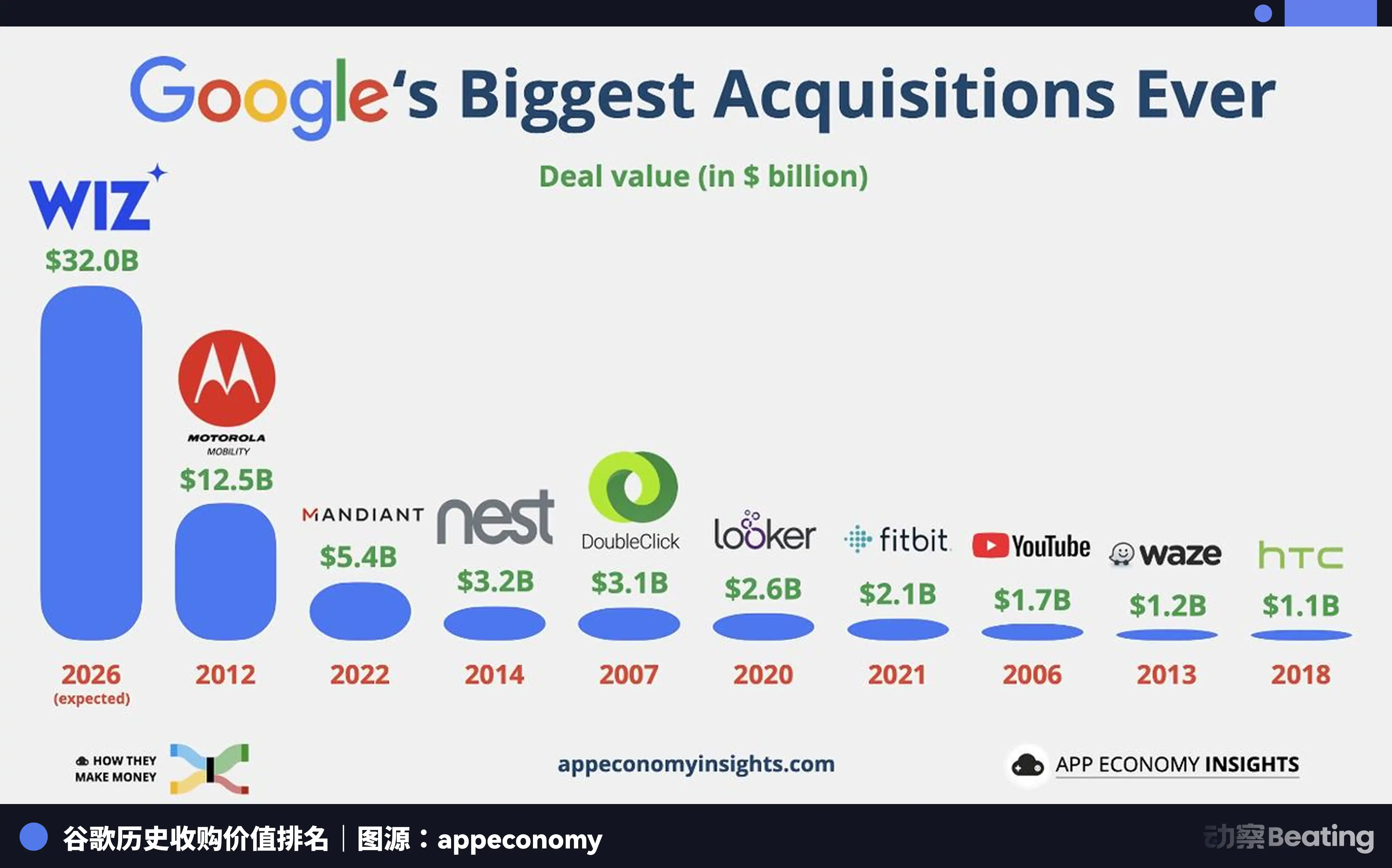

The cloud war is incredibly expensive. This is Google's largest acquisition ever.

Last week, Google officially completed the acquisition of cloud security company Wiz for $32 billion. This surpasses Google's 2012 acquisition of Motorola Mobility for $12.5 billion and also becomes the highest-value exit in Israeli high-tech history.

