Author: RWA.xyz

Compilation: Block unicorn

Summary

Allocation vaults are increasingly becoming the primary distribution infrastructure for tokenized assets to access on-chain capital. This guide will explain what allocation vaults are, how they operate, and what institutional asset managers need to know to evaluate this opportunity.

-

Development History. Institutional tokenization has gone through three stages: recording, capitalization, and construction. Initially, tokenized assets recorded on-chain did not generate market demand. Tokenized treasury bonds found product-market fit and were capitalized on-chain by crypto-native capital. Private credit emerged later but required "tokenization engineering" to integrate with DeFi infrastructure due to its structural mismatch with on-chain capital.

-

What is an Allocation Vault? An allocation vault is a smart contract-based allocation tool built on top of DeFi lending protocols. Risk managers are responsible for reviewing which tokenized assets qualify as collateral, setting risk parameters, and allocating stablecoin liquidity. The closest financial analogy is the collateral and margin trading department of a prime broker: lending protocols provide the infrastructure, but financing cannot be achieved without risk managers willing to accept the assets.

-

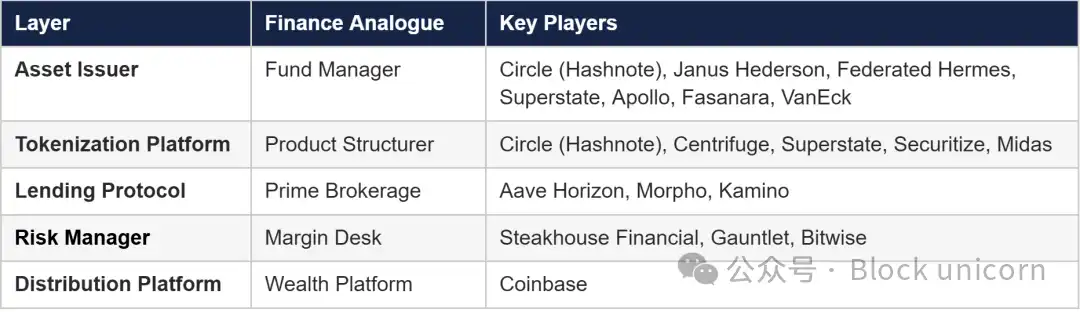

Why Should Investment Managers Care? Allocation vaults are not just risk infrastructure; they are also distribution channels. The on-chain version of the fund-to-investor value chain consists of five layers: asset issuer, tokenization platform, lending protocol, risk manager, and distribution platform. When a tokenized product is accepted as collateral, it connects to the entire system.

-

How is Demand Generated? Being accepted as collateral initiates a leverage loop: borrowers provide tokens, borrow stablecoins, increase exposure, and repeat the process. This borrowing demand generates yield for the depositors of the allocation vault, attracting more liquidity and creating a self-reinforcing mechanism. By integrating with distribution platforms like Coinbase, this demand can be extended to retail and institutional deposits.

-

What This Guide Covers. We will delve into the market dynamics that drive on-chain demand for tokenized assets, explain how allocation vaults work and how they compare to traditional fund structures, introduce the five-layer allocation architecture, and use Fasanara's mF-ONE as a case study to demonstrate the practical application of this model in private credit. Finally, we will provide a strategic overview for fund managers evaluating their first move.

Despite the growing interest in allocation vaults, it is difficult to find a comprehensive resource specifically prepared for non-crypto institutional asset managers. This is the purpose of our introductory guide. As tokenized assets approach an allocation inflection point, RWA.xyz aims to create a strategic guide that is both informative and accessible for institutional asset managers.

Development History

The development of institutional tokenized assets has gone through three stages. Each stage addressed the limitations of the previous one and laid the foundation for the next.

As early as 2018, a few crypto-native venture capital funds began representing their portfolios in tokenized form on public blockchains. But the first large alternative asset manager to tokenize a fund was KKR, which partnered with Securitize in September 2022 to tokenize a portion of its Healthcare Strategic Growth Fund II on Avalanche. Hamilton Lane followed shortly after with a similar sub-fund structure.

The initial idea was to improve operational efficiency. Tokenized sub-funds reduced management costs, lowered the minimum investment threshold, and thus attracted a broader investor base. It was expected that lowering the barrier to entry would ultimately drive demand for these fund products.

However, in practice, lowering the barrier to entry did not bring the expected significant growth. The real demand came from an unexpected place. To understand why, we need to understand how on-chain yields are set.

Most decentralized finance (DeFi) lending protocols follow a simple model: lenders deposit stablecoins, and borrowers borrow against crypto assets as collateral, usually to take leveraged long positions. Since the cryptocurrency market is generally biased towards long positions, DeFi lending rates are typically higher than U.S. Treasury yields.

