Zhenbao Technology ignited the entire STAR Market with a capital frenzy on its first trading day, soaring 1207% at debut, with single-application profits exceeding 270,000 yuan. Becoming the second '10-bagger' new stock of the year, its closing price of 585 yuan also secured a place in the top 20 of the A-share market's stock price rankings. Supported by the entire semiconductor industry chain as the 'first stock in semiconductor consumables', this company tells a 'band-aid' story more compelling than selling equipment through its integrated closed-loop of 'raw materials + components + surface treatment'—as long as wafer fabs are running, revenue keeps flowing in.

01

Not a "Scalpel," but a "Band-Aid"

The STAR Market has been ignited by a new stock in the past two days.

The newly listed semiconductor equipment component manufacturer—Zhenbao Technology (the new stock "N Zhenbao")—saw its share price skyrocket 1207% after opening, triggering a temporary trading halt. Based on one lot of 500 shares for the STAR Market, the maximum profit per lot from Zhenbao Technology exceeded 270,000 yuan.

In fact, during the issuance stage, Zhenbao Technology already showed signs of 'overheating'—the offline subscription multiple reached as high as 4363 times, making it one of the most crowded IPOs on the STAR Market in recent years. Its shareholder list reads like a 'family portrait' of the semiconductor industry chain: National Integrated Circuit Industry Investment Fund Phase II, SMIC, BOE, Yangtze Memory, Huahong Group... from upstream to downstream, from capital to industry, almost all are present.

This means one thing: it is a target almost 'collectively supported' by the entire industry chain. But we have a question—what exactly has it done to warrant such pricing and expectations?

To explain with a simple analogy, there are essentially two types of businesses in the semiconductor industry. One is 'selling scalpels.' For example, etching machines, thin-film deposition equipment—these core equipment cost hundreds of millions each and can be used by wafer fabs for years, resulting in extremely low repurchase rates.

The other is 'selling band-aids.' Zhenbao Technology is exactly in this category—key consumable parts inside the equipment: silicon rings, quartz components, silicon carbide rings, etc. These components are constantly exposed to high-temperature plasma environments and typically have a lifespan of only a few months. In other words, as long as wafer fabs are still operational, these consumables will be continuously consumed, forming stable, predictable cash flow.

Image | Source: Company Official Website

Selling scalpels means waiting for hospitals to buy new ones; but selling band-aids means revenue every day as long as there is consumption.

This is precisely why the capital market is willing to grant it a higher premium: it's not about whether you have orders, but whether the orders are continuous.

If the story stopped here, it would at most be a good business, far from the current market frenzy. The key question is, how did Zhenbao Technology break into this market?

Unlike most hard-tech companies, Zhenbao Technology's starting point was not in the lab, but on the front lines of the market. Founder Wang Bing, born in the 1980s, started his career as a sales engineer at Shanghai Yaohua FRP Co., Ltd. after graduation, later entering the semiconductor equipment and materials field, also working in sales for many years. Based on the post-issuance total share capital of approximately 155 million shares, Wang Bing's direct shareholding is diluted to about 33%. Calculated at the latest market capitalization, his personal wealth is approximately 28.7 billion yuan.

Wang Bing noticed early on the structural challenges faced by domestic wafer fabs during rapid expansion: overseas manufacturers monopolized the technology for preparing high-purity silicon, quartz, and other materials. Domestic wafer fabs not only faced high equipment maintenance costs but also extremely unstable supply lead times.

In the past, this issue was tolerable. However, with increasing uncertainty in the geopolitical environment, supply chain security has transformed from a cost issue into a survival issue.

Therefore, Zhenbao Technology offered a very clever and pragmatic solution: performance reaches 80%, price reaches 50%, but delivery speed and responsiveness reach 100%.

To achieve this, Wang Bing chose the hardest path. Traditional component manufacturers often only engage in 'OEM + material sales,' but Zhenbao Technology has established a full-chain closed loop encompassing 'raw materials + components + surface treatment.' The company independently developed and mass-produced key raw materials such as large-diameter monocrystalline silicon rods, polycrystalline silicon rods, CVD high-purity silicon carbide ultra-thick materials, and ceramic granulated powders. This not only ensures supply chain stability but also significantly reduces production costs.