A Deal That Doesn't Seem to Make Financial Sense

From any traditional financial model perspective, this deal seems somewhat outrageous.

Wiz was founded in 2020. Initially just an ordinary cybersecurity startup, it quickly pivoted a year later to focus on providing a cloud security platform for large enterprises. By the time of acquisition, its annual revenue was approximately $700 million. Yet Google paid $32 billion for it.

This means the Price-to-Sales (P/S) ratio for this deal exceeds 45x. In comparison, already public and mature security companies like CrowdStrike and Palo Alto Networks typically have P/S ratios of only 15 to 25x. Google paid nearly double the premium.

Independent analyst Frank Wang once calculated: even if Wiz grows to the size of CrowdStrike and Palo Alto Networks in the coming years, the combined revenue would only be between $10 billion and $12 billion.

From a purely financial return standpoint, this looks like an extremely "unprofitable" deal.

Why did Google make this decision? To answer this, we must first understand the path Google has traveled in the cloud computing race.

Google's role in the cloud computing race has always been somewhat微妙. It was one of the earliest pioneers, yet also the last major player to commercialize. For a long time, Google Cloud resembled a technology lab more than a true commercial product. But it was in this lab that Google created many technologies that later became industry standards.

The most typical example is Kubernetes. Google internally had a system for managing massive server containers, codenamed Borg. It was later transformed into an open-source project, becoming Kubernetes (K8s), which now dominates the cloud-native world. This move almost changed the entire technological landscape of the cloud computing industry—AWS and Azure eventually had to fully support K8s.

Google didn't make money earliest in the cloud war, but it set many of the rules.

Even before the AI wave arrived, Google began preparing for the next round of competition by developing specialized chips for machine learning computation: TPUs (Tensor Processing Units). Compared to general-purpose GPUs, TPUs offer higher energy efficiency in large-scale AI training. The training of AlphaGo and later the inference of Gemini largely ran on this architecture. This gave Google Cloud a unique card to play in the field of AI computation.

But technological advantage doesn't automatically translate into market share. Google gradually realized that cloud services are not just about technology; they are also an art of sales.

The change happened after Thomas Kurian took over. This executive, who spent 22 years at Oracle, was poached by Google to become CEO of Google Cloud. The first thing he did was rapidly expand the sales team, splitting out vertical industries like finance, retail, healthcare, and manufacturing for separate operation. The old Google-style approach of "engineer culture主导, let customers figure out the documentation themselves" was gradually rewritten.

In 2023, Google Cloud finally achieved quarterly profitability for the first time.

It was at this juncture that a company came into their view. This company was called Wiz.

One of the Fastest-Growing Software Companies in History

Even in Silicon Valley, few companies have grown as fast as Wiz.

Within 18 months of its founding, its Annual Recurring Revenue (ARR) broke $100 million. This pace is almost unprecedented in SaaS history; Slack took about 3 years, Shopify took nearly 5 years, while Wiz did it in a year and a half.

In the following years, its growth was almost exponential. ARR quickly surged to $500 million, then approached $1 billion. More importantly was its customer quality; nearly half of the Fortune 100 companies were using Wiz's product. BMW, Morgan Stanley, Salesforce were赫然在列.

The four founders of Wiz, Assaf Rappaport, Ami Luttwak, Roy Reznik, and Yinon Costica, have a rather legendary background. They initially served in the Israeli Defense Forces' famous intelligence Unit 8200, an elite unit equivalent to the US NSA or UK GCHQ. Founders of many top global security companies like Check Point, Palo Alto Networks, and Armis hail from here.

But this wasn't their first startup. In 2012, they founded cloud security company Adallom, which was acquired by Microsoft for $320 million three years later. After the acquisition, Rappaport even directly became the head of Microsoft's Israel R&D center, managing thousands of engineers. But they didn't stay at Microsoft long; in March 2020, they left collectively, taking some of the old team with them, and started anew. This time, the goal was bigger.

