterizes a recession in the first place?

While many refer to 2 consecutive quarters of negative GDP growth as the main signal for a recession, the NBER instead looks at consumer spending, the labor market and corporate earnings.

GDP reports are delayed and often subject to big revisions.

The NBER methodology is more robust, and it allows us to assess live whether we are in a recession or not mostly looking at consumers, the labor market and earnings growth.

So: let's do that.

Here are 4 leading macro indicators that can help assess when and how hard a recession could hit.

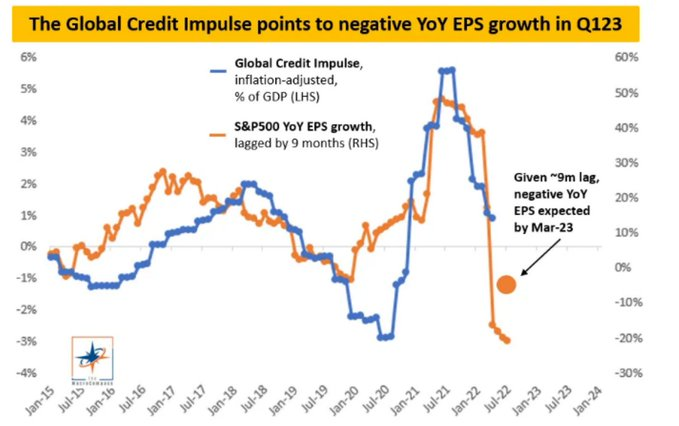

#1: The Global Credit Impulse

When Recession? - March/April 2023

How Bad? - Bad

The global credit impulse (blue) leads S&P500 earnings growth (orange) by 9 months, and given its rapid decline in 2022 it’s now pointing to negative YoY EPS by March/April 2023

Rapid declines in the Global Credit Impulse have preceded YoY EPS contraction in the 10-20% area

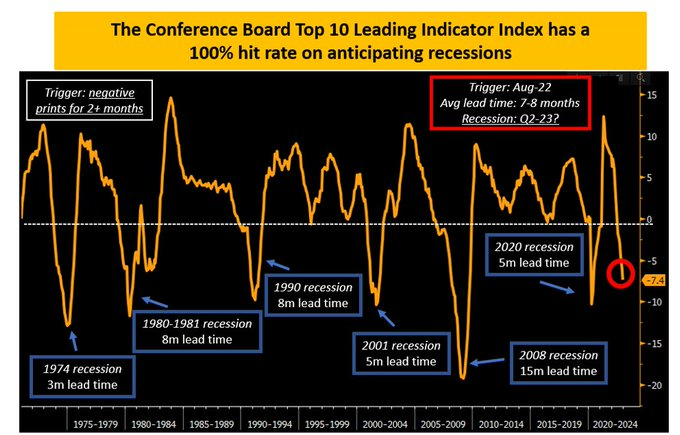

#2: The Conference Board Leading Indicator Index

When Recession? - April/May 2023

How Bad? - On par with 2001 at least

This index incorporates the top 10 statistically significant forward-leading indicators for the US economy.

Over the last 50+ years, every time the YoY series of this index prints in negative territory for 2+ consecutive months a recession is guaranteed.

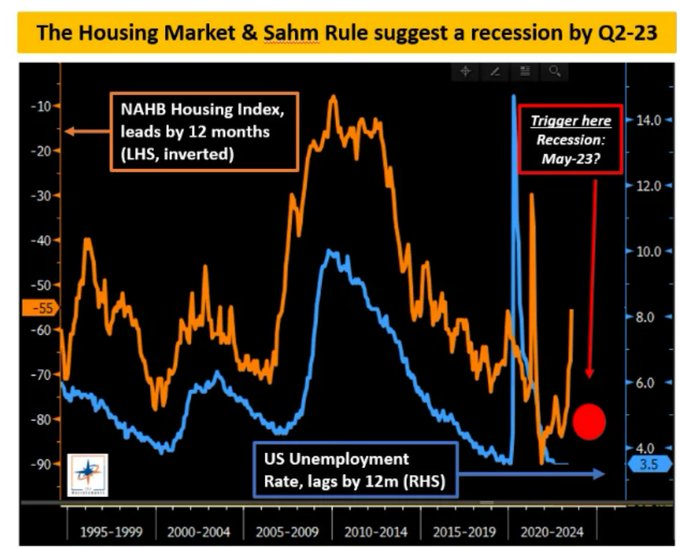

The Housing Market

When Recession? - May 2023

How Bad? - Pretty bad, given unemployment rate is supposed to breach 7% by early 2024

In 2007 Edward Leamer of the University of California stated that the housing market IS the business cycle

I believe he is fundamentally right

Housing-related jobs and economic activity represent anything between 12-15% of US GDP and employment alone

The NAHB housing index (orange, inverted) leads trends in US unemployment rate (blue) by roughly 12 months

According to the Sahm Rule, a recession starts when the 3-month moving average of the US unemployment rate rises by 50+ bps relative to its low during the previous 12m

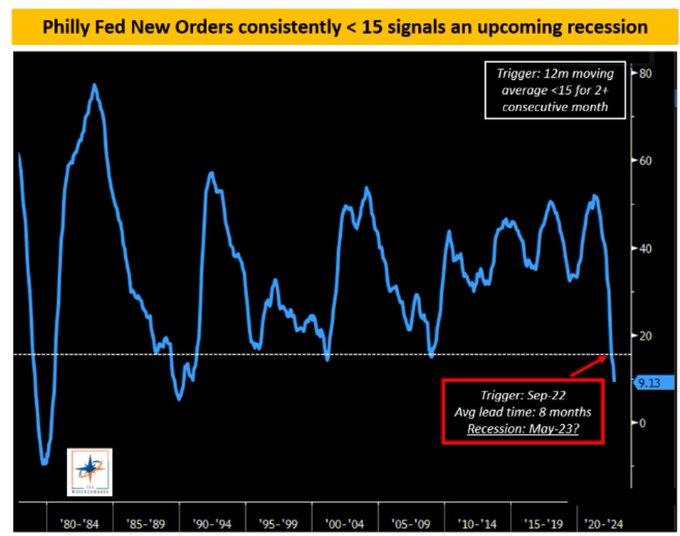

#4: Philly Fed New Orders

When Recession? - May 2023

How Bad? - Too early to say, probably on par with 2001 at least

The survey goes out to 125 CEOs of relevant companies who tend to have a good grasp of where economic activity is headed.

Over the last 40 years, every time the 12m moving average of this index dropped below 15 for 2+ months, a recession always followed.

Conclusion: several leading macro indicators are pointing to a US recession starting in 4-5 months, and of a magnitude at least on par with 2001.

Looking under the hood, the latest GDP report also confirms organic growth is rapidly trending down and heading below zero.