This changed when the Federal Reserve raised the federal funds rate from 0.25% to 5.5% in July 2023. As the crypto bear market suppressed borrowing demand, stablecoin yields fell to around 3%, and on-chain capital began to flow into tokenized treasury products. Product-market fit was immediate, and by February 2026, the market capitalization of tokenized treasuries had exceeded $10 billion.

Through tokenized treasuries, institutional asset management companies discovered that blockchain networks are not just a platform for improving operational efficiency; they are also a new distribution channel that can reach the pool of funds already on-chain. With the return of the crypto bull market, on-chain investors became increasingly familiar with tokenized products, and demand for high-yield tokenized private credit products grew naturally.

However, unlike treasury products, private credit has structural issues that cause a fundamental mismatch with decentralized finance (DeFi). Institutional asset management companies quickly realized that tokenizing high-yield products does not automatically create on-chain demand. These products must be restructured and integrated with suitable DeFi infrastructure.

This is where allocation vaults come in. They solve the distribution problem by integrating tokenized credit products as collateral into DeFi lending markets, which standalone tokenized funds cannot address.

What is an Allocation Vault?

Vaults

"Vault" is one of the most overused terms in the cryptocurrency space. Broadly speaking, it usually refers to a "smart contract that holds assets." In practice, this label can be applied to various concepts, from passive wrappers to automated strategy contracts to credit pools.

For institutional readers, a vault is essentially an on-chain investment vehicle that provides exposure to a specific strategy. Investors deposit assets (usually stablecoins) and receive receipt tokens representing proportional ownership in the pool, similar to fund shares.

The key difference lies in the governance and execution mechanisms. Traditional investment vehicles are governed by legal documents and manager discretion, with rules enforced through contracts and regulatory frameworks. Vaults, on the other hand, are governed by parameters encoded in smart contracts and executed programmatically.

Given the increasing maturity of the tokenized asset industry and its growing service to institutional users, we believe it is more prudent to use more specific terminology. In this introductory guide, we will focus on a special type of vault: the allocation vault.

Allocation Vaults

An allocation vault is a smart contract-based allocation mechanism built on top of lending protocols. A risk manager (often referred to as a "curator" on DeFi platforms) is responsible for setting the strategy and parameters, deciding how deposited assets are deployed to various independent lending markets.

Note: The implementation of allocation vaults varies by protocol. This introductory guide primarily uses Morpho's architecture as an example, but the basic concepts are largely similar, with only slight differences in terminology.

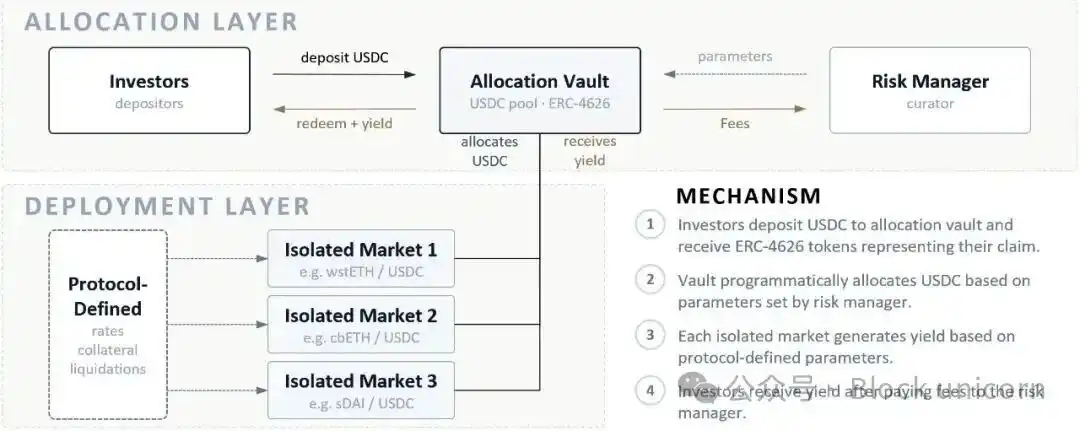

Figure 1: Allocation Vault Architecture and Yield Distribution

An allocation vault can be understood as a two-tier system. The bottom layer is the deployment layer, where yield is generated. The protocol defines how interest accrues in each independent market, eligible collateral, and liquidation methods.

The top layer is the allocation layer, where risk managers set parameters. The vault accepts a single loan asset (usually USDC) and deploys it to multiple independent markets in the deployment layer.