For those wafer fab customers, this choice might not be perfect, but it is usable, controllable, and sustainable.

Thus, a subtle yet crucial relationship began to form—upstream suppliers are no longer just technology providers but also risk-sharing partners; downstream wafer fabs no longer pursue a single optimal solution but accept a combination that is 'sub-optimal yet secure.'

Because of this, Zhenbao Technology's customer list includes not only domestic leading wafer fabs such as BOE, Nexchip, CR Micro, and Silergy Integration; it has also entered the supply systems of international manufacturers like SK Hynix (Dalian), GlobalFoundries, United Microelectronics Corporation, and Texas Instruments.

This indicates that its competitiveness is not merely based on import substitution but also possesses a certain degree of global comparability.

According to Frost & Sullivan data, in 2024, among local enterprises directly supplying semiconductor equipment components to wafer fabs, Zhenbao Technology ranked first in the silicon component market with a revenue market share of 4.5%, and first in the quartz component market with a revenue market share of 8.8%.

02

Behind the 1.6 Billion Fundraising

If the 1200% surge tells a story of 'imagination,' then the 1.6 billion fundraising corresponds to a more realistic balance sheet.

For this IPO, Zhenbao Technology raised a net amount of 1.605 billion yuan, primarily for investment in capacity expansion. This in itself is not a problem. However, once this money is converted into production capacity, it quickly becomes an unavoidable cost: depreciation.

According to the prospectus estimates, after the fundraising projects reach full capacity, the annual peak of newly added depreciation and amortization expenses will be 72.7718 million yuan. This is not a flexible cost but a rigid expense. Compared to the company's 2025 net profit of 226 million yuan, this expense would directly consume about one-third of the profit. In other words, as long as capacity utilization does not increase, the income statement will be the first to 'change face.' This is an unavoidable turning point for all heavy-asset manufacturing enterprises.

Looking at the company's recent growth performance, such pressure once seemed manageable. From 2022 to 2025, Zhenbao Technology's revenues were 386 million, 506 million, 635 million, and 846 million yuan respectively, with net profits attributable to the parent company being 81.62 million, 108 million, 152 million, and 226 million yuan respectively, showing a trend of continuous and accelerating growth.

