Author: @intern_cc, Crypto KOL

Compiled by: Felix, PANews

Crypto options are poised to become the iconic financial instrument of 2026, thanks to the convergence of three major trends: the squeeze on traditional DeFi yields due to 'yield doomsday,' a new generation of simplified 'entry-level products' that abstract options into one-click trading interfaces, and institutional validation from Coinbase's $2.9 billion acquisition of Deribit.

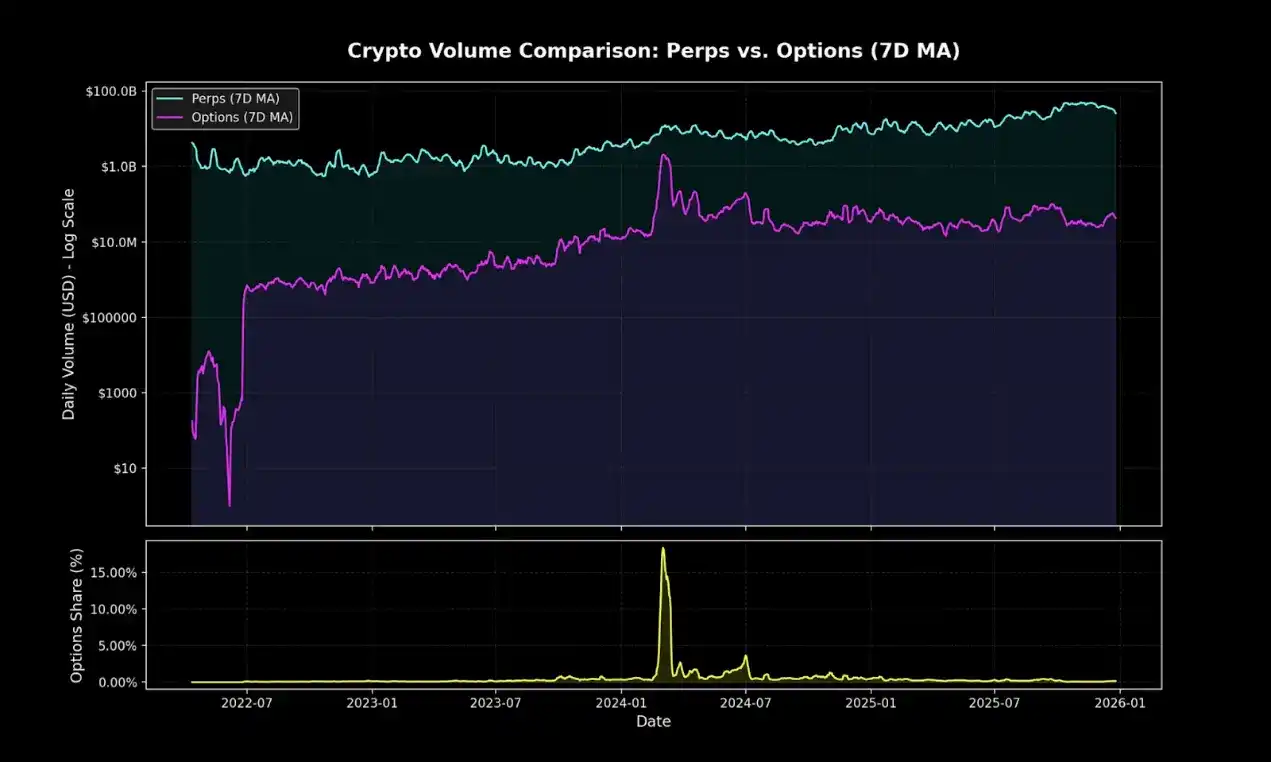

Although on-chain options currently account for only a small fraction of crypto derivatives trading volume, perpetual contracts still dominate the market absolutely. This gap mirrors the situation of TradFi options before their popularization by Robinhood.