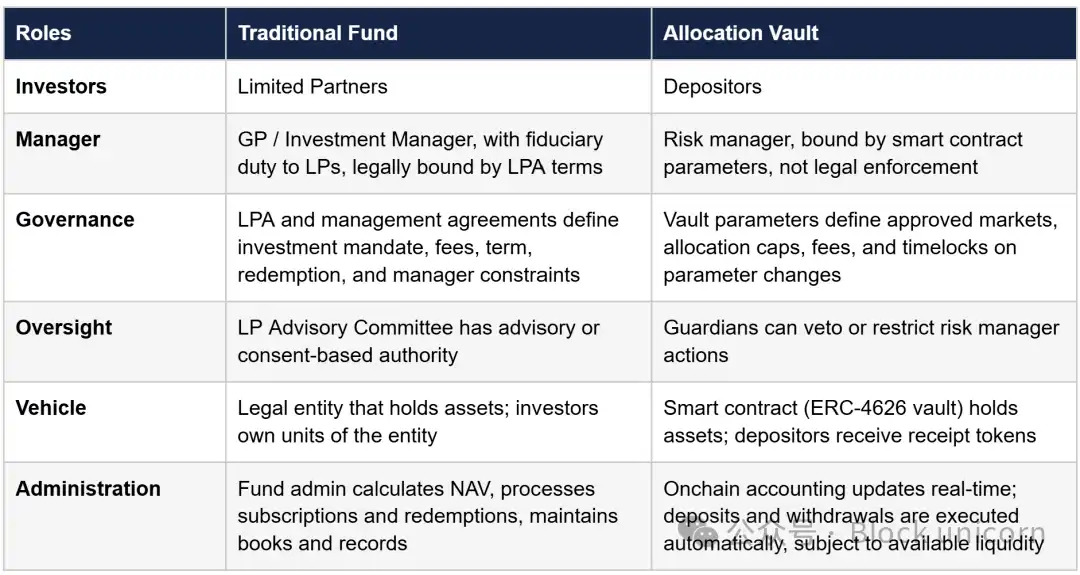

Fund vs. Allocation Vault

For institutional readers, a more straightforward way to understand is to directly compare traditional fund structures with allocation vaults. The table below outlines the roles of each and highlights the differences in execution mechanisms.

The most important takeaway from this comparison is that allocation vaults represent a fundamentally different trust model. Blockchain transforms part of the legal and contractual terms into software, changing the enforcement of rules from court-enforced to code-enforced. Risk managers are no longer bound by fiduciary duties or legal documents but are constrained by the scope of authorization in the smart contract. Execution is ex-ante rather than ex-post: any violation of policy will not be executed.

On-Chain Distribution Stack

This section describes the entire process of tokenized products from issuance to distribution. In this architecture, the role of the risk manager is more akin to the collateral department of a prime broker.

Traditional fund products follow a clear value chain. The fund manager executes the strategy, structurers package it, prime brokers provide leverage, the margin department determines collateral terms, and finally, wealth management platforms distribute the product to end investors.

On-chain products follow a similar process. The difference is that blockchain can compress settlement times, automate execution, and connect with platforms for product distribution.

Layer 1: Asset Issuer (Fund Manager)

It all starts here. The fund manager develops the investment strategy, issues assets, and manages the portfolio.

In traditional markets, distribution and financing rely heavily on relationships. Investors subscribe directly, and leverage (if any) requires a prime broker to accept the position as eligible collateral and operate on negotiated terms. For many private assets, this process is customized, time-consuming, and limited to investors with the right counterparties and balance sheet resources.

In on-chain markets, the issuer's responsibilities remain the same: execute the strategy. The difference lies downstream. Once the exposure is tokenized, it can be evaluated as collateral, financed in lending markets, and distributed through on-chain channels without the issuer having to build custom infrastructure for each counterparty.

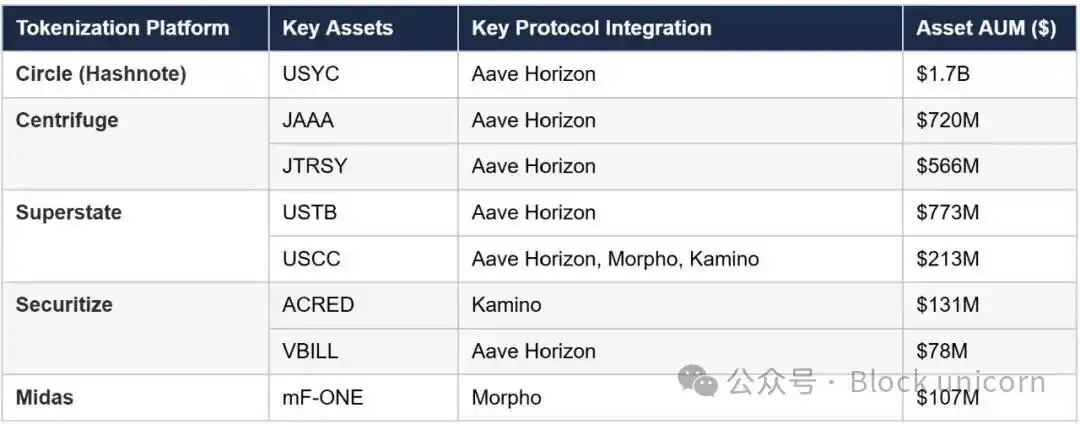

A list of fund managers who have actively integrated tokenized products into on-chain markets is shown in Chart A.