In the summer of 2024, Silicon Valley temperatures were high, and the AI创业潮 was at its most疯狂 stage. Wiz had just raised a $1 billion Series E round in May of that year, with extremely ample cash reserves, not short of money at all. It was at this time that Google extended an olive branch to Wiz.

Actually, as early as March that year, Google CEO Sundar Pichai had personally emailed Rappaport expressing acquisition interest. But Rappaport didn't see it until May when they formally met at Google headquarters.

Google immediately offered $23 billion.

In Silicon Valley at the time, this was an astronomical figure, enough to make most startup founders instantly financially free. The外界普遍认为 this was a done deal.

But Wiz refused.

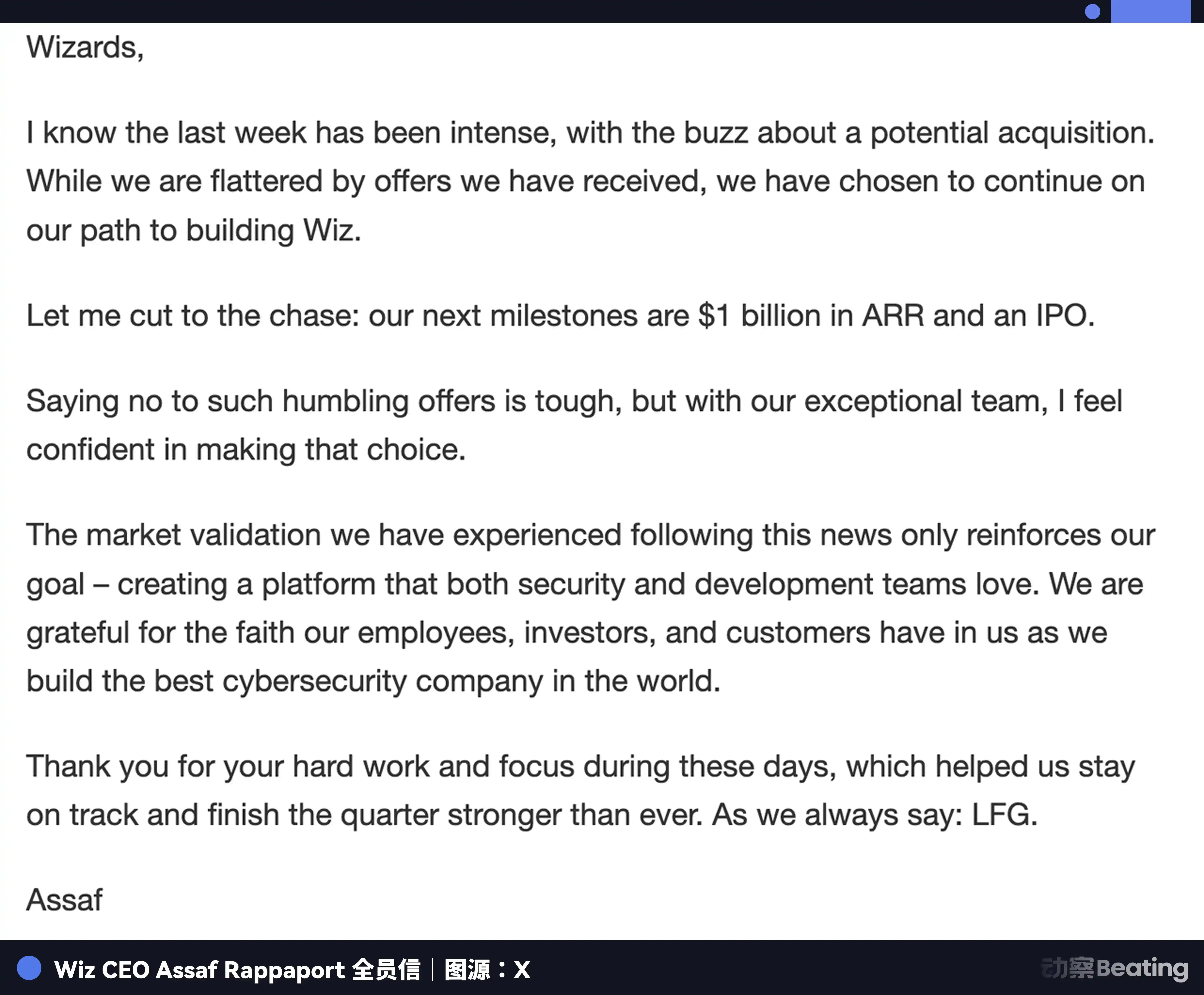

"I know the past week has been very tense, with constant rumors about a potential acquisition. Although we are flattered by the offer we received, we have chosen to continue on the path of building Wiz," Wiz CEO Assaf Rappaport said in an email to all employees, stating Wiz's next milestone was $1 billion in annualized revenue and an IPO.

He later recalled at the TechCrunch Disrupt conference: "That was probably the toughest decision of my life."

At that time, Wiz's annualized revenue was approaching $1 billion, and its growth rate showed almost no signs of slowing down. "The fastest-growing software startup in history" was Wiz's shiniest label and one of the media's favorite titles to引用.

Before being fully acquired by Google, Wiz was still in a typical high-growth, high-investment phase. As a company aiming for an IPO, it invested the vast majority of its revenue and financing (cumulatively about $1.9 billion raised) into R&D, global sales network expansion, and acquisitions of smaller companies like Gem Security. In Q2 2024, the overall market size was about $700 million, and Wiz's year-over-year growth rate was a high 94%. In comparison, competitors Palo Alto Networks had an ARR of about $8 billion (20% growth), and CrowdStrike had an ARR of about $2.6 billion (49% growth).

Although Wiz was still smaller in size, its growth rate was clearly not in the same league. The capital market普遍认为 that once this company went public, its valuation could easily exceed $50 billion.

Google didn't go far, closely watching Wiz's growth curve from the background. In just half a year, Wiz pushed its ARR from $350 million to $500 million and successfully locked in nearly half of the Fortune 100 enterprise customers.