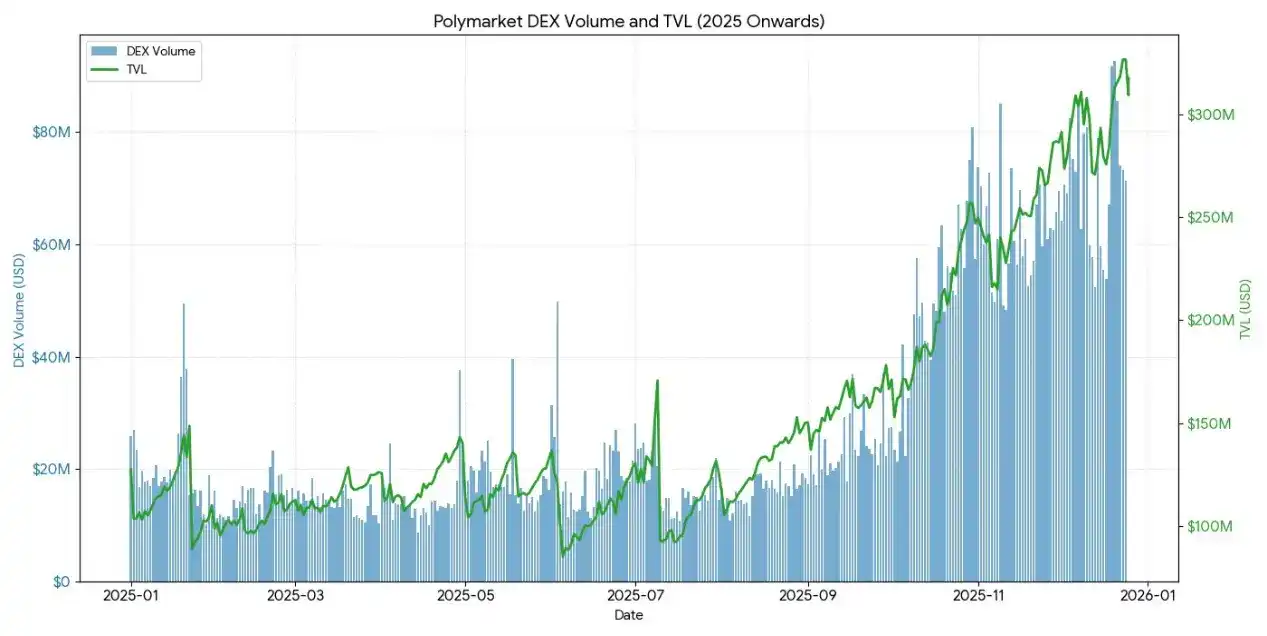

Polymarket processed $9 billion in trading volume in 2024 by repackaging binary options, complemented by excellent marketing. If the retail market's demand for probabilistic betting is confirmed, can DeFi options achieve the same structural shift? When infrastructure and yield dynamics finally align, execution will determine whether options break through the bottleneck or remain a niche tool.

The End of Passive Yields

To understand why crypto options might explode in 2026, one must first understand what is dying.

For nearly five years, the crypto ecosystem has flourished, with market analysts retrospectively calling it the golden age of 'lazy yield,' where participants could achieve significant risk-adjusted high returns with almost no complex operations or active management. The typical representatives were not complex option strategies but rather simple, brute-force arbitrage methods like token issuance mining, looping strategies, and perpetual contract basis trading.

Basis trading was the core of crypto yields. Its mechanism seems simple but is not: due to a structural long bias among retail investors, longs pay funding fees to shorts to maintain their positions. By buying spot and shorting perpetual contracts, savvy participants constructed delta-neutral positions unaffected by price fluctuations while also securing 20% to 30% annualized returns.

However, there is no free lunch. With the approval of Bitcoin spot ETFs, the entry of traditional financial institutions brought industrial-scale efficiency. Authorized participants and hedge funds began executing this trade with tens of billions of dollars, compressing the spreads to treasury rates plus a thin risk premium. By the end of 2025, this 'bubble' had dissipated.

The 'Graveyard' of DeFi Options Protocols

- Hegic launched in 2020 with pool-to-pool innovation but shut down twice early on due to code errors and game theory flaws.

- Ribbon's market cap fell from a peak of $300 million, mainly due to the 2022 market crash and subsequent strategic migration to Aevo, leaving only about $2.7 million exploited by hackers in 2025.

- Dopex introduced concentrated liquidity options but ultimately collapsed due to uncompetitive products generated by the model, low capital efficiency, and an unsustainable token economy in a brutal macro bear market.

- Opyn pivoted to infrastructure and abandoned retail after realizing options trading was still dominated by institutions.

The failure mode was highly consistent: ambitious protocols struggled to achieve both liquidity bootstrapping and simplified user experience.

The Paradox of Complexity

Ironically, options, which are theoretically safer and more aligned with user intent, are less popular than the riskier, more complex perpetual contracts.

Perpetual contracts seem simple, but their mechanisms are extremely complex. Every time the market crashes, people get liquidated or automatically deleveraged, and even large traders may not fully understand how perpetuals work.

In contrast, options do not face these problems at all. Buying a call option limits risk to the premium, with maximum loss determined before entry. Yet perpetuals dominate simply because 'sliding to 10x leverage' is always easier than 'calculating delta-adjusted risk.'

The Mental Trap of Perpetual Contracts

Perpetual contracts force you to take cross-spreads and pay fees twice per trade.

Even hedged positions can wipe you out.

They are path-dependent; you cannot 'set and forget' a position.