Chart A: Key Management Institutions with Enabled Protocol Integration

Layer 2: Tokenization Platform (Product Structurer)

When a fund needs to reach investors through specific channels, product structurers package it into a suitable product. For example, an investment bank might structure equity product into an ETF or structured note. Credit products might be packaged into CLOs or credit-linked notes. Structurers do not execute the strategy; they make it distributable.

Tokenization platforms function in the same way. They package the fund manager's strategy into tokens, which are standardized, chain-readable on-chain instruments. The key difference from traditional wrappers is their composability. Once tokenized, the asset can be integrated into DeFi protocols, used as collateral, programmatically allocated, and embedded into end-consumer portfolios and yield products.

A list of platforms that have actively integrated into tokenized DeFi markets is shown in Chart B.

Chart B: Key Tokenization Platforms with Enabled Protocol Integration

Layer 3: Lending Protocol (Prime Broker)

Prime brokerage consists of two parts: the platform that executes financing and liquidation, and the risk function that decides which collateral to accept and on what terms.

On-chain lending protocols provide the platform side. They are automated systems that execute lending, interest accrual, and liquidation based on predefined parameters. These protocols are generally asset-agnostic: they only enforce rules and do not make underwriting judgments.

Protocols rely on oracles, which are the on-chain counterparts of pricing agents, to obtain the value of the underlying assets and publish the information on-chain. This information is used to set loan-to-value (LTV) ratios and automatically execute liquidations.

The three most active lending protocols in the tokenized asset market are Aave Horizon, Morpho, and Kamino. Detailed profiles of each protocol are shown in Chart C.

Chart C: Key Lending Protocols with Enabled Tokenized Asset Collateral

Although lending protocols are the primary example of the deployment layer in this introductory guide, the architecture is not limited to lending. Any smart contract-driven vault, including yield aggregators, structured products, liquidity strategies, or other on-chain investment tools, can be paired with allocation vaults.

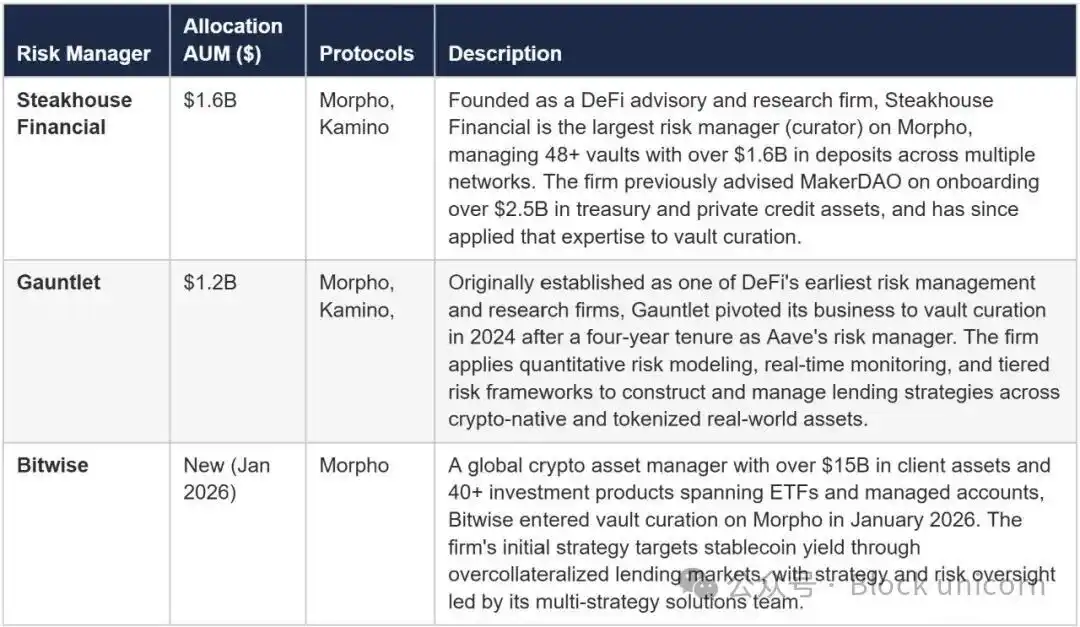

Layer 4: Risk Manager (Margin Department)

Within a prime broker, the margin department is responsible for evaluating collateral eligibility, setting collateral rates and concentration limits, and adjusting terms based on changing market conditions.

Risk managers perform the same function on-chain. They approve which tokenized assets can be used as collateral in their vaults, set risk parameters, and allocate stablecoin liquidity across the markets they underwrite. The protocol is responsible for execution; the risk manager is responsible for underwriting. If an asset is not underwritten by a risk manager with substantial liquidity, it cannot be financed at scale, even if it can be tokenized.