If they didn't act now, the next price would only be higher, or it might not be available at all.

Google, Why Was Wiz or Nothing?

Most billion-dollar acquisitions typically use a mix of stock and cash. For example, when Meta (then Facebook) acquired WhatsApp for $19 billion in 2014, only $4 billion was cash, the rest was stock; Google's 2012 acquisition of Motorola was also partly cash.

Before acquiring Wiz, Google's cash flow was approximately $110 billion. This $32 billion deal unusually adopted an all-cash model. Wiz took nearly 30% of Google's cash reserves.

Furthermore, the most common practice after large tech company acquisitions is "Rebranding" and "organizational restructuring." But Google gave Wiz extremely high autonomy. Wiz did not need to change its name and could operate as independently as possible. In Google's history, only YouTube and early Android enjoyed similar long-term preferential treatment. Google承诺 that Wiz's approximately 1,800 employees would maintain an independent team structure and even have independent offices.

They say at the negotiating table, whoever is more anxious gives more privileges.

To understand why Google was willing to pay $32 billion for Wiz, besides the aforementioned "Wiz is one of the fastest-growing software companies in history," we must also zoom the lens out a bit further to look at the entire CNAPP (Cloud-Native Application Protection Platform) industry.

Before Wiz was acquired, the cloud security market was at a微妙 turning point. The entire market could be roughly divided into three forces.

The first force comes from traditional security giants, let's call them the "Old Kings." The two most typical are Palo Alto Networks and CrowdStrike. They rose during the traditional network security era and gradually pieced together a huge security platform through years of acquisitions—Palo Alto acquired Twistlock, Bridgecrew, and others, integrating分散的安全工具 into Prisma Cloud. This model is like a giant aircraft carrier, extremely comprehensive, with endpoint security, network firewalls, cloud scanning, vulnerability management, all in one. But it also has an obvious drawback: it's too heavy. Deployment is complex, the system is庞大, upgrades are slow. In a rapidly changing environment like cloud computing, a "heavyweight architecture" is somewhat笨拙.