But even if you believe short-term retail directional flow will still go to perpetuals, options can still dominate the market share in most chain-native finance. They are a more flexible and powerful tool for hedging risk and creating yield.

Looking five years ahead, on-chain infrastructure will gradually evolve into the backend for allocation layers, with broader coverage than traditional finance.

Today's innovative vaults, like Rysk and Derive, represent the initial wave of this shift, offering structured products that go beyond basic leverage or lending pools. Savvy asset allocators will need a richer toolkit for risk management, volatility trading, and portfolio yield to fully utilize the decentralized ecosystem.

TradFi Proves Retail Loves Options

The Robinhood Revolution

The surge in retail options trading in TradFi provides a roadmap. Robinhood launched commission-free options trading in December 2017, sparking an industry transformation that culminated in October 2019 when Charles Schwab, TD Ameritrade, and Interactive Brokers eliminated commissions within days of each other.

The impact was massive:

- The share of US retail options volume soared from 34% at the end of 2019 to 45-48% in 2023

- In 2024, the Options Clearing Corporation (OCC) cleared a record 12.2 billion option contracts annually, the fifth consecutive record year

- In 2020, meme stocks accounted for 21.4% of options trading volume

The Explosive Growth of Zero-Day-to-Expiration (0DTE) Options

0DTE options show retail's interest in short-term, high-convexity bets. 0DTE's share of S&P 500 index options volume grew from 5% in 2016 to 51% in Q4 2024, with average daily volume exceeding 1.5 million contracts.

The appeal is obvious: lower capital outlay, no overnight risk, built-in leverage exceeding 50x, and same-day feedback loops, dubbed 'dopamine trading' by insiders.

Convexity and Defined Risk

The non-linear payoff structure of options attracts directional traders seeking asymmetric returns. A call buyer might risk only $500 in premium for a potential gain of over $5000. Spread trades allow for more precise strategy tuning: maximum loss and profit are defined before entry.