Leading risk management firms like Steakhouse Financial and Gauntlet operate across multiple lending protocols. Bitwise became the first major traditional asset management company to launch an allocation vault on Morpho in January 2026, marking the beginning of institutional crossover. Detailed profiles of various risk management institutions are shown in Chart D.

Chart D: Key Risk Management Institutions

Unlike Morpho and Kamino, Aave Horizon does not operate through an independent allocation layer. Eligible collateral, risk parameters, and allocation rules are defined at the protocol level by Aave Labs in coordination with risk management firms like Llama Risk, so the protocol itself assumes the risk function rather than delegating it to independent risk managers.

The extent to which risk managers operate under programmatic constraints also varies by platform type. On public open platforms like Morpho and Kamino, parameter changes are subject to timelocks and governance vetoes, ensuring that no single party can unilaterally alter vault behavior. In contrast, private or enterprise deployments can be built as permissioned systems where parameters can be adjusted by agreement between the deploying institution and its counterparties.

In addition to native lending platforms, there are vault infrastructure providers like Veda that manage significant capital in DeFi yield strategies. Their existing products are primarily focused on crypto-native assets, but many providers are actively exploring integration with tokenized assets, so they may become important channels for institutional asset management companies in the near future.

Layer 5: Distribution Platform (Wealth Platform)

Any financing market needs a funding base. In traditional markets, the capital used to finance margin loans and repo transactions comes from aggregated pools: money market funds, bank vaults, institutional cash management, and wealth platforms that intermediate retail and institutional deposits. End investors see only the yield, not the underlying collateral chain.

On-chain distribution platforms play the same role, aggregating stablecoin deposits and routing them to allocation vaults. Coinbase is the most obvious example. Its USDC lending product routes deposits through Steakhouse-allocated Morpho vaults on Base. The platform and vault infrastructure are abstracted away, and end users see only the yield product.

Many allocation vaults attract direct deposits, but integration with distribution platforms is a key scaling mechanism. In traditional asset management, distribution is the most difficult and costly problem. It requires placement agents, sales teams, investor relations, and often years of relationship building before a product reaches meaningful scale.

In the allocation vault model, distribution can be embedded into the system itself. Once an asset is accepted as collateral by widely used allocation vaults, integration with various distribution platforms becomes much easier.

This dynamic applies to Morpho and Kamino, but Aave is different: it is vertically integrated and can act as its own distribution channel. Major wallets like MetaMask and Bitget have directly integrated Aave to power stablecoin yield products. In November 2025, Aave launched a consumer savings app on the Apple App Store that runs on its lending protocol, targeting retail savers with no on-chain experience. Aave controls both the infrastructure and distribution, while Morpho and Kamino are composable infrastructures for others to build on, with no single entity owning the full tech stack.