The second force is represented by新一代云安全公司 like Wiz. Wiz, Orca Security belong to this category. Their core idea is: cloud security shouldn't be as complex as traditional security. Before Wiz appeared, most cloud security products required installing an "Agent," a small monitoring program, on every virtual machine. If an enterprise had tens of thousands of servers, it meant installing tens of thousands of Agents, a deployment process that could take weeks or even months. Wiz did something very bold: eliminate the Agent. This Agentless technology brought an极其巨大的 experience difference, reducing deployment from weeks to minutes.

The third force is the cloud providers themselves. AWS, Microsoft Azure, Google Cloud all have their own security tools. These products have a natural advantage: they come built-in with the cloud platform; enterprises often turn on security features顺手 when using cloud services. But they have a structural weakness: they can only manage their own turf well, with extremely limited cross-cloud capabilities.

With so many choices on the market, why didn't Google acquire Wiz's competitors, like Palo Alto Networks or CrowdStrike?

Size is a big reason. Palo Alto's市值长期稳定 around $100 billion to $120 billion around 2025, and CrowdStrike, after experiencing a widespread outage风波 in 2024, also quickly rebounded to over $60 billion.

This size is rather difficult for Google to swallow.

Another key issue is "asset purity." Palo Alto Networks follows a platform integration route, with lots of firewall and traditional network security business. CrowdStrike's core阵地 is endpoint security, also carrying significant baggage.

Whereas every line of Wiz's code was written for the cloud environment, perfectly契合 Google Cloud's needs. Google doesn't need to prune outdated hardware businesses; it can directly inject Wiz's agentless scanning capability into GCP's底层. This is what Google truly wanted: a clean, native tool that could be directly embedded into its strategic skeleton.

This means Google Cloud's services can be sold better.

Nowadays, within enterprises, the person making the cloud service purchasing decision is no longer the IT department, but the Chief Information Security Officer (CISO) responsible for security. This has led to a change in the purchasing path and logic:

Initially, enterprises first chose a cloud platform, then configured security tools. But now, security has become a prerequisite for cloud selection, so enterprises first assess security, then choose a cloud platform.

As security partners for nearly 50% of Fortune 100 companies, these CISOs are already old acquaintances of Wiz. This can greatly help Google expand its sales channels; it's a very short sales path. In enterprise cloud procurement, deals often worth tens of millions of dollars with decision cycles lasting years, this path advantage is extremely valuable.

So from another perspective, what Google is really buying is not Wiz's current profit or market value, but its庞大的 enterprise customer base behind it, and the growth inertia of this rapidly growing company. If Wiz maintains a growth rate close to 100%, its revenue scale could approach $2 billion in two years—and once these customers migrate to the Google Cloud ecosystem with Wiz, the synergistic benefits will far exceed that.

Looking back then, $32 billion might not seem so expensive.

Simultaneously, in today's era, the proliferation of AI is fundamentally changing the complexity of enterprise cloud environments. Although there are voices in the market suggesting that AI development will impact the growth logic of traditional software and cloud service companies, Google's acquisition, through action, provides the answer: AI's expansion has not weakened the value of cloud security; instead, it is rapidly放大 its necessity.

Model training data resides in the cloud, AI Agents automatically call various APIs in the cloud, data flow between different clouds is becoming increasingly frequent, and the attack surface is expanding exponentially. The previous cloud environment was relatively static with a clear structure; the current cloud environment has become extremely dynamic due to AI, with blurred boundaries.

Therefore, products that can uniformly manage the security posture of all clouds will change from "optional" to "mandatory" in the coming years.

Wiz's product design naturally fits such multi-cloud, hybrid cloud complex environments. And this $32 billion acquisition is essentially Google securing the best entry ticket提前 before the incremental market matures.

After a series of regulatory lobbying tug-of-war, on March 11, 2026, the acquisition was officially completed. Approximately 2,700 Wiz employees merged into the Google Cloud system. Index Ventures profited about $3.8 billion, Sequoia Capital about $3.2 billion, Insight Partners about $2.9 billion, the total value of employee-held equity is about $3 billion, and Google additionally承诺 $1.5 billion in retention incentives.