Entry Products and Infrastructure

Abstraction as the Solution

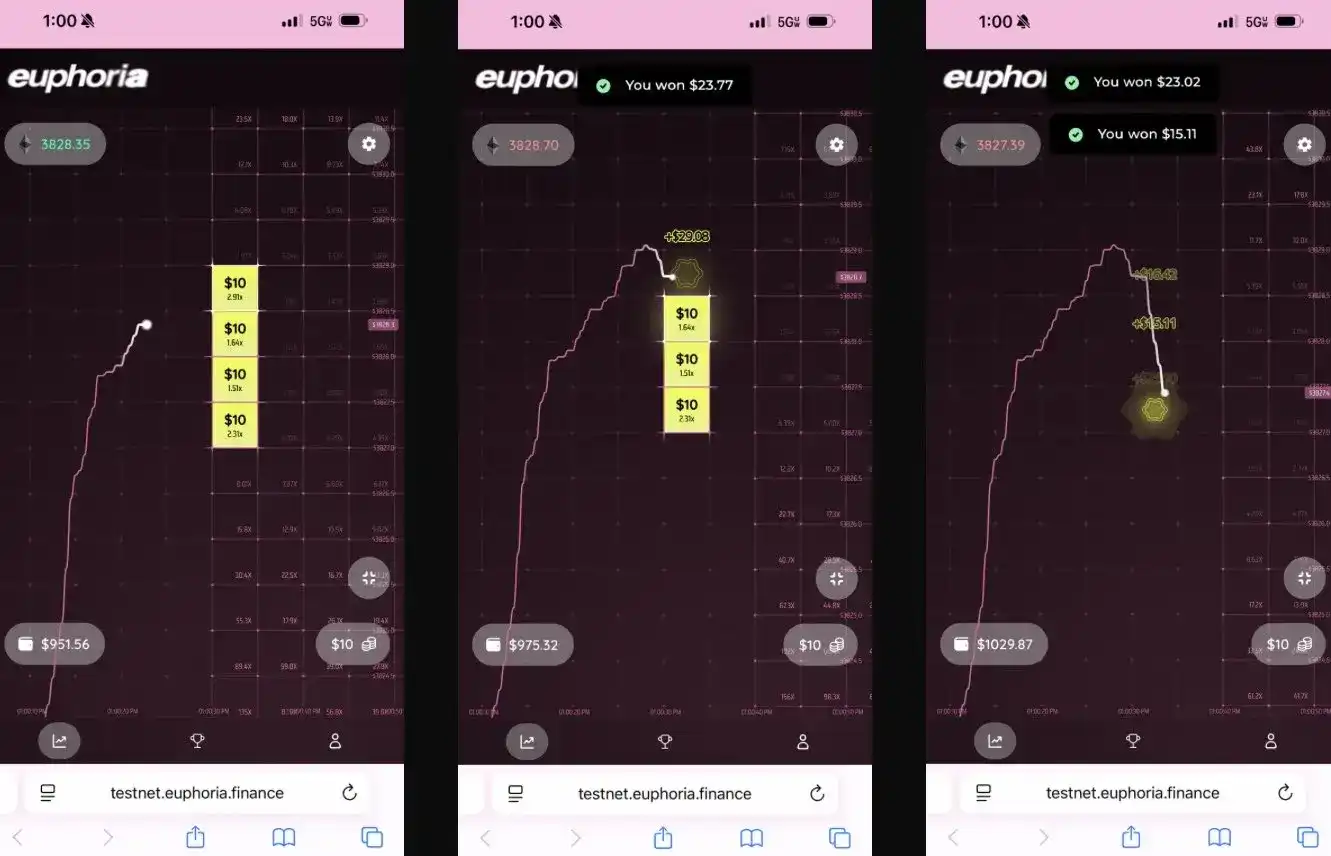

A new generation of protocols solves the complexity problem by completely hiding options behind simple interfaces, known in the industry as 'dopamine apps.'

Euphoria secured a $7.5 million seed round with a radical simplification vision: "You just look at the chart, see where the price line is moving, and click on the grid square you think the price will hit next." No order types, no margin management, no Greeks, just executing the right directional bet on a CLOB.

Built on MegaETH's sub-millisecond infrastructure.

The explosion of prediction markets confirms the concept of simplified strategies:

- Polymarket processed over $9 billion in volume in 2024, with a peak of 314,500 monthly active traders.

- Kalshi's weekly volume has stabilized above $1 billion.

Both platforms are structurally identical to binary options, but the concept of 'prediction' transforms the stigma of gambling into collective wisdom.

As Interactive Brokers explicitly acknowledged, their prediction contracts are "'prediction markets' for binary options."

The lesson: retail doesn't want complex financial instruments; they want simple, clear probabilistic bets with straightforward outcomes.

State of DeFi Options in 2025

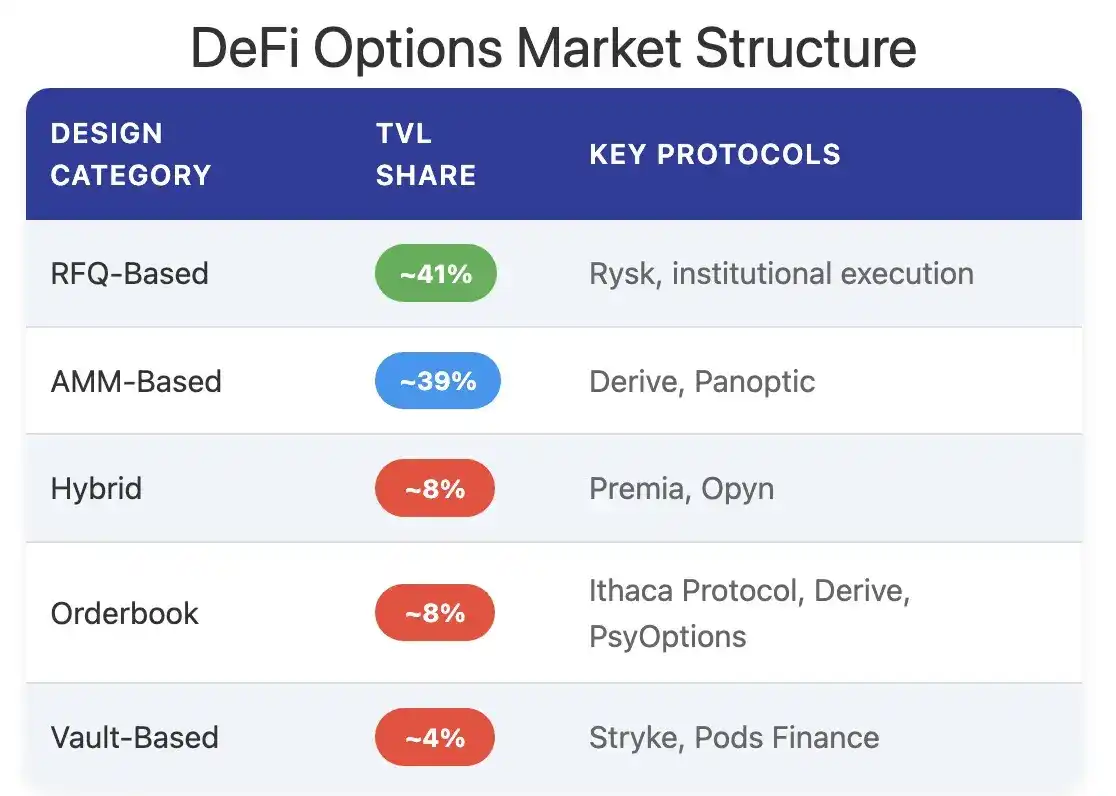

As of the end of 2025, the DeFi options ecosystem is transitioning from experimental designs to more mature, composable market structures.