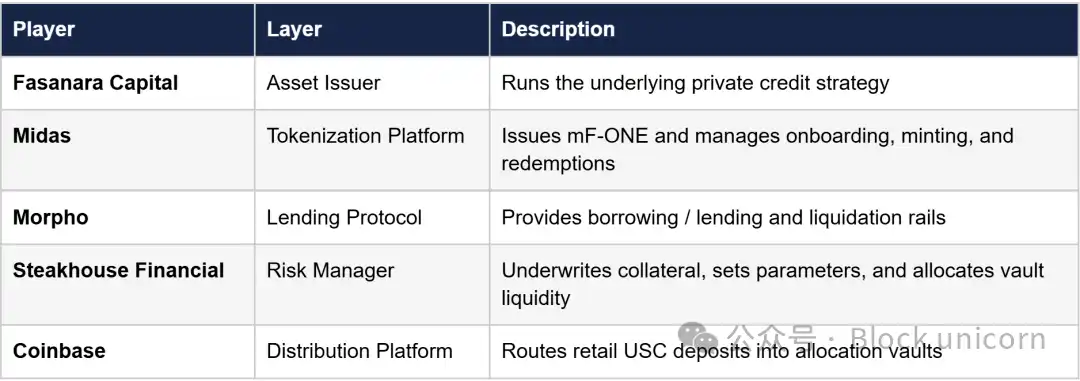

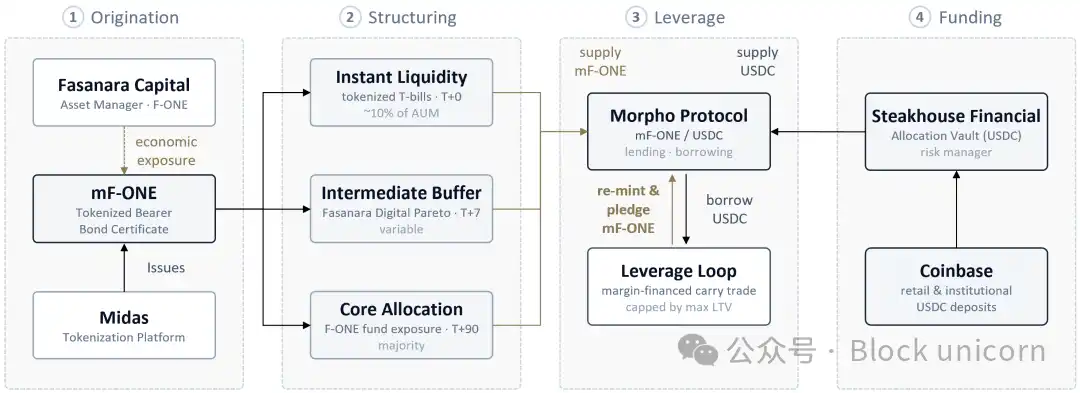

Case Study: Fasanara and Midas's mF-ONE

Background

In 2025, London-based, FCA-regulated private credit manager Fasanara Capital, with over $5 billion in assets under management, partnered with German-registered tokenization platform Midas to bring its flagship strategy F-ONE on-chain, named mF-ONE. The product launched on Morpho with Steakhouse Financial as the risk manager and quickly scaled to over $160 million within months, becoming one of the largest tokenized collateral markets on the protocol.

mF-ONE is a valuable case study because it demonstrates what "successful tokenization" truly requires. Simply putting a fund on-chain is not enough to unlock new capital. A tokenized product may exist but remain unusable in on-chain capital markets. mF-ONE was able to scale because it was designed to be financed, liquidated, and distributed within DeFi rails.

Problem: Structural Mismatch

Tokenized treasuries work naturally on-chain because their underlying instruments are liquid and settle quickly. Private credit is different. Fasanara's F-ONE fund operates with traditional liquidity terms: monthly subscriptions, quarterly redemptions.

This directly creates a mismatch with on-chain lending markets:

-

Lenders expect instant liquidity. They provide USDC with the expectation of being able to withdraw based on available liquidity, not a 90-day redemption cycle.

-

Liquidation requires an exit path. If collateral is seized, liquidators need to be confident they can convert it to stablecoins under stress, not hold an illiquid position and wait for a redemption window.

-

Transfer restrictions break composability. Directly holding fund interests often comes with regulatory friction: manager approval, KYC, transfer restrictions, etc., which prevent tokens from flowing freely between smart contracts and counterparties.

Solution: Legal Structuring and Liquidity Engineering

Legal Architecture for Composability

mF-ONE does not represent direct ownership of F-ONE fund shares. Instead, it is a bearer bond certificate issued by Midas, giving the holder contractual beneficial rights to F-ONE exposure through a bankruptcy-remote structure.

In practice, this serves two critical functions for DeFi markets:

-

Permissioned Issuance, Transferable Collateral. Token minting can have KYC gates, while secondary trading remains permissionless for use as collateral, so tokens can flow freely between wallets/contracts and be seized in liquidation without authorization.

-

Resolvable Fallback. In stress scenarios, the structure is designed to be unwound, allowing sale or settlement through traditional channels, providing an underwritable exit path for liquidators and risk managers.

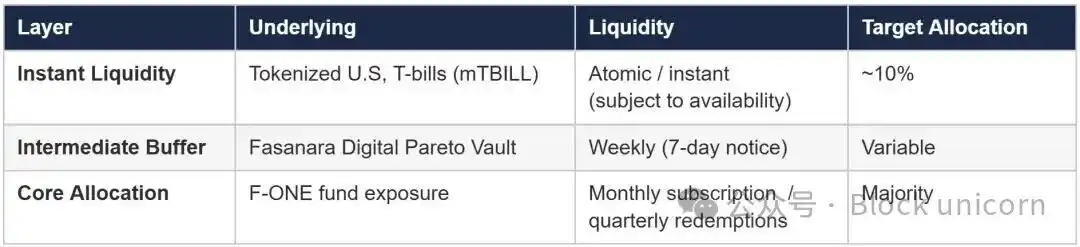

Liquidity Engineering as a Core Product Feature

Even with a composable instrument, collateral still needs reliable liquidity. mF-ONE addresses this with a three-tier capital structure, progressively layering liquidity into the product.

Instant Liquidity Arbitrage is the key innovation. This tranche targets ~10% of AUM, allowing holders to instantly redeem mF-ONE for USDC (subject to available liquidity) for a redemption fee that compensates remaining holders for cash drag. Effectively, it transforms a quarterly redeemable credit fund into an instrument that can operate in a real-time settlement market.

The middle buffer layer addresses a second practical timing issue: new subscription funds would otherwise sit idle until the next subscription window. This buffer keeps capital working while maintaining faster liquidity than the core fund.