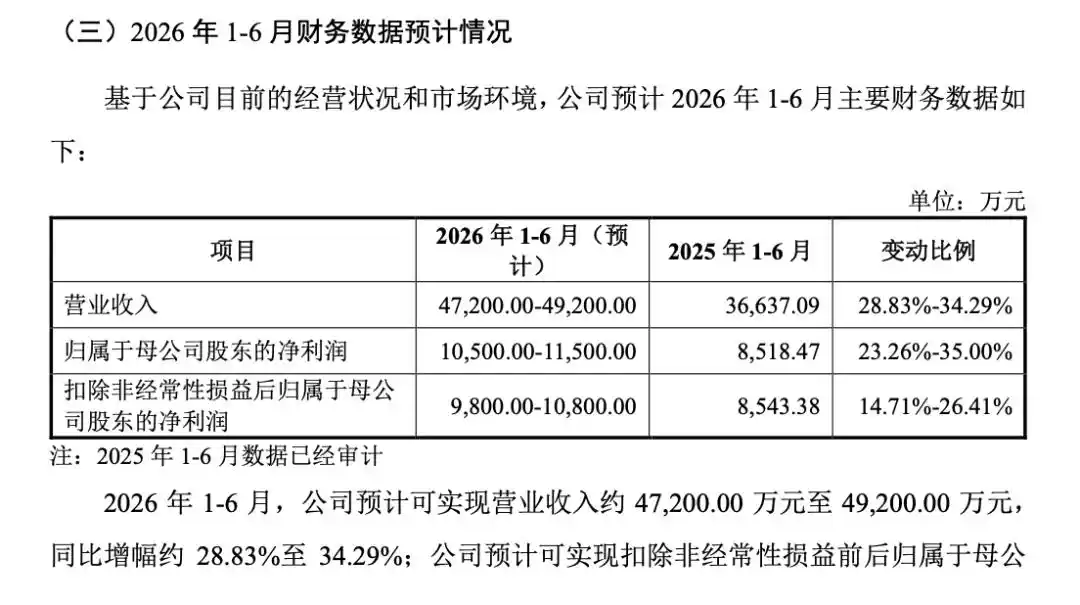

In the first half of this year, the company expects to achieve revenue of 472 million to 492 million yuan, a year-on-year increase of approximately 29% to 34%, and net profit attributable to the parent company of 105 million to 115 million yuan, a year-on-year increase of approximately 23% to 35%. On the surface, such growth rates seem sufficient to offset the profit erosion caused by new depreciation. However, the question is whether this growth itself is built upon a sustainable demand cycle.

Image | Source: Company Prospectus

The company's answer is optimistic: it expects revenue by 2028 to grow by 144.14% compared to 2024. This assumption implies a premise—downstream wafer fabs will continue to maintain high-intensity expansion.

However, judging by industry patterns, semiconductors are a typical strong-cycle industry. Especially for the component segment where Zhenbao Technology operates, although it possesses 'consumable attributes,' its essence is still tied to equipment utilization rates and new production lines. Once memory or logic chips enter a destocking cycle and utilization rates drop, consumable demand will also contract.

A more immediate pressure comes from external competition. Japanese manufacturers still hold technological advantages in the high-end component field. If they counterattack through price reductions or by bundling with equipment manufacturers, the room for domestic manufacturers' 'cost-performance strategy' will be significantly compressed. At that point, the capacity that has been built but cannot operate at full load will no longer be a moat, but a burden.

Aside from the uncertainty on the capacity side, the fund occupation issue evident in the financial statements is equally worthy of vigilance. In mid-2025, the company's accounts receivable as a percentage of revenue once reached as high as 70.83%, indicating a clear decline in turnover efficiency. Behind this indicator lies a typical industry chain position—although the company has secured leading customers, its bargaining power is limited, necessitating more lenient payment terms to secure orders. For investors, this means profits may not smoothly convert into cash flow. Once downstream customers delay payments or industry sentiment declines, pressure on the capital chain will amplify rapidly.

The concentration of the customer structure further amplifies this uncertainty. The sales proportion of the top five customers has long exceeded 70%, seemingly indicating 'binding with leaders.' However, from a risk perspective, it is closer to single-point reliance. This structure poses few problems during industry upswings but tends to magnify volatility during downturns.

A more subtle risk stems from the substance of its 'science and technology innovation attributes.' During the critical application period, the company rapidly expanded its R&D personnel from 38 to 113, just crossing the STAR Market's 10% threshold. However, 34 people were subsequently transferred out in the first half of 2025. Such drastic fluctuations in personnel structure inevitably raise market doubts about the authenticity and sustainability of its R&D investments.

Furthermore, the company's early R&D management was relatively crude, with abnormal fluctuations in work-hour records and energy consumption statistics. For example, R&D energy consumption surged 1135% year-on-year in 2024. While such details may not directly impact current performance, in an industry like semiconductors that demands extremely high process stability, they affect the market's judgment of its long-term technological capabilities.

In summary, the core contradiction for Zhenbao Technology is already very clear: on one side is the valuation premium brought by the certainty of the 'consumable logic,' on the other is the performance volatility risk brought by heavy-asset expansion.

For the secondary market, a high valuation can be paid in the short term for the 'band-aid' story. However, mid-to-long-term pricing will ultimately return to two variables—whether capacity utilization can remain high and whether cash flow can keep up with the income statement. If deviations occur in these two points, then this 72 million yuan depreciation may not merely be an erosion of profit, but the starting point for valuation compression.

This article is from the WeChat public account "Phoenix Network Technology," author: Lu Chunfeng, editor: Dong Yuqing