Early frameworks exposed numerous issues: liquidity fragmented across expiries, reliance on oracles for settlement added latency and manipulation risk, and fully collateralized vaults limited scalability. This prompted a shift towards liquidity pool models, perpetual option structures, and more efficient margin systems.

Current DeFi options participants are primarily yield-seeking retail, not hedging-seeking institutions. Users view options as passive income tools, selling covered calls for premium, not as volatility transfer instruments. When market volatility spikes, vault depositors face adverse selection risk due to a lack of hedging tools, leading to persistent underperformance and TVL outflows.

Protocol architecture has moved beyond traditional expiry-based models, giving rise to new paradigms in pricing, liquidity, etc.

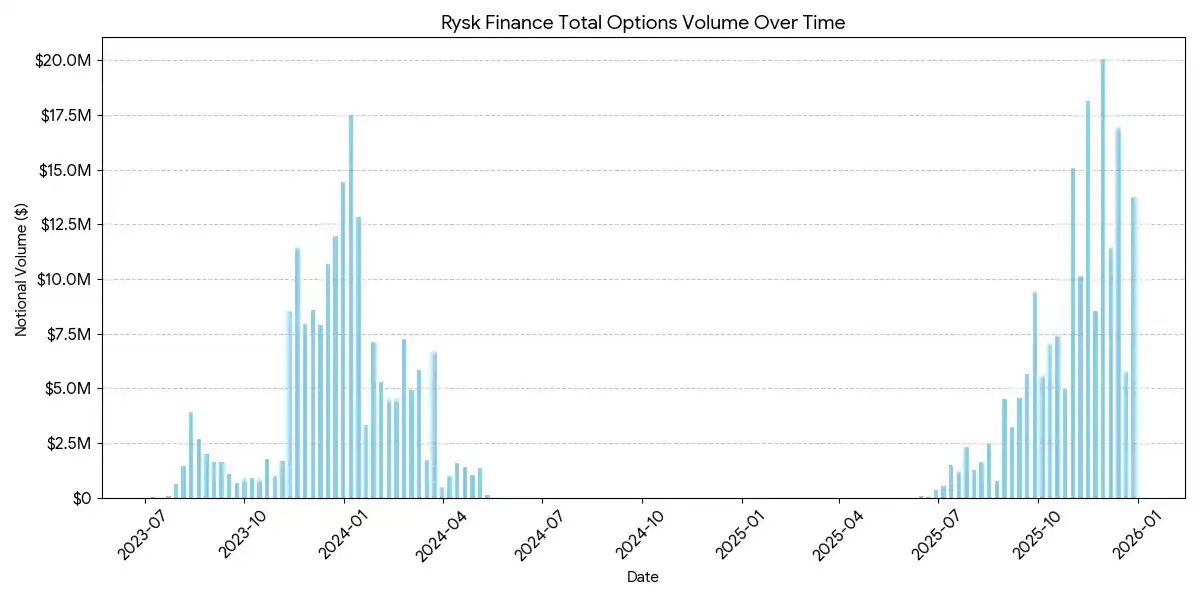

Rysk

Rysk applies traditional option writing mechanics to DeFi via on-chain primitives, supporting covered calls and cash-secured puts. Users deposit collateral directly into smart contracts to establish single positions, customizing strike price and expiry. Trades are executed via a real-time request-for-quote mechanism, where counterparties provide competitive quotes through fast on-chain auctions, enabling instant confirmation and upfront premium collection.

Payoffs follow standard covered call structure:

- If price < strike at expiry: Option expires worthless, seller keeps collateral + premium

- If price ≥ strike at expiry: Collateral is physically delivered at the strike price, seller keeps premium but forgoes upside.

A similar structure applies to cash-secured puts, with physical delivery automated on-chain.

Rysk targets premium sellers seeking sustainable, non-inflationary yield, with each position fully collateralized, no counterparty risk, and deterministic on-chain settlement. It supports diverse collateral like ETH, BTC, LSTs, and LRTs, making it suitable for DAOs, treasuries, funds, and institutions managing volatile assets.

Average position sizes on Rysk reach five figures, indicating institutional-level capital involvement.