Capital Flows: From Subscription to Leverage

Figure 2: Simplified mF-ONE End-to-End Flowchart

The on-chain distribution mechanism described in the previous sections maps directly to mF-ONE's distribution strategy.

-

Origination: Accredited investors complete Midas's onboarding, deposit USDC, and receive mF-ONE. mF-ONE represents a tokenized bearer certificate granting economic exposure to the Fasanara F-ONE fund.

-

Structuring. Capital is allocated across a portfolio constructed by Fasanara, Midas, and Steakhouse Financial to minimize cash drag and provide ample liquidity.

-

Leverage. Investors deposit mF-ONE as collateral into Morpho's mF-ONE/USDC market and borrow USDC supplied by Steakhouse's allocation vault. Investors can repeat this up to LTV thresholds. As long as asset yield exceeds borrowing cost, yield is amplified.

-

Funding & Distribution. Coinbase's USDC Lend product routes retail deposits directly to Steakhouse-managed Morpho vaults on Base. Coinbase users clicking "Lend" in the app see only the yield, not the underlying collateral chain. In the background, part of that yield is generated by interest paid by borrowers collateralized with assets like mF-ONE.

Stress Test Scenario

When a borrower's position in the mF-ONE lending market becomes undercollateralized due to net asset value (NAV) markdowns, Morpho's liquidation mechanism is triggered. Unlike traditional repo, where collateral can typically be seized and sold immediately, private credit assets are not "saleable on demand."

To compensate for this, Fasanara, Midas, and Steakhouse Financial designed for liquidators to purchase mF-ONE collateral at a significant discount to the last published NAV, creating enough expected return to compensate for the time and operational steps required to exit.

Once liquidators acquire the collateral, they can access liquidity through three paths:

Path 1: Atomic Redemption (Fastest). A portion of mF-ONE is allocated to a liquidity arbitrage invested in tokenized U.S. treasuries, redeemable atomically on-chain. This path is best for small positions and routine churn, not large-scale stress.

Path 2: Secondary Market Sale (Medium). mF-ONE tokens can be broken down into the underlying private credit notes and sold to off-chain institutional buyers who cannot custody tokenized instruments. This expands the buyer base beyond on-chain participants. Buyers can choose to hold the notes or redeem directly with Fasanara via standard redemption processes.

Path 3: Standard Fund Redemption (Slowest, Most Reliable). As a backstop, liquidators can hold the collateral and submit a standard redemption request to the fund, receiving cash at NAV within 90 days. Since the collateral was purchased at a discount, the expected return over that period remains attractive.

These paths form a liquidity waterfall analogous to structured credit. The key due diligence question is off-chain execution: are the secondary market and broken-note sales processes deep enough, operationally robust, and free of conflicts to function in a stress environment.

Key Takeaways

The mF-ONE case shows that successful tokenization of a private credit fund requires solving four interconnected problems simultaneously.

-

Structure the token for composability. Use legal wrappers that enable permissionless secondary market transfer so the token can be used as collateral, seized in liquidation, and moved between participants without issuer involvement. Build a two-track redemption path so liquidators have a backstop they can underwrite.

-

Build liquidity engineering into the structure itself. Don't rely on external market makers or secondary trading to solve liquidity post-issuance. Build a multi-tier capital structure with an instant liquidity layer backed by atomically redeemable assets, ensuring the token's liquidity meets the real-time settlement expectations of lending protocols from day one.

-

Partner with a reputable risk manager. Without a risk manager willing to accept your token as collateral and allocate stablecoin liquidity, you cannot fund a lending market. This leverage loop generates self-reinforcing demand that no standalone tokenized fund can achieve. Partnering with a risk manager is a core part of the go-to-market strategy.

-

Design for distribution infrastructure. Allocation vaults are not just a risk layer; they are a distribution channel. By integrating with distribution platforms, vaults can access liquidity at a scale no single asset manager could achieve independently.

-

Pre-engineer stress test scenarios. For tokenized private credit, liquidation discounts, the sequence of exit options, and access to off-chain secondary buyers must be set and tested before issuance. The exit path must be designed so liquidators can participate.

Considerations for Institutional Asset Managers

Before designing a tokenized product for the allocation vault ecosystem, institutional asset management companies should reach consensus on a series of strategic, regulatory, and operational issues. This section is not an exhaustive due diligence checklist but a starting point for early discussions with legal counsel, compliance, and product leads.