"We Reward Risk"

In 2004, Google founders Larry Page and Sergey Brin's first sentence in their pre-IPO "Founders' IPO Letter" became Google's underlying operating logic for over twenty years: "Google is not a conventional company. We do not intend to become one... We will not shy away from high-risk, high-reward projects because of short-term earnings pressure."

As a continuation of this基因, their successor Sundar Pichai, in a 2023 interview, was asked: "How do you reconcile a giant organization like Google/Alphabet, with so many stakeholders you must be responsible to, while maintaining that innovative spirit without becoming overly cautious?"

The背景 then was that ChatGPT had just sparked the AI frenzy, and Google was facing fierce criticism for being "slow to react, hesitant to take risks due to giant company包袱."

Sundar Pichai's answer at the time, three years later, seems to have become the best annotation for this $32 billion acquisition. He believed that the driving force of innovation stems from rewarding risk, even if the results are not immediately apparent: "I encourage people, I promote people, because I know they took a risk, did their best, made a smart decision."

Indeed, the challenges facing this transaction are more complex than the financial premium and harder to quantify.

The real challenge Google faces is more隐蔽 than the financial premium and even harder to quantify. Those who have watched "Succession" probably have a sense that large acquisitions are often not just about asset transfer, but also an identity crisis. And this time, this crisis has a very specific source: Wiz is an Israeli company.

In Israeli startup culture, there is a word that's hard to translate: Chutzpah.

This word roughly implies a混合气质: bold, direct, even带有一点傲慢, with not too much reverence for authority and rules.

In many Israeli tech companies, junior engineers can directly interrupt the CEO's speech to point out mistakes. Conference room debates are激烈, voices are loud, but after arguing, everyone still drinks coffee together as if nothing happened. This culture is very efficient in the startup phase.

But when it encounters the organizational systems of large US tech companies, friction is almost inevitable. Big companies emphasize consensus, process, and emotional management more. When expressing differing opinions, one must often be委婉, restrained, and consider everyone's feelings. Thus, the two cultures can easily create a错位. Google employees might find the Israeli team too direct, even somewhat咄咄逼人; while Wiz engineers might find the big company's discussion style too迂回 and inefficient.

Historically, there are countless cases of core teams leaving and products becoming平庸 after being acquired by large companies. Google offered generous retention incentives, but money can retain people, not necessarily the entrepreneurial spirit.

Besides cultural issues, there is another more微妙 challenge. Wiz's neutrality.

Before being acquired, Wiz could simultaneously serve enterprise customers on AWS, Azure, and Google Cloud precisely because of its independent identity.

It didn't belong to any cloud provider, had no baggage of立场, so enterprises felt safe letting it scan their entire cloud environment's security status. But the moment Wiz puts on the Google jersey, this relationship becomes微妙.

If you are an enterprise with core business deployed on AWS, are you willing to let a product旗下的 by Google scan all your security vulnerabilities? This concern won't erupt overnight, but it will悄悄渗透 into the most细微 operating metrics: customer renewal rates, contract cycles, new customer acquisition speed.

Wiz and $32 Billion in Cash, Which is More Important?

Before the acquisition happened, besides Google, there were actually industry rumors that Amazon had also expressed acquisition interest in Wiz. Also rejected.

Some also speculated that作为 Wiz founding team's "old employer," Microsoft might have internally seriously assessed the possibility of bringing this team back under its wing.

In other words, Google wasn't the only one who wanted this card. This is where the deal is truly微妙.

On the surface, Google spent $32 billion to buy a company with only $700 million in annual revenue. But from another angle, what Google bought is not Wiz itself. It bought a kind of模糊的确定性.

$32 billion in cash is not致命 for a company like Google.

Think of it this way: if Wiz ultimately fell into the hands of Microsoft or Amazon, the situation would be completely different. A security platform with cross-cloud global visibility, once held by a competitor, would mean Google loses this trump card and also has to face this card being played against itself.

So if you ask Google: Wiz and $32 billion, which is more important?

The answer might be: For Google, neither is that important. But ensuring Wiz does not fall into the hands of Microsoft or Amazon is very important to Google.

This deal may not guarantee Google's absolute victory in the cloud war. But at least, it makes it very hard for Google to lose.