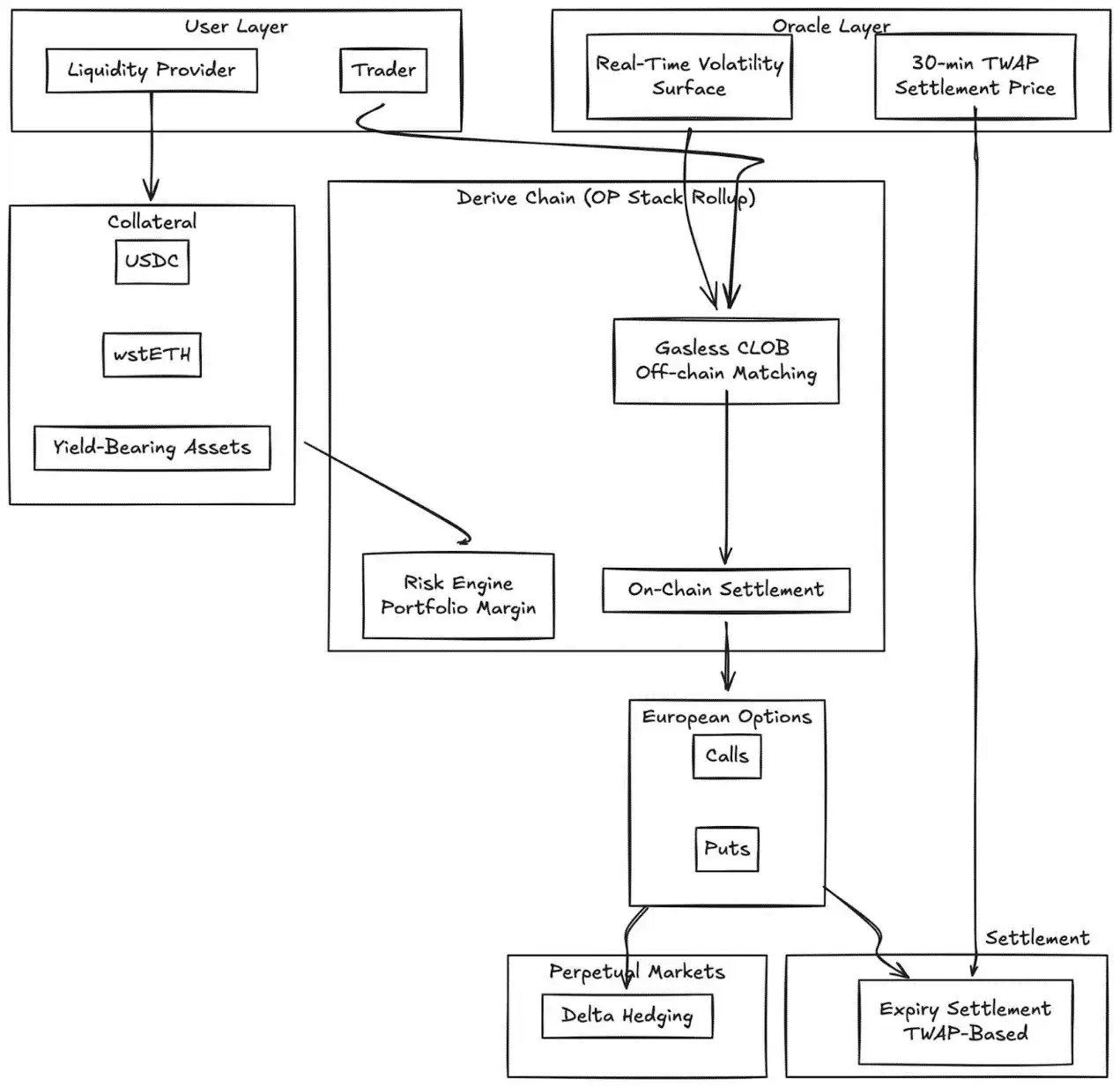

Derive.xyz

Derive (formerly Lyra) transitioned from its pioneering AMM architecture to a gasless central limit order book with on-chain settlement. The protocol offers fully collateralized European options with dynamic volatility surfaces and settlement based on 30-minute TWAP.

Key innovations:

- Real-time volatility surface pricing via external feeds

- 30-minute TWAP oracle reduces expiry manipulation risk

- Integration with perpetual markets for continuous delta hedging

- Support for yield-bearing collateral (e.g., wstETH) and portfolio margin, improving capital efficiency