Strategic Considerations

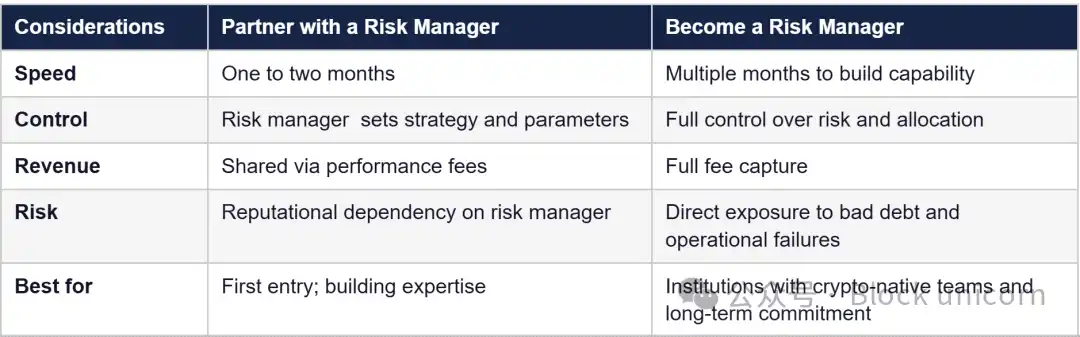

There are two paths into the allocation vault ecosystem:

-

The first is to tokenize your fund and partner with an established risk management firm that will build the integration, design the risk parameters, allocate liquidity, and provide access to its existing depositors and distribution partners.

-

The second is to build or acquire risk management capabilities to deploy and manage your own allocation vaults. Bitwise Asset Management became the first major traditional asset manager to launch an allocation vault on Morpho in January 2026, marking the beginning of this institutional crossover.

For most institutions, the pragmatic approach is to gain experience first as a partner before evaluating the possibility of self-management. This is similar to how traditional asset managers typically enter new markets: partner with external managers first, learn the mechanics, and then bring the capabilities in-house once the strategy is proven.

Regulatory Considerations

Security Classification. Under the Howey Test, vault tokens exhibit characteristics of investment contracts. Pooling of funds, expectation of profit, active risk management. Assess whether your product triggers securities registration requirements and whether the Investment Company Act or Investment Advisers Act applies to your structure.

KYC/AML and Gating Mechanisms. Compliance infrastructure for permissionless systems exists. Evaluate which permissioning model aligns with your regulatory obligations.

Risk Manager Liability. No court has yet tested the fiduciary duties of risk managers, but their function is highly analogous to investment management. Risk managers have discretion over asset allocation, charge fees, and depositors rely on their expertise. Build governance infrastructure (e.g., timelocks, guardian vetoes, transparent reporting) and assume regulatory frameworks will eventually impose trustee-like obligations.

Jurisdiction. Under MiCA, if a vault has an identifiable risk manager making management decisions, it likely does not qualify for the "fully decentralized" exemption and requires CASP registration. In the U.S., a risk manager exercising discretionary allocation decisions over a pool may trigger investment adviser registration under the Investment Advisers Act.

Operational Considerations

Oracle and Valuation Risk. For tokenized asset vaults, the oracle is the most critical single point of failure. Stale or inaccurate price feeds can trigger improper liquidations or create bad debt. Understand who controls the price feed and what safeguards exist.

Key and Upgrade Controls. Audit the full permission structure: who holds admin keys, what timelocks prevent unilateral parameter changes, and what is truly immutable vs. upgradeable.

24/7 Operational Resilience. There is no market close. Liquidations, oracle updates, and stress events happen around the clock. Assess if your ops team has capacity for continuous monitoring or if you need to find a partner.

Smart Contract Risk. Immutable code means no bug fixes post-deployment. Determine your risk tolerance early.

Accounting and Tax Considerations

The accounting and tax treatment of DeFi vault participation remains unsettled. FASB ASU 2023-08 provided fair value measurement guidance for certain crypto assets, and the repeal of SAB 121 removed the requirement to record safeguarded crypto assets as a balance sheet liability.

Beyond these developments, there is currently no specific guidance on the classification of vault shares or whether depositing funds into a vault constitutes a taxable event. Consult specialized digital asset accounting and tax advisors before deploying capital.

Conclusion

Tokenized assets have reached an allocation inflection point. The question is no longer which assets can be tokenized, or even how to tokenize them. It is how to structure products for compatibility with DeFi infrastructure and distribution to on-chain investors. RWA.xyz believes allocation vaults will play a central role in shaping this evolution, and 2026 will mark an acceleration of TradFi-DeFi convergence.

The mF-ONE case study shows a proven path, but it is not the only model. We anticipate a spectrum of approaches aimed at solving the same fundamental problem: structuring tokenized assets for integration with existing on-chain infrastructure and access to the capital already sitting within it.

As these frameworks mature, first-mover advantages will widen. Institutions building DeFi expertise, risk management relationships, and distribution track records today are building moats that will be difficult to replicate when the broader wave arrives. We hope this primer serves as a springboard for the next generation of institutional asset managers who will explore and ultimately upgrade our financial infrastructure.

This is not the end of institutional tokenization, nor even the beginning of the end. But it is, perhaps, the end of the beginning. RWA.xyz remains committed to partnering with institutional asset managers to support the vision of building a truly open and interoperable financial system.