- Execution quality: Competitive with smaller CeFi venues

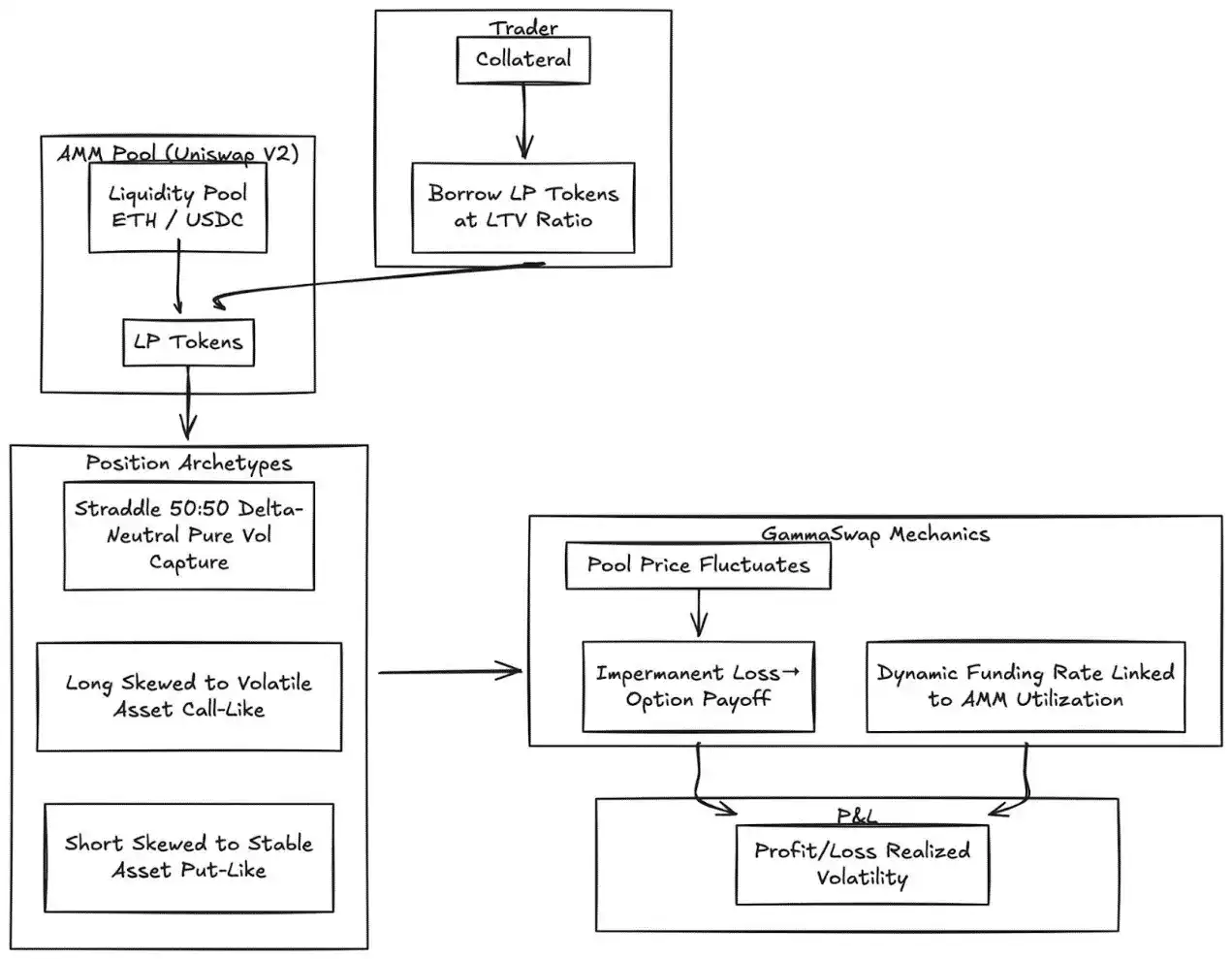

GammaSwap

GammaSwap introduces non-synthetic perpetual options built on AMM liquidity.

Instead of relying on oracles or fixed expiries, it generates continuous volatility exposure by borrowing liquidity from AMMs like Uniswap V2.

The mechanism transforms impermanent loss into a tradable options payoff:

- Traders borrow LP tokens at a specified loan-to-value ratio

- As pool prices move, collateral value relative to the borrowed amount changes

- P&L is proportional to realized volatility

- Dynamic funding rate is tied to AMM utilization

Position types:

- Strangle: Delta neutral (50:50), purely capturing volatility

- Long bias: Collateral skewed towards more volatile asset (call-like)

- Short bias: Collateral skewed towards more stable asset (put-like)

The mechanism eliminates oracle reliance entirely by deriving all prices from endogenous AMM state.

Panoptic

Perpetual, oracle-free options on Uniswap.

Panoptic represents a fundamental shift: perpetual, oracle-free options built on Uniswap v3 concentrated liquidity. Any Uniswap LP position can be interpreted as a combination of long and short options, with fees existing as a continuous stream of premium.

Core insight: A Uniswap v3 position within a specific price range behaves like a short option portfolio, its delta varying with price. Panoptic formalizes this concept by allowing traders to deposit collateral and select liquidity ranges to establish perpetual option positions.

Key features:

- Oracle-free valuation: All positions are priced using quotes and liquidity data inside Uniswap

- Perpetual exposure: Options are held indefinitely, with premium stream continuous, not discrete expiries

- Composability: Built on Uniswap, integrated with lending, structured yield, and hedging protocols

Comparison with CeFi:

The gap with centralized exchanges remains significant. Deribit dominates globally with over $3 billion in daily open interest.

Several structural factors cause this disparity:

Depth and Liquidity

CeFi concentrates liquidity in standardized contracts with tightly spaced strikes, supporting order books of tens of millions per strike. DeFi liquidity remains fragmented across protocols, strikes, and expiries, with each protocol running independent pools unable to share margin.

Execution quality: Deribit and CME offer near-instant order book execution. AMM-based models like Derive offer tighter spreads for liquid, near-the-money options, but execution quality degrades for large orders and deep out-of-the-money strikes.

Margin efficiency: CeFi platforms allow cross-margining across instruments; most DeFi protocols still isolate collateral by strategy or pool.

However, DeFi options have unique advantages: permissionless access, on-chain transparency, and composability with the broader DeFi tech stack. This gap will narrow as capital efficiency improves and protocols eliminate fragmentation by removing expiries.

Institutional Positioning

The Coinbase-Deribit Super Stack:

Coinbase's $2.9B acquisition of Deribit achieves strategic integration across the entire crypto capital stack:

- Vertical integration: Users' spot Bitcoin custodied on Coinbase can be used as collateral for options trading on Deribit.

- Cross-margin: In fragmented DeFi, capital is scattered across protocols. On Coinbase/Deribit, it's concentrated in one pool.

- Full lifecycle control: With the acquisition of Echo, Coinbase controls issuance => spot trading => derivatives trading.

For DAOs and crypto-native institutions, options provide effective treasury risk management mechanisms:

- Buy puts to hedge downside risk, locking in a minimum value for treasury assets.

- Sell covered calls on idle assets, creating a systematic income stream.

- Tokenize risk positions by encapsulating option exposure into ERC-20 tokens.

These strategies transform volatile token holdings into more stable, risk-adjusted reserves, crucial for institutional DAO treasury adoption.

LP Strategy Optimization

An extensible toolkit for LPs, turning passive liquidity into active hedging or yield enhancement strategies:

- Options as dynamic hedges: LPs in Uniswap v3/v4 can reduce impermanent loss by buying puts or constructing delta-neutral spreads. GammaSwap and Panoptic allow liquidity to serve as collateral for continuous option yield, offsetting AMM exposure.

- Options as yield stacking: Vaults can automatically execute covered call and cash-secured put strategies against LP or spot positions.

- Delta-targeted strategies: Panoptic's perpetual options allow selecting delta-neutral, short, or long exposure by adjusting strikes and ranges.

Composable Structured Products

- Vault integration: Automated vaults package short-vol strategies into tokenized yield instruments, akin to structured on-chain notes.

- Multi-leg options: Protocols like Cega design path-dependent payoffs (dual currency notes, auto-callables) with on-chain transparency.

- Cross-protocol composition: Combine option yield with lending, restaking, or redemption rights to create hybrid risk instruments.

Outlook

The options market will not evolve into a single category. It will bifurcate into two distinct tiers, each serving different user bases with vastly different products.

Tier 1: Abstracted Options for the Mass Retail

Polymarket's success proves retail doesn't reject options; they reject complexity. $9 billion in volume didn't come from traders understanding implied vol; it came from users seeing a question, picking a side, and clicking a button.

Euphoria and similar dopamine apps will push this theory further. The option mechanics run invisibly beneath the click-to-trade interface. No Greeks, no expiries, no margin calculations, just price targets on a grid. The product *is* the option.

The UX feels like a game.

This tier will capture the volume currently monopolized by perpetuals: short-term, high-frequency, dopamine-driven directional bets. The competitive advantage isn't financial engineering; it's UX design, mobile-first interfaces, and sub-second feedback. The winners in this tier will look more like consumer apps than trading platforms.

Tier 2: DeFi Options as Institutional Infrastructure

Protocols like Derive and Rysk won't compete for retail. They will serve a completely different market: DAOs managing eight-figure treasuries, funds seeking uncorrelated yield, LPs hedging impermanent loss, and asset allocators building structured products.

This tier requires sophistication. Portfolio margin, cross-collateralization, RFQ systems, dynamic vol surfaces—features retail may never touch but are essential for institutions.

Today's vault providers are the early infrastructure at the institutional layer.

On-chain asset allocators need the full expressive power of options: explicit hedging, yield stacking, delta-neutral strategies, composable structured products.

Leverage sliders and simple lending markets won't suffice.

Related reading: Are Prediction Markets an Extended Form of Binary Options?